The Backlash of Sanctions: Latin America's Financial System Defection Seen from Maduro's Arrest

- Core Viewpoint: Latin America is breaking free from U.S. financial control through parallel financial ecosystems.

- Key Elements:

- Stablecoins (e.g., USDT) have become crucial tools for evading sanctions and facilitating trade.

- Local fintech solutions (e.g., Brazil's Pix, Nubank) enable efficient and inclusive payments.

- Non-dollar trade channels (e.g., China-Latin America local currency swaps) provide strategic decoupling options.

- Market Impact: Weakens dollar hegemony and promotes the development of decentralized finance.

- Timeliness Note: Long-term impact.

Original Author: Sleepy.txt, Dongcha Beating

In the 1980s, Latin America's total external debt approached 50% of its GDP. This metric was once a ruler used by Washington to measure loyalty and control while surveying its backyard.

Today, that number has dropped to 20%.

However, this 22-percentage-point difference does not signify that Latin Americans are becoming wealthier day by day. To free themselves from the constraints of others' currencies and rules, they are still struggling within the old order, paying a heavy price for it.

This is a contest between "control" and "loss of control." The United States has attempted to grasp the economic lifeline of this continent through debt, currency, and sanctions. Yet, when such control is pushed to its limits, the system inevitably sparks an endogenous force of resistance.

Three Weapons of U.S. Financial Control in Latin America

Over the past half-century, the American financial empire's dominance over Latin America has primarily relied on three unfailing weapons.

The first weapon is debt. This is the empire's oldest colonial tool and its most effective instrument of financial governance.

On August 12, 1982, a distress call from Mexico's finance minister ignited the Latin American debt crisis. As Mexico declared its inability to repay $80 billion in external debt, the first domino fell. Brazil, Argentina, and Venezuela successively tumbled into the quagmire of default.

Subsequently, the "creditor alliance" composed of the U.S. Treasury, the Federal Reserve, and the IMF entered the scene. Their lifelines were exorbitantly expensive; attached to each aid package were extremely harsh conditionalities.

This later became the infamous Washington Consensus, which forced these countries to slash government spending, sell off state-owned assets, and completely open their domestic markets and capital controls.

It was an era when the U.S. could determine a nation's fate for the next decade with a single check. Debt became a noose tightening around the necks of Latin American countries, with the rope's end firmly held in American hands. Behind every aid package, the price of power was already clearly marked.

The second weapon is dollarization.

When debt control proved insufficient, a more extreme solution was pushed to the forefront: simply abolish your national currency and adopt the U.S. dollar directly.

First, through earlier debt harvesting, the U.S. induced foreign exchange depletion and hyperinflation in these countries, instilling a physiological fear of their own currencies among the populace. Then, Washington's think tanks launched a large-scale public relations campaign promoting "monetary stability theory," packaging the dollar as the only safe haven from turmoil.

When providing emergency loans, the U.S. often hinted, or even explicitly stated, that only by adopting the dollar could they gain long-term financial credibility. In 2000, teetering on the edge of social unrest, Ecuador was forced to announce the abandonment of its national currency; shortly after, El Salvador, Panama, and others followed suit.

This is a domineering logic: if a country no longer has its own currency, its economic sovereignty is essentially in a state of trusteeship. Abandoning the national currency is like handing over the keys to your house. From then on, your inflation rate, your interest rates, are all determined by others.

The third weapon is sanctions. This is the final, and most destructive, heavy weapon, specifically used against those attempting to break away from the orbit and challenge the existing order.

Take Venezuela as an example. The U.S. has imposed over 900 sanctions on it, targeting 209 key individuals, almost sealing off all avenues of survival for the country.

Venezuela is incredibly rich in oil—literally "swimming in oil." Its oil reserves amount to 303 billion barrels, more than Saudi Arabia's. However, the problem is that much of this oil is extra-heavy, asphalt-like crude, extremely difficult to extract, requiring external capital, technology, and diluents to monetize.

U.S. sanctions precisely severed these lifelines, leaving Venezuela sitting on the "world's largest oil vault" unable to cash in. The result was Venezuela's oil production plummeting from 3 million barrels per day to a low of less than 500,000 barrels per day within just seven years.

It wasn't until early 2026, when U.S. forces, citing "narcoterrorism" and related criminal charges, conducted a military operation in Venezuela to extract Maduro, and Trump announced that major oil companies would take over and invest billions to repair infrastructure, that the sanctions blade finally completed its closed loop.

First, use sanctions to completely paralyze a country's liquidity; then, under the banner of "management and restoration," enter the ruins with billions of dollars in hand, openly completing a new harvest of the global energy landscape.

Debt, dollarization, and sanctions—these three shackles constituted the U.S. financial blockade of Latin America for half a century. This net was once impenetrable, stretching from Mexico City all the way to Buenos Aires.

Three Variables

Today, a series of variables are eroding the foundations of imperial hegemony. The three once-unfailing weapons are losing their effectiveness amidst the shifting logic of global competition.

The loosening of the debt shackle began in the first decade of the 21st century. The biggest variable behind it is China.

In 2001, China joined the WTO, triggering a decade-long supercycle for commodities. Latin America, as a major global supplier of raw materials, became the biggest beneficiary of this feast.

Brazil's iron ore, Chile's copper, Argentina's soybeans flowed continuously to the East, bringing back unprecedented foreign exchange accumulation. This accumulation gave Latin American countries breathing room and the confidence to break free from the IMF's grip.

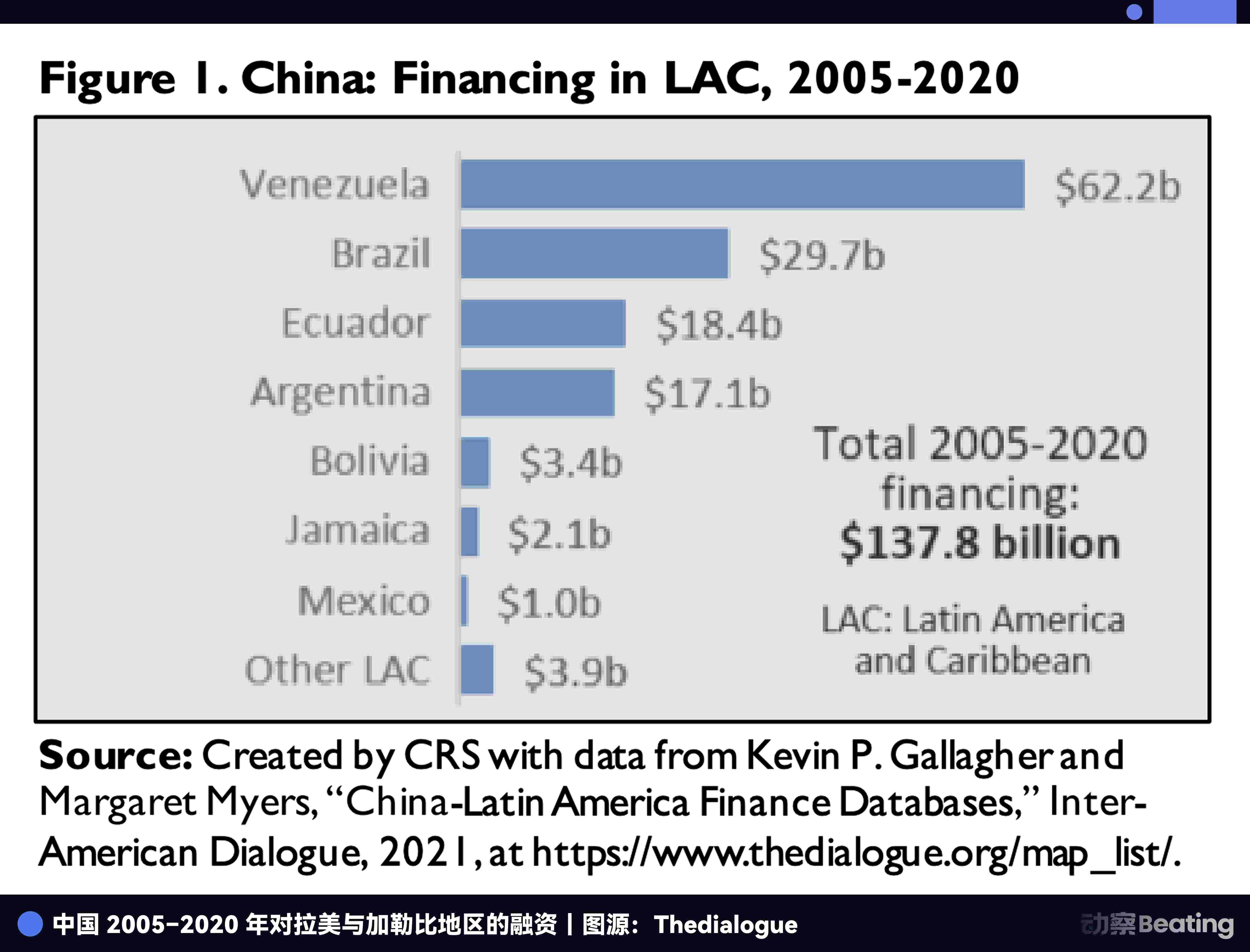

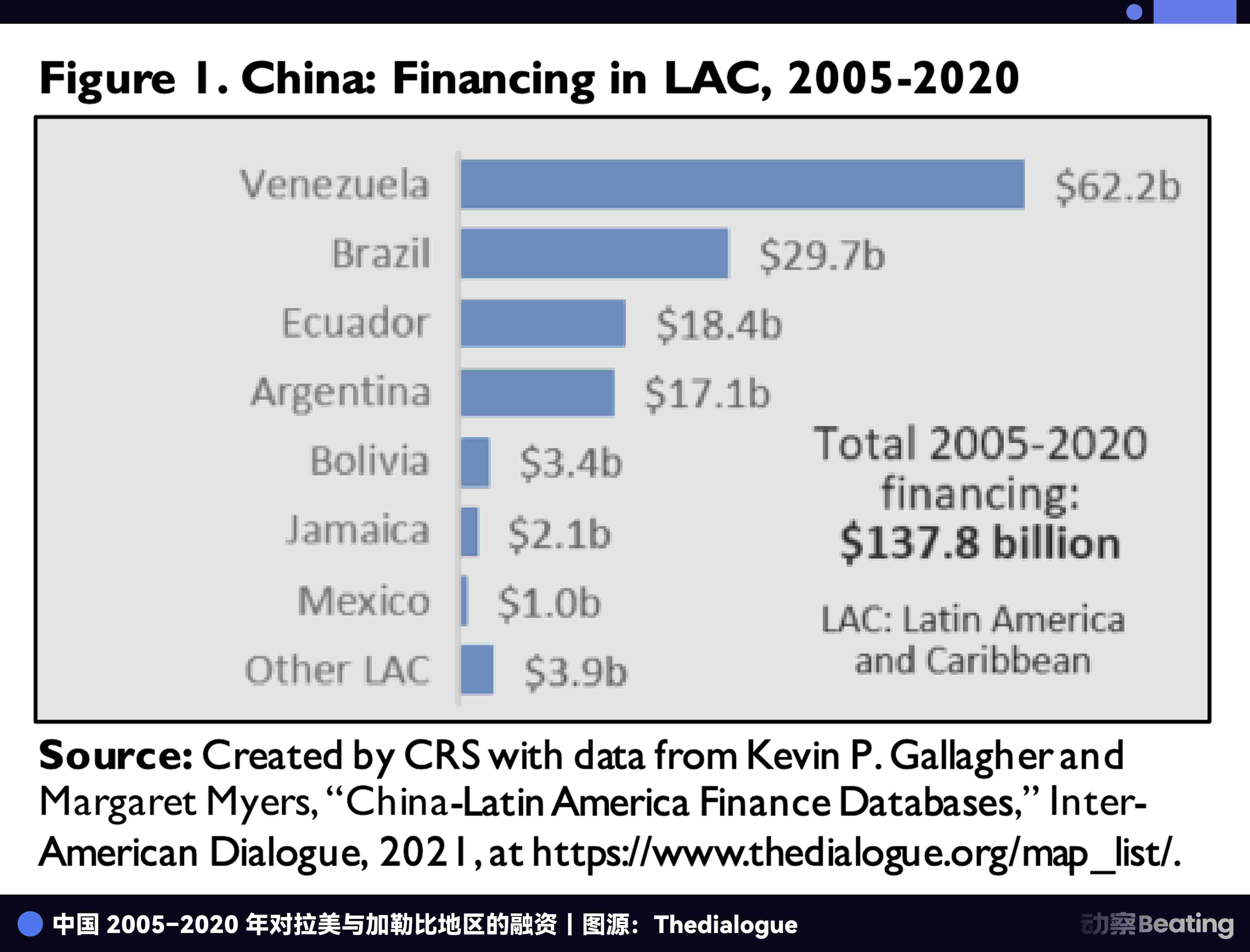

In 2005, Brazil and Argentina successively announced the early repayment of all their debts to the IMF. From 2005 to 2020, China provided Latin America with over $137 billion in loans without political strings attached.

Venezuela received $62 billion, with other major recipients including Brazil, Ecuador, and Argentina. These "oil-for-loans" agreements helped build much-needed infrastructure and gave these countries more bargaining chips in negotiations with Western creditors.

Meanwhile, Washington soon discovered it could not control these countries' economic policies through dollarization. The large-scale holding of dollars by Latin Americans was to hedge against the collapse of their national currencies, not out of yearning for the "American Dream." In the streets and alleys of Latin America, the dollar was stripped of its political color, reduced to a pure financial instrument—a reliable hard currency that wouldn't turn into worthless paper tomorrow.

This is the so-called "de-Americanized dollarization."

People need the stability of the dollar but reject Washington's rules. The dollar is becoming a global, neutral measure of value, much like gold. It belongs to the world, no longer solely to the U.S. government.

As vast amounts of dollar transactions spontaneously operate outside the official monitoring system, Washington finds that while it can still print money, it is increasingly difficult to manipulate other countries' economic lifelines through monetary leverage.

As debt and dollarization gradually lost their potency, the U.S. opted for more radical sanctions.

On one hand, Venezuela's internal governance failures and corruption led to the collapse of its economic pillar, rendering its national currency worthless amid hyperinflation. On the other hand, external sanctions directly caused its GDP to shrink by approximately 75%. It was precisely this sense of suffocation from internal and external pressures that gave rise to a parallel financial ecosystem completely independent of the dollar's closed loop.

Simultaneously, to avoid the risk of exorbitant U.S. fines, global major banks initiated a so-called "de-risking" movement, proactively severing business ties with Latin America. According to an Atlantic Council report, over 21 banks in the Caribbean lost correspondent banking relationships, with some countries even losing the ability to handle basic dollar-denominated trade and diaspora remittances.

This defensive financial exclusion did not reinforce the original hegemony; instead, it pushed more innocent individuals and businesses toward the emerging parallel financial ecosystem.

The Parallel Financial Ecosystem Beyond the Iron Curtain

In this game of financial sovereignty and survival instinct, Latin America's parallel financial ecosystem is being woven into a network independent of Washington's will by four forces: stablecoins, local Fintech, non-U.S. trade channels, and the underground economy.

In Latin America, stablecoins are no longer just chips for investment or speculation.

Take Venezuela as an example. To evade sanctions, the government established a shadow financial network. By December 2025, approximately 80% of the country's oil revenue was collected in the form of the stablecoin USDT.

Furthermore, intelligence suggests that through a gold refining and over-the-counter trading channel spanning Turkey and the UAE, Venezuela may have secretly amassed Bitcoin reserves worth up to $60 billion—a holding size comparable to MicroStrategy's.

However, this channel bypassing the SWIFT system, traversing Turkey and the UAE for gold and cryptocurrency, while technically evading sanctions, also became a key point of contention for Washington's accusations of illegal fund flows and support for drug trafficking due to its high level of opacity.

For ordinary Latin Americans, when traditional bank accounts were frozen due to sanctions, they bypassed the cumbersome and politically charged instructions of the settlement systems, directly moving funds across borders via blockchain.

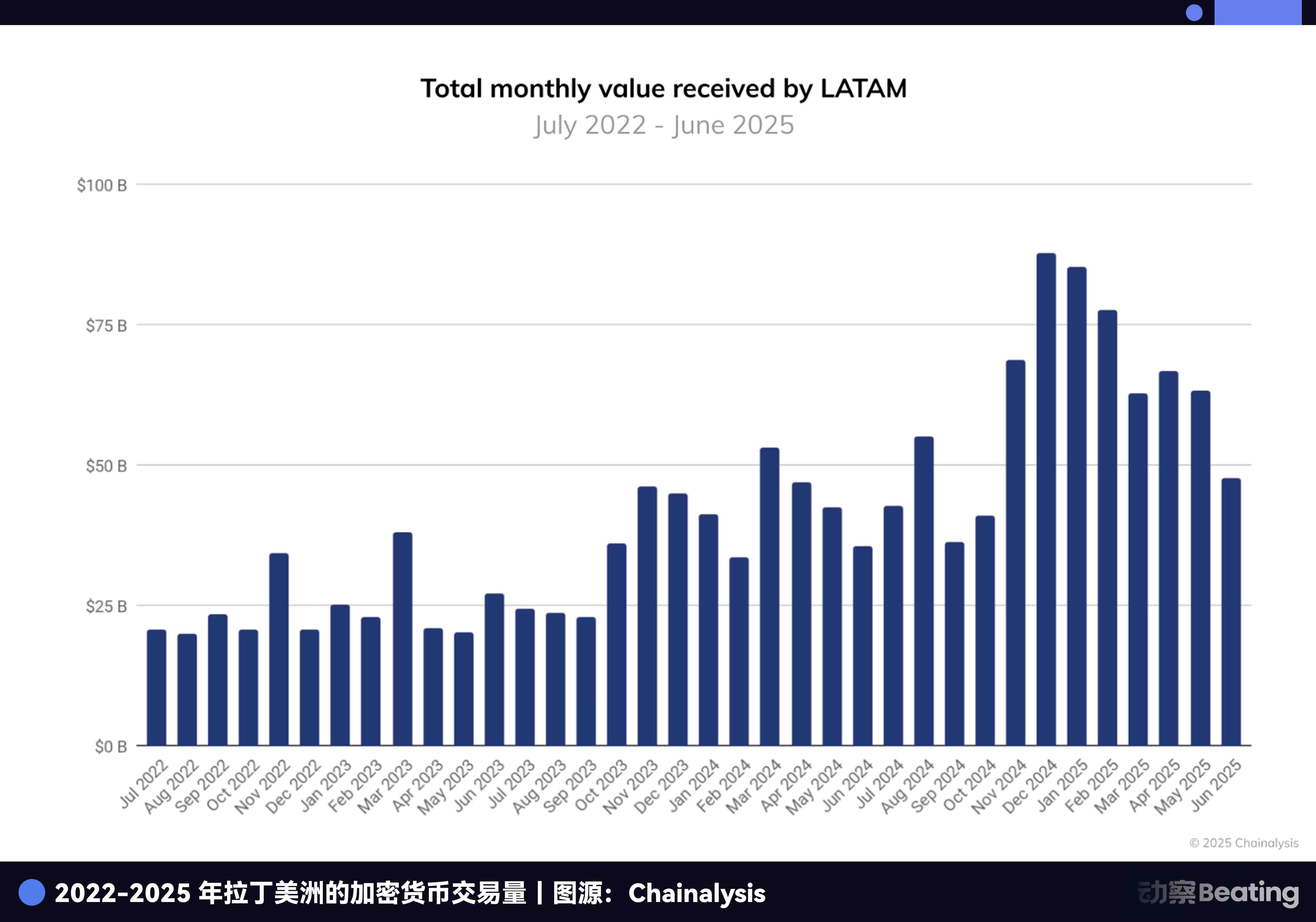

According to Chainalysis data, from 2022 to 2025, cryptocurrency transaction volume in Latin America approached $1.5 trillion. In Brazil, over 90% of transactions were related to stablecoins.

Unlike Manhattan bankers accustomed to looking down from above, local Fintech companies care more about the soil beneath their feet and concrete livelihoods. In Brazil, for instance, while only 60 million people own credit cards, the user base of the central bank-led Pix payment system surged to 170 million.

In 2024, Pix's total transaction volume reached a staggering $3.8 trillion, 1.7 times Brazil's GDP. Behind this figure lies an extreme push in capital turnover efficiency.

Meanwhile, digital banking giant Nubank grew its user base from 1.3 million to 114 million in just eight years, capturing over 60% of Brazil's adult population and achieving nearly $2 billion in net profit in 2024.

Payment giant Mercado Pago swept across Latin America with $142 billion in payment volume, while remittance market newcomer Bitso directly wrested a 4% share of the U.S.-Mexico remittance market from traditional giants like Western Union.

Additionally, non-dollar channels and the underground economy converged. The $5 billion currency swap between Argentina and China, along with the ongoing promotion of local currency settlement between China and Brazil, is becoming a symmetrical choice amid great power competition. This top-level decoupling is granting Latin American trade a breathing space independent of the dollar.

On the streets of Argentina, a black-market exchange rate known as the "Blue Dollar" (Dólar Blue) has become the nation's economic barometer. Its vast gap with the official rate starkly reveals the bankruptcy of official credit and has spawned countless street currency exchangers called "little trees" (arbolitos) and specialized USDT trading spots known as "cryptocurrency caves" (cuevas cripto).

The penetrating power of stablecoins, the infiltration rate of local Fintech, the strategic choice of non-U.S. channels, and the wild growth of the underground economy together weave this financial network free from centralized control.

Who is Handing Over the Knife?

The breakthrough of any species requires not only an internal will to survive but also often a drastic catalyst from the external environment. The driving force behind the rise of Latin America's parallel financial system ironically comes from the United States, which seeks to defend the old order.

A series of Washington's maneuvers have not only failed to stifle the sprouts of the new order but have instead provided the most fertile ground for its expansion.

The first thrust comes from politicians' forced conscription of financial pipelines.

The Trump administration once proposed a 1% tax on remittances sent from the U.S. This might seem like a minor levy, but against the backdrop of Latin America's annual remittance volume exceeding $150 billion, it was enough to shake the lifelines of tens of millions of low-income families.

Consider that in traditional financial channels, sending $200 to Latin America could incur fees of $6–$8 taken by giants like Western Union alone.

This additional 1% tax became the last straw. This tax slip sent an extremely dangerous signal to every laborer: traditional remittance channels are not only expensive but can also become pawns in political games at any moment.

Trump may have thought he was building a financial wall, but objectively, he drove tens of millions of users to flee the old system, collectively rushing into the embrace of stablecoins and local Fintech. When the cost of survival is pushed to its limit by politics, users migrate at an unprecedented speed.

The second thrust stems from a severe rift among Wall Street elites over profit distribution.

As mentioned earlier, to comply with increasingly stringent anti-money laundering regulations, Wall Street giants initiated a "de-risking" movement, proactively severing business ties with "high-risk regions" like Latin America. As early as 2014, JPMorgan Chase closed tens of thousands of Latin American client accounts citing "excessive risk."

By the end of 2025, JPMorgan Chase, on one hand, froze the bank accounts of two stablecoin companies operating in Venezuela, BlindPay and Kontigo, playing the role of the dollar system's most loyal "gatekeeper." On the other hand, it was frantically hoarding physical precious metals to hedge against dollar risk.

Public data shows JPMorgan Chase has become the world's largest holder of physical silver. More intriguingly, JPMorgan Chase moved large quantities of silver from a deliverable status to a non-deliverable status.

This means this silver, while sitting in warehouses, is no longer allowed to be used to fulfill futures contract deliveries. In other words, JPMorgan Chase is taking these "chips" off the gambling table and locking them away in its own private backyard.

While the dollar's hegemony remains effective, these Wall Street elites aim to use the rules to maximize their financial control. But simultaneously, they are also preparing for the eventual collapse of this system. JPMorgan Chase is both the number one defender of the existing dollar system and its biggest "internal short seller."

Thus, the more the U.S. tries to tighten the dollar's reins, the more the dollar leaps over the fence in a wild manner, seeking safer pastures. When core players within a system begin preparing for a post-dollar era, this control inevitably turns into its opposite.

The Curse of Hegemony

This dilemma of "control" and "loss of control" is not unique to this era. If we cast our gaze back to the fog-laden 19th century, in the long river of financial history, we can hear a distant and similar echo—the decline of the British pound.

Throughout that long century, the pound sterling was the undisputed world currency. But when a currency truly belongs to the world, it no longer completely belongs to its home country.

To export pounds globally, Britain was forced to maintain a chronic trade deficit, a cost that directly led to the hollowing out of its manufacturing sector and the slow decline of its national power. In 1931, after three devastating runs on its gold reserves, Britain was forced to abandon the gold standard, and sterling's hegemony fell from its pedestal.

The British Empire paid a century's tuition to learn a lesson: the more you try to use a currency's status to harvest the world, the more you accelerate the depletion of its vitality.

Today, the U.S. dollar is stepping into the same dilemma.

The more Washington tries to weaponize the dollar, using sanctions, taxes, and stringent regulations to encircle and intercept, the more likely the dollar is to accelerate its flight from home. You build the overt plank road, while the populace secretly crosses at Chencang.

Stablecoins, local Fintech, non-U.S. trade channels, the wildly growing underground economy... these diverse choices are essentially covert paths for the dollar to escape Washington's grasp.

From the near-obsessive hoarding of physical gold by central banks in recent years to the locking away of physical assets by top financial capital, this collective choice is tilting the global financial center of gravity back toward the era of hard assets.

This transformation is not occurring amidst the total collapse of the old empire but is being deconstructed spontaneously by hundreds of millions of micro-individuals and enterprises during America's surface prosperity.

The echoes of history are already circling over Washington, ringing loud and clear.