Strategy’s “Moonshot” Plan

- 核心观点:Strategy比特币策略推动季度净利100亿美元。

- 关键要素:

- 140亿美元比特币未实现收益。

- 比特币持有量达597,325枚。

- 软件业务收入仅1.145亿美元。

- 市场影响:比特币投资工具属性强化。

- 时效性标注:中期影响。

Originally Posted by Prathik Desai

Original translation: Block unicorn

Today, we delve into Strategy Corporation’s (formerly MicroStrategy) Q2 2025 financial results, which marked the company’s first net positive quarter since adopting fair value Bitcoin accounting standards, generating one of the largest quarterly profits in the company’s history.

Today, we delve into Strategy Corporation’s (formerly MicroStrategy) Q2 2025 financial results, which marked the company’s first net positive quarter since adopting fair value Bitcoin accounting standards, generating one of the largest quarterly profits in the company’s history.

Key Points

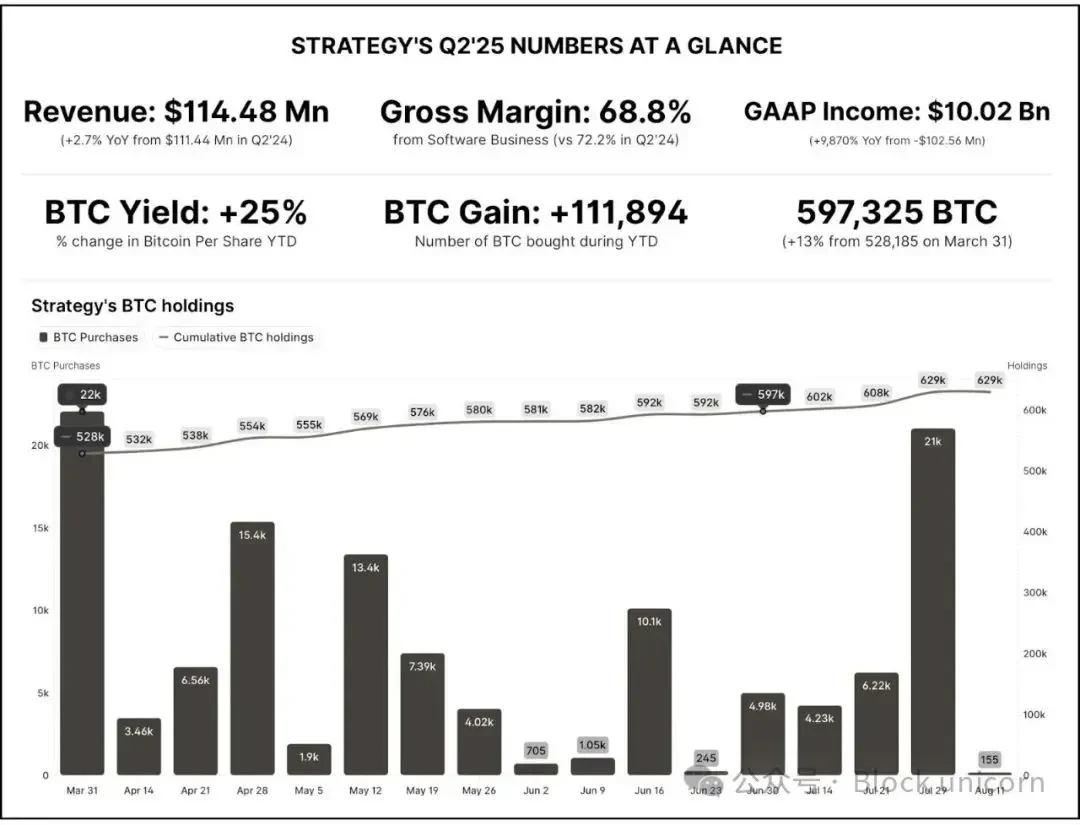

- The Strategy’s Bitcoin Treasury strategy generated $10 billion in net income (compared to a loss of $102.6 million in the second quarter of 2024), driven entirely by $14 billion in unrealized Bitcoin gains under the new accounting standards.

- The software business remained stable but secondary, with revenue of $114.5 million (up 2.7% year-over-year), narrowing margins, and contributing approximately $32 million of underlying operating income.

- Aggressive capital raising continued, with $6.8 billion raised through equity and preferred stock offerings in the second quarter, expanding Bitcoin holdings to 597,325 BTC, 3% of the circulating supply, valued at approximately $64.4 billion.

- Strategy's stock price fell 8% after the earnings report was released, from $401 to $367; the stock has since recovered to over $370.

- Strategy shares trade at a 60% premium to Bitcoin’s net asset value, meaning investors pay $1.60 for every $1 in Bitcoin they hold.

Main argument: While Strategy's Bitcoin treasury strategy works as long as Bitcoin prices continue to rise and capital markets remain open, it introduces significant return volatility and dilution risk, rendering traditional software metrics irrelevant. However, its early entry into the money management space provides Strategy with ample buffer against Bitcoin price crashes.

Financial Performance: Bitcoin is the Key Driver

Strategy Analytics reported a GAAP net profit of $10.02 billion for the second quarter of 2025, compared to a net loss of $102.6 million in the same period last year. Diluted earnings per share reached $32.60, compared to a loss of $0.57 in the second quarter of 2024.

The 9,870% year-over-year increase in net income stemmed almost entirely from the $14 billion in unrealized Bitcoin windfall gains recognized following the adoption of fair value accounting standards in January 2025. This marked a departure from the old accounting system, which required companies to value their BTC holdings at cost less impairment, where price increases were not recognized and any price declines had to be recorded as an impairment charge.

The scale of this accounting impact is even more pronounced when compared to Strategy's operating income. Strategy's total revenue for the second quarter was just $114.5 million, meaning the company reported a net profit margin of over 8,700%, an anomaly driven entirely by the appreciation of cryptocurrencies.

The scale of this accounting impact is even more pronounced when compared to Strategy's operating income. Strategy's total revenue for the second quarter was just $114.5 million, meaning the company reported a net profit margin of over 8,700%, an anomaly driven entirely by the appreciation of cryptocurrencies.

Excluding the Bitcoin revaluation, underlying operating income was approximately $32 million, with a healthy margin of approximately 28% on software revenue, but this was insignificant relative to the unexpected gains from cryptocurrencies.

GAAP operating income reached $14.03 billion, a significant improvement from an operating loss of $200 million in the same period last year, which included a large Bitcoin impairment charge under the old accounting system.

Quarterly fluctuations were extremely significant. In the first quarter of 2025, as Bitcoin fell to approximately $82,400 in March, the company reported a GAAP net loss of $4.22 billion. However, as Bitcoin rebounded to $107,800 in June, the company achieved a $10 billion profit in the second quarter, marking a quarter-over-quarter turnaround to profitability and exceeding $14 billion in profits.

Management acknowledged that fair value accounting makes earnings “extremely sensitive” to the market price of Bitcoin. Strategy’s profitability is currently driven primarily by cryptocurrency market fluctuations, rather than software sales.

Adjusted net income (excluding stock-based compensation and minor items) was approximately $9.95 billion, compared to negative $136 million in the prior year, essentially flat with GAAP, as bitcoin-related adjustments far outweighed traditional add-back adjustments.

Treasury Financing

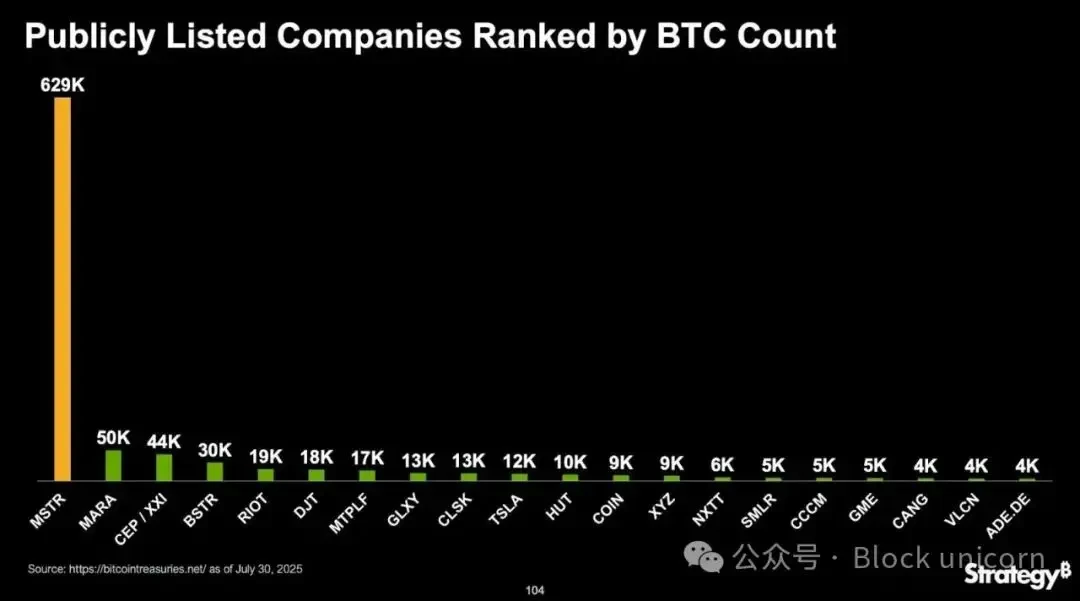

As of June 30, 2025, Strategy held 597,325 Bitcoins, a more than 2.5-fold increase from 226,331 Bitcoins a year earlier. With additional purchases in the third quarter, holdings now stand at 628,946 BTC. The total cost basis is $46.094 billion (an average of $73,290 per BTC), while the market value is approximately $74.805 billion. This translates to approximately $29 billion in unrealized gains—more than double the amount reported in the second quarter.

During the second quarter, Strategy acquired 69,140 BTC for approximately $6.8 billion, equal to the total funds raised by the firm during the same period. The average purchase price during the second quarter was approximately $98,000 per BTC, indicating steady accumulation as prices climbed from April lows. No Bitcoin sales occurred, and no gains were realized, in line with Chairman Michael Saylor's "HODL" strategy.

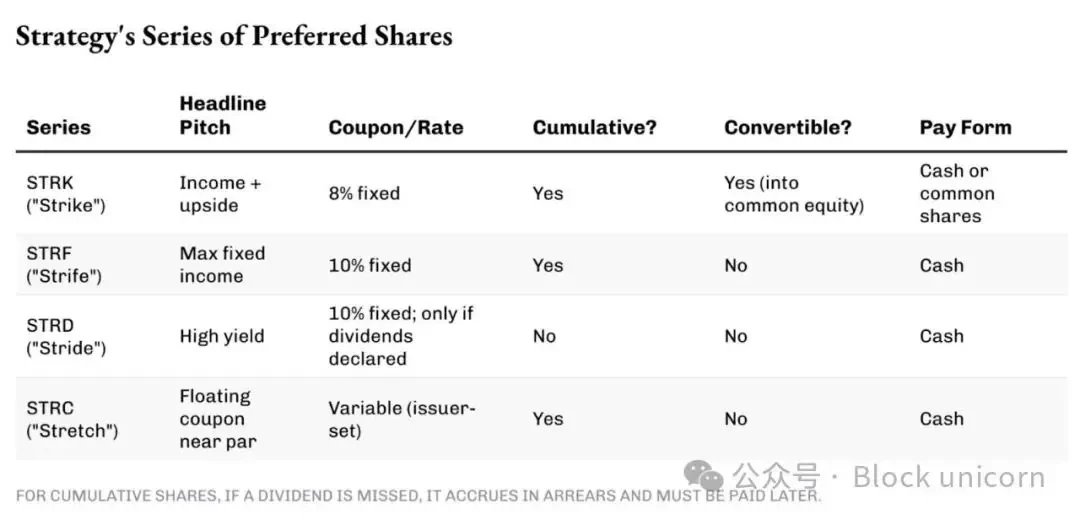

Financing structures have evolved into complex capital market operations:

Common Equity ATM Program: $5.2 billion was raised in the second quarter through the issuance of approximately 14.23 million shares, with an additional $1.1 billion raised in July. The program currently has approximately $17 billion in capacity.

Preferred Stock Series: This strategy utilizes a variety of perpetual preferred stocks to continuously raise funds for Bitcoin purchases in any market environment while limiting dilution of common stock. Different series offer varying yields and maturities, allowing the cost of capital to match investors’ preferences at the time.

Convertible Bonds: In February, Strategy issued $2 billion worth of 0% convertible senior notes, due in 2030, with a conversion price of $433.43. While these notes do not pay interest, bondholders have the right to convert them into Strategy's Class A common stock if the stock price exceeds $433.43. While conversion to equity would further dilute existing shareholders, it would eliminate Strategy's debt obligations. The company redeemed $1.05 billion of its convertible bonds due in 2027 in this manner in the first quarter.

Convertible Bonds: In February, Strategy issued $2 billion worth of 0% convertible senior notes, due in 2030, with a conversion price of $433.43. While these notes do not pay interest, bondholders have the right to convert them into Strategy's Class A common stock if the stock price exceeds $433.43. While conversion to equity would further dilute existing shareholders, it would eliminate Strategy's debt obligations. The company redeemed $1.05 billion of its convertible bonds due in 2027 in this manner in the first quarter.

This capital structure supports continued Bitcoin accumulation but also introduces significant fixed costs. The preferred shares carry substantial dividends (8-10% coupon rate, totaling hundreds of millions of dollars annually) that must be paid regardless of Bitcoin's performance. The Strategy maintains a leverage ratio (debt relative to BTC assets) of approximately 20-30%, meaning the majority of purchases are funded by equity/preferred stock issuance, rather than debt.

Software business: stable but secondary

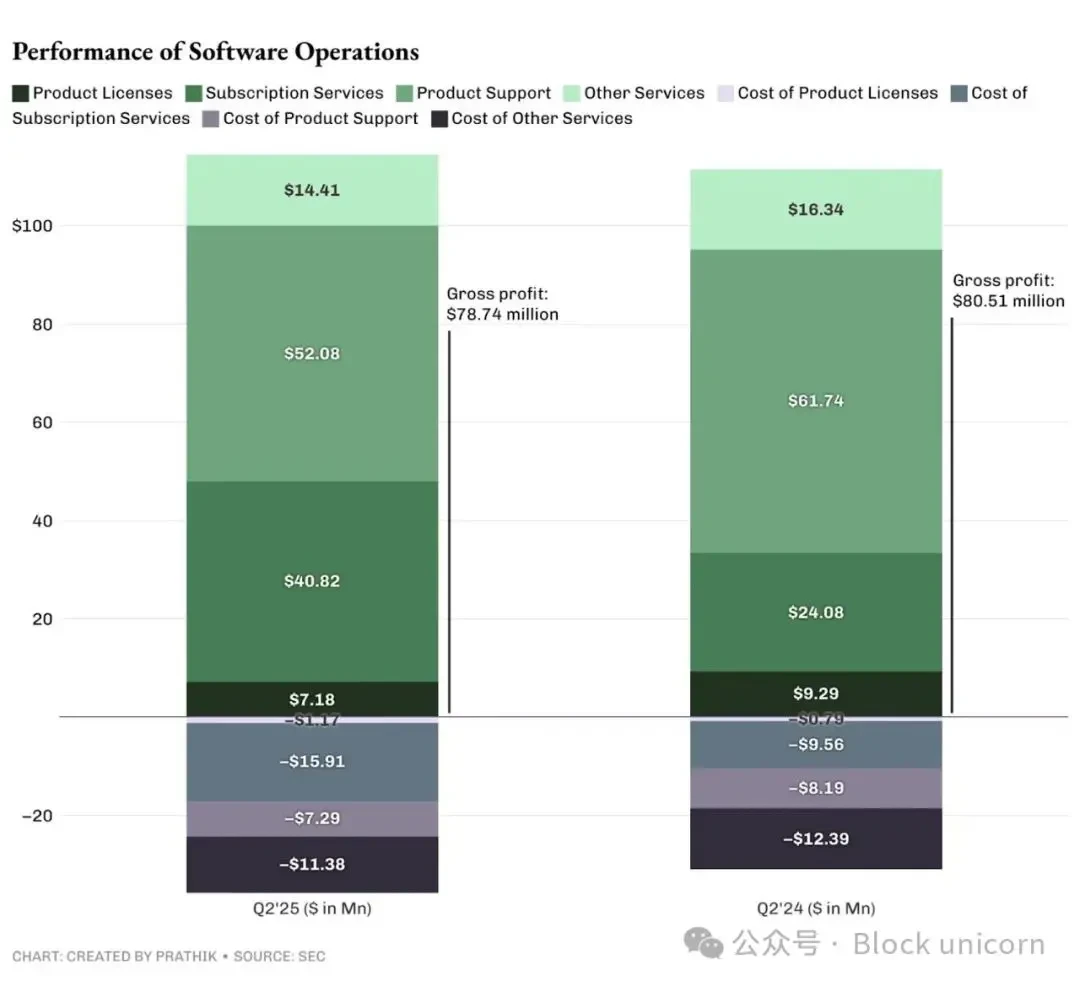

The traditional analytics business generated revenue of $114.5 million in the second quarter of 2025, a year-on-year increase of 2.7%, returning to growth after a 3.6% decline in the first quarter. Revenue composition continues to tilt towards subscription services:

- Subscription Services: $40.8 million (up 69.5% year-over-year), now representing approximately 36% of total revenue, compared to approximately 22% in the same period last year.

- Product licenses: approximately $7.2 million, down approximately 22% as customers shift to cloud services.

- Product Support: $52.1 million (down 15.6% year-over-year), driven by lower maintenance revenue during the cloud transformation.

- Other services: $14.4 million (down 11.8% year-over-year), reflecting lower consulting demand.

- Software gross profit was $78.7 million (68.8% gross margin) compared to $80.5 million (72.2% gross margin) in the second quarter of 2024

Margin compression was driven by increased subscription services costs (cloud hosting, customer success services) and a decrease in high-margin support revenue.

Margin compression was driven by increased subscription services costs (cloud hosting, customer success services) and a decrease in high-margin support revenue.

Operating expenses have historically been comparable to gross profit levels, resulting in meager software operating revenue. Non-Bitcoin operating profit of approximately $32 million in the second quarter indicates that the core business has achieved modest profitability after years of cost reductions. This software contribution helped cover interest obligations ($17.897 million) and some preferred stock dividends ($49.11 million), but represented less than 1% of the company's total profit.

Strategy is expected to operate its business analytics business in a similar manner in the coming quarters, as it remains the company's only cash flow-generating business with real earnings, given its "buy, hold, don't sell" approach to Bitcoin. However, management's commentary focused on Bitcoin accumulation rather than its product roadmap, suggesting that while software services may continue to exist, it may no longer be a meaningful growth driver or valuation component.

Cash flow quality and sustainability

Operating profits and other items on a company's financial statements can be adjusted through clever accounting tricks, but cash flow cannot be faked. If cash flow doesn't reflect what the company says it is doing, then there's a problem.

Strategy's cash flow profile highlights the low quality of its reported earnings. After deducting $14 billion in unrealized gains, $10 billion in net revenue generated virtually no cash. While the company reported $5.75 billion in GAAP net income, its cash balance increased by only $12 million over the two quarters of 2025.

- Operating Cash Flow: The software business probably generates modestly positive operating cash flow, just enough to cover basic expenses. After accounting for non-cash items like depreciation and stock-based compensation, true cash earnings from operations are close to break-even.

- Investing cash flow: Primarily driven by approximately $6.8 billion of Bitcoin purchases in the second quarter, funded entirely by financing activities rather than operations.

- Financing Cash Flow: Net $6.8 billion provided through equity and preferred stock issuance, which was immediately used for Bitcoin purchases, with almost no cash retained.

This pattern of negative investment, positive financing, and meager operating cash flow clearly indicates that Strategy is an asset accumulation tool rather than a cash-generating business.

The company faces rising fixed costs from debt interest (approximately $68 million annualized) and preferred stock dividends (approximately $200 million annualized). If Bitcoin prices stagnate or decline, and capital markets tighten, Strategy could face liquidity pressures, requiring it to sell Bitcoin or issue equity, further diluting its ownership.

Market reaction and valuation

Despite Strategy's record profits, its stock price fell after the second-quarter earnings report as the market priced in unexpected gains from Bitcoin. Subsequently, news of a $4.2 billion STRC stock sale further depressed the stock price. This reaction also reflects investors' understanding that these were not operating profits but rather market capitalization adjustments that could potentially reverse.

However, the stock price has been closely correlated with BTC’s price movements.

Strategy currently trades at a premium of approximately 60% to Bitcoin’s net asset value (NAV), meaning MSTR investors pay $1.60 for every $1 of Bitcoin value on Strategy’s balance sheet.

Why would you pay a premium instead of buying Bitcoin directly? Reasons for the premium include:

- Gain exposure to rising Bitcoin prices per share through corporate structures

- Michael Saylor on Strategy Execution and Market Timing

- Scarcity Value as a Proxy for Liquid Bitcoin in Equity Markets

- Option value of future value-added financing

This premium supports a self-reinforcing strategy: issuing shares at a premium to NAV allows the purchase of more Bitcoin, potentially increasing existing shareholders' Bitcoin holdings per share. If Strategy's stock price is $370 and its Bitcoin NAV is $250 per share, the company can sell new shares at $370 and use the cash to purchase $370 worth of Bitcoin. Existing shareholders now own more Bitcoin per share than they did before the dilution. Despite the massive dilution, Strategy's "Bitcoin per share" metric has increased by 25% year-to-date, validating the effectiveness of this strategy during Bitcoin's bull run.

Strategy's Bitcoin investment requires investors to use unconventional methods for valuation, as traditional valuation metrics are no longer meaningful. Why?

Strategy's second-quarter revenue ($114 million) suggests an annualized revenue of $450 million, while its current enterprise value is $120.35 billion. This means that Strategy's stock price-to-earnings ratio exceeds 250 times its revenue, a traditionally astronomical multiple. The problem is that when investors buy Strategy stock, they aren't betting on its software analytics business. The market is pricing in Bitcoin's potential for appreciation, a potential magnified by corporate leverage and continued accumulation.

Investment Perspective

The quarterly results reflect Strategy's complete transformation from a software company to a leveraged Bitcoin investment vehicle. While significant, the $10 billion quarterly profit represents unrealized appreciation, not operational success. For equity investors, Strategy provides high-risk Bitcoin exposure, with significant leverage and active accumulation, but at the expense of extreme volatility and dilution risk.

This strategy performed well during Bitcoin's bull run, as it facilitated incremental financing to fund additional purchases while mark-to-market gains drove reported earnings higher. However, the sustainability of this model relies on continued market access and Bitcoin appreciation. Any significant cryptocurrency market decline would quickly reverse Q2 results, while fixed obligations such as debt interest and preferred stock dividends would continue to accrue.

However, among all Bitcoin vaults, Strategy is the best positioned to absorb such unexpected shocks. It began accumulating Bitcoin more than five years ago and has done so systematically at a much lower cost than other companies.

Today, Strategy holds 3% of all Bitcoin in circulation.

Strategy's premium valuation reflects the market's confidence in Michael Saylor's vision and execution for Bitcoin. Investors are betting on the long-term trajectory of Bitcoin and management's ability to leverage the company's structure for maximum accumulation.

Strategy's premium valuation reflects the market's confidence in Michael Saylor's vision and execution for Bitcoin. Investors are betting on the long-term trajectory of Bitcoin and management's ability to leverage the company's structure for maximum accumulation.

With Bitcoin holdings now accounting for over 99% of economic value, traditional software metrics have become less important in defining Strategy’s future cryptocurrency story.

This concludes Strategy's analysis of its second-quarter earnings report. We will be back with new coverage soon.