Is the "Gold Standard" Making a Comeback? Let's Imagine: How Can Web3 Rebuild a "Gold-Denominated" Payment Loop?

- Core Viewpoint: Empowered by blockchain technology and RWA (Real World Assets), gold is transitioning from a traditional safe-haven reserve asset into a potential "digital physical gold" with capabilities for divisibility, verifiability, and global circulation for payments. It holds the potential to re-enter the forefront of monetary systems in specific regions where fiat systems are failing.

- Key Elements:

- In regions with hyperinflation, fiat currency fails as a unit of account, leading people to turn to USD stablecoins as a "parallel currency." The core of this shift is the combination of "USD consensus + blockchain technology."

- Historically, gold exited daily payments primarily due to the circulation, verification, and settlement challenges posed by its physical form, relegating it to a "store of value" rather than a "circulating currency."

- Tokenized gold (e.g., XAUt), by being 1:1 backed by physical gold and placed on-chain, enables infinite divisibility of the asset, transparent on-chain verification, and 24/7 global transferability, solving gold's physical limitations.

- Payment card products (e.g., imToken Card) build a seamless payment loop connecting on-chain gold assets to real-world merchants by instantly converting gold tokens into fiat currency for settlement on the backend.

- This technological combination endows gold, for the first time, with the simultaneous capabilities of serving as a unit of account, a medium of exchange, and a means of payment, completing the critical leap from a "store of value asset" to a "payment medium."

As is well known, throughout the over thousand-year history of financial development, the role of gold in the global monetary system has been redefined multiple times.

The most recent transformation undoubtedly occurred after the establishment of the modern fiat currency system based on credit. Gold gradually receded from daily transactions, existing more as a 'safe-haven asset,' 'central bank reserve,' and 'macroeconomic hedging tool.' Particularly in the lives of ordinary people, aside from its value in specific cultural contexts like 'three golds' or 'five golds,' gold has almost completely exited the payment scene.

However, if we shift our perspective away from developed economies and observe regions with runaway inflation and frequently failing monetary systems, we discover a new line of thought for reconsideration:

With the support of blockchain technology, gold has the potential to regain its capabilities of being 'valuable, transferable, and payable,' thus no longer being merely a safe-haven asset on paper but stepping back into the forefront of the monetary system.

This article will also explore how, against the current economic and technological backdrop, revisiting the 'gold standard' may not be merely a nostalgic fantasy but a practical discussion about the credibility of the unit of account.

1. The Problem Isn't Just Inflation, It's the Failure of the 'Weights and Measures'

Objectively speaking, in countries like Venezuela and Argentina, the inflationary pain faced by the populace cannot be summarized by the simple phrase 'rising prices.' The truly fatal issue is that due to the severe volatility of the local currency's exchange rate, its function as a 'measure of value' is completely lost, while the fruits of people's labor rapidly depreciate amidst inflation.

Imagine, under hyperinflation, the price of a glass of iced lemonade could double within a week or even a few days. In such a scenario, people might not even know 'how much money is valuable.' This uncertainty not only leads to the silent erosion of labor's value but also signifies that the unit of account is naturally no longer trustworthy, resulting in a systemic problem deeper than 'declining purchasing power.'

In such an environment, for self-preservation, people will instinctively seek alternatives. This explains why dollar-pegged stablecoins, represented by USDT and USDC, have rapidly achieved grassroots penetration in countries like Argentina, becoming de facto 'parallel currencies.'

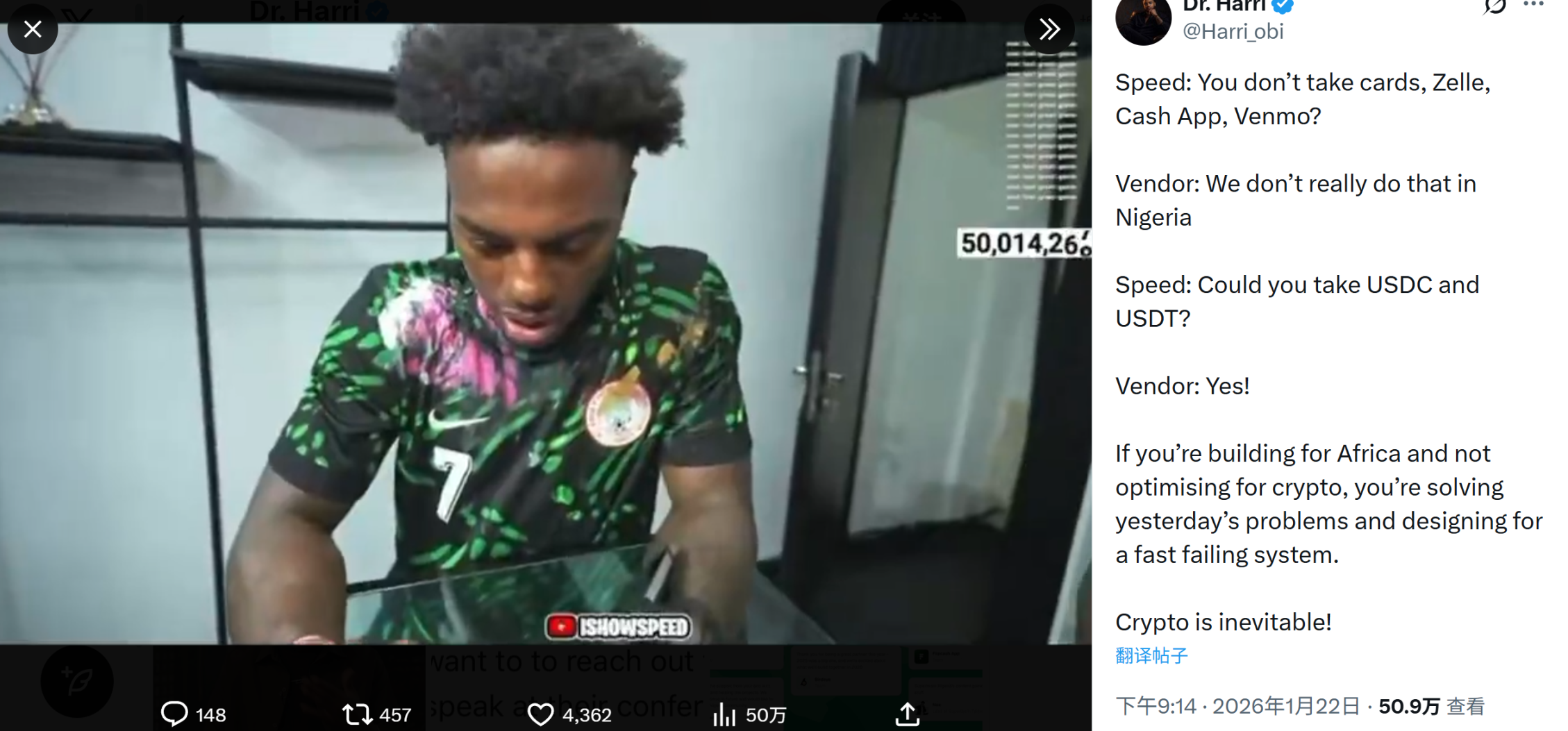

A recent typical case that broke into the mainstream: When globally renowned internet personality 'iShowSpeed' was shopping in Nigeria, traditional financial payment methods were frequently restricted (he mentioned issues with bank cards, Cash App, etc.). Ultimately, he chose to complete the payment using USDT/USDC, and the merchant was willing to accept it directly.

As shown in the video, a transaction worth approximately 2.3 million Naira (around $1,500 USD) was settled within seconds.

Ultimately, the widespread adoption of dollar stablecoins is not because they are 'more advanced,' but because the US dollar itself remains the unit of account with the strongest global consensus. Simultaneously, stablecoins bypass the local banking system, avoiding cumbersome foreign exchange controls and clearing/settlement barriers.

Consensus (USD) + Technology (Blockchain) – both are indispensable.

This leads to a logical question: If what people seek is a long-term, credible unit of account, then gold, with its thousand-year monetary history, lost out to credit-based fiat currency in the competition for everyday payments not because it wasn't a good store of value, but because it had fatal physical limitations as a medium of exchange – it was difficult to circulate and use for payments. Physically, it was hard to divide, transport, verify, had low settlement efficiency, and high transfer costs...

This is why, in the traditional financial system, gold is treated more as a 'store of value' rather than 'money' in the true sense. In fact, even in historical 'gold standard' monetary systems like the British pound, gold's significance was more about 'serving as a reserve,' acting as the anchor for the entire system, rather than directly serving as the unit of account.

This has also led gold to gradually recede into the background, existing only on balance sheets and in central bank vaults.

2. Transforming Gold from a 'Dead Asset' into 'Live Money'

Ultimately, what has truly prevented gold from returning to its monetary role has never been a lack of consensus, but rather technological constraints. If gold cannot participate in payments, it will forever remain a 'held asset' and cannot become 'used currency.'

And this is precisely where a fundamental change is occurring for the first time, empowered by RWA and Crypto – leveraging blockchain technology, heavy gold bars can be broken down into countless tiny digital particles, enabling free global circulation 24/7.

Take XAUt (Tether Gold), issued by Tether, as an example. Each XAUt token corresponds to 1 troy ounce of physical gold stored in a London vault. The physical gold is held in professional vaults, is auditable and verifiable, and tokenized gold holders possess a claim on the underlying gold.

When an on-chain transaction occurs, the system automatically reallocates the gold shares in the vault to ensure the tokens held by users always correspond to specific physical assets. The physical gold is stored in a high-security vault in Switzerland. While the custodian is a related party, it operates independently with separate financial accounts and customer records. Users can also visit the official 'Look-up Website,' input their on-chain address, and directly query the serial number, weight, and purity of the gold bars associated with their assets.

It can be said that this design does not introduce complex financial engineering, nor does it attempt to amplify gold's properties through algorithms or credit expansion. On the contrary, it deliberately maintains respect for traditional gold logic. Moreover, thanks to blockchain's transparency, anyone can verify the full collateralization of on-chain assets at any time—a level of transparency unmatched by traditional gold certificates.

Ultimately, tokenized gold like XAUt and PAXG is not about 'creating a new narrative for gold,' nor is it as simple as 'moving gold onto the chain' like some RWA projects for real estate tokenization. It enables gold, for the first time, to simultaneously possess the capabilities of being a unit of account, a medium of exchange, and a means of payment.

This is equivalent to using blockchain to repackage the oldest form of asset. In this sense, XAUt is more like a rebirth of 'digital physical gold' (Extended reading: Tether's 'Gold Standard' Ambition: Deconstructing XAUt, How the Stablecoin Titan is Buying Gold):

- Infinite Divisibility: You no longer need to cut gold bars; RWA allows you to pay with 0.00001 grams of gold;

- Instant Verification: No need for fire assays or chemical tests; an on-chain signature is the best proof of purity;

- Global Transfer: Gold is no longer constrained by geography; it becomes a piece of digital information flowing 24/7.

It is precisely in this sense that Web3 + RWA is not about speculating on gold, but about returning gold to the core of monetary discussion.

Of course, on-chain gold primarily solves the problems of asset form and the settlement layer. To truly achieve the 'monetization' of gold, one final practical challenge remains:

How can it be truly 'spent' in the real world?

3. How to Form a Closed Payment Loop?

A theoretical payment closed loop must satisfy two conditions simultaneously: It must be sufficiently simple and seamless for the user; it must not require merchants to change their existing systems.

This requires an efficient terminal tool, which is precisely the purpose of various payment card products currently on the market. Taking imToken Card as an example, if it can bridge the connection between on-chain gold and the real world, it truly has the potential to turn 'gold standard payments' from a geek's idea into an everyday occurrence at supermarket checkouts.

The core value of imToken Card lies in its ability to handle the backend clearing of complex assets. For instance, if a user holds RWA gold assets (like XAUt) in their imToken wallet, at the moment of consumption, the system automatically completes the following closed loop:

- Asset Storage: During non-consumption periods, your wealth exists in the form of 'gold tokens,' enjoying their inflation-hedging properties.

- Instant Clearing: When you swipe the card at tens of millions of merchants worldwide that accept Mastercard, the backend converts a portion of the gold tokens to fiat currency at the real-time exchange rate.

- Seamless Payment: The merchant receives fiat currency settlement, while you pay from your gold token balance.

And this entire process is seamless for the user, yet completes a 'gold → payment' value transfer at the underlying layer. The assets also remain stored in the user's personal on-chain wallet, not in a traditional 'paper gold certificate' or bank account. This means you have absolute ownership and control over the gold tokens, rather than relying on a bank's promise to pay.

If RWA solves the problem of 'how to put gold on-chain,' then payment cards solve the problem of 'how to spend on-chain gold.'

Overall, when gold can both serve as a long-term held value anchor and be used as readily as cash, it truly completes the transition from a 'store of value asset' to a 'payment medium' once again.

It is precisely at this moment that we might be standing at a rather interesting inflection point: A monetary form with a history of over a thousand years is being revitalized by cutting-edge technology that is barely over a decade old.