The Great Exodus: The Lost "Golden Exit Channel" for Crypto VCs

- Core Viewpoint: The crypto venture capital industry is facing structural challenges. The traditional exit model reliant on token issuance is failing due to changes in market structure. VC firms need to redefine their value proposition, shifting from merely providing capital to offering brand endorsement and substantive empowerment.

- Key Factors:

- Projects like HYPE demonstrate that on-chain revenue has become a core threshold for token value, shaking the logic of narrative-driven governance tokens with weak fundamentals.

- The explosive growth of meme coins (e.g., PUMP) has fragmented market liquidity and attention, compressing the lifecycle and return potential of other tokens.

- Retail capital is being diverted to emerging risky assets like prediction markets and stock perpetual contracts, further weakening the capital appeal of altcoins.

- Return expectations for token projects are being compressed, while equity-based or "Web2.5" companies with real revenue are regaining favor from venture capital.

- High-quality projects (e.g., Axiom, HYPE) can bypass institutional capital. VCs need to prove their value to founders through brand identity and actual empowerment capabilities, not just by providing funds.

Original Title: The Great Attrition of Crypto VCs

Original Author: Catrina

Original Compilation: Peggy, BlockBeats

Editor's Note: When "token launch equals exit" is no longer valid, crypto venture capital is also losing its once most solid logic.

Over the past three cycles, tokens have been the core path for capital recovery and profit amplification. Built around this premise, the industry established a familiar rhythm: early-stage financing, narrative expansion, listing and circulation, and price realization. However, against the backdrop of on-chain revenue becoming the new threshold, meme coins diverting liquidity, and retail capital spilling over into more risky assets, this mechanism is failing.

A more direct change is that the return expectations for token projects are being compressed, while the equity path is regaining attractiveness. Early-stage investors are becoming more cautious about projects planning "token exit," while later-stage capital is shifting towards "web2.5" companies with real revenue and merger & acquisition expectations. Crypto VCs are no longer in a relatively closed competitive environment but are forced into a field where they compete head-to-head with traditional fintech funds.

In this process, a deeper question gradually emerges: when capital itself is no longer scarce, what can VCs still offer?

In recent years, some of the most representative projects have almost bypassed institutional capital, directly building network effects and revenue models. This means capital is no longer a "passport" to access high-quality projects. For founders, whether to bring in a VC depends on whether the latter can provide clear brand endorsement and actual incremental value, not just capital on the books.

Under the new market structure, crypto VCs need to rediscover their own "product definition." Otherwise, they risk becoming one of the entities eliminated in this cycle.

The following is the original text:

Crypto venture capital is at a watershed moment. Over the past three cycles, token exits have been the primary source of outsized returns, but this model is now undergoing a substantive reset. The definition of what constitutes a valuable token is being rewritten in real-time, while a unified industry-level evaluation framework has yet to form.

So, what exactly happened?

The change in this round of crypto market structure is the result of the superposition of multiple forces that have never appeared in the same cycle before:

1/ The emergence of HYPE has impacted the entire token market from the flank. It proved one thing: token prices can be supported by real revenue, with over 97% of its eight or even nine-figure revenue coming from on-chain. This case quickly triggered collective disillusionment with "narrative-driven but fundamentally weak" governance tokens—such as early L1s and "governance tokens" primarily used to circumvent securities regulations but difficult to directly distribute revenue from. Almost overnight, HYPE reshaped market expectations: revenue capability is no longer a bonus but a minimum threshold.

2/ The chain reaction impact on other projects followed: before 2025, if a project had on-chain revenue, it was often deemed a security; after HYPE, if it lacked on-chain revenue, in the eyes of most hedge funds, its path to zero was just a matter of time. This has forced the vast majority of projects, especially non-DeFi ones, into a dilemma, scrambling to adjust their paths.

3/ PUMP delivered a severe "supply shock" to the system. The meme coin frenzy brought an explosive growth in token supply, fundamentally disrupting the market structure—attention and liquidity were severely fragmented. On Solana alone, the number of newly issued tokens surged from about 2,000–4,000 per year to a peak of 40,000–50,000, equivalent to slicing the pie into about 20 times more pieces with almost no growth in liquidity. The same batch of capital and attention seeking high yields began shifting from holding altcoins to shorter-term meme coin trading.

4/ Alternative destinations for retail risk capital are also rapidly increasing. Products like prediction markets, stock perps, and leveraged ETFs are directly competing for the capital that previously flowed into crypto altcoins. Meanwhile, the maturation of asset tokenization technology allows investors to leverage blue-chip stocks. These assets neither face the zero-risk of most altcoins nor operate under stricter regulation with greater transparency and less information disadvantage.

These changes collectively lead to one result: the token lifecycle is significantly compressed. The cycle from peak to trough has shortened dramatically, retail willingness for "long-term holding" has plummeted, replaced by faster capital rotation.

Core Questions

Against this backdrop, almost all VCs are repeatedly pondering several core questions:

1/ Are we investing in equity, tokens, or a combination of both?

The biggest difficulty is that there is currently no mature paradigm for "how token value accumulates." Even top projects like Aave still face ongoing controversy between DAO and equity structures.

2/ What is the best practice for on-chain value accumulation?

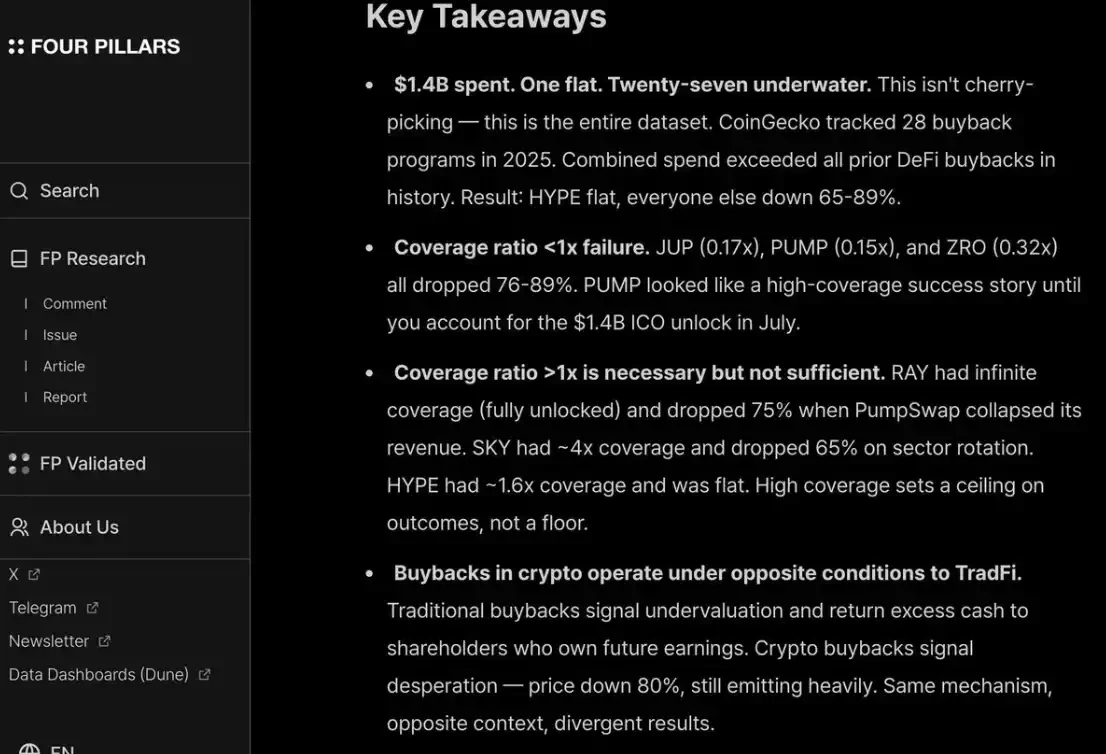

The most common current practice is token buybacks, but "common" does not mean "correct." We have long opposed the mainstream buyback logic: this mechanism is "toxic," placing truly revenue-capable projects in a dilemma.

The problem is, its motivation is wrong from the start.

Traditional companies buy back stock, typically when growth investment opportunities diminish or the stock price is undervalued; crypto project buybacks are often forced into "immediate execution" under pressure from retail and market sentiment—a pressure that is highly emotional and unstable. You might just allocate $10 million for buybacks, funds that could have been reinvested, only to see them completely swallowed by the market the next day because some market maker got liquidated.

Public companies buy back stock when undervalued; token buybacks are often front-run and executed at local highs.

If your business is a B2B model primarily generating off-chain revenue, such buybacks are even more futile. In my personal view, at a stage with annual revenue below $20 million, there is almost no justification for buybacks to please retail—these funds should be prioritized for growth.

I agree with a report/screenshot from fourpillars: even buybacks on a nine-figure scale are unlikely to substantially help establish a long-term price floor for a project.

Furthermore, to please both retail and hedge funds, you must also conduct buybacks continuously and transparently, like HYPE. Failure to do so will be punished by the market, like PUMP—its fully diluted valuation (P/F) is only 6x because the market "doesn't trust" it. Even though, in fact, it has burned $1.4 billion in revenue that could have gone into its treasury.

3/ Will the "crypto premium" completely disappear?

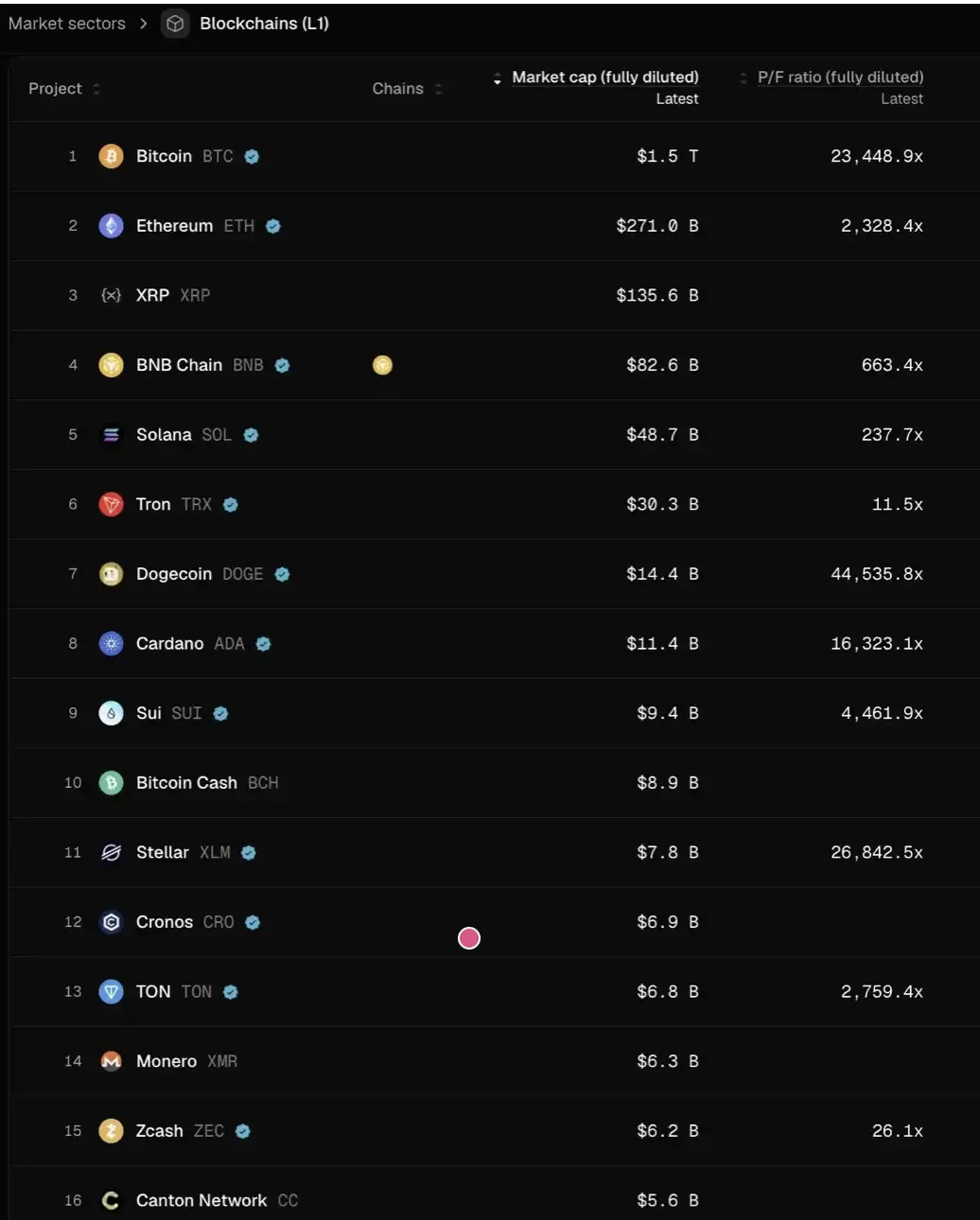

This means that future valuations for all projects may revert to ranges similar to traditional public companies—roughly between 2–30x revenue.

Think seriously about the implications: if this holds true, then from current levels, most L1 prices might need to fall by over 95% more to align with this valuation system. Only a few exceptions—like TRON, HYPE, and other DeFi projects with real revenue—could stand relatively firm.

And this hasn't even considered the additional selling pressure from token vesting.

Personally, I don't believe things will go that far. HYPE essentially set an "outlier" market expectation, making investors exceptionally impatient about whether early-stage projects have "revenue/user growth upon launch." For "sustaining innovations" like payments and DeFi, such demands are reasonable; but for "disruptive innovations," time is inherently needed from building, launching, growing, to truly experiencing a revenue explosion.

Over the past two cycles, we've rapidly swung from being overly tolerant of "disruptive technologies," experiencing 8–9 rounds of financing in highly abstract narratives like new L1s, Flashbots/MEV, fueled by "patience + hopium," to the other extreme—only willing to bet on DeFi projects. This is essentially an overcorrection.

But the pendulum will swing back.

For DeFi projects, pricing based on "quantitative fundamentals" is indeed a sign of industry maturity; but for non-DeFi sectors, "qualitative fundamentals" are equally indispensable: including culture, technological innovation, disruptive ideas, security, degree of decentralization, brand value, and industry connectivity. These dimensions are not simply reflected in TVL or on-chain buyback data.

So, what happens next?

Return expectations for token projects have clearly compressed, while equity-based businesses have not cooled to the same extent. This divergence is particularly evident in early and growth-stage investments:

At the early stage, investors have become more price-sensitive towards projects planning "future token exits"; meanwhile, interest in equity-based projects has risen significantly, especially against the current relatively friendly M&A environment. This contrasts sharply with 2022–2024—when token exit was the default path, based on the assumption that "token valuation premiums would persist."

At the later stage, investors with brand advantages and resource capabilities in the crypto-native context are gradually moving away from purely "crypto-native" projects, betting more on "web2.5" companies—whose valuation logic is more anchored to real revenue growth. This also thrusts them into an unfamiliar competitive arena: needing to compete directly with crossover funds and traditional Web2 fintech funds (like Ribbit Capital or Founders Fund), which have deeper accumulation in traditional finance context, portfolio synergy, and early-stage project sourcing capabilities.

The entire crypto VC industry is entering an "attribution period."

Who stays depends on whether they can find their own "product-market fit" (PMF) in the minds of founders—and this "product" is not just capital, but a combination of brand identity and actual enabling capabilities.

For high-quality projects, VCs need to "sell themselves to founders" to earn a spot on the cap table. Especially in recent years, some of the most successful projects have relied little on institutional capital (e.g., Axiom), or even raised no funds at all (e.g., HYPE). If a VC can only offer capital, it is almost destined to be marginalized.

VCs truly qualified to remain at the table must clearly answer two questions:

First, what is its brand identity—why would the best founders proactively seek it out;

Second, where is its value add—ultimately determining its ability to win that deal.