Galaxy's 26 Predictions: Bitcoin Will Still Reach $250,000 Next Year and Reach $250,000 the Year After.

- 核心观点:Galaxy Research发布2026年加密市场26项预测。

- 关键要素:

- 比特币2027年底目标价25万美元。

- 稳定币交易量将超越ACH支付系统。

- DEX现货交易量占比将超25%。

- 市场影响:描绘行业长期发展趋势与潜在增长点。

- 时效性标注:长期影响。

Original author: Galaxy

Original article translated by: Deep Tide TechFlow

introduction

Somewhat predictably, Bitcoin appears poised to end 2025 at roughly the same price level as at the beginning of the year.

The cryptocurrency market experienced a genuine bull run in the first ten months of the year. Regulatory reforms made progress, ETFs continued to attract inflows, and on-chain activity increased. Bitcoin (BTC) hit an all-time high of $126,080 on October 6th.

However, the market's euphoria failed to deliver the expected breakthrough, instead being defined by rotation, repricing, and readjustment. A combination of macroeconomic disappointments, a shift in investment narrative, leveraged liquidations, and massive whale selling threw the market into disarray. Prices declined, confidence cooled, and by December, BTC had fallen back to just over $90,000, though the process was far from smooth.

While 2025 may end with a price decline, it still witnessed genuine institutional adoption and laid the foundation for the next phase of practical implementation in 2026. We anticipate that in the coming year, stablecoins will surpass traditional payment networks, asset tokenization will emerge in mainstream capital and collateral markets, and enterprise-grade Level 1 (L1) chains will move from pilot phases to actual settlement. Furthermore, we expect public chains to rethink their value capture methods, DeFi and prediction markets will continue to expand, and AI-driven payments will finally be realized on-chain.

Below are Galaxy Research's 26 predictions for the crypto market in 2026, along with a review of last year's predictions.

2026 forecast

Bitcoin price

Bitcoin will reach $250,000 by the end of 2027 .

The market in 2026 is too volatile and unpredictable, but the possibility of Bitcoin reaching a new all-time high in 2026 remains. Current options markets show roughly equal probabilities of Bitcoin reaching $70,000 or $130,000 by the end of June 2026, and equally probable probabilities of reaching $50,000 or $250,000 by the end of 2026. These broad price ranges reflect the uncertainty surrounding the market in the short term. As of this writing, the entire crypto market is deeply mired in a bear market, and Bitcoin has yet to re-establish its bullish momentum. We believe downside risks remain in the short term until Bitcoin prices stabilize in the $100,000 to $105,000 range. Other factors in the broader financial markets also add to the uncertainty, such as the pace of AI capital expenditure deployment, monetary policy conditions, and the US midterm elections in November.

Over the past year, we have observed a structural decline in Bitcoin's long-term volatility levels—partly due to the introduction of larger-scale covering options/Bitcoin yield generation programs. Notably, the Bitcoin volatility curve now prices the implied volatility of put options higher than that of call options, a situation that did not exist six months ago. In other words, we are evolving from a skew typically seen in developing, growth markets towards a market more aligned with traditional macro assets.

This maturation trend is likely to continue, regardless of whether Bitcoin falls further to near its 200-week moving average; the asset class is maturing and institutional adoption is steadily increasing. 2026 may be a lackluster year for Bitcoin, and whether it ends the year at $70,000 or $150,000, our (long-term) bullish outlook for Bitcoin will only strengthen. With increased institutional access, looser monetary policy, and strong market demand for non-dollar safe-haven assets, Bitcoin is likely to follow gold's lead and gain widespread acceptance as a hedge against currency devaluation within the next two years.

—Alex Thorn

Layer-1 and Layer-2

Solana's total market capitalization in the Internet Capital Market is expected to surge to $2 billion (currently around $750 million).

Solana's on-chain economy is maturing, evidenced by its successful shift from meme-driven activities to a platform launching with a business model focused on real revenue. This transformation is driven by improvements in Solana's market structure and increased demand for tokens with fundamental value. As investors increasingly favor sustainable on-chain businesses over fleeting meme cycles, the internet capital markets will become a core pillar of Solana's economic activity.

—Lucas Tcheyan

At least one general-purpose Layer-1 blockchain will be embedded with revenue-generating applications that can directly generate value for its native token.

As more projects rethink how L1 captures and sustains value, blockchains are moving towards more explicitly designed functionalities. Hyperliquid's success in embedding a revenue model in its perpetual contract exchange, and the trend of economic value capture shifting from the protocol layer to the application layer (the "fat application theory"), are redefining expectations for neutral underlying chains. More and more chains are exploring whether certain revenue-generating infrastructure should be directly embedded into the protocol to strengthen token economic models. Ethereum founder Vitalik Buterin's recent call for low-risk, economically meaningful DeFi to prove ETH's value further underscores the pressure on L1. MegaEth plans to launch a native stablecoin that returns revenue to validators, while Ambient's AI-focused L1 plans to internalize inference fees. These examples demonstrate that blockchains are increasingly willing to control and monetize key applications. In 2026, a major L1 may formally embed a revenue-generating application at the protocol layer, directly channeling its economic benefits to the native token.

—Lucas Tcheyan

Solana's inflation reduction proposal for 2026 will not pass, and the existing proposal SIMD-0411 will be withdrawn.

Solana's inflation rate has been a focal point of community debate over the past year. Despite the introduction of a new inflation reduction proposal (SIMD-0411) in November 2025, a consensus on the optimal solution has yet to be reached. Instead, a view has gradually emerged that inflation has distracted from more important priorities, such as the implementation of Solana market microstructural adjustments. Furthermore, changes to Solana's inflation policy could impact its future market perception as a neutral store of value and monetary asset.

—Lucas Tcheyan

Enterprise-level L1 will move from the pilot phase to a true settlement infrastructure.

At least one Fortune 500 bank, cloud service provider, or e-commerce platform is expected to launch a branded enterprise-grade L1 blockchain in 2026, settling over $1 billion in real-world economic activity while running production-grade bridges connecting to public DeFi. While previous enterprise blockchains were largely internal experiments or marketing campaigns, the next wave will be closer to application-specific underlying chains designed for specific verticals. The validation layer will be licensed by regulated issuers and banks, while the public chain will be used for liquidity, collateral, and price discovery. This will further highlight the difference between neutral public L1 and enterprise-grade L1 that integrates issuance, settlement, and distribution capabilities.

— Christopher Rosa

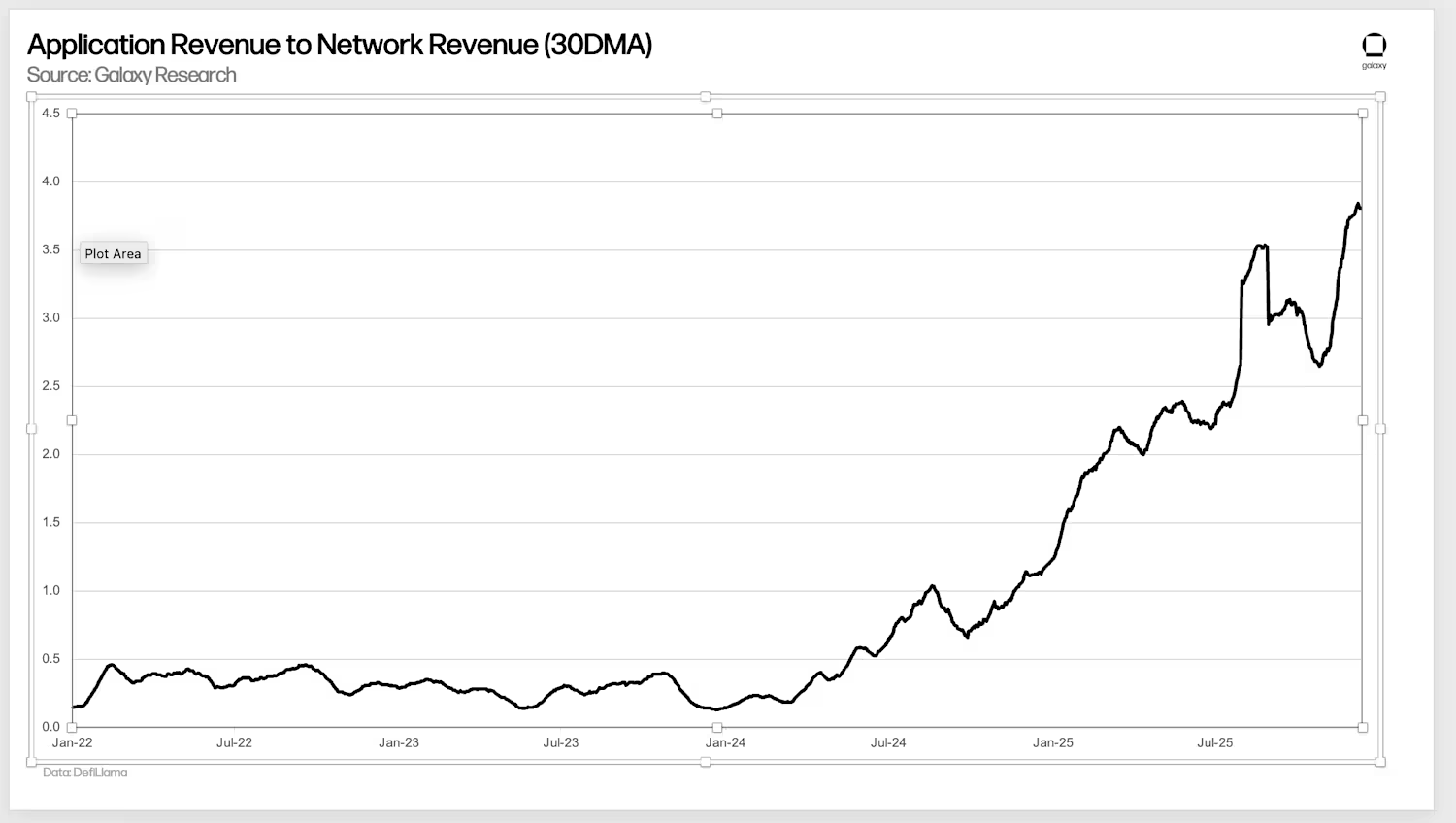

The ratio of application layer revenue to network layer revenue will double by 2026.

As transactions, DeFi, wallets, and emerging consumer applications continue to dominate on-chain fee generation, value capture is shifting from the underlying infrastructure to the application layer. Simultaneously, the network is structurally reducing MEV (Miner Extractable Value) leakage and pursuing fee compression at L1 and L2, leading to a shrinking revenue base at the infrastructure layer. This will accelerate value capture at the application layer, allowing the "fat application theory" to continue to outperform the "fat protocol theory."

—Lucas Tcheyan

Stablecoins and Asset Tokenization

The U.S. Securities and Exchange Commission (SEC) will provide some exemption for the use of tokenized securities in DeFi.

The U.S. Securities and Exchange Commission (SEC) will offer some form of exemption to allow the development of an on-chain tokenized securities market. This could take the form of a so-called "no-action letter" or a new "innovation exemption," a concept repeatedly mentioned by SEC Chairman Paul Atkins. This would allow legitimate, unpackaged on-chain securities to enter the DeFi market, rather than simply using blockchain technology for back-office capital market activities, as seen in the recent DTCC "no-action letter." Early stages of formal rulemaking are expected to begin in the second half of 2026, establishing rules for brokers, dealers, exchanges, and other traditional market participants using cryptocurrencies or tokenized securities.

—Alex Thorn

The U.S. Securities and Exchange Commission will face lawsuits from traditional market participants or industry organizations over the "innovation exemption" program.

Whether it's trading firms, market infrastructure, or lobbying firms, certain parts of traditional finance or banking will challenge regulators' granting of exemptions to DeFi applications or crypto companies, arguing that they have failed to develop comprehensive rules to regulate the expansion of tokenized securities.

—Alex Thorn

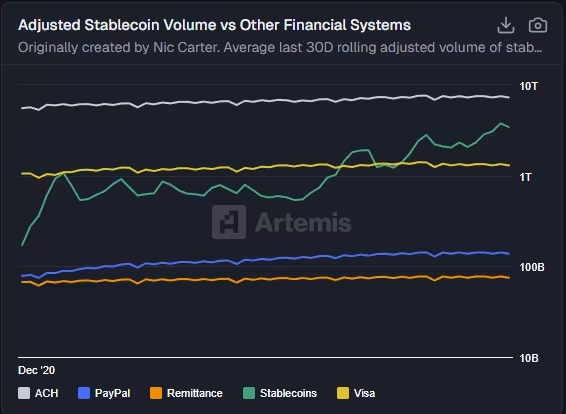

Stablecoin trading volume will surpass that of the ACH system.

Compared to traditional payment systems, stablecoins offer significantly higher velocity of money. We've already seen stablecoin supply grow at a compound annual growth rate (CAGR) of 30-40%, with transaction volume increasing accordingly. Stablecoin transaction volume has already surpassed that of major credit card networks like Visa and currently processes approximately half the transaction volume of the Automated Clearing House (ACH) system. With the definition of the GENIUS Act finalized in early 2026, we may see stablecoin growth exceed its historical average growth rate, as existing stablecoins continue to grow and new entrants compete for this expanding market share.

— Thad Pinakiewicz

Stablecoins that partner with traditional finance (TradFi) will accelerate integration.

Despite the launch of numerous stablecoins in the US by 2025, the market struggles to support a large number of widely adopted options. Consumers and merchants will not use multiple digital dollars simultaneously; they will tend to choose one or two of the most widely accepted stablecoins. We have already seen this consolidation trend in the collaborations of major institutions: nine major banks (including Goldman Sachs, Deutsche Bank, Bank of America, Santander, BNP Paribas, Citigroup, MUFG Bank, TD Bank Group, and UBS) are exploring plans to launch stablecoins based on G7 currencies; PayPal and Paxos have partnered to launch PYUSD, combining a global payments network with a regulated issuer.

These cases demonstrate that success hinges on the scale of distribution, specifically the ability to integrate with banks, payment processors, and enterprise platforms. It is anticipated that more stablecoin issuers will collaborate or integrate systems in the future to compete for meaningful market share.

— Jianing Wu

A major bank or brokerage firm will accept tokenized shares as collateral.

To date, tokenized stocks have remained on the fringes, confined to DeFi experiments and private blockchains piloted by major banks. However, core infrastructure providers in traditional finance are now accelerating their transition to blockchain-based systems, with increasing regulatory support. In the coming year, we may see a major bank or brokerage begin accepting tokenized stocks as on-chain deposits, treating them as assets fully equivalent to traditional securities.

— Thad Pinakiewicz

The card payment network will be connected to a public blockchain.

At least one of the world's top three card payment networks will settle more than 10% of its cross-border transaction volume via public blockchain stablecoins by 2026, although most end users may not have access to the cryptocurrency interface. Issuers and acquirers will still display balances and liabilities in traditional formats, but in the background, a portion of net settlements between regional entities will be completed via tokenized US dollars to reduce settlement deadlines, upfront funding needs, and correspondent banking risks. This development will make stablecoins a core financial infrastructure of existing payment networks.

— Christopher Rosa

DEFI

Decentralized exchanges (DEXs) will account for more than 25% of spot trading volume by the end of 2026.

While centralized exchanges (CEXs) still dominate liquidity and drive new user traffic, structural changes are driving increasing spot trading activity onto-chain. Two of the most obvious advantages of decentralized exchanges (DEXs) are the absence of KYC (Know Your Customer) access and a more economically efficient fee structure, making them increasingly attractive to users and market makers seeking lower friction and greater composability. Currently, spot trading volume on DEXs accounts for approximately 15%-17%, depending on the data source.

—Will Owens

The assets of a DAO governed under the Futarchy model will exceed $500 million.

Based on our prediction a year ago that futarchy (future markets) would see wider adoption as a governance mechanism, we now believe it has demonstrated sufficient effectiveness in real-world applications for Decentralized Autonomous Organizations (DAOs) to begin using it as the sole decision-making system for capital allocation and strategic direction. Therefore, we project that by the end of 2026, the total assets of DAO treasuries governed through the futarchy model will exceed $500 million. Currently, approximately $47 million of DAO treasury assets are fully governed through the futarchy model. We believe this growth will primarily come from newly established futarchy DAOs, while the growth of existing futarchy DAO treasuries will also play a role.

—Zack Pokorny

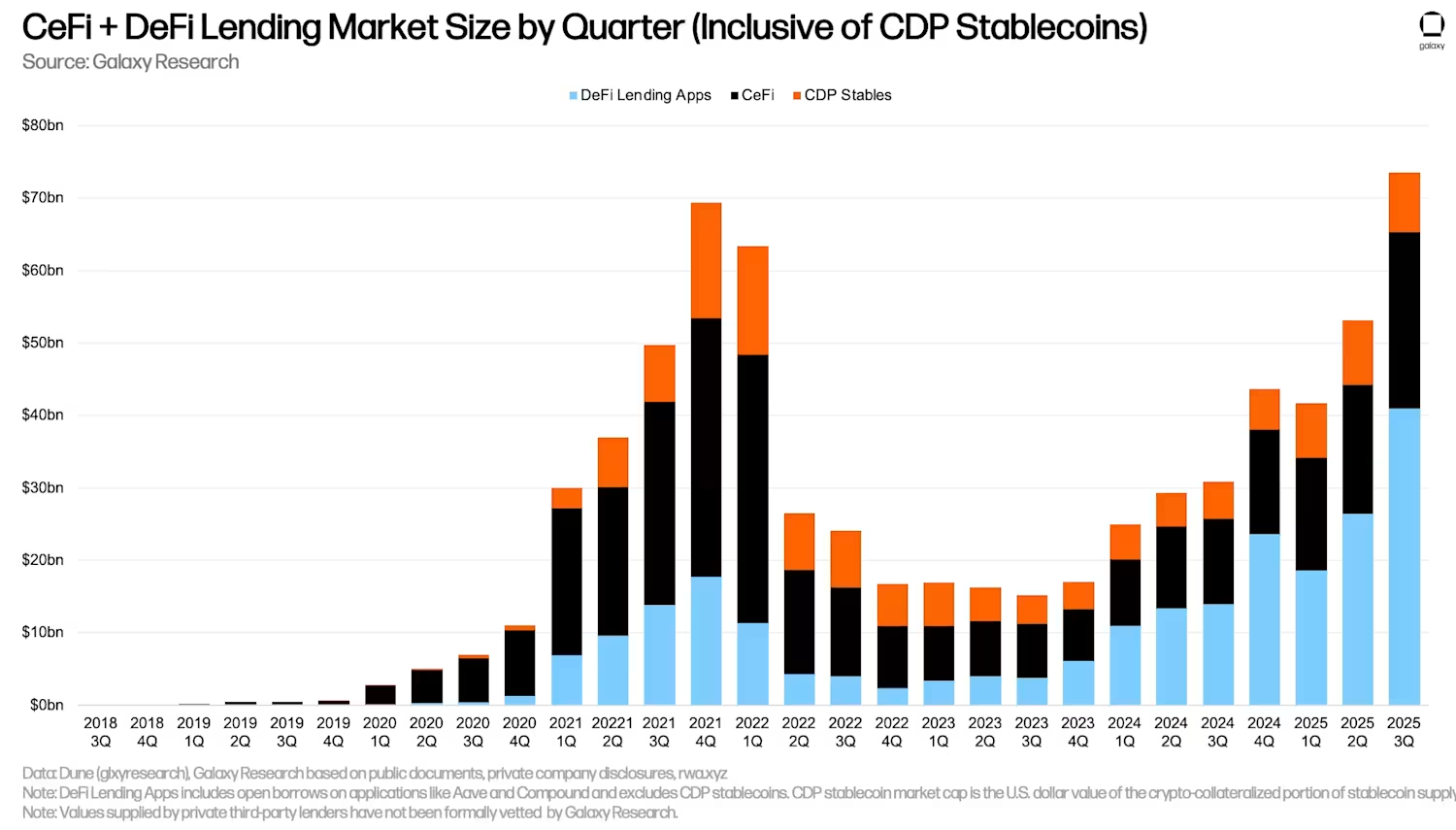

The total outstanding balance of crypto-secured loans will surpass $90 billion in the quarterly snapshot.

Following the growth momentum of 2025, the total volume of crypto-collateralized loans in decentralized finance (DeFi) and centralized finance (CeFi) is expected to continue to expand in 2026. On-chain dominance (i.e., the share of loans issued through decentralized platforms) will continue to rise as institutional participants increasingly rely on DeFi protocols for lending activities.

—Zack Pokorny

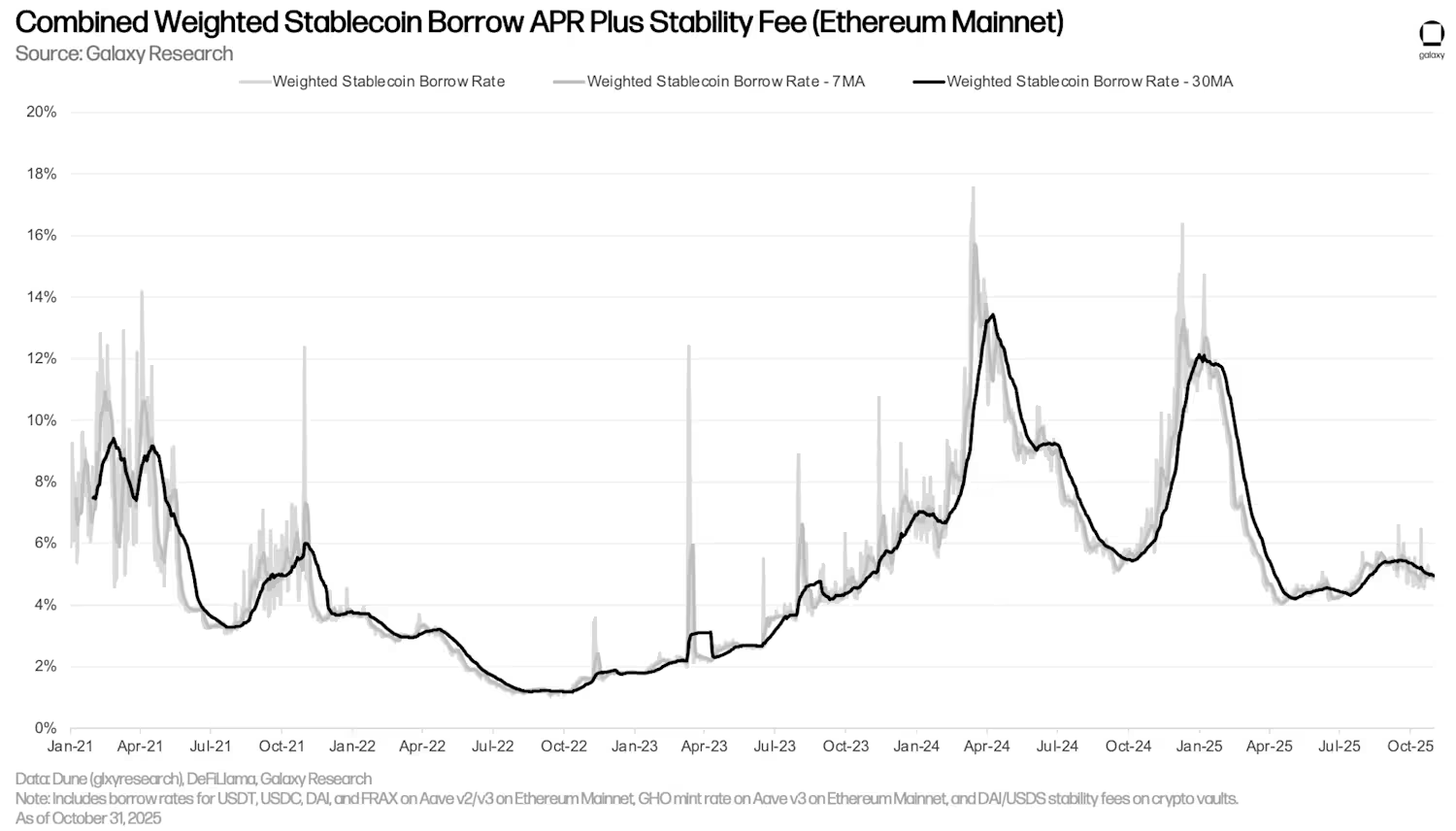

Stablecoin interest rate volatility will remain moderate, and DeFi lending costs will not exceed 10%.

As institutional participation in on-chain lending grows, we expect deeper liquidity and more stable, slower-moving capital to significantly reduce interest rate volatility. Simultaneously, on-chain and off-chain rate arbitrage becomes easier, while the barrier to entry for DeFi is increasing. Off-chain rates are projected to decline further in 2026, keeping on-chain lending rates low—a crucial floor even in a bull market.

The core argument is:

(1) Institutional capital has brought stability and sustainability to the DeFi market;

(2) The declining off-chain interest rate environment will cause on-chain interest rates to fall below the typical level during the expansion period.

—Zack Pokorny

The total market capitalization of privacy tokens will exceed $100 billion by the end of 2026.

In the fourth quarter of 2025, privacy tokens gained significant market attention, with on-chain privacy becoming a focal point as investors deposited more funds on-chain. Among the top three privacy tokens, Zcash rose by approximately 800% in the quarter, Railgun by approximately 204%, while Monero saw a more modest increase of 53%. Early Bitcoin developers, including the pseudonymous founder Satoshi Nakamoto, explored ways to make transactions more private or even completely anonymous, but at that time, practical zero-knowledge techniques were not widely available or ready for deployment.

As more and more funds are stored on-chain, users (especially institutions) are beginning to question whether they really want their crypto asset balances to be fully publicly visible. Whether a completely anonymous design or a mixer-style approach ultimately prevails, we expect the total market capitalization of privacy tokens to exceed $100 billion by the end of 2026, compared to a current valuation of approximately $63 billion on CoinMarketCap.

— Christopher Rosa

Polymarket's weekly trading volume is projected to consistently exceed $1.5 billion by 2026.

Prediction markets have become one of the fastest-growing categories in the crypto space, with Polymarket's weekly nominal trading volume approaching $1 billion. We expect this figure to stabilize above $1.5 billion by 2026, thanks to improved liquidity from the new capital efficiency layer and increased trading frequency from AI-driven order flow. Polymarket's distribution capabilities are also continuously improving, accelerating capital inflows.

—Will Owens

TradFi

More than 50 spot altcoin ETFs and another 50 crypto ETFs (excluding single spot token products) will be launched in the United States.

With the U.S. Securities and Exchange Commission (SEC) approving the Common Listing Standard, we expect the pace of spot altcoin ETF launches to accelerate in 2026. In 2025, over 15 spot ETFs for Solana, XRP, Hedera, Dogecoin, Litecoin, and Chainlink were already listed. We anticipate that other major assets will follow suit with spot ETF applications. In addition to single-asset products, we also expect multi-asset crypto ETFs and leveraged crypto ETFs to launch. With over 100 applications in progress, we anticipate a continued influx of new products in 2026.

— Jianing Wu

Net inflows into US spot crypto ETFs will exceed $50 billion.

In 2025, US spot crypto ETFs attracted $23 billion in net inflows. We expect this figure to accelerate in 2026 as institutional adoption deepens. With financial services firms removing restrictions on advisor-recommended crypto products and major platforms that were previously hesitant about crypto (such as Vanguard) joining crypto funds, inflows into Bitcoin and Ethereum will surpass 2025 levels and enter the portfolios of more investors. Furthermore, the launch of numerous new crypto ETFs, especially spot altcoin products, will release pent-up demand and drive additional inflows in the early stages of distribution.

— Jianing Wu

A major asset allocation platform will include Bitcoin in its standard model portfolio.

With three of the Big Four financial services firms (Wells Fargo, Morgan Stanley, and Bank of America) removing restrictions on advisory recommendations for Bitcoin and supporting allocations of 1%-4%, the next step is to include Bitcoin products on their recommendation lists and incorporate them into formal research coverage, which will significantly increase their visibility among clients. The ultimate goal is to include Bitcoin in model portfolios, which typically requires higher assets under management (AUM) and consistent liquidity, but we expect Bitcoin funds to meet these thresholds and enter model portfolios with a strategic weight of 1%-2%.

— Jianing Wu

More than 15 crypto companies will go public or upgrade their listing in the United States.

In 2025, 10 crypto-related companies (including Galaxy) successfully went public or upgraded to a US listing. Since 2018, over 290 crypto and blockchain companies have completed private funding rounds exceeding $50 million. With easing regulatory conditions, we believe a large number of companies are now poised to seek US listings to access the US capital markets. Among the most likely candidates, we anticipate CoinShares (if it does not go public in 2025), BitGo (which has filed for listing), Chainalysis, and FalconX will move towards going public or upgrading to a US listing in 2026.

— Jianing Wu

More than five digital asset treasury companies (DATs) will be forced to sell assets, be acquired, or shut down completely.

The second quarter of 2025 saw a surge in the formation of Digital Asset Treasury Companies (DATs). Starting in October, their market capitalization-to-net-value (mNAV) multiples began to compress. As of this writing, Bitcoin, Ethereum, and Solana DATs are trading at an average mNAV of less than 1. During the initial boom, many companies from different business lines quickly transitioned to DATs to capitalize on market conditions. The next phase will differentiate between sustainable DATs and those lacking a coherent strategy or asset management capabilities. To succeed in 2026, DATs need robust capital structures, innovative liquidity management and yield generation methods, and strong synergies with relevant protocols (if not already established). Scale advantages (such as Strategy's large Bitcoin holdings) or geographic advantages (such as Metaplanet in Japan) could provide additional competitive advantages. However, many DATs that initially flooded the market lacked adequate strategic planning. These DATs will struggle to maintain mNAV and may be forced to sell assets, be acquired by larger players, or even shut down entirely in the worst-case scenario.

— Jianing Wu

policy

Some Democrats will focus on the issue of "de-banking" and gradually accept cryptocurrency as a solution.

While unlikely, this scenario warrants attention: In late November 2025, the Financial Crimes Enforcement Network (FinCEN), a division of the U.S. Treasury Department, urged financial institutions to be “vigilant about suspicious activity related to cross-border money transfers involving undocumented immigrants.” Although the warning primarily highlighted risks such as human and drug trafficking, it also noted the responsibility of money service businesses (MSBs) to file Suspicious Activity Reports (SARs), including cross-border money transfers related to income from undocumented employment. This could cover remittances sent back by undocumented immigrants—such as plumbers, farm workers, or restaurant servers—a group of immigrants who, despite their work violating federal law, still enjoy sympathy from left-wing voters.

This warning follows FinCEN's earlier Geographic Targeting Order (GTO), which requires MSBs to automatically report cash transactions in designated border counties, with a threshold as low as $1,000 (far below the statutory $10,000 threshold for currency transaction reporting). These measures broaden the scope of everyday financial activities that could trigger federal reporting, increasing the likelihood that immigrants and low-income workers face funds freezes, denial of service, or other forms of financial exclusion. These situations may garner more sympathy from some pro-immigration Democrats regarding the issue of "debanking" (an issue primarily focused on by the right wing in recent years) and make them more accepting of license-free, censorship-resistant financial networks.

Conversely, populist, pro-bank, and rule-of-law Republicans may begin to dislike cryptocurrencies for the same reasons, despite strong support for the industry from the Trump administration and the Republican innovator wing. The ongoing work by federal banking regulators to modernize Bank Secrecy Act and anti-money laundering compliance requirements will only further draw attention to the inherent trade-offs between financial inclusion policy goals and crime reduction—trade-offs that different political factions prioritize differently. If this political reshuffling materializes, it will demonstrate that blockchain does not have a fixed political camp. Its permissionless design means that acceptance or opposition to it is not based on ideology, but rather on how it influences the political priorities of different groups across different eras.

—Marc Hochstein

The United States will launch a federal investigation into insider trading or match-fixing related to prediction markets.

With US regulators giving the green light to on-chain prediction markets, trading volume and open interest have surged. Simultaneously, several scandals have surfaced, including allegations of insiders using private information to gain a competitive edge and federal raids on match-fixing rings in major sports leagues. Because traders can participate under pseudonyms without going through betting platforms that require Know Your Customer (KYC), insiders are now more susceptible to the temptation to exploit privileged information or manipulate the market. Therefore, we may see investigations triggered by unusual price fluctuations in on-chain prediction markets, rather than the routine monitoring of traditional regulated sports betting platforms.

— Thad Pinakiewicz

AI

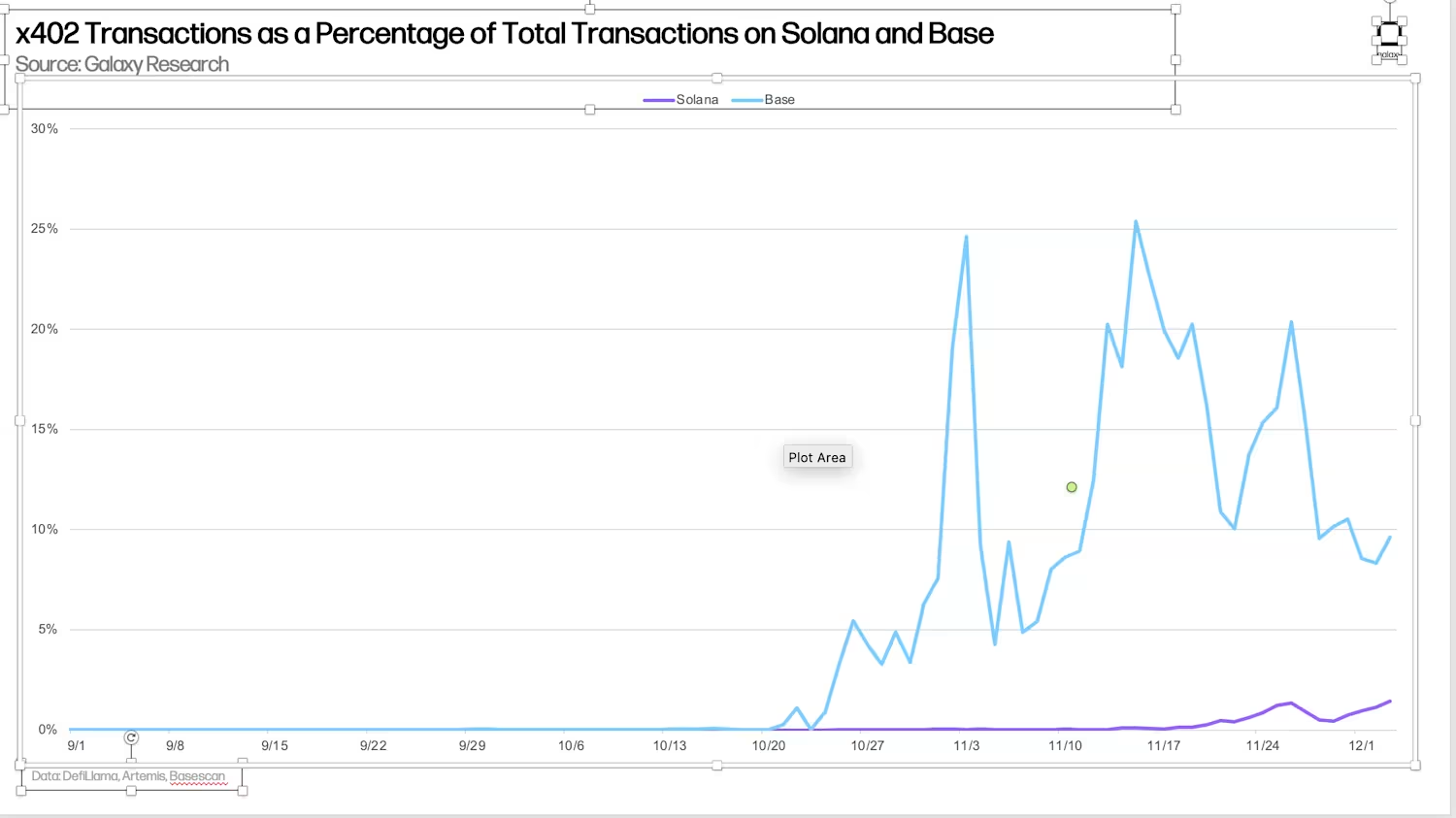

Payments based on the x402 standard will account for 30% of the daily transaction volume on the Base chain and 5% of the non-voting transaction volume on Solana, marking the widespread adoption of on-chain proxy interactions.

With the increasing intelligence of AI agents, the continued adoption of stablecoins, and improvements in developer tools, x402 and other proxy payment standards will drive a larger share of on-chain activity. As AI agents increasingly conduct transactions autonomously across various services, standardized payment primitives will become a core component of the execution layer.

Base and Solana have emerged as leading blockchains in this field—Base benefiting from Coinbase's significant role in the creation and promotion of the x402 standard, while Solana stands out thanks to its large developer community and user base. Furthermore, we anticipate rapid growth in emerging payment-specific blockchains like Tempo and Arc, driven by agent-driven business models.

—Lucas Tcheyan

A Look Back at 2025 Predictions: The Gains and Losses of Bitcoin and the Crypto Market

At the end of 2024, there was boundless optimism surrounding the future of Bitcoin and cryptocurrencies. The new presidential administration pledged to end the "enforcement-style regulation" of the Biden administration, while incoming President Trump promised to make the United States the "crypto capital of the world." With a month to go before the president's second inauguration, going long on Bitcoin became the most popular trade globally.

On December 31, 2024, we released 23 predictions for 2025, anticipating further expansion of market breadth and narratives throughout the year. Some of these predictions came true perfectly, while others deviated significantly. For many of these predictions, our team was on the right track, but not entirely accurate. From the resurgence of on-chain revenue sharing to the expanding role of stablecoins and the steady progress in institutional adoption, the major trends we identified continue to evolve.

Below, we examine our 23 predictions for 2025 and assess their accuracy. If we underestimated one theme for 2025, it's the surge in digital asset treasury companies (DATs). While this boom may have been brief in the summer of 2025, its impact cannot be ignored. We scrutinize our successes and failures against rigorous standards and offer commentary where appropriate.

Bitcoin

❌Bitcoin will break $150,000 in the first half of 2025 and test or exceed $185,000 in the fourth quarter.

Result: Bitcoin failed to break $150,000, but reached a new high of $126,000. In November, we lowered our year-end price target to $125,000. As of this writing, Bitcoin is trading between $80,000 and $90,000, and it seems unlikely that it will reach our updated year-end target for 2025.

—Alex Thorn

❌ By 2025, the total assets under management (AUM) of US spot Bitcoin ETPs will exceed $250 billion.

Results: As of November 12, AUM reached $141 billion, up from $105 billion on January 1, but failed to meet the forecast target.

—Alex Thorn

❌ In 2025, Bitcoin will once again become one of the best-performing risk-adjusted assets globally.

Result: This prediction was accurate for the first half of 2025. As of July 14, Bitcoin's year-to-date Sharpe ratio was 0.87, higher than the S&P 500, Nvidia, and Microsoft. However, Bitcoin is projected to end the year with a negative Sharpe ratio, failing to be one of the best-performing assets of the year.

—Alex Thorn

✅At least one top wealth management platform will announce recommendations to allocate 2% or more to Bitcoin.

Result: Morgan Stanley, one of the Big Four financial services firms, removed the restriction on advisors allocating Bitcoin to any account. That same week, Morgan Stanley released a report recommending a maximum allocation of 4% of portfolios to Bitcoin. Additionally, the Digital Assets Council of Financial Professionals, led by Ric Edelman, released a report recommending an allocation of 10%-40% to Bitcoin. Bridgewater Associates founder Ray Dalio also recommended allocating 15% of assets to Bitcoin and gold. —Alex Thorn

❌ Five Nasdaq 100 companies and five national or sovereign wealth funds will announce the inclusion of Bitcoin on their balance sheets.

Results: Currently, only three Nasdaq 100 companies hold Bitcoin. However, approximately 180 companies globally hold or have announced plans to purchase cryptocurrencies on their balance sheets, involving more than 10 different tokens. More than five countries have invested in Bitcoin through official reserves or sovereign wealth funds, including Bhutan, El Salvador, Kazakhstan, the Czech Republic, and Luxembourg. Digital Asset Treasury (DAT) companies are among the major institutional forces driving cryptocurrency purchases in 2025, particularly in the second quarter.

— Jianing Wu

❌Bitcoin developers will reach a consensus on the next protocol upgrade in 2025.

Result: Not only did a consensus fail to be reached on the next protocol upgrade, but a dispute also arose within the Bitcoin developer ecosystem regarding how to treat non-monetary transactions. In October 2025, the most widely used Bitcoin Core software released version 30, which controversially expanded the restrictions on the OP_RETURN field.

The expansion of this data field was intended to guide the most disruptive arbitrary data transactions to locations that cause the least harm to the blockchain, but this move sparked significant opposition within the Bitcoin community. In late October, an anonymous developer released a new Bitcoin Improvement Proposal (BIP) suggesting a “temporary soft fork” to “combat spam transactions.” While this proposal gradually lost momentum in the following months, the debate surrounding this issue essentially exhausted developers’ efforts to reach a consensus on other, more forward-looking upgrades. Although proposals like OP_CAT and OP_CTV still garnered some attention in 2025, unresolved governance issues prevented developers from reaching an agreement on the next major protocol upgrade by December.

—Will Owens

✅Of the top 20 listed Bitcoin mining companies by market capitalization, more than half will announce transformations or partnerships with hyperscale computing, artificial intelligence (AI), or high-performance computing (HPC) companies.

Result: Major mining companies have generally shifted to a hybrid AI/HPC mining model to more flexibly monetize their infrastructure investments. Of the top 20 publicly traded Bitcoin mining companies by market capitalization, 18 have announced plans to transition to AI/HPC as part of their business diversification efforts. The two companies that have not announced a transition are American Bitcoin (ABTC) and Neptune Digital Assets Corp (NDA.V).

— Thad Pinakiewicz

❌The Bitcoin DeFi ecosystem, which refers to the total amount of BTC locked in DeFi smart contracts and staking protocols, will nearly double by 2025.

Results: The amount of Bitcoin locked in DeFi grew by only about 30% in 2025 (from 134,987 BTC on December 31, 2024 to 174,224 BTC on December 3, 2025). This growth was primarily driven by lending activity, with Aave V3 Core adding 21,977 wrapped Bitcoins throughout the year, and Morpho adding 29,917. However, Bitcoin staking protocols, as a significant category, experienced capital outflows, losing over 13,000 wrapped Bitcoins.

—Zack Pokorny

ETH

❌Ethereum's native token ETH will break $5,500 in 2025.

Result: Ethereum's native token, ETH, briefly hit an all-time high in September 2025, but failed to break $5,000. Analysts believe that the price surge from April to the fall of 2025 was primarily due to purchasing activity by treasury companies like Bitminer. However, as the activity of these treasury companies subsided, the price of ETH declined, struggling to stay above $3,000 since October.

—Alex Thorn

❌Ethereum staking ratio will exceed 50% in 2025.

Results: Ethereum's staking ratio peaked at approximately 29.7% in 2025, up from 28.3% at the beginning of the year. In the past few months, ETH staking has been limited due to the unwinding of revolving transactions and a key reorganization of large validators, with both exiting and entering queues being disrupted.

—Zack Pokorny

❌ The ETH/BTC ratio will fall below 0.03 in 2025, while also breaking through 0.045.

Result: This prediction was nearly accurate. The ETH/BTC ratio fell to a low of 0.01765 on April 22, reaching the lower end of our prediction; while it rose to a high of 0.04324 on August 24, but failed to reach the upper end of our prediction of 0.045. Despite the rebound in the ETH/BTC ratio, it is still expected to close lower year-over-year for the full year.

—Alex Thorn

❌ Layer 2 (L2) overall economic activity will surpass Alt-L1 (which replaces the first layer blockchain) by 2025.

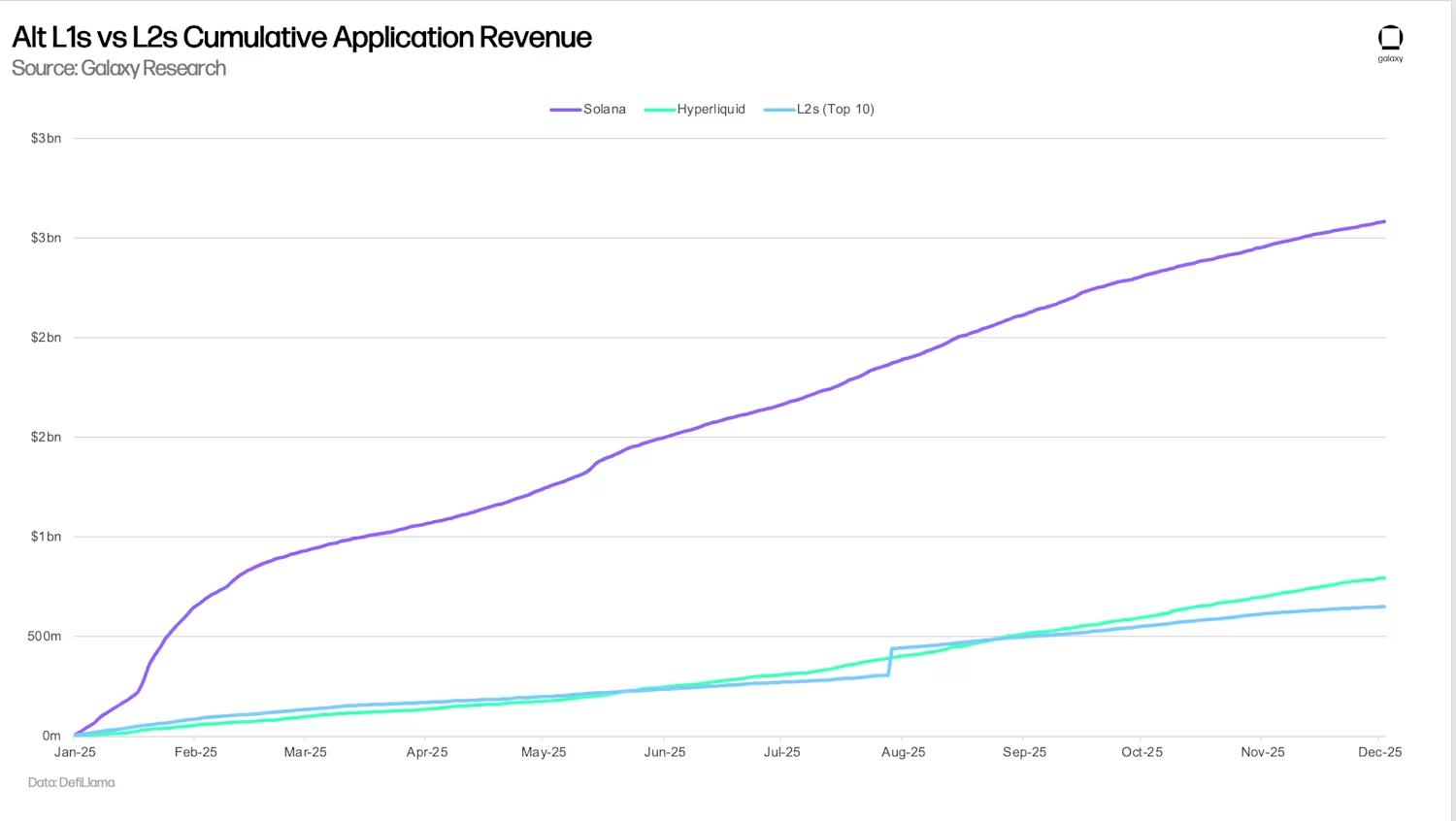

Result: This prediction failed to materialize. At both the network and application levels, Layer 2 as a whole underperformed major Alt-L1 chains. Solana solidified its position as the de facto retail speculative chain, consistently holding the largest share of trading volume and fee revenue across the industry. Meanwhile, Hyperliquid became the dominant platform for perpetual contract trading, with its single platform generating more cumulative application revenue than the entire Layer 2 ecosystem. While Base was the only Layer 2 chain approaching Alt-L1 level of appeal—accounting for nearly 70% of Layer 2 application revenue in 2025—even Base's growth was insufficient to surpass the economic dominance of Solana and Hyperliquid.

—Lucas Tcheyan

DeFi

✅ DeFi is entering a "dividend era," with on-chain applications distributing at least $1 billion in nominal value to users and token holders through treasury funds and revenue sharing.

Results: As of November 2025, at least $1.042 billion has been repurchased through app revenue. Hyperliquid and Solana-based apps are the projects that have repurchased the most tokens this year. Repurchase activities have become a major narrative this year, widely accepted by the market, and even rejected in some cases by projects that do not support such activities. To date, top apps alone have returned $818.8 million to end users. Hyperliquid is far ahead in this area, returning nearly $250 million through token buybacks.

—Zack Pokorny

✅ On-chain governance will see a revival, with applications experimenting with futarchy (future market) governance models, and the total number of active voters will increase by at least 20%.

Results: In 2025, the use of the futarchy model in DAO governance increased significantly. Optimism began experimenting with this concept, while the Solana-based MetaDAO introduced 15 DAOs within a year, including well-known organizations such as Jito and Drift. Currently, nine of these DAOs fully adopt the futarchy model for managing strategic decisions and capital allocation. Participation in these decision-making markets has grown exponentially, with one MetaDAO market reaching a trading volume of $1 million. Furthermore, nine of the top ten MetaDAO proposals by trading volume occurred this year. We have witnessed more and more DAOs using futarchy for strategic decision-making, and some DAOs launching purely on the futarchy model. However, the vast majority of futarchy experiments have taken place on the Solana network and are spearheaded by MetaDAO.

—Zack Pokorny

Banks and stablecoins

❌The world’s four largest custodian banks (Bank of New York Mellon, JPMorgan Chase, State Street, and Citigroup) will offer digital asset custody services in 2025.

Result: This prediction was nearly accurate. BNY Mellon did indeed launch its crypto custody service in 2025. State Street and Citigroup, while not yet launched, announced plans to offer the service in 2026. Only JPMorgan Chase remains cautious, with an executive telling CNBC in October, "Custody is not currently in our plans," but the large bank will participate in digital asset trading. In summary, three of the four major custodian banks have either offered or announced plans to offer crypto custody services.

—Alex Thorn

✅ At least 10 stablecoins backed by traditional financial (TradFi) partners will be launched.

Results: While some of these stablecoins have not yet officially launched, at least 14 major global financial institutions have announced plans. For example, in the US, JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo have formed a consortium of US banks planning to launch a joint stablecoin; there are also brokerage firms like Interactive Brokers, and payment and fintech companies like Fiserv and Stripe. The wave is even stronger outside the US, including Klarna, Sony Bank, and a global banking consortium of nine major banks. Furthermore, crypto-native stablecoin issuers like Ethena have joined the competition, partnering with federally regulated Anchorage to issue its native USDtb stablecoin.

— Jianing Wu

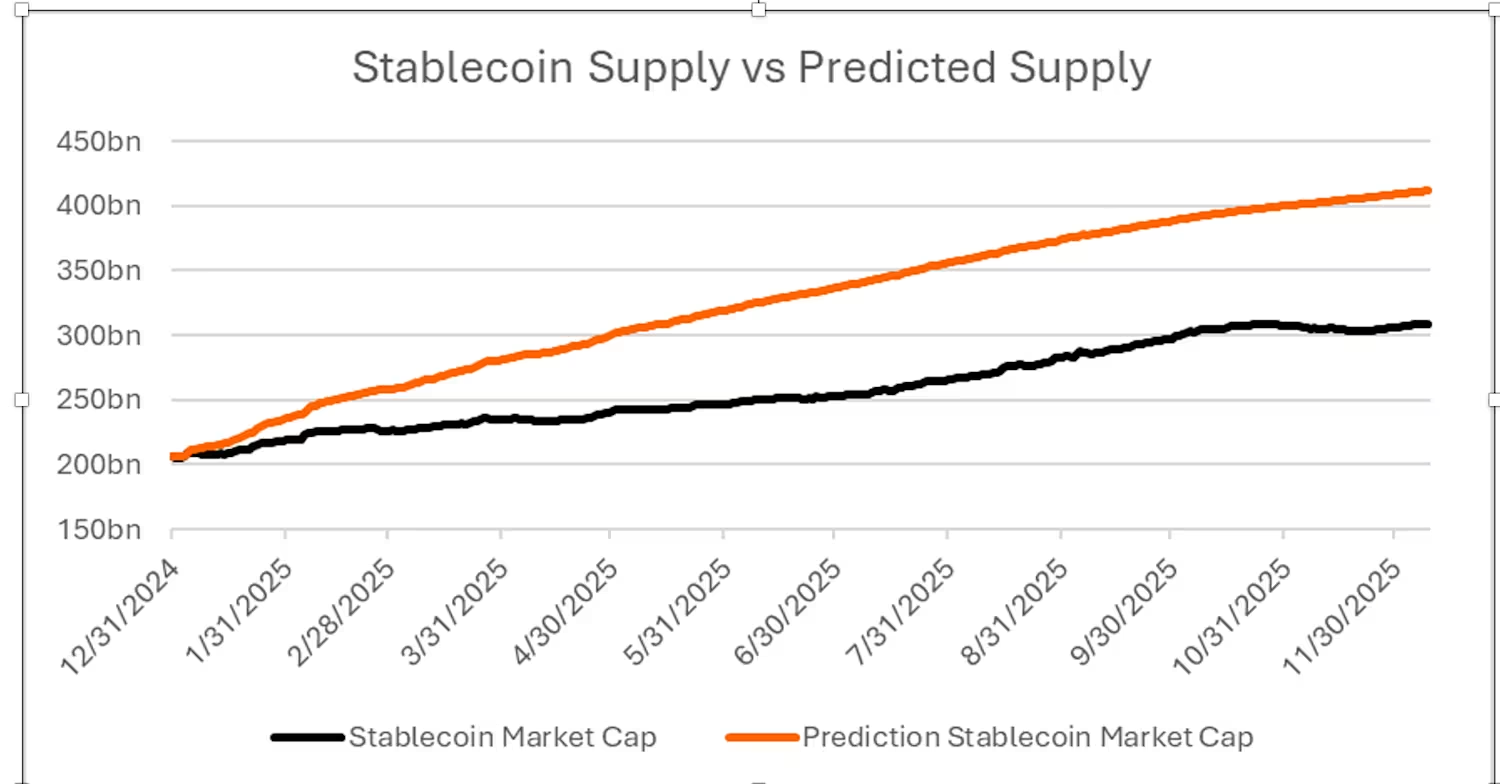

❌ The total supply of stablecoins will double in 2025, exceeding $400 billion.

Results: Stablecoin growth remains strong, having increased by 50% year-to-date to nearly $310 billion, but has fallen short of the initial 100% growth rate forecast. With the passage of the GENIUS Act and the establishment of related implementing rules, regulatory clarity for stablecoins is emerging, therefore, stablecoin growth is expected to remain robust.

— Thad Pinakiewicz

❌ Tether's long-term stablecoin market dominance will fall below 50% by 2025, challenged by yield-generating stablecoins such as Blackrock's BUIDL, Ethena's USDe, and Coinbase/Circle's USDC rewards.

Outcome: This narrative seemed within reach at the start of the year due to the explosive growth of USDe and yield-generating stablecoins. However, with the market downturn in the second half of the year and a slight overall decline in the total stablecoin supply, Tether has maintained its position as the leading stablecoin issuer in the crypto market. As of this writing, Tether holds nearly 70% of the market supply. Tether is poised to launch a new stablecoin, USAT, compliant with the GENIUS Act, to complement its flagship token, USDT, but appears not to have adjusted its collateral portfolio to comply with the proposed U.S. law. Circle's USDC remains Tether's main competitor, with its market share increasing from 24% to 28% of the total supply this year.

— Thad Pinakiewicz