Q1 net loss of $394.1 million, Coinbase can only cling to Circle's coattails

- Core Thesis: Coinbase's Q1 2026 earnings report shows a 31% year-over-year revenue decline and a second consecutive quarterly net loss. The root cause is not merely market weakness but reflects the fact that its high-premium spot trading business is facing user attrition and intensifying competition. The company is responding by cutting costs through layoffs and pivoting towards derivatives, prediction markets, and stablecoin revenue, with the revenue-sharing agreement with Circle being a critical long-term pillar.

- Key Elements:

- Total Q1 2026 revenue was $1.41 billion, down 31% year-over-year, with a net loss of $394.1 million. Retail trading revenue fell by 48.2% quarter-over-quarter, returning to 2024 levels.

- Even excluding crypto asset book writedowns ($482 million), Coinbase's operating profit for the quarter was still negative (a loss of $21.4 million), indicating a deterioration in core business profitability.

- Maturing U.S. regulation has intensified competition, with over 10 exchanges now licensed to offer lower fee services. Retail users are shifting to low-cost platforms like Robinhood, and the company's market share gains are primarily driven by new products like derivatives.

- The company announced a 14% workforce reduction (~700 employees), officially attributed to the AI revolution and market downturn, but practically aimed at reducing costs and increasing efficiency in response to declining revenue.

- Under its "everything exchange" strategy, new businesses (derivatives, prediction markets) contributed a maximum of $73.6 million in Q1 revenue, far from the dominant role of spot trading. Base on-chain revenue was not independently disclosed, and its long-term contribution remains uncertain.

- Stablecoin revenue reached $305 million, up 10% year-over-year, representing the second largest revenue source. The distribution agreement with Circle is "perpetual," tying Coinbase to USDC's growth, with 25% of circulating USDC stored on its platform.

- Coinbase is promoting USDC for AI agent payment scenarios via the x402 protocol, predicting substantial AI agent transaction volume by 2030, laying the groundwork for future stablecoin revenue growth.

Original by Odaily Planet Daily (@OdailyChina)

Author: Golem (@web3_golem)

On May 8, Coinbase released its Q1 2026 earnings report. During the earnings call, CEO Brian Armstrong summarized the quarter by saying, "Despite headwinds in the crypto trading market, Coinbase has performed admirably within our control."

In the earnings presentation, Coinbase highlighted its Q1 achievements, such as its crypto trading market share reaching a record high of 8.6%; derivatives trading volume (TTM) growing 169% year-over-year; the prediction market generating an annualized revenue of $100 million in March (only two months after launch); and 12 products generating over $100 million in annual revenue.

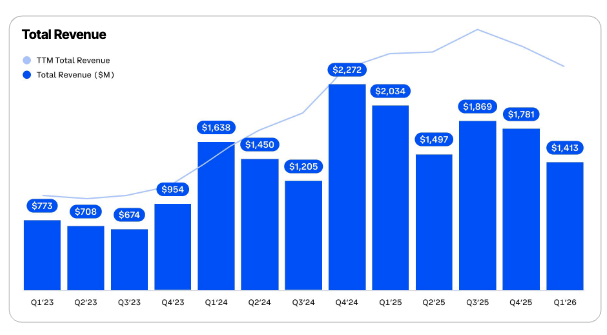

However, no amount of impressive slides could mask the bleak core financial metrics in Coinbase's Q1 report. The report shows that Coinbase's total revenue for Q1 2026 was $1.41 billion, a 31% decrease year-over-year and a 21% decrease quarter-over-quarter, missing market expectations. The net loss reached $394.1 million, marking Coinbase's second consecutive quarter of net losses (Odaily Note: Q4 2025 net loss was $666.7 million).

Following the release, Coinbase (NASDAQ: COIN) fell over 5% intraday on May 8 but managed to recover all losses by the close, ending the trading day at $201.16.

Is a Weakening Crypto Market the Sole Reason for Coinbase's Losses?

The post-earnings stock decline already reflected market concerns about Coinbase's short-term performance, and Coinbase attributed the primary cause of its losses to a weakening crypto market. Since Q3 2025, Coinbase's revenue has been declining, and the overall quarterly revenue trend coincides with the crypto market's transition from a bull to a bear cycle.

Coinbase Quarterly Revenue

But is market weakness the only reason for Coinbase's losses? What other potential issues can we uncover from the earnings report?

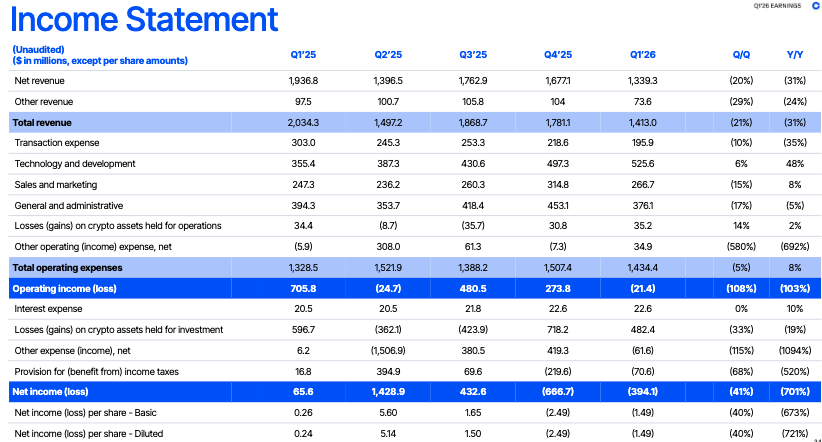

Some analysts believe Coinbase's net loss in Q1 was affected by impairment losses on its held crypto assets. The report also shows a $482 million loss from digital assets held for investment purposes. However, examining Coinbase's Q1 income statement reveals that even without these non-operating expenses, Coinbase's operating income for Q1 2026 was negative, with an operating loss of $21.4 million.

In Q4 2025, also impacted by the overall decline in the crypto market and weak trading activity, Coinbase's impairment losses on crypto assets were as high as $718.2 million, resulting in a final net loss of $666.7 million. Yet, in that quarter, Coinbase's operating income remained positive at $273.8 million.

Coinbase Q1 Income Statement

This indicates that while the weak crypto market impacted Coinbase's net profit, the company's performance was not as stable and well-controlled as Brian Armstrong described.

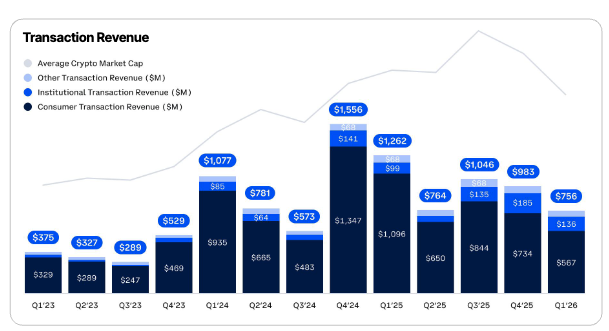

The problem lies in Coinbase's primary revenue source – its brokerage business, which provides digital asset trading intermediary services for retail and institutional clients. The Q1 2026 report shows Coinbase's transaction revenue was $756 million, of which retail contributed $567 million, a 48.2% decrease year-over-year and a 23% decrease quarter-over-quarter. Retail trading revenue has fallen back to 2024 levels.

Coinbase Quarterly Transaction Revenue

This effectively reflects a potential threat facing Coinbase: user attrition has already begun during the crypto market downturn.

Investors should not be misled by Coinbase's record-high market share in crypto trading volume highlighted in its presentation, as this includes products like derivatives and prediction markets, not just the spot market. According to Coinbase CFO Alesia Haas, revenue from these new products is not booked under transaction revenue (though it is included in total revenue).

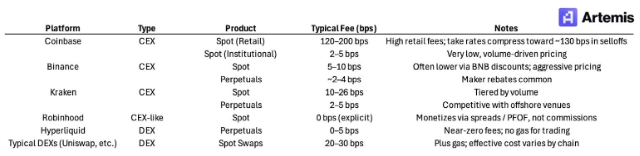

Coinbase's core competitive advantage has been its compliance in the US. Consequently, Coinbase has historically charged fees significantly higher than most global exchange counterparts. This was both to cover high compliance costs and to capture a premium from users after its early "monopoly" in the US crypto market. However, the US regulatory landscape has changed. Coinbase's compliance status is no longer a "game-ending" advantage, as over 10 exchanges have obtained licenses to offer crypto trading services to US users, including Robinhood, Kraken, and Binance.US.

These newcomers, without exception, charge lower fees than Coinbase and use this as a primary competitive strategy to attract retail users.

Fee Percentage Charged by Different Exchanges

For US retail investors, in the early days of the crypto market, they might have been willing to pay a premium to Coinbase for convenience, trust, and regulatory certainty. But as crypto regulations mature and the market downturns, retail users naturally gravitate towards platforms with lower fees, especially after traditional brokers and financial institutions like Robinhood entered the crypto space.

Addressing the fee issue during the earnings call, Brian Armstrong responded, "Clients choose us not because we are the cheapest, but because we can offer products that meet their needs." Although Coinbase One's paid subscribers have surpassed 1 million, when competing in terms of token variety and listing speed, the rise of DEXs like Hyperliquid has also posed a significant challenge to Coinbase and other CEXs.

Recently, Coinbase announced a 14% workforce reduction, leaving approximately 4,300 employees (down from 4,988 at the end of Q1). Brian Armstrong attributed the layoffs to the market downturn and the AI technology revolution. However, the real revenue situation disclosed in the Q1 report confirms that this was merely a cost-cutting and efficiency-enhancing measure disguised as an AI revolution. (Related reading: Coinbase Lays Off 14%: Is the Bear Market or AI the Main Cause?)

Painting a Grand Vision While Relying on Circle to Stay Afloat

Facing challenges like a weak crypto market, declining spot trading volumes, and user attrition, Coinbase is seeking new paths. Brian Armstrong stated on the earnings call that Coinbase is moving away from its dependence on spot trading, transitioning from a "spot-focused crypto platform" to one where users can trade a broader range of asset classes, including derivatives, stocks, commodities, and prediction market contracts – an "Everything Exchange."

These products were launched in early 2026. According to Coinbase, retail-focused derivatives generate over $200 million in annualized revenue, while the prediction market generates over $100 million. Coinbase CFO Alesia Haas noted that revenue from these new products is not included in transaction or subscription revenue. Assuming all other revenue was generated by these new products, the reality from the report is that they contributed a maximum of $73.6 million in total revenue in Q1.

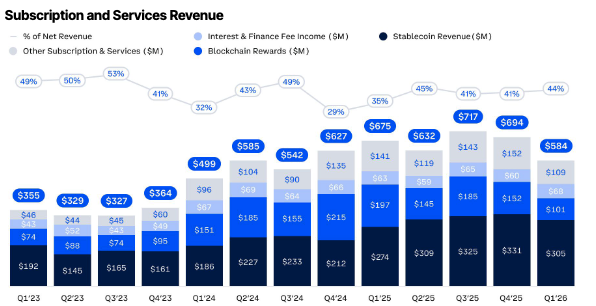

At the same time, Coinbase is deliberately "obscuring" the profit generated by Base. Brian Armstrong stated that Base handles 62% of global on-chain stablecoin transaction volume and over 90% of on-chain agent stablecoin transaction volume occurs on Base. However, Coinbase did not break out Base's revenue separately in the report. After carefully reviewing the report, Coinbase either did not disclose Base's real revenue or lumped it into the "Other subscription and services revenue" line item. In past quarters, Coinbase has often included on-chain revenue here, and in Q1 2026, this item generated only $109.4 million.

Base's on-chain fee revenue over the past 30 days was $2.72 million (Source: DeFiLlama)

In summary, Coinbase appears to be using long-term narratives around derivatives, prediction markets, AI, and on-chain activity to paint a grand picture for investors, diverting attention from its lackluster core business performance. Whether these areas ultimately become Coinbase's new "cash cows" remains to be seen over time. Chasing market hotspots and excessively expanding product lines might provide more stories to tell the market, but a misstep could lead to a chaotic mess.

However, Coinbase has the capital to experiment, thanks to its "good partner" Circle, which keeps it afloat.

The Q1 report shows that Coinbase's stablecoin revenue in Q1 2026 was $305 million, up 10% year-over-year. Stablecoin revenue is Coinbase's second-largest revenue source (Odaily Note: Retail trading revenue is the largest, and together they account for 62% of total revenue).

Coinbase Q1 Subscription and Services Revenue

This substantial revenue is primarily due to the revenue-sharing agreement between Coinbase and Circle. According to the agreement signed in August 2023, Coinbase receives the full interest income from USDC held on its platform, while interest income from USDC outside the platform is split 50/50 between Coinbase and Circle. During the Q1 2026 earnings call, Alesia Haas reiterated that the distribution contract between Coinbase and Circle auto-renews every three years and never terminates.

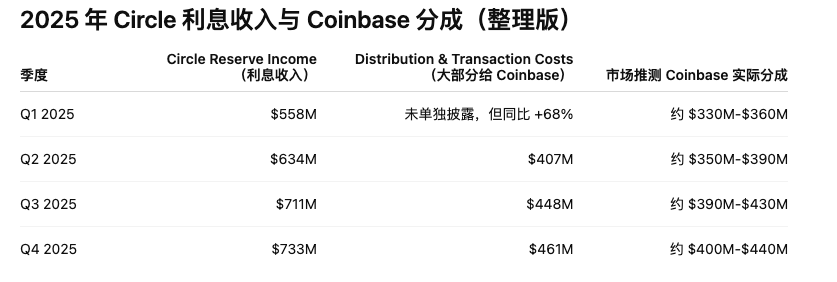

This structure effectively makes Coinbase a toll collector for USDC, and stablecoin revenue could very likely become Coinbase's primary revenue source in the future. On one hand, the amount of USDC deposited on Coinbase's platform and products continues to grow. The report disclosed that over 25% of the circulating USDC is stored on Coinbase (averaging about $19 billion in USDC held within Coinbase products). On the other hand, as stablecoins become more mainstream, Circle's interest income is also growing. As shown in the chart below, Circle's interest income increased from $558 million in Q1 2025 to $733 million by the end of the year.

On May 11, Circle will officially release its Q1 2026 earnings report, allowing investors to see Circle's interest income for Q1 2026 and the profit share for Coinbase.

But Coinbase has indeed played a significant role in distributing USDC. Beyond conventional channels, Coinbase is also actively promoting USDC in the AI and Agent-to-Agent (A2A) payment space. According to the report, Coinbase's x402 protocol (Odaily Note: now operated by the Linux Foundation) has processed over 100 million payments, with more than 99% of x402 transactions completed using USDC. Coinbase estimates that by 2030, AI agents will handle between $3 trillion and $5 trillion in transactions, making cryptocurrency the native execution channel for agents. If USDC becomes dominant in settling agent transactions, it could create immense economic value for Coinbase.

Therefore, if the distribution agreement between Coinbase and Circle never terminates, Coinbase will be permanently tied to the USDC "money printer." As long as the global stablecoin market continues to grow and USDC expands further into areas like payments, AI agents, cross-border settlements, and internet finance, Coinbase can steadily extract revenue. To some extent, this could be more profitable and more stable than Coinbase's current exchange business and various new products.