Daily 10 AM Dump: Is Jane Street the Mastermind Behind Bitcoin's Halving?

- Core Argument: The article alleges that Jane Street Capital leverages its privileged position as a primary market maker and authorized participant for Bitcoin ETFs to artificially suppress Bitcoin prices and profit through undisclosed derivatives positions and algorithmic trading strategies, thereby undermining the market's genuine price discovery mechanism.

- Key Elements:

- The lawsuit alleges that Jane Street precisely unwound positions before the Terra/Luna collapse using insider information, avoiding over $200 million in losses, demonstrating a pattern of trading behavior that exploits informational advantages.

- From late 2024 into 2025, Bitcoin exhibited regular, programmed sell-offs daily at 10 AM Eastern Time, triggering liquidations of highly leveraged long positions. This pattern paused after the Terra lawsuit became public but later resumed.

- Jane Street holds approximately $790 million worth of BlackRock's IBIT ETF shares. However, as an authorized participant, these spot holdings could be fully hedged by undiscovered short positions in derivatives like options and futures.

- Current 13F filings only require disclosure of long equity positions, not short derivatives positions. This may lead the market to misinterpret their holdings as a bullish signal, while their actual net exposure could be zero or even negative (net short).

- Jane Street has a precedent in the Indian market, where it was fined and restricted by regulators for manipulating BANKNIFTY index options (using coordinated trading across spot and derivatives markets).

- The article posits that through undisclosed derivatives, Jane Street can create unlimited "synthetic" Bitcoin exposure on top of its spot Bitcoin ETF holdings, thereby distorting the true supply-and-demand-based price discovery predicated on the 21 million cap.

Everyone knows Bitcoin should be at least $150,000 by now.

But why isn't it? A federal lawsuit filed yesterday in Manhattan provides the answer.

For the first time, let's connect three things: a federal insider trading case linked to a private chat group called "Bryce's Secret"; a program that consistently dumped Bitcoin to suppress its price at exactly 10 AM EST until late 2025; and an undisclosed derivatives book that may have turned the holdings of the world's largest Bitcoin ETF into a tool for suppressing Bitcoin.

All three threads lead to the same name: Jane Street Capital.

The Intern

It starts with an intern named Bryce Pratt.

Bryce interned at Terraform Labs, the Singapore-based company behind the algorithmic stablecoin UST and its token, Luna. In September 2021, he left Terraform and joined Jane Street as a full-time employee.

Jane Street is also where SBF learned to trade before founding FTX and Alameda Research. Many of his colleagues either came from Jane Street or had close ties to it.

According to a lawsuit filed by Terraform's bankruptcy administrator, Todd Snyder, Bryce became a bridge between his old and new employers through a chat group—referred to in court documents as "Bryce's Secret."

The lawsuit alleges Jane Street used this group to obtain material non-public information about Terraform's internal capital movements.

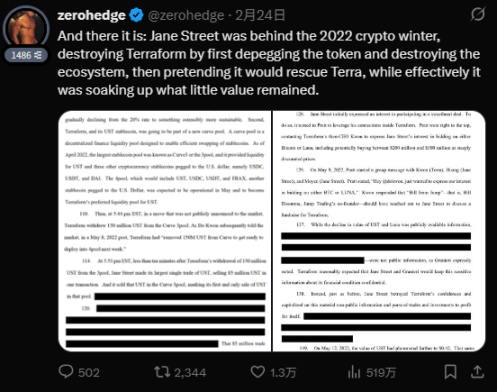

The critical moment was May 7, 2022. Terraform withdrew $150 million in UST from a decentralized exchange platform called the Curve 3pool—the stablecoin's primary liquidity pool. Within ten minutes of this withdrawal, before Terraform announced anything publicly, a wallet linked to Jane Street pulled $85 million in UST from the same pool.

What happened next is familiar. Selling pressure caused UST to depeg. Within days, Luna's algorithmic mechanism spiraled out of control, the token hyperinflated, $40 billion in market value evaporated, and retail investors were wiped out.

The lawsuit claims Jane Street "accurately closed its positions hours before the collapse of the Terraform ecosystem," avoiding over $200 million in potential losses. The filing states plainly: these trades "would have been impossible without insider information."

Jane Street's response: the lawsuit is "ridiculous" and "baseless," arguing that Terra and Luna holders' losses were caused by Terraform's own fraud.

Incidentally, Do Kwon is now serving a 15-year prison sentence. Snyder also sued Jump Trading for $4 billion on similar grounds—suggesting this is a systematic investigation into institutional behavior during Terra's collapse, not just targeting Jane Street.

The Clock Starts Ticking

Starting in late 2024 and intensifying through 2025, Bitcoin exhibited a pattern that baffled traders:

Every day at 10 AM Eastern Time, coinciding with the US stock market open, Bitcoin would experience a sharp, programmed sell-off. The drops were precise, clearly algorithmic, disproportionately large, and disconnected from overall market trends. They specifically targeted highly leveraged long positions, triggering cascading liquidations, only for the price to recover hours later.

Two founders of blockchain analytics firm Glassnode documented this pattern. Tracking months of data, they found the regularity unmistakable. Charts from December showed Bitcoin dropping from $89,700 to $87,700 within minutes of the 10 AM open, wiping out $171 million in long positions before slowly recovering.

Day after day, without fail.

As a designated market maker and authorized participant for multiple Bitcoin ETFs, Jane Street held the spot inventory and possessed the infrastructure for large-scale selling. Dumping at the open during the weakest liquidity could depress prices, trigger liquidations among leveraged traders, and allow buying back at lower levels. A seamless operation: create the dip, then buy it.

Then something interesting happened.

Glassnode's founders noted that shortly after the Terraform lawsuit documents became public early last year, these daily flash crashes stopped. Bitcoin's price stabilized noticeably. This wasn't a coincidence—it looked like a company realizing lawyers were about to scrutinize its books.

But the stability didn't last. By Q3 2025, the 10 AM dumps returned, and by year-end, they were back in full "glory."

In short: Jane Street stopped dumping when lawyers were watching and resumed when the heat died down.

The Quant Machine

In its Q4 2025 13F filing, Jane Street disclosed holding over 20.31 million shares of IBIT (BlackRock's Bitcoin ETF), worth approximately $790 million. It added 7.1 million shares worth $276 million that quarter alone. At one point last year, its total IBIT holdings neared $2.5 billion.

Simultaneously, it aggressively bought MicroStrategy stock, increasing its stake by 473% to over 950,000 shares worth about $121 million. Meanwhile, BlackRock and Vanguard were selling billions worth of MicroStrategy shares.

Many crypto media outlets saw this 13F and proclaimed, "Wow, institutions are buying!" But anyone who understands market structure knew something was off.

Does this look like bullish conviction, a massive accumulation? That's only if you don't know what Jane Street does.

Jane Street is one of only four firms authorized for "physical creation and redemption" of IBIT shares, alongside Virtu Americas, JPMorgan, and Marex. It's also an authorized participant for Fidelity and WisdomTree's Bitcoin ETFs. What does this mean? It means direct access to the plumbing connecting ETF prices to real Bitcoin. It can move actual Bitcoin in and out of ETFs, arbitrage between fund and spot prices, and hoard inventory inaccessible to ordinary investors.

In other words, Jane Street holds the "pipes" connecting Bitcoin ETFs to real Bitcoin, while others do not.

The Invisible Ledger

Former hedge fund manager Michael Green said watching people interpret Jane Street's 13F as bullish makes him "uncomfortable." He pointed out that Jane Street's IBIT holdings are "almost certainly offset by undisclosed options and futures positions," and "they are absolutely not accumulating Bitcoin; this is standard market-making."

Former proprietary trader Ryan Scott was blunter: "Anyone taking this as a bullish signal is a financial death row inmate. This should be interpreted as: 'Guess who else holds undisclosed hedging derivatives?'"

Nicholas Batia summed it up: Jane Street holds IBIT to sell options, arbitrage, and engage in various fast-paced quant strategies.

What does this mean for anyone holding Bitcoin or IBIT?

13F filings only disclose long equity positions; they don't require disclosure of options, futures, or swaps. So when Jane Street says it holds $790 million in IBIT shares, you have no idea if those shares are hedged with put options, offset by short futures, or wrapped in some options strategy—its actual Bitcoin exposure could be zero, or even negative (i.e., net short).

The public only sees the buying. Its actual position could be a massive short—because the hedged half remains invisible under current disclosure rules.

A 13F is like a photo showing only half a body; only Jane Street knows what the other half looks like.

So every Bitcoin holder must ask an unavoidable question: If Jane Street holds $790 million in IBIT and hedges it with $790 million in put options or short futures, its net exposure is zero. If its derivatives position is larger than its equity position, its net exposure is negative—meaning it profits when Bitcoin falls.

In that scenario, it has every incentive to use its privileged status as an authorized participant to hammer the spot price, trigger others' liquidations, and profit from the spread.

The question: Is Jane Street net long or net short on Bitcoin? Under current disclosure rules, it doesn't have to answer.

Precedent

Jane Street's activities in Bitcoin markets haven't been scrutinized by regulators yet, but they have in other markets.

In 2025, the Securities and Exchange Board of India issued a 105-page penalty order accusing Jane Street of manipulating BANKNIFTY index options in Indian markets.

SEBI found that through coordinated trading in spot and derivatives markets, Jane Street made INR 365 billion (~$4.3 billion) over two years, including INR 73.5 billion (~$880 million) in a single day. The regulator stated plainly: such conduct is illegal in any jurisdiction with proper financial regulation. It then restricted Jane Street's trading activities.

Look at its modus operandi in Indian index derivatives: use speed and scale to create moves in one market, then harvest profits in the layered derivatives market above it.

The question now is: Is the Bitcoin market the same?

21 Million

The hard cap of 21 million is maintained by a global network of Bitcoin nodes.

But this cap only works under one premise: price discovery is genuine, and the market reflects real supply and demand. Institutions hold Bitcoin or Bitcoin-related products because they are genuinely bullish, not because they are using it as "raw material" for invisible derivatives strategies.

In other words, the 21 million cap only matters if the "market is honest."

And now?

Jane Street is one of four firms holding the keys to Bitcoin ETF infrastructure. It is facing a federal lawsuit alleging it front-ran using insider information, helping wipe out $40 billion in market value. It is accused of suppressing Bitcoin's price for months with programmed dumps. It holds the largest disclosed ETF position while maintaining a derivatives book that could make it appear bullish while being bearish.

So, the 21 million cap is just a number to Jane Street. Because through undisclosed derivatives, it can create infinite "synthetic" Bitcoin on top of its ETF inventory.

Bitcoin is scarce at the protocol level, but the price discovery mechanism built on top of it has been corrupted by a firm treating its privilege as an ATM. And current disclosure rules allow it to continue, unseen.

Every Bitcoin holder deserves to know the answer: Is Jane Street's real position long or short?

Until we know, Bitcoin's price isn't set by the market. It's set by Jane Street.