Distribution is king: Robinhood is eating the prediction market

- Core Thesis: By integrating event contracts (prediction markets) into its multi-asset trading platform, Robinhood has built a formidable distribution moat. This cross-selling strategy is not only generating over $400 million in annualized revenue but also gives it a significant competitive advantage over standalone platforms like Kalshi and Polymarket, with the potential to capture further value through its own clearing entity, Rothera.

- Key Elements:

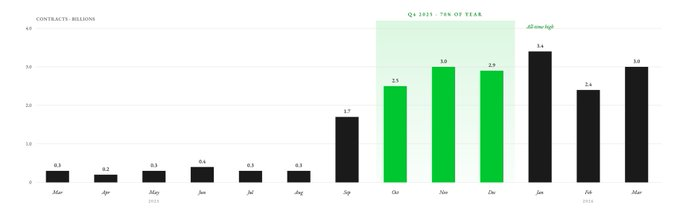

- In nine months, Robinhood's prediction market business traded 12 billion contracts, booked 8.8 billion in Q1 2026 alone, with an annualized revenue exceeding $415 million.

- By integrating Kalshi's contracts and distributing them to its 27.4 million funded accounts, Robinhood contributed 50% of Kalshi's first-year trading volume, demonstrating immense distribution power.

- Robinhood is embedding event contracts into asset pages like stocks and cryptocurrencies, enabling users to execute cross-asset hedging on a single screen, transforming from a passive broker into an information pricing platform.

- Through its joint venture Rothera, Robinhood has acquired a CFTC-licensed clearinghouse, allowing it to self-list any event contract in the future and potentially double its economic capture.

- Regulatory risk poses an existential threat to Kalshi and Polymarket, with over 60% of their revenue coming from sports contracts; Robinhood can mitigate this risk by diversifying across asset classes.

- Model projections indicate that even in a bearish scenario, Robinhood's prediction market business could be worth $12 billion by 2028, far exceeding Kalshi's current valuation.

- Integrating prediction markets into a retail brokerage not only serves existing traders but also acts as an information pricing tool for all other users—an advantage standalone platforms find difficult to replicate.

Original author: @Decentralisedco

Original compilation: AididiaoJP, Foresight News

In a previous article, we explored how HIP-4 brings structured products to Hyperliquid. Robinhood has made a similar move by recently venturing into prediction markets; the table below provides some context.

Fidelity, Schwab, and Interactive Brokers grew up in an era before prediction markets existed. Even spot cryptocurrencies account for only a small fraction of their overall product offerings. In contrast, Robinhood serves a younger demographic who might want to bet on sporting events, go long on semiconductor stocks, actively trade Solana, while holding crude oil positions in the futures market. A generation of users raised on "watching the situation" will flock to platforms like Polymarket or Kalshi if Robinhood fails to offer the same risk assets.

One way to mitigate this risk is to offer event contracts. These are binary instruments that settle on a "Yes" or "No" outcome. Each contract is priced between $0 and $1, reflecting the market's real-time probability of an event occurring. If you're right, the contract settles at $1; if wrong, it settles at $0. The user's entry cost is the probability of the event. For example, a $0.60 contract on the Strait of Hormuz being open by May 30th signals the market's belief. If most people are convinced something will happen, there's little room for profit from that event.

On Robinhood, these tools can serve as hedges. You could go long on the Strait of Hormuz being open while going long on crude oil, assuming that if the strait isn't open, oil prices will remain high.

Robinhood first launched its prediction market business in March 2025, routing customers through KalshiEX. In nine months, users traded 12 billion contracts. About 70% of that full-year volume was concentrated in the fourth quarter. In Q1 2026, Robinhood already recorded 8.8 billion event contracts.

Over 1 million Robinhood customers traded event contracts in 2025. Instead of launching these markets and building liquidity itself, Robinhood directly integrated Kalshi's prediction markets. Robinhood acts as a distribution layer by providing a dashboard for its customers. The entire infrastructure, at least for now, is still supported by Kalshi (more details later).

Kalshi and Polymarket dominate the market, accounting for over 90% of total prediction market volume. Robinhood distributes Kalshi's contracts to its 27.4 million funded customers who invest across multiple asset classes, including stocks, cryptocurrencies, futures, and options. Kalshi is merely a prediction market platform and cannot match this distribution capability.

In fact, Robinhood contributed 50% of Kalshi's trading volume in its first year.

While Coinbase allows users to trade stocks, cryptocurrencies, futures, and options (via the Deribit acquisition), it only launched its prediction market this January. In contrast, Robinhood's prediction market business has been operating for over a year, already generating over $415 million in annualized revenue. Robinhood also has significantly more monthly active users than Coinbase, with 13.5 million compared to Coinbase's 9.2 million.

Prediction markets can evolve further on Robinhood. Currently, they exist as a separate Hub within the app, disconnected from the rest of the platform. But soon, they could be cross-linked with assets like stocks, options, and cryptocurrencies – meaning Robinhood's stock traders could also directly purchase prediction market event contracts.

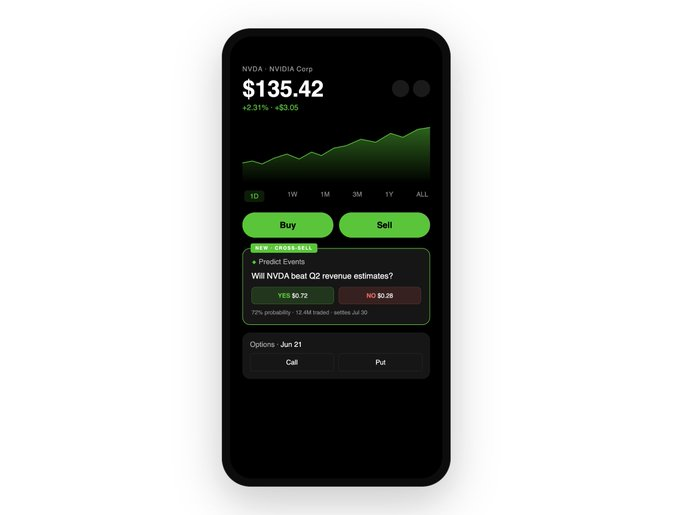

Imagine opening Nvidia's stock page before its earnings report. You see the usual information: stock price and option chain. But now, you also see an event contract next to it: "Will Nvidia exceed Q2 revenue expectations?" The contract trades at $0.72, implying the market sees a 72% probability of exceeding expectations. You believe the market is underestimating demand for Nvidia products.

In this scenario, Robinhood lets you buy the stock, buy a call option, or buy 500 "Yes" contracts for $360 – netting you $140 profit if you're right ($0.28 profit per contract × 500 contracts).

Robinhood puts these three tools on the same screen, no tab switching required.

As mentioned earlier with the crude oil example, you can also use these tools to hedge positions. You could bet on Nvidia exceeding expectations while shorting the stock to hedge your prediction market wager. Thus, Robinhood allows you to build a cross-asset hedging strategy on the same screen in under a minute.

So far, this integration on the stock trading page has worked well for Robinhood, but it's still leaving money on the table. That will change soon, as Robinhood is about to take the next step.

Richer Context for Information Pricing

Robinhood's moat lies in providing users with all relevant information where and when they need it most. The era of buying Bitcoin on Coinbase, trading options on Deribit, holding stocks on Robinhood, and trading crude oil futures on IBKR is over. Users prefer to avoid switching contexts and platforms.

Once Robinhood embeds prediction markets across all asset pages, it transforms from a passive broker into an information pricing platform. Beyond price and analyst ratings, Robinhood will offer a real-time probability market for events related to that stock. Event contracts reflect the real-time consensus of participants with skin in the game. These contracts help users make better decisions, even if they never trade a single prediction market contract.

Take Nvidia again. The stock price at any moment reflects the sentiment of those holding the underlying equity. Accompanying equity are legal rights, shareholder reports, analyst Q&A sessions, and a framework built over 400 years to protect investors. But most of the time, traders might not care about those. The information they want to price might be "Will Nvidia exceed revenue expectations?" In this case, prediction markets are arguably a better source of pricing information than the stock price itself. Robinhood's attempt to bring derivatives, event contracts, and equities under one roof is precisely to capture value from all users who might want to trade that event.

But Polymarket and Kalshi have been doing this for years, so where is Robinhood's moat? Why not simply integrate third-party markets into its interface to increase revenue, instead of owning these markets itself? Cross-selling and volume more clearly reveal the incentive structure.

h2>Cross-Selling as a Regulatory Moat

In March 2026, two bipartisan bills were introduced aimed at banning sports-related event contracts at the federal level. Legal hurdles also exist at the state level. This is an existential crisis for platforms like Kalshi – 89% of its 2025 fee revenue came from sports-related event contracts. Approximately 60% of Polymarket's open interest also comes from sports-related event contracts.

If sports contracts face legal setbacks, Kalshi and Polymarket will be hit hardest. Without this dominant category, they cannot support valuations exceeding $20 billion. While Robinhood initially started with a heavy focus on sports markets, its cross-selling capability allows it to diversify revenue into stock and macro events (like earnings reports, Fed decisions, CPI data, and jobs reports).

For Robinhood, sports are just one revenue item. For Kalshi, the sports category is almost everything. Any regulatory crackdown on sports-related markets could impact Kalshi and Polymarket's claims to valuations above $20 billion. Robinhood is now moving up the value chain through a joint venture named Rothera.

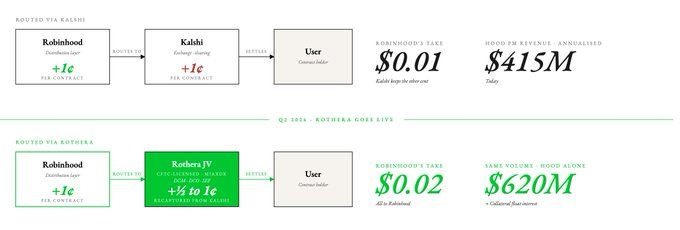

In November 2025, Robinhood formed a joint venture called Rothera LLC. The venture subsequently acquired MIAXdx – a CFTC-registered Designated Contract Market (DCM), Derivatives Clearing Organization (DCO), and Swap Execution Facility (SEF). This fundamentally changes the economic model, control, ownership, and clearing & settlement process of event contracts.

Relying on Kalshi to provide event markets limited the types of contracts Robinhood could list on its prediction market. Rothera allows Robinhood to list any event contract at any time.

Economically, this could mean Robinhood captures the cent currently going to Kalshi, potentially doubling event contract revenue. If Robinhood can direct half of that revenue to its own entity, its prediction market revenue could increase by 50% based on current event contract fee rates, reaching $620 million.

There's reason for optimism about the venture, as the latest quarterly results showed Robinhood beginning to invest in Rothera. Q1 2026 results included $14 million in venture-related costs. There's also a small bonus: once prediction market contracts are routed through Rothera, the collateral backing open positions sits on Robinhood's balance sheet, adding interest income to its revenue. With collateral for open interest reaching ~$100 million, this could generate an additional ~$4-5 million in annual revenue.

Every trading platform has a simple mission: get traders to move money as frequently as possible and take a small fee on each transaction; or get them to park large amounts of idle capital and keep the interest income. For Robinhood, it seems to be the latter strategy.

Robinhood's cross-selling moat via prediction markets is similar to the moat we previously described Hyperliquid enjoying through HIP-4 event contracts. Hyperliquid's unified risk engine integrates primitives like spot, perpetuals, deployment markets, and prediction markets, ensuring capital efficiency in a decentralized marketplace. The same logic applies to Robinhood, albeit within a centralized market.

Kalshi does not possess Robinhood's distribution moat across different asset classes. A standalone prediction market product is far less valuable than one embedded within all other trading products. Coinbase has just dipped its toes into prediction markets, while Robinhood's advantage of integrating its full asset stack with event contracts on one screen puts it ahead of Coinbase in the prediction market space.

By the Numbers

Any valuation discussion comparing Coinbase, Kalshi, and Robinhood essentially tries to answer the same question: what is the lifetime value of a user on each platform? Kalshi users may be fewer, but they pay much higher fees. The same user, if Robinhood can match Kalshi's liquidity at lower fees, will trade entirely on Robinhood.

The market has already seen this divergence. Kalshi and Robinhood trade at similar valuation multiples (15x), while Coinbase trades at a lower multiple of 7.5x. For Kalshi, prediction markets represent 100% of its revenue. For Robinhood, it's only 7%. For Coinbase, the figure is negligible.

Once Rothera goes live, Robinhood can price more competitively than any standalone prediction market platform. It can cut Kalshi's fees, absorb the margin hit, and still grow because every prediction market user is also a potential stock, options, and crypto customer. Kalshi hasn't remained silent, reportedly planning to launch cryptocurrency trading, starting with perpetuals. But transitioning from a prediction market to a multi-asset platform is far more difficult than integrating prediction markets into a multi-asset trading platform.

Robinhood has spent over a decade acquiring 27.4 million funded customers and building deep liquidity, market maker relationships, compliance infrastructure, and user trust. Kalshi will have to start from scratch.

One way to understand the value of this business is to hypothetically spin off Robinhood's prediction market unit and take it public independently. If it has $415 million ARR and the same growth trajectory, how much would it be worth? The easiest answer is 15 times Kalshi's, i.e., $6.2 billion. But all else being equal, a Kalshi with Robinhood's revenue lines would command a much higher valuation.

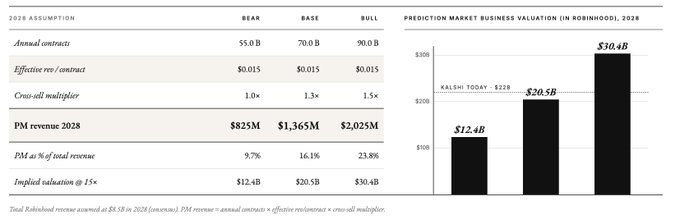

We built a three-year estimation model using the following assumptions:

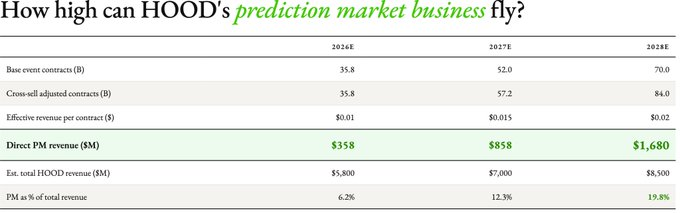

- Contract Volume: 70 billion event contracts in the base case for 2028. This assumes a ~40% CAGR over the next two years, based on Robinhood already recording 8.8 billion in Q1 this year (~35 billion annualized).

- Rothera Economics: We expect effective revenue per contract to rise from $0.01 to $0.015 in the bear case, or $0.02 in the base/bull case (three years out).

- Cross-Selling Boost: Multiplier of 1.0x for 2026 (cross-linking not live), 1.1x for 2027 (initial rollout on stock pages), 1.2x for 2028 (mature adoption). This assumes cross-selling adds 10-20% incremental volume on top of organic prediction market growth.

- Robinhood Total Revenue: Using consensus estimates: $5.4 billion for 2026, $6.4 billion for 2027, and $7.2 billion for 2028.

We then stress-tested for 2028 under bear, base, and bull scenarios.

Even in the bear case scenario, Robinhood's prediction market revenue alone would reach $825 million in 2028, over three times Kalshi's 2025 revenue ($260 million). Using Kalshi's current revenue multiple (15x), Robinhood's prediction market business would be worth $12 billion in this scenario. In the most optimistic scenario, it could be worth $30 billion by 2028.

What we are likely witnessing is: a business with a distribution moat, pioneering a new market and capturing most of the value for itself. The open question is whether Polymarket and Kalshi are a re-run of OpenSea in 2021, or whether they can successfully reinvent themselves when new threats emerge. Polymarket has expanded its perpetuals products in recent days, but its users are unlikely to switch to perpetuals trading because prediction markets were their primary intent. In contrast, Robinhood benefits from a core user base that consistently came for its high-risk, zero-fee trading tools. The latter seems to have an edge over the former.

Today, the market views Robinhood as a traditional finance broker with an add-on prediction market product, which is why prediction markets only account for 7% of its revenue. But if Robinhood CEO Vladimir Tenev delivers on his stated direction, Robinhood will become the platform that prices, in real-time, every financial view on earnings, interest rates, elections, and commodities, while also facilitating trading in the assets driven by those views.

A standalone prediction market will only attract those already trading event contracts. In contrast, a prediction market integrated into a retail broker becomes an information-pricing machine for everyone else. The vertical integration of capital aggregators is visible everywhere.