Original title: "Artemis Research: Why does ETH become the reserve asset of the on-chain economy?"

Original author: Kevin Li

Original translation: TechFlow

There has been a recent resurgence of interest in Ethereum, especially following the emergence of ETH as a reserve asset. Our fundamental analysts explore a valuation framework for ETH and construct a compelling long-term bull case. As always, we’d love to connect with you and exchange ideas – just remember to do your own research (DYOR).

Let’s take a deeper dive into ETH with our fundamental analyst Kevin Li.

Key Points

Ethereum (ETH) is transforming from a misunderstood asset to a scarce, programmable reserve asset that provides security and power to a rapidly compliant on-chain ecosystem.

ETH's adaptive monetary policy predicts a decline in inflation - even if 100% of ETH is staked, inflation will be around 1.52% at best, and will drop to around 0.89% by the 100th year (2125). This is much lower than the average annual growth rate of 6.36% in the U.S. M2 money supply (1998-2024), and is even comparable to the growth rate of gold supply.

Institutional adoption is accelerating, with firms like JPMorgan and BlackRock building on Ethereum, driving continued demand for ETH to secure and settle on-chain value.

The annual correlation between on-chain asset growth and native ETH staked is as high as 88%, highlighting strong economic alignment.

The U.S. Securities and Exchange Commission (SEC) released a policy statement on staking on May 29, 2025, reducing regulatory uncertainty. Ethereum ETF filings now include staking provisions, thereby improving returns and enhancing institutional consistency.

ETH’s deep composability makes it a productive asset — it can be used for staking/re-staking, as DeFi collateral (e.g. Aave, Maker), AMM liquidity (e.g. Uniswap), and as a native gas token on Layer 2.

While Solana has gained traction in Memecoin activity, Ethereum’s greater decentralization and security allow it to dominate high-value asset issuance — a larger and more durable market.

The rise of Ethereum reserve asset trading, which began with Sharplink Gaming ($SBET) in May 2025, has resulted in public companies holding over 730,000 ETH. This new demand trend mirrors the wave of Bitcoin reserve asset trading in 2020 and has contributed to ETH’s recent outperformance of BTC.

Not long ago, Bitcoin was widely viewed as a legitimate store of value — its pitch as “digital gold” seemed fanciful to many. Today, Ethereum (ETH) faces a similar identity crisis. ETH is often misunderstood, has underperformed in annual returns, has missed key meme cycles, and has experienced slowing retail adoption across much of the crypto ecosystem.

A common criticism is that ETH lacks a clear value accumulation mechanism. Skeptics believe that the rise of Layer 2 solutions has cannibalized base layer fees and weakened ETH's status as a monetary asset. When ETH is viewed primarily from the perspective of transaction fees, protocol revenue, or "actual economic value," it begins to look like a cloud computing security - more like Amazon stock than a sovereign digital currency.

In my view, this framework constitutes a classification error. Valuing ETH purely through cash flows or protocol fees confuses fundamentally different asset classes. Instead, it is best understood through a commodity framework similar to Bitcoin. More accurately, ETH constitutes a unique asset class: a scarce but highly productive, programmable reserve asset whose value accrues through its role in securing, settling, and driving an increasingly institutionalized, composable on-chain economy.

The Debasement of Fiat Currencies: Why the World Needs Alternatives

To fully understand ETH's evolving monetary role, it must be placed in the broader economic context, especially in an era of fiat debasement and monetary expansion. Driven by continued government stimulus and spending, inflation rates are often underestimated. Although official CPI data shows inflation hovering around 2% per year, this metric is subject to adjustment and can mask a true decline in purchasing power.

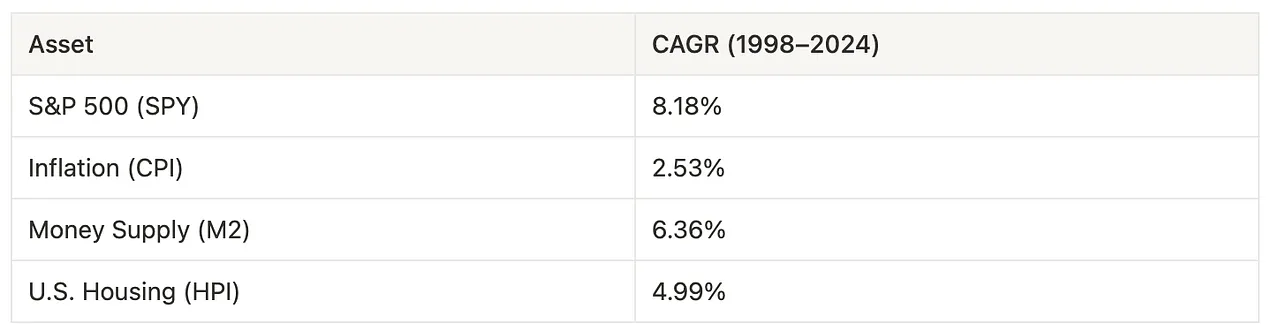

CPI inflation has averaged 2.53% per year between 1998 and 2024. In contrast, the US M2 money supply has averaged 6.36% per year, outpacing inflation and house prices and close to the S&P 500’s 8.18% return. This even suggests that much of the stock market’s nominal growth may be more due to monetary expansion than productivity gains.

Figure 1: Returns of the S&P 500, CPI, M2 Supply, and Housing Index (HPI)

Source: Federal Reserve Economic Data

The rapid growth of the money supply reflects the government's increasing reliance on monetary stimulus and fiscal spending programs to respond to economic instability. Recent legislation, such as Trump's "Big, Beautiful Act" (BBB), introduced radical new spending measures that are widely considered to be inflationary. At the same time, the launch of the Department of Government Efficiency (DOGE), which was strongly advocated by Elon Musk, does not seem to have the expected effect. These developments have contributed to a growing consensus that the existing monetary system is inadequate and a more reliable store of value asset or form of currency is urgently needed.

What constitutes a store of value — and where ETH fits in

A reliable store of value generally meets four criteria:

Durability – It must stand the test of time without degrading.

Value preservation – It should maintain its purchasing power throughout market cycles.

Liquidity – must be easily tradable in an active market.

Adoption and Trust – There must be widespread trust or adoption.

Today, ETH excels in durability and liquidity. Its durability stems from Ethereum’s decentralized and secure network. Its liquidity is also high: ETH is the second most traded crypto asset, with a rich market on both centralized and decentralized exchanges.

However, when evaluating ETH from a purely traditional "value storage" perspective, its value preservation, application, and trust remain a controversial criterion. For this reason, the concept of "scarce programmable reserve assets" is more appropriate, highlighting the positive role of ETH in value maintenance and trust building and its unique mechanism.

ETH’s Monetary Policy: Scarce but Adaptable

One of the most controversial aspects of ETH’s role as a store of value is its monetary policy, specifically how it controls supply and inflation. Skeptics often point to Ethereum’s lack of a fixed supply cap. However, this criticism ignores the architectural complexity of Ethereum’s adaptive issuance model.

ETH issuance is dynamically related to the amount of ETH staked. While issuance increases with stake participation, the relationship is sublinear: inflation increases at a slower rate than the total amount staked. This is because issuance is inversely proportional to the square root of the total amount of ETH staked, creating a natural regulatory effect on inflation.

Figure 2: Rough inflation formula for staking ETH

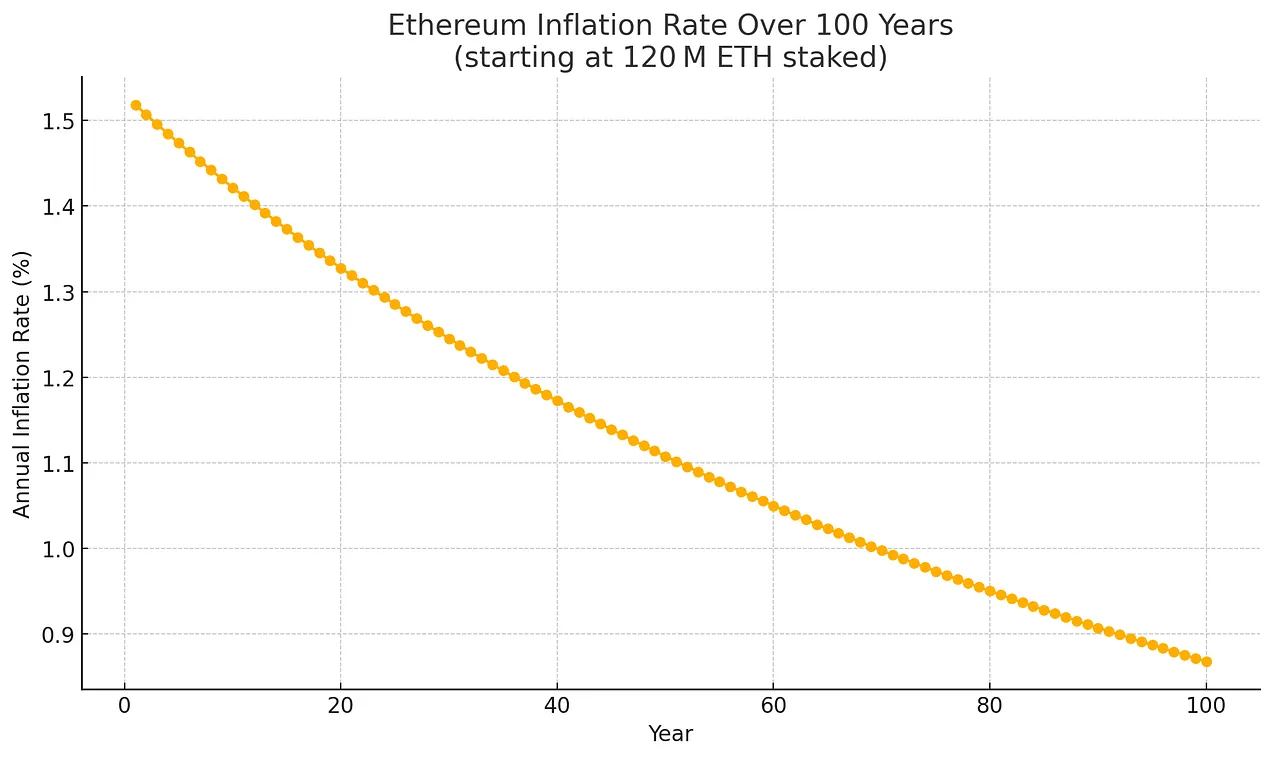

The mechanism introduces a soft cap on inflation, which gradually decreases over time even as staking participation increases. In the worst-case scenario simulated (i.e. 100% of ETH is staked), the annual inflation rate is capped at approximately 1.52%.

Figure 3: Illustrative extrapolation of ETH maximum issuance, assuming 100% of ETH is staked, starting at 120 million ETH, and a term of 100 years

Importantly, even this worst-case issuance rate will decline as the total supply of ETH increases, following an exponential decay curve. Assuming 100% staking and no ETH destruction, the expected inflation trend is as follows:

Year 1 (2025): ~ 1.52%

Year 20 (2045): ~ 1.33%

Year 50 (2075): ~ 1.13%

Year 100 (2125): ~ 0.89%

Figure 4: Illustrative extrapolation of ETH maximum issuance, assuming 100% of ETH is staked, starting at 120 million ETH, as total supply increases

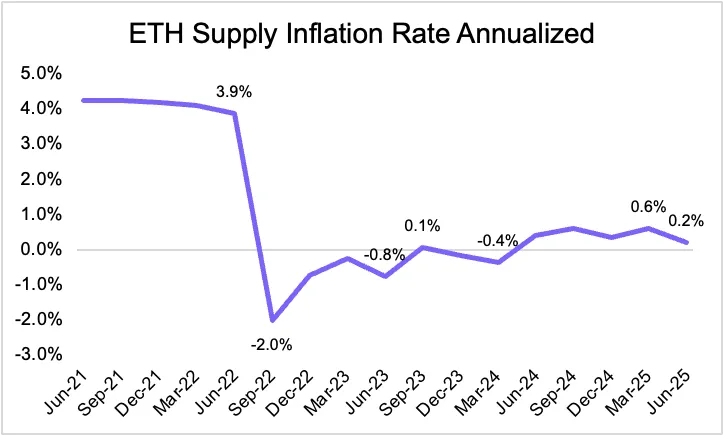

Even under these conservative assumptions, Ethereum’s declining inflation curve reflects its inherent monetary laws — which strengthens its credibility as a long-term store of value. The situation improves further when we consider the burn mechanism that Ethereum introduced through EIP-1559. A portion of transaction fees will be permanently removed from circulation, which means that the net inflation rate can be much lower than total issuance, and sometimes even fall into deflation. In fact, since Ethereum transitioned from proof-of-work to proof-of-stake, the net inflation rate has been lower than issuance and periodically fell into negative values.

Figure 5: ETH supply inflation rate annualized

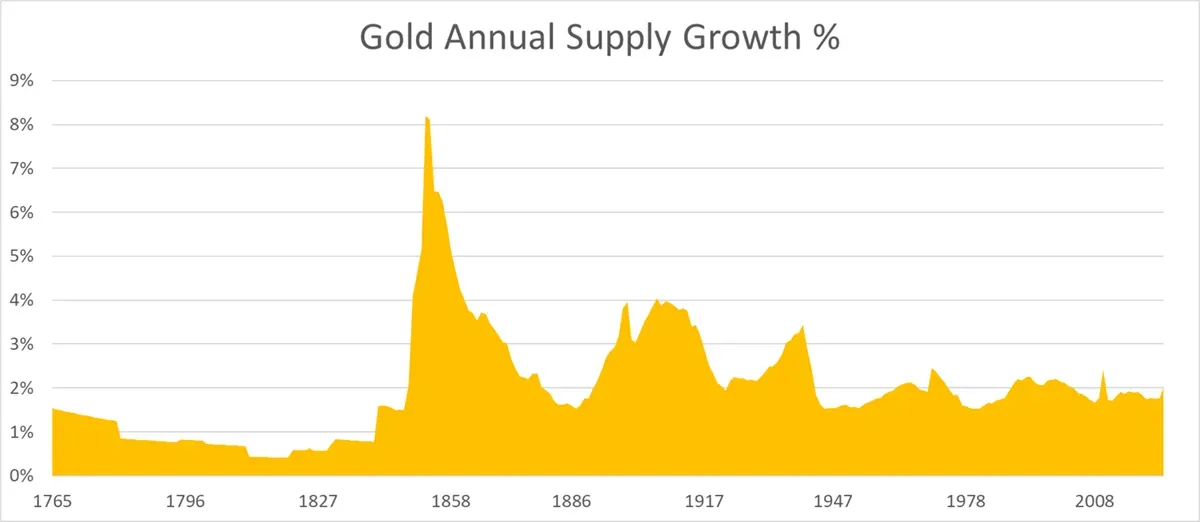

Compared to fiat currencies such as the US dollar (whose M2 money supply is growing at an average annual rate of over 6%), Ethereum’s structural constraints (and potential deflation) enhance its appeal as a store of value asset. Notably, Ethereum’s maximum supply growth rate is now comparable to or even slightly lower than that of gold, further solidifying its position as a sound money asset.

Figure 6: Annual gold supply growth rate

Source: ByteTree, World Gold Council, Bloomberg, Our World in Data

Institutional adoption and trust

While Ethereum’s currency design effectively solves the supply dynamics problem, its actual utility as a settlement layer has now become the primary driver of adoption and institutional trust. Major financial institutions are building directly on Ethereum: Robinhood is developing a tokenized stock platform, JPMorgan is launching its deposit token (JPMD) on Ethereum Layer 2 (Base) , and BlackRock is tokenizing a money market fund on the Ethereum network using BUIDL .

This on-chain process is driven by a strong value proposition that addresses legacy inefficiencies and unlocks new opportunities:

Efficiency and cost reduction: Traditional finance relies on intermediaries, manual steps, and slow settlement processes. Blockchain simplifies these processes through automation and smart contracts, thereby reducing costs, reducing errors, and shortening processing time from days to seconds.

Liquidity and fractional ownership: Tokenization enables fractional ownership of illiquid assets such as real estate or art, expanding investor access and unlocking locked capital.

Transparency and Compliance: Blockchain’s immutable ledger ensures a verifiable audit trail, streamlining compliance and reducing fraud through real-time visibility into transactions and asset ownership.

Innovation and market access: Composable on-chain assets allow new products (such as automated lending or synthetic assets) to create new revenue streams and expand the scope of finance outside of traditional systems.

ETH staking as security and economic coordination

The on-chain migration of traditional financial assets highlights two main drivers of ETH demand. First, the growing presence of real-world assets (RWAs) and stablecoins has increased on-chain activity, driving up demand for ETH as a gas token. More importantly, as Tom Lee observes, institutions may need to purchase and stake ETH to secure the infrastructure they rely on, aligning their interests with the long-term security of Ethereum. In this context, stablecoins represent Ethereum’s “ChatGPT moment,” a major breakthrough use case that demonstrates the platform’s transformative potential and broad utility.

As more and more value is settled on-chain, the alignment between Ethereum’s security and its economic value becomes increasingly important. Ethereum’s finality mechanism, Casper FFG, ensures that blocks can only be finalized when a majority (two-thirds or more) of the staked ETH reaches consensus. While an attacker who controls at least one-third of the staked ETH cannot finalize malicious blocks, they can completely undermine finality by disrupting consensus. In this case, Ethereum can still propose and process blocks, but due to the lack of finality, these transactions may be reversed or reordered, posing serious settlement risks for institutional use cases.

Even when running on Layer 2, which relies on Ethereum for final settlement, institutional participants rely on the security of the base layer. Far from harming ETH, Layer 2 increases the value of ETH by driving demand for base layer security and Gas. They submit proofs to Ethereum, pay base fees, and typically use ETH as their native Gas token. As Rollup execution scales, Ethereum continues to accumulate value through its fundamental role in providing secure settlement.

In the long term, many institutions may move beyond passive staking through custodians and begin operating their own validators. While third-party staking solutions offer convenience, operating a validator allows institutions to have greater control, higher security, and direct participation in consensus. This is particularly valuable for stablecoin and RWA issuers because it enables them to acquire MEV, ensure reliable transaction inclusion, and take advantage of privacy enforcement - features that are critical to maintaining operational reliability and transaction integrity.

Importantly, broader institutional participation in validator node operations helps address one of Ethereum's current challenges: the concentration of power in the hands of a few large operators, such as liquid proof-of-stake protocols and centralized exchanges. By diversifying the set of validators, institutional participation helps improve Ethereum's decentralization, strengthen its resilience, and enhance the network's credibility as a global settlement layer.

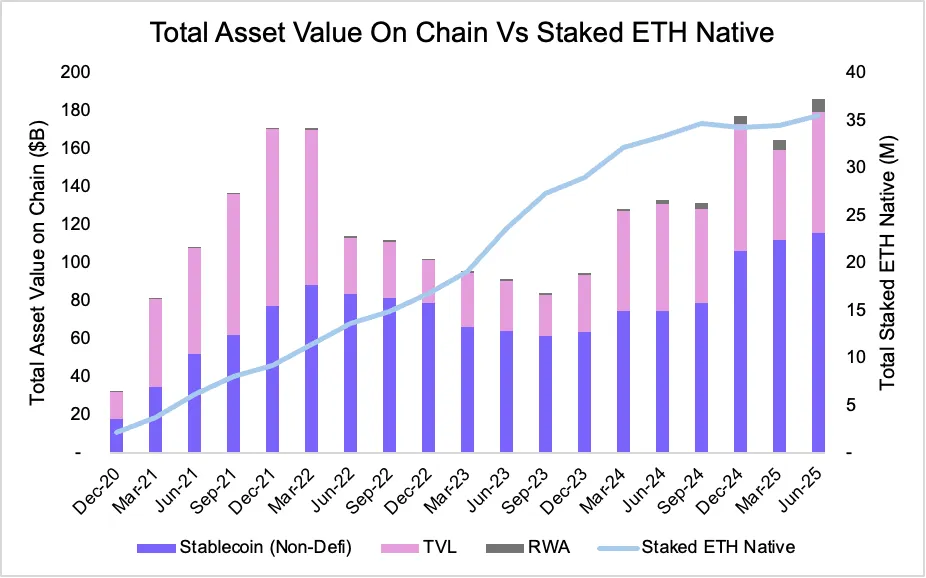

A notable trend between 2020 and 2025 reinforces this alignment of incentives: the growth of on-chain assets is closely tied to the growth of staked ETH. As of June 2025, the total supply of stablecoins on Ethereum reached a record $116.06 billion, while tokenized RWA climbed to $6.89 billion. At the same time, the amount of staked ETH grew to 35.53 million ETH, a significant increase that highlights how network participants balance security and on-chain value.

Figure 7: Total value of ETH on the chain vs. value of staked native ETH

Source: Artemis

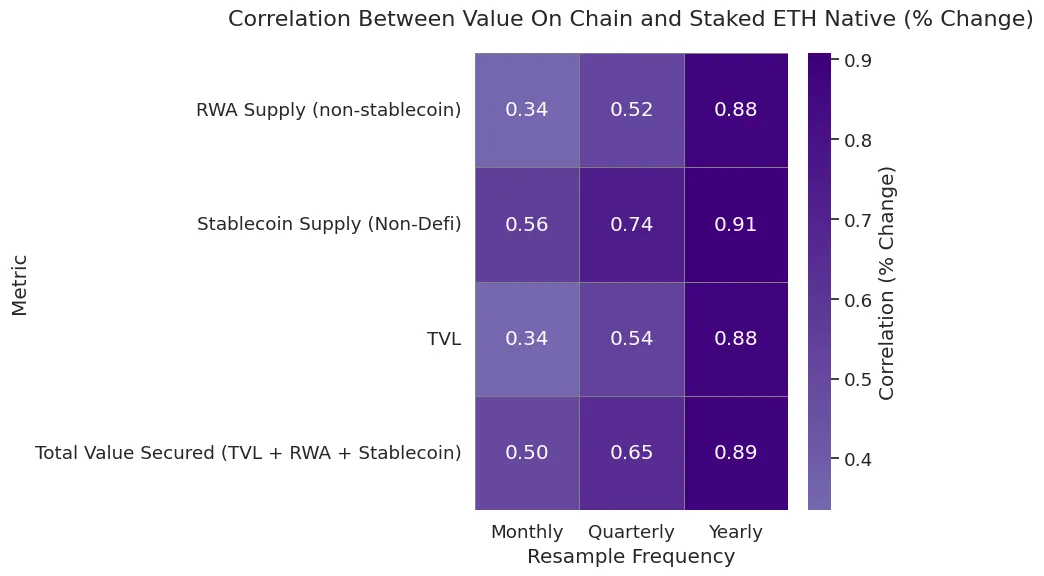

From a quantitative perspective, the annual correlation between on-chain asset growth and native ETH staked has remained above 88% across major asset classes. In particular, the supply of stablecoins is closely correlated with the growth of staked ETH. While quarterly correlations can be more volatile due to short-term fluctuations, the overall trend remains the same - as assets flow on-chain, the incentive to stake ETH increases.

Figure 8: Monthly, quarterly, and annual native correlations between staked ETH and on-chain value

Source: Artemis

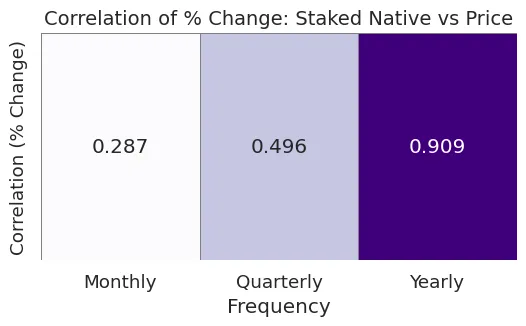

Additionally, the increase in staked ETH also impacts ETH’s price dynamics. As more ETH is staked and removed from circulation, the supply of ETH tightens, especially during periods of high on-chain demand. Our analysis shows that the amount of staked ETH is 90.9% correlated with ETH price on an annualized basis and 49.6% on a quarterly basis, supporting the view that staking not only secures the network, but also creates favorable supply and demand pressures on ETH itself in the long run.

Figure 9: Native correlation between staked ETH and price

Source: Artemis

A recent policy clarification from the U.S. Securities and Exchange Commission (SEC) eased regulatory uncertainty surrounding Ethereum staking. On May 29, 2025, the SEC's Division of Corporation Finance stated that certain protocol staking activities (limited to non-entrepreneurial roles, such as self-staking, entrusted staking, or custodial staking under certain conditions) do not constitute securities offerings. While more complex arrangements still need to be determined based on actual circumstances, this clarification encourages institutions to participate more actively. After the announcement, Ethereum ETF application documents began to include staking terms, allowing funds to be rewarded while maintaining network security. This not only improves the rate of return, but also further consolidates institutional acceptance and trust in the long-term adoption of Ethereum.

Composability and ETH as a productive asset

Another notable feature that distinguishes ETH from pure store-of-value assets such as gold and Bitcoin is its composability, which in itself drives demand for ETH. Gold and BTC are non-productive assets, while ETH is natively programmable. It plays an active role in the Ethereum ecosystem, providing support for decentralized finance (DeFi), stablecoins, and Layer 2 networks.

Composability refers to the ability of protocols and assets to interoperate seamlessly. In Ethereum, this makes ETH not only a monetary asset, but also a fundamental building block for on-chain applications. As more and more protocols are built around ETH, the demand for ETH grows - not only as Gas, but also as collateral, liquidity, and pledge funds.

Today, ETH is used for a variety of key functions:

Staking and re-staking — ETH secures Ethereum itself and can be re-staking through EigenLayer to provide security for oracles, rollups, and middleware.

Collateral in lending and stablecoins — ETH powers major lending protocols like Aave and Maker, and is the basis for over-collateralized stablecoins.

Liquidity in AMMs — ETH pairs dominate on decentralized exchanges like Uniswap and Curve, enabling efficient exchanges across the ecosystem.

Cross-chain Gas – ETH is the native gas token for most Layer 2s, including Optimism, Arbitrum, Base, zkSync, and Scroll.

Interoperability — ETH can be bridged, wrapped, and used in non-EVM chains like Solana, Cosmos (via Axelar), etc., making it one of the most widely transferable assets on-chain.

This deeply integrated utility makes ETH a scarce but efficient reserve asset. As ETH becomes more integrated into the ecosystem, switching costs rise and network effects strengthen. In a sense, ETH may be more like gold than BTC. Most of the value of gold comes from industrial and jewelry applications, not just investment. In contrast, BTC lacks this functional utility.

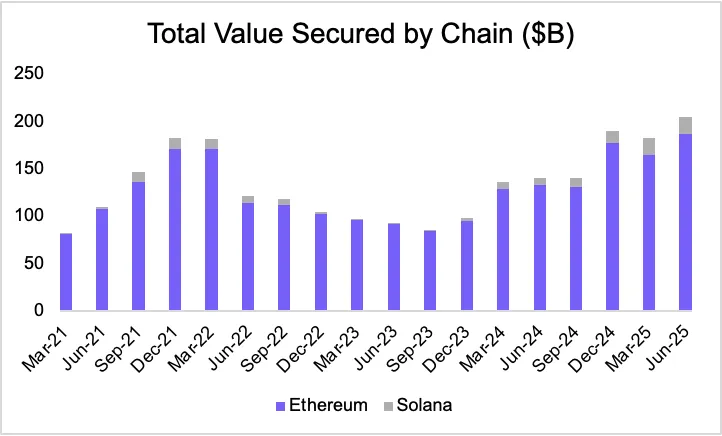

Ethereum vs. Solana: The Layer-1 Divergence

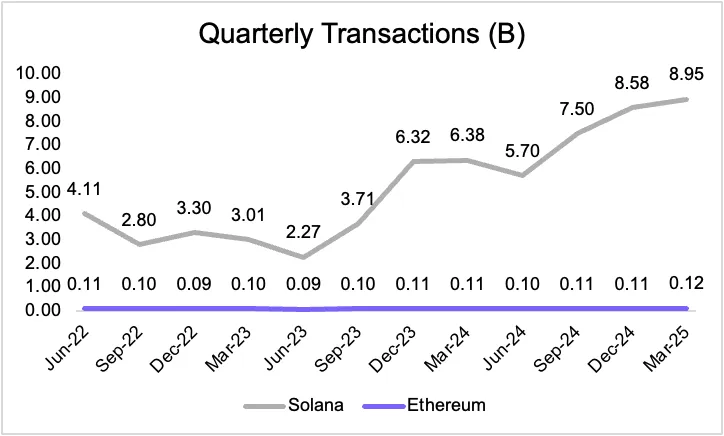

Solana appears to be the biggest winner in the Layer 1 space during this cycle. It has effectively taken over the memecoin ecosystem, creating a vibrant network for new tokens to be launched and developed. While this momentum is certainly there, Solana is still not as decentralized as Ethereum due to its limited number of validators and high hardware requirements.

That being said, demand for Layer 1 block space is likely to be stratified. In this stratified future, both Solana and Ethereum can thrive. Different assets require different tradeoffs between speed, efficiency, and security. However, in the long run, Ethereum — due to its greater decentralization and security guarantees — may capture a larger share of asset value, while Solana may capture a higher transaction frequency.

Figure 10: Quarterly transaction volume of SOL and ETH

However, in the financial markets, the market size of assets that pursue robust security is much larger than the market size of assets that only focus on execution speed. This dynamic is beneficial to Ethereum: as more and more high-value assets are added to the chain, Ethereum's role as a basic settlement layer will become more and more valuable.

Figure 11: Total value secured on-chain ($ billion)

Source: Artemis

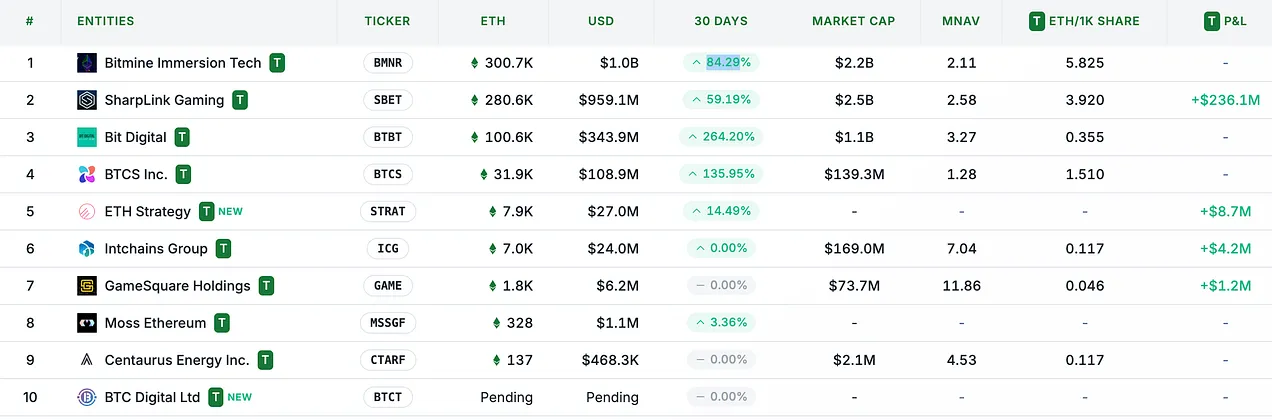

Reserve Asset Momentum: ETH’s Microstrategy Moment

While on-chain assets and institutional demand are long-term structural drivers for ETH, Ethereum asset management strategies — like MicroStrategy (MSTR) leverages Bitcoin — could be a sustained catalyst for ETH asset value. A key turning point in this trend was Sharplink Gaming ($SBET) announcing its Ethereum asset management strategy in late May, led by Ethereum co-founder Joseph Lubin.

Figure 12: ETH reserve asset holdings

Source: strategythreserve.xyz

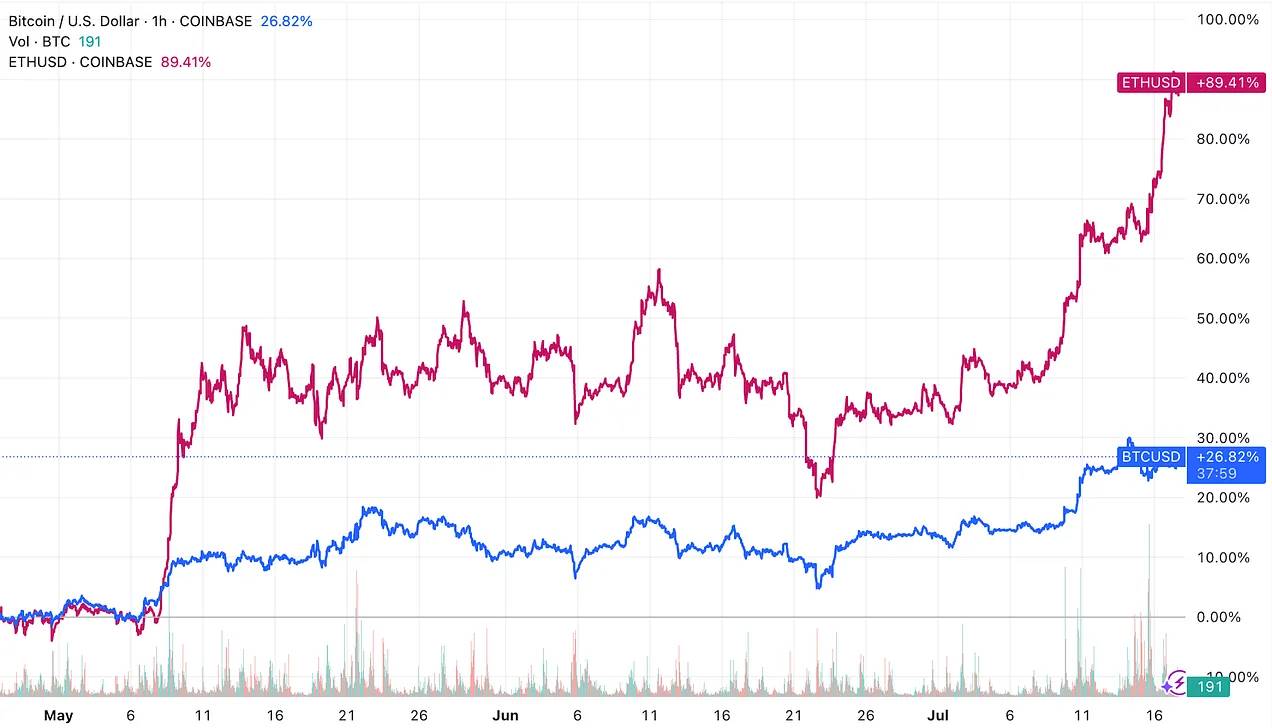

Asset management strategies are tools for tokens to access traditional financial (TradFi) liquidity, while increasing the value of each share of assets of the company involved. Since the emergence of Ethereum-based asset management strategies, these asset management companies have accumulated more than 730,000 ETH, and ETH has begun to outperform Bitcoin - a rare occurrence in this cycle. We believe this marks the beginning of a broader trend of Ethereum-centric asset management applications.

Figure 13: Price trends of ETH and BTC

Stay tuned for our upcoming research report that will dive deeper into the evolving landscape of Ethereum treasury adoption!

Conclusion: ETH is the reserve asset of the on-chain economy

Ethereum’s evolution embodies a broader paradigm shift in the concept of monetary assets in the digital economy. Just as Bitcoin overcame early skepticism to earn recognition as “digital gold,” Ether (ETH) is building its own unique identity — not by mimicking Bitcoin’s narrative, but by evolving into a more versatile, foundational asset. ETH is more than a cloud computing security, nor is it limited to being a utility token for transaction fees or a source of protocol revenue. Instead, it represents a scarce, programmable, and economically essential reserve asset — one that underpins the security, settlement, and functionality of an increasingly institutionalized on-chain financial ecosystem.