RootData:2023年Web3行业发展研究报告及年度榜单

Original author: RootData Research

Table of contents

The overall development trend characteristics of the Web3 industry

1.1. Bitcoin leads the global increase in major asset classes, and Bitcoin spot ETFs will promote the long-term development of the industry.

1.2. Total financing in 2023 will be US$9.043 billion, and the linkage of the primary and secondary markets will help the industry move towards a new cycle

1.3. The primary and semi-primary market is becoming a new choice for investment or exit.

1.4. Infrastructure and CeFi will dominate the development of the Web3 industry in 2023, with 6 new unicorns

1.5. The number of Web3 project failures will be reduced by 50% in 2023

Web3 asset development characteristics and sector trend analysis

2.1. The essence of the four waves of innovation in the Web3 industry is to find the native assets with the greatest consensus.

2.2. The number of Web3 developers increased by 66% year-on-year, and the Ethereum ecosystem has an overwhelming advantage

2.3. Rotation of popular Web3 sectors: L1/L2, DeFi, and GameFi are still the tracks that the market pays most attention to

2.4. Stanford has the most output of Web3 practitioners, and Google has the highest amount of project financing.

Web3 capital flow characteristics and trend analysis

3.1. Analysis of the style and activity of Web3 investment institutions in 2023

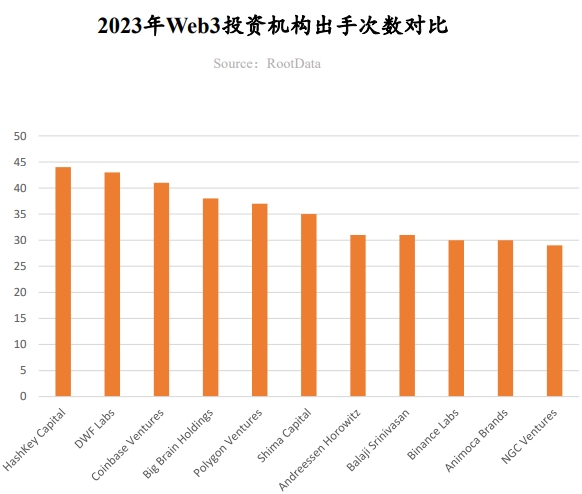

3.2. Analysis of the increase and decrease in the number of transactions of Web3 investment institutions in 2023

3.3. Research and analysis of the top ten projects with annual financing amount in the infrastructure track

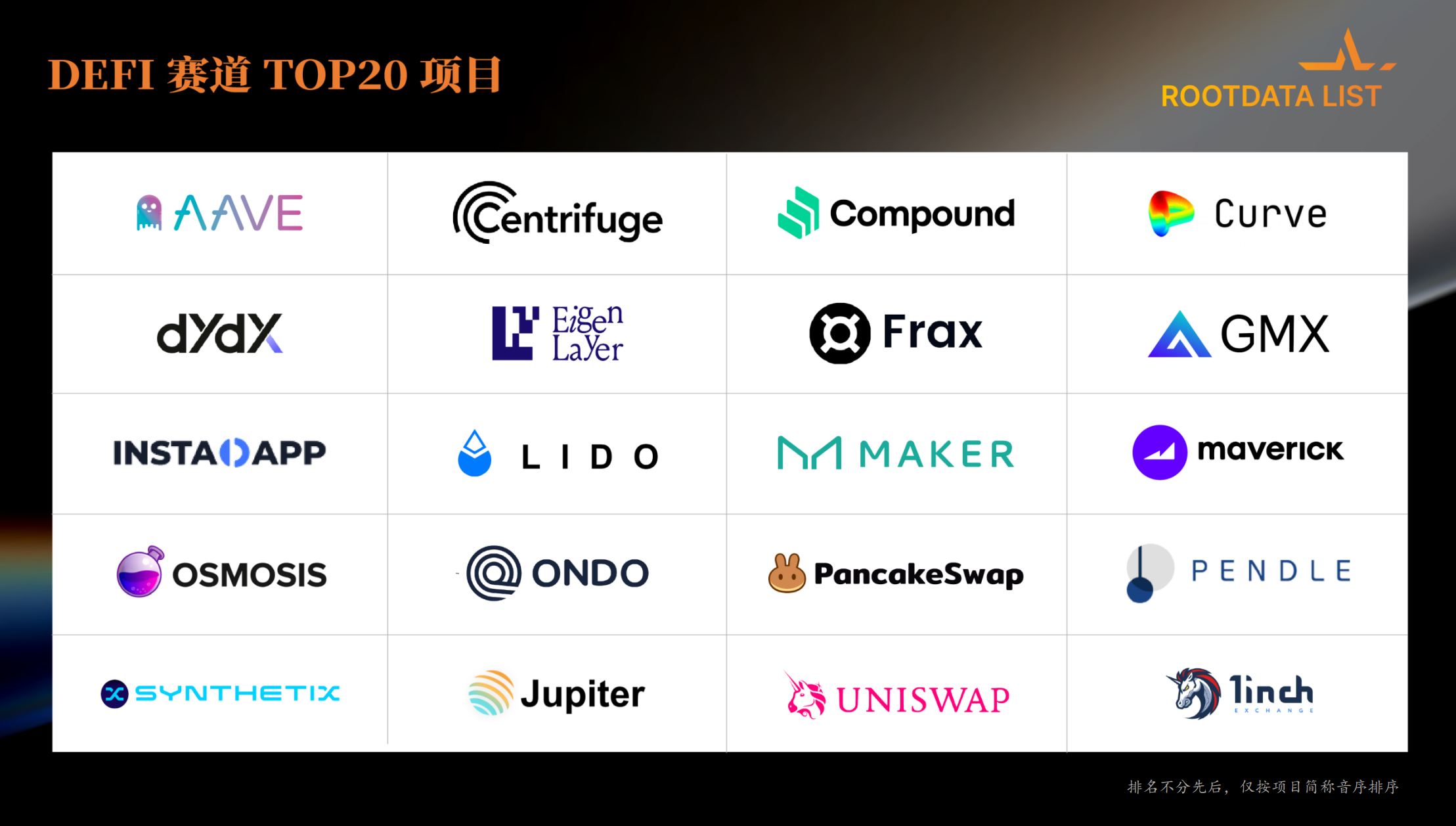

3.4. Research and analysis of the top ten projects in the DeFi track by annual financing amount

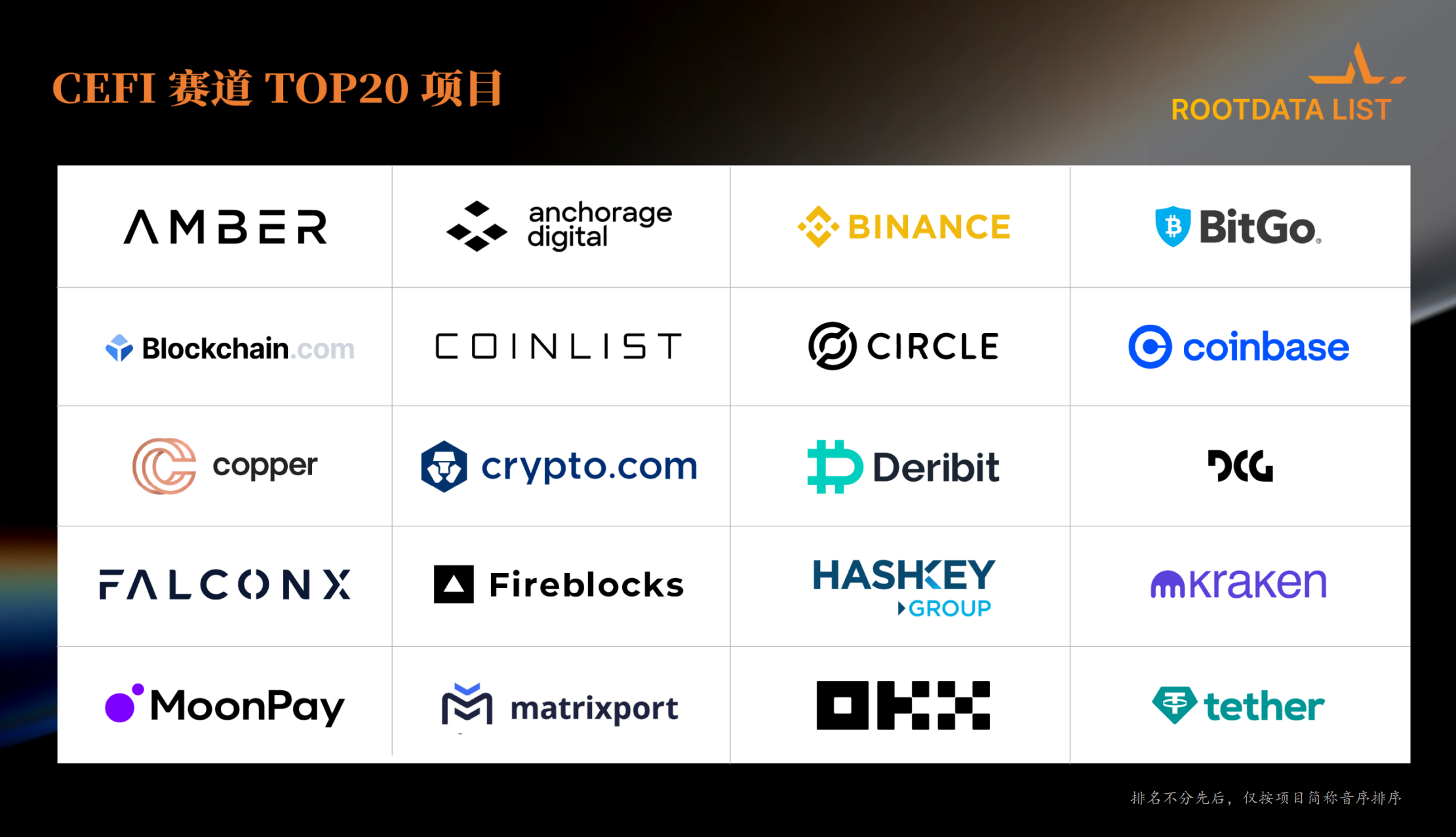

3.5. Research and analysis of the top ten projects with annual financing amount on the CeFi track

3.6. Research and analysis of the top ten projects with annual financing amount in GameFi track

2023 ROOTDATA LIST list

4.1. Top 50 projects in Web3 industry

4.2. Top 100 investment institutions in Web3 industry

4.3. Web3 industry vertical track list

Top 20 projects on the CeFi track

Layer 1 Track Top 20 Projects

GameFi Track Top 20 Projects

Top 20 projects on the DeFi track

Layer 2 Track Top 20 Projects

Top 20 projects in the SocialFi track

The Web3 industry as a whole shows a strong recovery trend. Bitcoins highest annual increase reached 160%. The return on investment leads the worlds major asset classes. Bitcoin spot ETF has become a new entry channel for incremental funds.

The total financing amount of the Web3 industry will reach US$9.043 billion in 2023, and the financing performance of different tracks is also different. Enterprise-level infrastructure and wallet directions are favored by capital. In the DeFi trend, DEX competition is fierce, and derivatives and RWA have attracted much attention. The total financing amount of the CeFi track has declined, but the Bitcoin ecological opportunities have attracted capital attention.

Finding new native assets with the greatest consensus has become an important rule for the development of the Web3 industry. The number of developers increased by 66% year-on-year, and the Ethereum ecosystem leads the trend with its overwhelming advantages. Popular sectors are concentrated in traditional areas such as DeFi, L1/L2, and Game, but opportunities in compliance and social directions are becoming an important consensus in the market.

In 2023, more than 10 institutions will lead investment at least 8 times. HashKey Capital topped the list of annual investments for the first time, with extensive deployment in infrastructure, DeFi and other directions in the Asia-Pacific region. DWF Labs became the dark horse of the year, mainly investing in projects that have already issued coins and are not very popular in the market.

1. Overall trend characteristics of Web3 industry

1.1. Secondary and macro analysis: Bitcoin leads the global increase in major asset classes, and spot ETFs open up a new dimension of market growth.

1. Bitcoin: The highlight of the global asset field

Bitcoin is having a great year as an asset class in 2023. According to NYDIG, as of October 2023, Bitcoin has become the best-performing asset among 40 selected asset classes with a gain of 63.3%. This outpaced the 28.2% gain in U.S. large-cap growth stocks, as well as other major asset classes such as U.S. equities (12.2%), commodities (6%), cash (3.8%) and gold (1.1%). Furthermore, Kaiko Research’s analysis shows that despite facing tight macroeconomic conditions and headwinds in the crypto industry, Bitcoin still rose by more than 160% in 2023.

2. Bitcoin Halving: New Opportunities for Market Supply and Demand

The Bitcoin halving event will occur in Q2 2024. Historically, Bitcoin’s price has risen significantly after each halving, but this has also been accompanied by increased volatility. On the demand side, according to Glassnode data, as of December 22, 2023, the number of non-zero balance Bitcoin addresses has exceeded 50 million. The increase in this figure reflects the growth of the user base. Together, these factors influence Bitcoin’s market value and trading activity.

3. Bitcoin Spot ETF: Leading the Growth Trend

The Bitcoin spot ETF market has been a standout, with trading volume exceeding $1.8 billion on January 16, three times the volume of the 500 other ETFs combined on the same day. Trading volume in the first three days was nearly $2 billion. Primarily including funds managed by Grayscale, BlackRock and Fidelity. Standard Chartereds head of foreign exchange research predicts inflows could hit $50 billion to $100 billion in 2024. This reflects high interest and growth potential in these ETFs.

4. Monetary policy changes: Catalyzing the new bull market wave of Web3

The last bull market was associated with loose monetary policy in the United States, and the latest data suggests the Federal Reserve may cut interest rates in 2024. In this context, cryptocurrencies such as Bitcoin may become a diversification choice for investors due to their non-correlated and safe-haven properties. After the approval of the Bitcoin spot ETF, Bitcoin shifted from individual investment to institutional investment, reducing circulation and increasing scarcity. The Federal Reserves interest rate cut expectations and inflation countermeasures may prompt more investors to allocate Bitcoin, heralding the beginning of a new bull market cycle in the Web3 industry.

1.2. The total investment and financing in 2023 will reach US$9.043 billion, and the primary and secondary markets will jointly promote the recovery and growth of the Web3 industry

Stimulated by the positive effects of Bitcoin spot ETFs, the price of BTC ushered in a breakthrough after testing the 30,000 mark multiple times. With the markets bullish sentiment prominent, as of December 31, the total financing of the Web3 industry in 2023 reached 9.13 billion US dollars, of which in a single month The highest amount of financing reached US$1.312 billion in November, and the amount of financing in Q4 was three quarters ahead. This is due to the short primary and secondary transmission paths of the Web3 industry, which shows that the primary market is gradually entering the track of recovery and growth.

Since entering the Q3 quarter of 2023, many funds have announced the completion of fundraising. Web3 fund Lightspeed Faction announced the completion of fundraising of US$285 million (14% over-raising). Standard Chartered Bank and Japanese financial giant SBI launched a US$100 million Web3 fund, supported by Li Zekai Web3 fund CMCC Global completed US$100 million in fundraising.

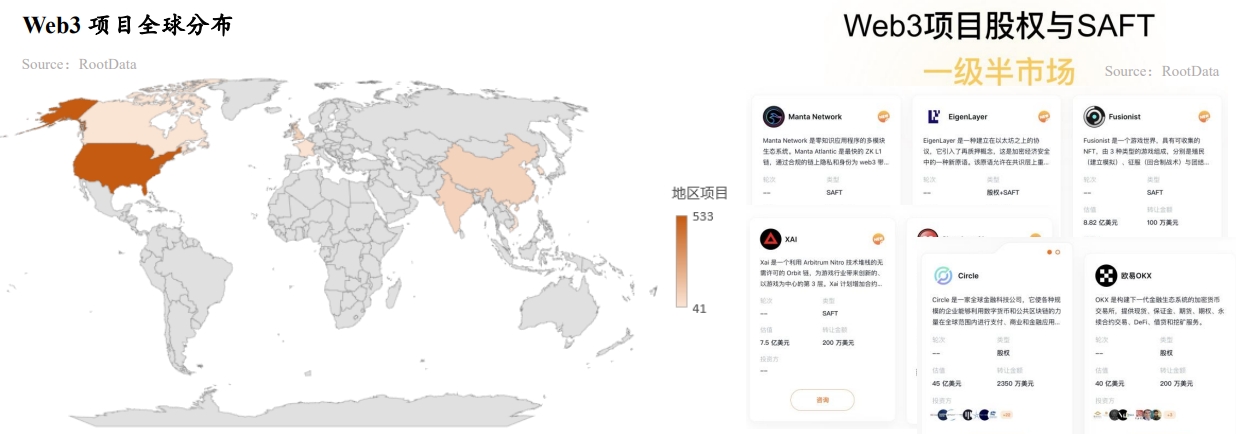

1.3. The primary and semi-level market is becoming a new choice for investment or exit. Fireblocks’ over-the-counter valuation has retreated the most, and EigenLayer’s over-the-counter valuation has increased the most.

As Web3 accelerates towards compliance, the high degree of linkage between the primary and secondary markets is more likely to cause investors FOMO emotions and high project valuations. More and more investors are considering the primary and semi-markets as important investment and exit paths.

Among the 45 projects listed on RootData’s primary and a half market, Fireblocks’ OTC valuation has retracted the most compared to its financing valuation, by approximately $4 billion. Copper and Dune Analytics both have off-market valuation retracements of approximately several hundred million dollars. EigenLayer has performed strongly and is now valued at $2.5 billion in over-the-counter transactions, five times its latest funding round valuation of $500 million. The off-market valuations of projects such as Aleo and LayerZero are relatively stable.

1.4. Infrastructure and CeFi will dominate the development of the Web3 industry in 2023, with 6 new unicorns

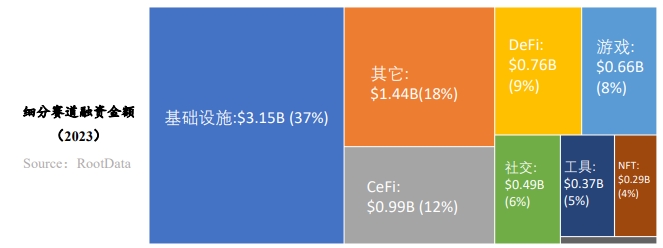

According to RootData data, infrastructure, CeFi, games, NFT, DeFi, etc. have been the tracks with the largest capital inflows in the past three years. The average amount raised in 2023 is $9.9 million, down by about half from $18.8 million in 2022. Even though the industry has gone through a two-year bear market, infrastructure has always been a hot topic.

As of December 31, 2023, a total of 91 unicorn projects have been born in the Web3 industry, of which 32 are CeFi, 29 are infrastructure, and 8 are NFT. However, the market has been sluggish in the past two years and the pace of investment in the primary market has slowed down. As a result, the number of Web3 unicorn projects (Andalusia Labs, Scroll, Flashbots, BitGo, Wormhole, Ramp) that will emerge in 2023 will only be 1/5 of that in 2022. .

1.5. The Web3 industry is becoming mature: the number of dead projects will decrease by 50% year-on-year in 2023

According to RootData data, about 120 projects declared bankruptcy or ceased operations in 2023, with a cumulative financing amount of US$940 million. Compared with the 239 projects that died in 2022, the total financing was US$4.033 billion, showing a significant decrease overall, reflecting that the industry is gradually maturing and stabilizing. These dead projects are distributed in various tracks, with the DeFi track having the most dead projects (40), followed by CeFi (18) and infrastructure (16).

Among the failed projects, the top three financing projects are Prime Trust (cumulative financing of US$163 million), Voice (cumulative financing of US$150 million), and Rally (cumulative financing of US$72 million). Insufficient funds are the main and most direct reason why projects cease operations. Other reasons include lack of market fit of products, stricter regulatory policies, hacker attacks, etc.

2. Web3 asset development characteristics and sector trend analysis

2.1. Four waves of innovation in the Web3 industry: Looking for native new assets with the greatest consensus

The essence of the four waves of innovation in the Web3 industry is to find new native assets with the greatest consensus. New assets drive the influx of funds, so it is important to find the paths and scenarios for the birth of new assets in the Web3 industry, especially native assets, because compared to non-native assets, It has less resistance and more narrative space.

2.2. The number of Web3 developers increased by 66% year-on-year, and the Ethereum ecosystem has an overwhelming advantage

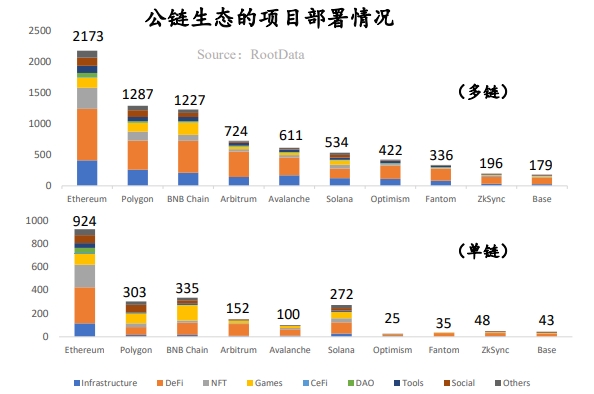

The Ethereum ecosystem has the greatest advantage: Whether it is a single chain or multiple chains, the Ethereum ecosystem has overwhelming advantages, and the rest of the ecosystem mainly takes over the value overflow of Ethereum;

Solana has become the most outstanding public chain in 2023: the SOL token has increased by nearly 1,000%, the Solana Foundation announced that the number of monthly active developers has remained above 2,500, and ecological star projects have taken turns to enter the battle, whether it is the old DeFi projects Raydium, Orca, Solend, It is also the current star projects such as Jito, Jupiter, and Pyth Network, which have gradually formed unique ecological advantages.

The number of developers has increased overall compared with the previous cycle: compared with the last bear market, the number of developers has increased by 66%;

Changes in developer types: Mature developers and builders are still strong in the Web3 industry, and speculative developers are leaving in batches; judging from the full-year data for 2023, the biggest changes in this bear market are novice developers (the number decreased by 58%) , and the number of experienced developers is growing, with developers with more than 1 year of experience accounting for 75% of code submissions.

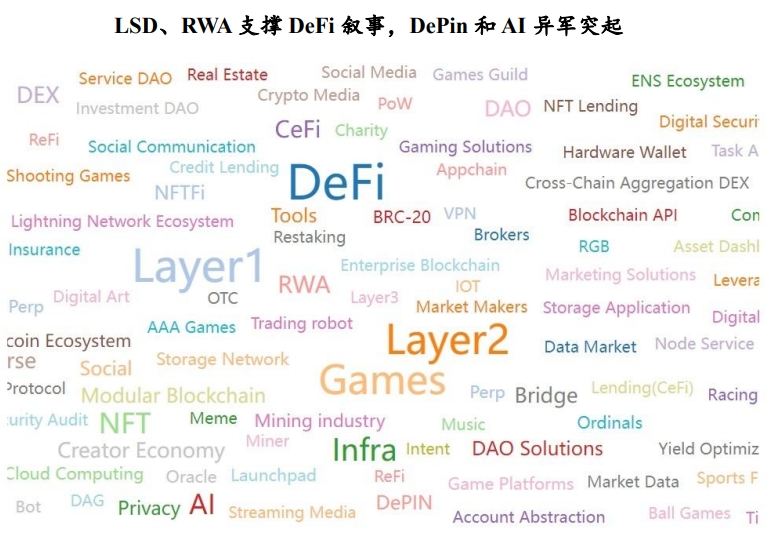

2.3. Rotation of popular Web3 sectors: L1/L2, DeFi, and Game are still the tracks that the market pays most attention to. Layer 3, Restaking and other sectors are receiving market attention.

Judging from the millions of tag clicks on RootData, DeFi, L1/L2, and Games are the most popular tags. Lido, the leading staking service, and MakerDAO, the RWA concept pioneer, have brought the DeFi track back to life.

Sectors such as Layer 3, Intent and Restaking are receiving market attention. EigenLayer introduces Ethereum-level trust into middleware and has created a new re-staking ecosystem.

In 2023, Binance will list a total of 26 new currencies, covering more than 20 popular tags such as infrastructure, Layer 1, and Meme. Tags such as NFTFi, DAG, and DOV will see a greater decline in search popularity.

2.4. Stanford is the Web3 practitioner with the most output, and Google has the highest amount of project financing.

Judging from education and work experience, the United States, China and Singapore are the most important countries where Web3 projects were born. Mainstream Web3 practitioners basically have both financial and technical capabilities and resources.

The Web3 entrepreneurial team from Harvard University and the Google entrepreneurial team have the highest cumulative financing amount. The Web3 entrepreneurial team from Peking University ranks fifteenth in cumulative financing amount, and the Binance entrepreneurial team ranks tenth in cumulative financing amount. Among Chinese, Binance and HTX have the largest number of entrepreneurial teams. In addition, the number of entrepreneurial teams from OKX and Bitmain is increasing. Non-native Chinese practitioners mainly come from Alibaba and Tencent.

3. Web3 capital flow characteristics and trend analysis

3.1. Analysis of the style and activity of Web3 investment institutions in 2023: HashKey Capital is most willing to invest, and a16z Crypto prefers to lead the investment

Hashkey Capital becomes the institution with the most transactions in the year

HashKey Capital topped the list of annual investments for the first time, with a wide range of investments in infrastructure, DeFi and other directions, with a special focus on projects in the Asia-Pacific region. In January 2023, it announced that its third phase of funds had completed US$500 million in fundraising, providing strong support for its high-frequency investments. Typical investment cases: MyShell, DappOS, Supra, SynFutures, PolyHedra.

DWF Labs becomes the dark horse of the year

DWF Labs mainly invests in projects that have issued coins and are not very popular in the market, and its style has caused a lot of controversy. Typical investment cases: EOS, Conflux, Mask Network, Synthetix, Fetch.ai.

a16z Crypto prefers leading and large investments

a16z Crypto prefers leading and large investment styles, and maintains an active investment posture in infrastructure, games, entertainment and other fields. Typical investment cases: Gensyn, Mythical Games, Proof of Play, Story Protocol, CCP Games.

More than 10 institutions will lead at least 8 investments in 2023

In terms of the number of leading investments, Andreessen Horowitz, Polychain, Bitkraft Ventures, Dragonfly, 1kx, Hack VC, Shima Capital, Jump Crypto, and ABCDE Capital ranked among the top ten in 2023, leading at least 8 times.

3.2. Analysis of the increase and decrease in the number of transactions by Web3 investment institutions in 2023: Animoca Brands has the largest contraction in the number of transactions, with 85 institutions investing more than 10 times throughout the year

Judging from the number of investments, a total of 85 investors made more than 10 times, and 9 investors made more than 30 times, a sharp decline from 2022. This reflects that the vast majority of investment institutions are affected by difficulties in raising funds and lack of confidence. Due to the influence of the reasons, the frequency of investment has been significantly reduced.

Among them, the number of investments by investment institutions such as Animoca Brands, GSR, Coinbase Venture, Shima Capital, Spartan Group, a16z, Paradigm, Circle Ventures, and Mirana Ventures has dropped significantly in 2023, falling by more than 40%.

Web3 investment institutions generally face difficulties in raising funds. Only Blockchain Capital, HashKey Capital, CMCC Global, Bitkraft Ventures, No Limit Holdings and other institutions have announced that the amount of funds raised exceeds 50 million US dollars.

At the same time, a small number of investment institutions are also accelerating the frequency of investments to inject momentum into the bleak market. According to statistics, the number of investments from ABCDE Capital, Superscrypt, Foresight Ventures, OKX Ventures, Sora Ventures, No Limit Holdings and other institutions has increased significantly in 2023, rising by more than 50%.

During the Bitcoin ecological craze at the end of the year, institutions such as ABCDE Capital, Sora Ventures, and Waterdrip Capital remained active and became major investors in Bitcoin ecological projects.

3.3. Infrastructure track: The largest financing case of the year was born in the cross-chain direction, and enterprise-level infrastructure and wallet directions are sought after by capital.

The largest financing case of the year was born in the cross-chain track

Wormhole announced the completion of US$225 million in financing in November 2023, becoming the highest-financing project of the year. Cross-chain is also one of the hottest industry trends in 2023. With the widespread emergence of Layer 1, Layer 2 and even Layer 3, users cross-chain demand for assets and data is growing rapidly. Wormhole and LayerZero have broken down the barriers between various blockchains through cross-chain communication.

The wallet serves as a traffic portal to gain capital support.

As the entrance to user traffic, the wallet track is still the target of capital injection. Both the encryption hardware wallet Ledger and the social login wallet Magic have received huge amounts of financing, reflecting users needs for wallet security and convenience respectively. Their development and evolution are the key to the blockchain hosting the next billion users.

Enterprise-level infrastructure becomes the focus of layout

Enterprise-level infrastructure has become the focus of the layout. Auradine, the digital asset custody and issuance infrastructure, and QuickNode, the blockchain development platform, are mainly targeted at enterprise-level customers, helping companies solve asset issuance, application development and other issues on the asset side, thereby delivering a steady stream of high-quality assets and projects to the market.

3.4. DeFi track: DEX competition continues to intensify, derivatives and RWA have become the focus of the industry

Derivatives agreements become the focus of capital attention

Derivatives protocols are the focus of the DeFi field. Focusing on perpetual contracts, synthetic assets, structured products, etc., protocols such as SynFutures, Thetanuts Finance, and Synthetix have received capital support. Their core highlights are more transparent and permissionless operations. mechanisms and more user-friendly products.

Competition on the DEX track is intensifying in compliance, order book, cross-chain and other aspects

There are also many bright spots in the decentralized trading track. Mauve, which focuses on compliance, tanX, which focuses on order book trading, and iZUMi Finance, which focuses on multi-chains, are competing for market share from leaders such as Uniswap through market segmentation and functions, and are being Investment institutions have high hopes.

The market has high expectations for RWA

RWA assets are becoming the most watched direction in the DeFi market. Since real estate, treasury bonds, bills and other assets have stable yields, RWA can provide sustainable and rich types of real yields for the crypto market. Superstate, newly founded by the founder of Compound, is one of the latest major players in the RWA track. The project is committed to purchasing short-term US Treasury bonds and tokenizing them on the chain, which can be directly traded on the chain.

3.5. CeFi track: The total amount of financing dropped the highest among the major tracks, and the Bitcoin ecological opportunities are sought after by capital.

The highest decline among major circuits

In 2023, the total financing amount of the CeFi track was US$1.18 billion, a decrease of 75.%, which was the highest decline among the major tracks. This is mainly affected by the CeFi vicious thunderstorm event starting in 2022.

Bitcoin-related financial services receive capital bets

Bitcoin-related financial services have attracted the most attention from capital. Swan, Unchained, and River Financial all provide solutions for the Bitcoin ecosystem, providing savings, lending, brokerage and other services. As the most valuable crypto asset, Bitcoin provides its holders with various solutions and creates huge untapped value.

The exchange track undergoes a turning point

After the FTX incident, the vacant market space in the exchange track still attracts the attention of many capitals. Exchanges such as Blockchain.com and One Trading have obtained huge amounts of financing by virtue of their vertical business, regional or license advantages.

3.6. GameFi track: total financing fell by more than 57%, 3A games are still favored by investment institutions

The overall financing amount of GameFi track fell by more than 57%

Affected by the secondary market conditions, the overall financing amount of the GameFi track dropped significantly by more than 57%. Large-scale financing was mainly initiated by a16z Crypto, Griffin Gaming Partners, Bitkraft Ventures and other institutions.

Playability first becomes the mainstream trend

3A games are especially favored by investment institutions, and the prospects of Web3 for traditional games such as football, shooting, and adventure are also promising. Playability has become the trend of GameFi; in addition, full-chain games are receiving high hopes from capital and the market.

4. 2023 ROOTDATA LIST

Web3 is becoming an important transformative force that cannot be ignored in the global society. In order to more clearly present the power of Web3 that has made great contributions, RootData relies on its leading and rich data advantages and more than 10 million visits and queries from users, adhering to the professional, objective, and Based on the principles of rigor and fairness, we are committed to creating a data-driven list with industry credibility - ROOTDATA LIST, which will present more industry representatives in the Web3 field and help the industry develop with high quality.

The 2023 ROOTDATA LIST list includes WEB3 Industry Top 50 Projects, WEB3 Industry Top 100 Investment Institutions, CEFI Track Top 20 Projects, DEFI Track Top 20 Projects, LAYER 1 Track Top 20 Projects , LAYER 2 Track Top 20 Projects, GAMEFI Track Top 20 Projects, SOCIALFi Track Top 20 Projects.

Selection criteria description:

Institutional selection: The core measurement indicators include the number of investments, the number of leading investments, the quality of investment projects, media popularity, RootData popularity, etc.

Project Selection: Core measurement indicators include market capitalization/valuation, media popularity, total lock-up value, financing amount, RootData popularity, investment institution quality, narrative and track position.

About RootData

RootData is a data platform for Web3 asset discovery and tracking. It is the first to encapsulate the on-chain and off-chain data of Web3 assets. The data is more structured and more readable. It is committed to becoming a productivity-level tool for Web3 enthusiasts and investors.

Note: This report was produced by RootData Research. Neither the information nor the opinions expressed in this report constitute investment strategies or recommendations for anyone. The information, opinions and speculations contained in this report only reflect the judgment of RootData Research on the date this report is released, and past performance should not be relied upon as a basis for future performance. At different times, RootData Research may issue reports that are inconsistent with the information, opinions and speculations contained in this report. RootData Research does not guarantee that the information contained in this report is kept up to date and reliance on the information in this material is at the readers discretion, which is provided for informational purposes only.

This report can be accessed through theLinkDownload PDF full version.