From the perspective of on-chain data and derivatives, has a bear market arrived?

Original compilation: 0x137

Original compilation: 0x137

This article is based on the opinions of Dylan LeClair, a co-creator of 21st Paradigm, on his personal social media platform. Rhythm BlockBeats organizes and translates them as follows:

first level title

On-chain data analysis

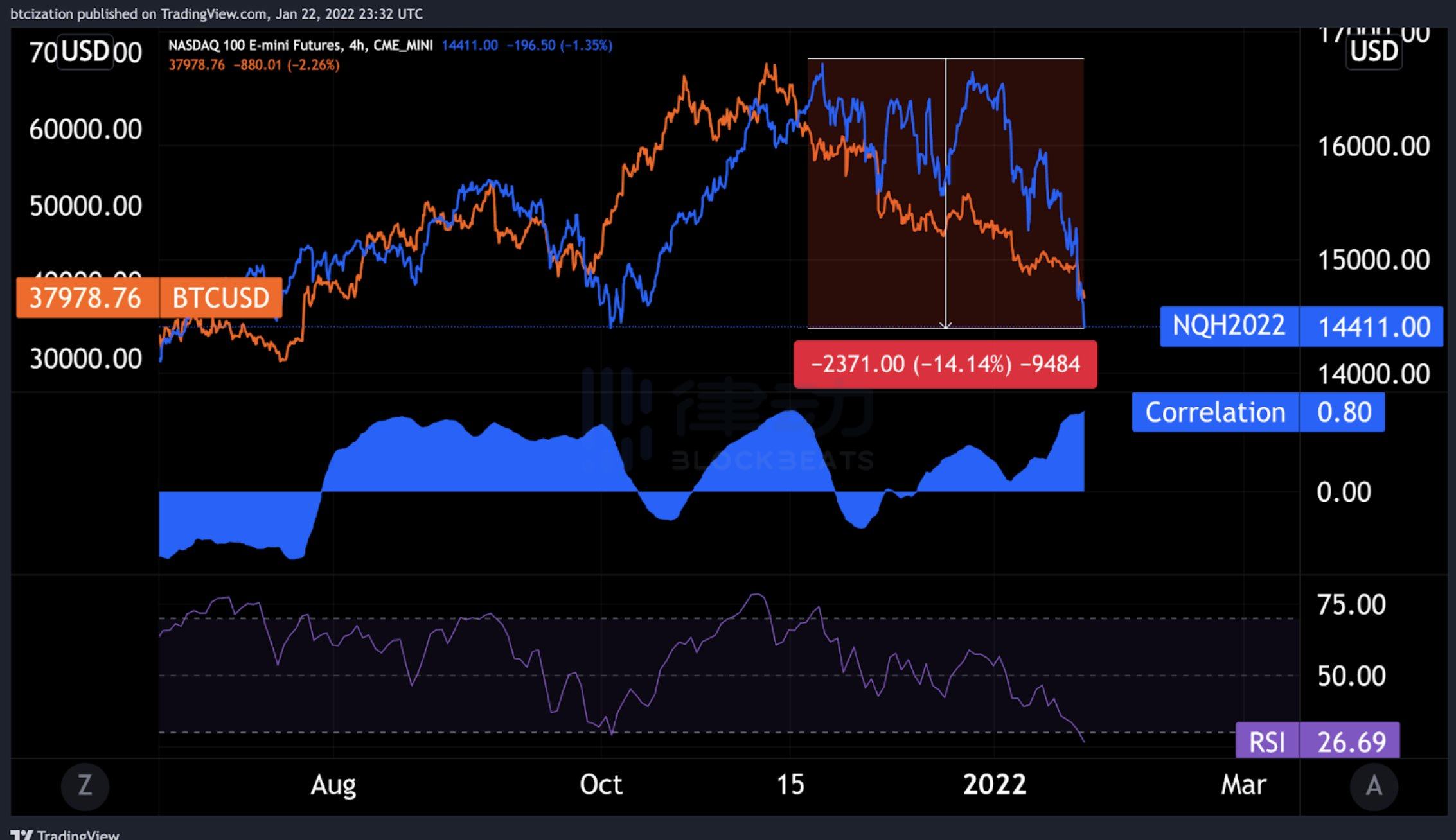

One of the hottest topics of late has been Bitcoin's correlation with the Nasdaq (and other types of risky assets). Currently, the Nasdaq is down 14% from its peak, the most oversold since March 2020. The 30-day correlation index between Bitcoin and Nasdaq is as high as 0.80.

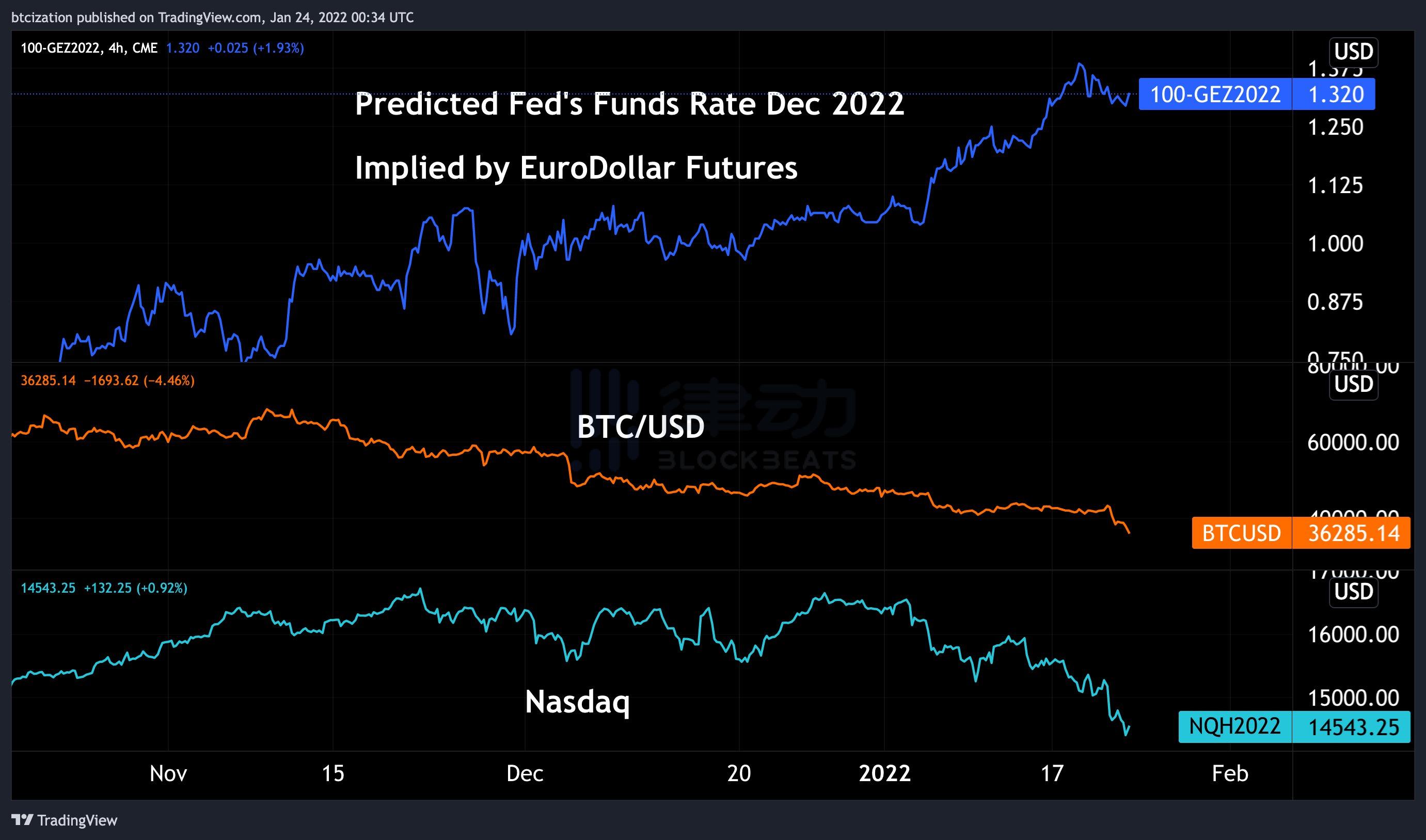

Eurodollar futures can be seen as a market reflecting Fed Funds rate expectations, which have already reacted to 4 rate hikes in 2022. When there is an expectation of tightening loose monetary policy, the market will inevitably react.

The increasing acceptance of Bitcoin by macro funds between 2020 and 2021 makes Bitcoin more and more like a highly correlated risk asset. We can look at one of the early drivers of the bull market, Grayscale, which acquired nearly 400,000 Bitcoins on behalf of accredited investors and institutions in exchange for Grayscale shares (GBTC).

These investors sought to buy GBTC at net asset value from Grayscale and mark their books with a premium for a "risk-free" arbitrage trade, but when GBTC began trading at a price below net asset value in February last year, they realized This arbitrage model has been broken.

Note, however, that $650,000 worth of Bitcoin is still traded as a derivative in Grayscale shares on the over-the-counter market. And as its premium turned into a discount, funds began to stop entering the market, and the incentive for investors to allocate funds to GBTC instead of Bitcoin itself also emerged.

GBTC has also been indiscriminately sold off as the market has recently switched to de-risking mode, with GBTC’s discount to net asset value widening to a record low, but this also makes sense given the situation of many trust holders: they are with The macro investors allocating capital to Bitcoin in 2020-2021 are the same people.

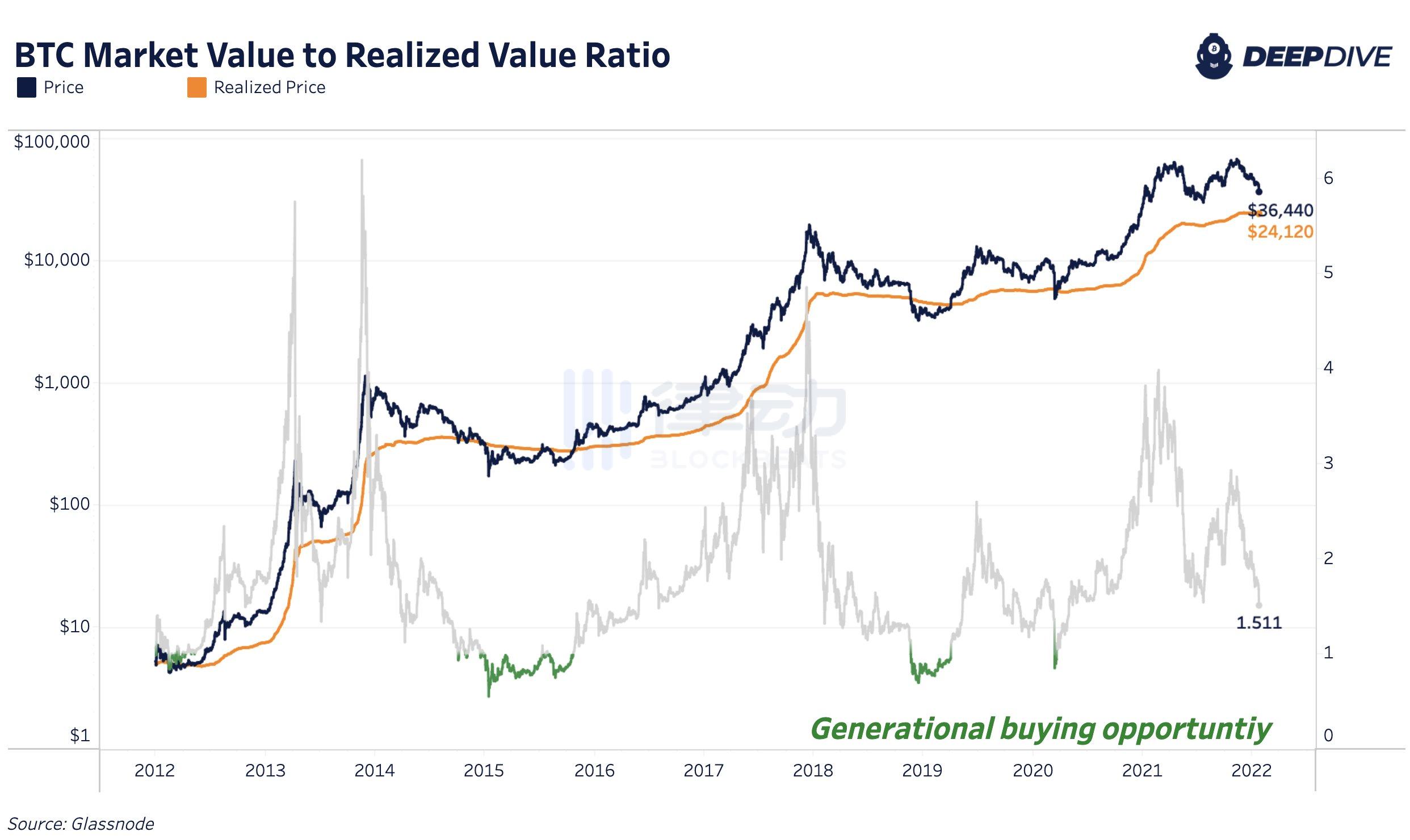

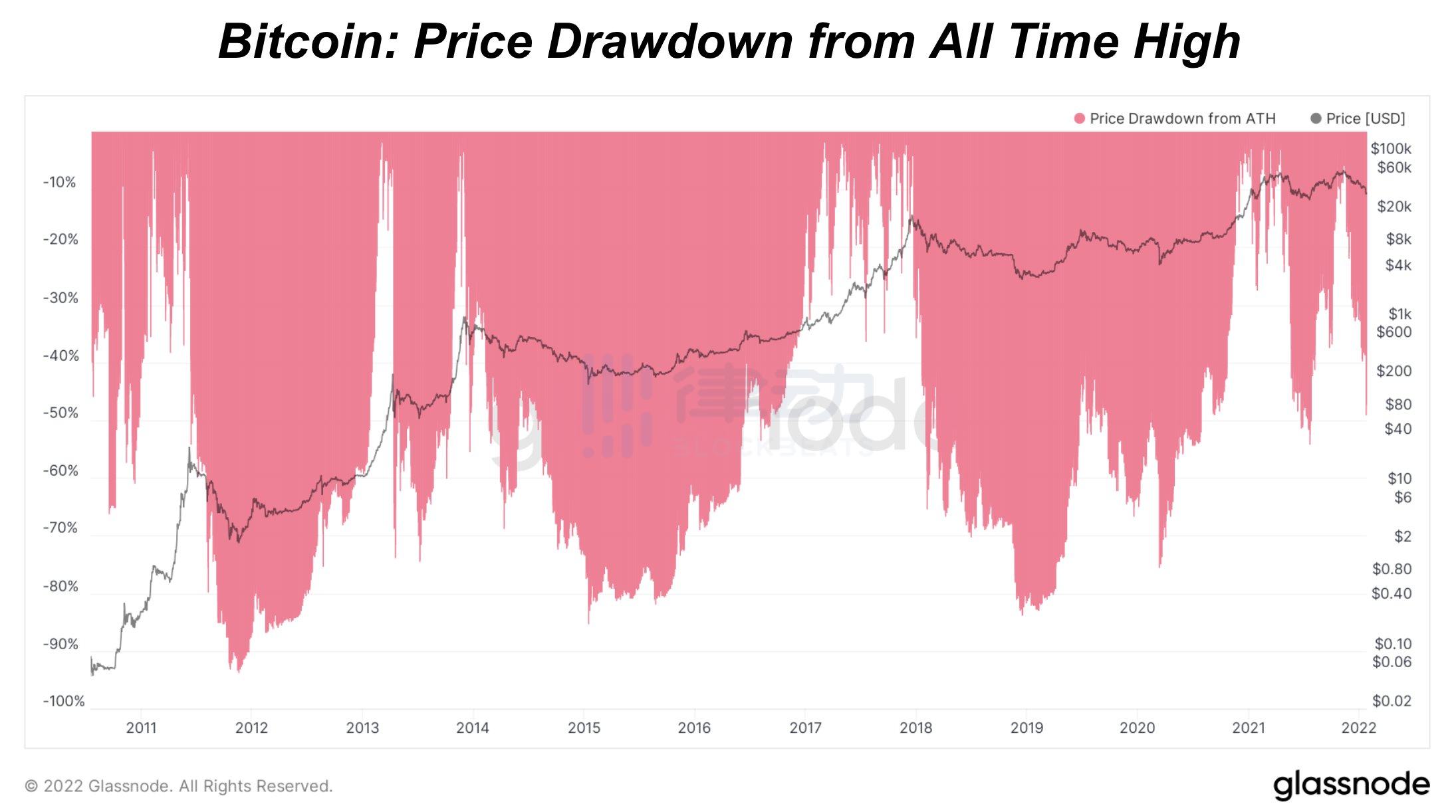

Let's now look at where the current Bitcoin trading price is relative to historical valuations.

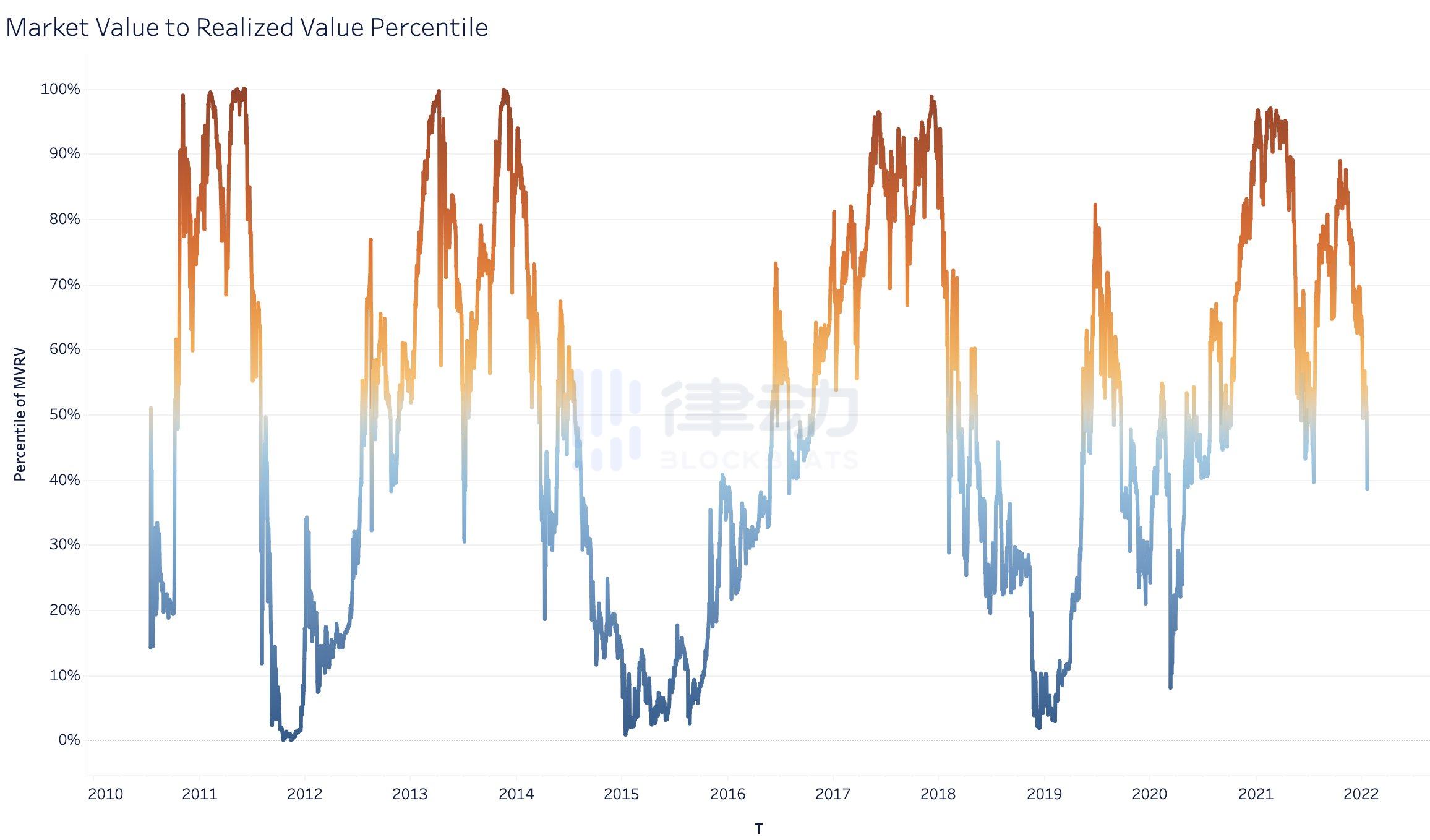

The MVRV ratio (the ratio of cost basis to price) shows Bitcoin's historical boom and bust cycles. The current on-chain cost basis for Bitcoin is $24,000 with an MVRV ratio of approximately 1.5.

Bitcoin's current MVRV ratio is in the 38th percentile of historical readings. Past data has shown that when Bitcoin falls below the actual price (MVRV below 1.0), it is almost always an excellent buying opportunity. While Bitcoin won't necessarily drop to $24,000, the price will certainly be very attractive to buy.

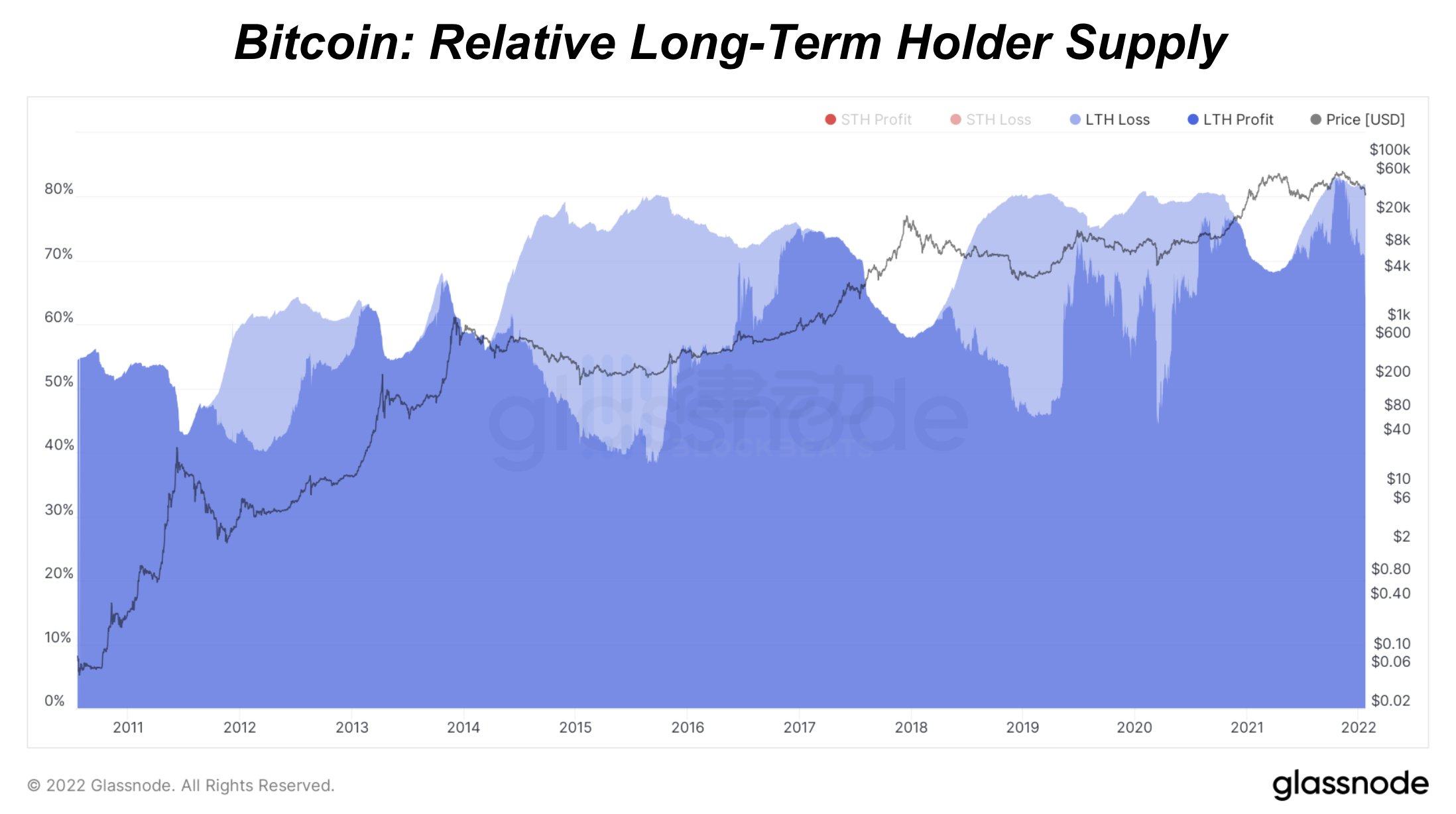

We have also seen long-term holders continue to sell during the downtrend of the past few months. sell in trend.

Obviously macro concerns are one of the driving factors behind it, but the good news is that the trend of hoarding coins has now started again.

first level title

text

For Bitcoin derivatives, the following points need to be focused on:

1. Perpetual futures

2. Quarterly Futures

secondary title

Perpetual futures

Perpetual futures funds show whether the derivative is higher or lower than the price of spot bitcoin. The speculative bulls are no longer dominant at the moment, but the bears are not overly aggressive either. Market bottoms are often characterized by persistent negative funding, accompanied by extreme greed by bears in the derivatives market.

secondary title

quarterly futures

secondary title

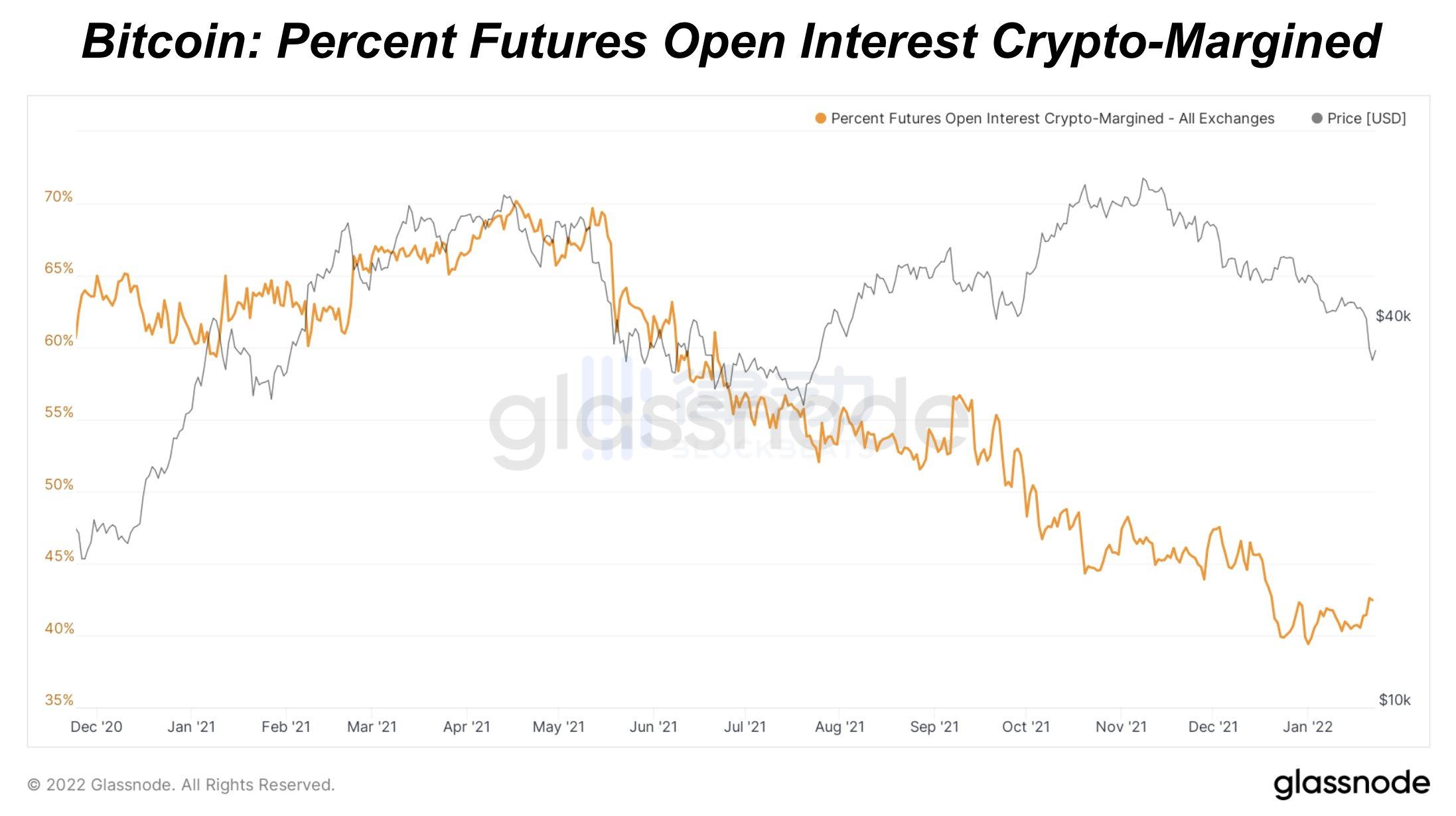

Collateral Types Used to Enter Derivatives Contracts

The use of crypto collateral for Bitcoin futures continues its long-term downward trend, which is a positive development as stablecoins do not exhibit convex relationships during market downturns like Bitcoin margin futures do.

DXY, an indicator used to measure the value of the U.S. dollar against other fiat currencies, has been on an upward trend since early 2021. As the Fed tries to tighten policy, it will be critical to watch the dollar strengthen as a strong dollar is not good for any asset.

first level title

Macro market analysis

From a macro perspective, a key question is when will the marginal selling of macro funds turn into marginal buying?

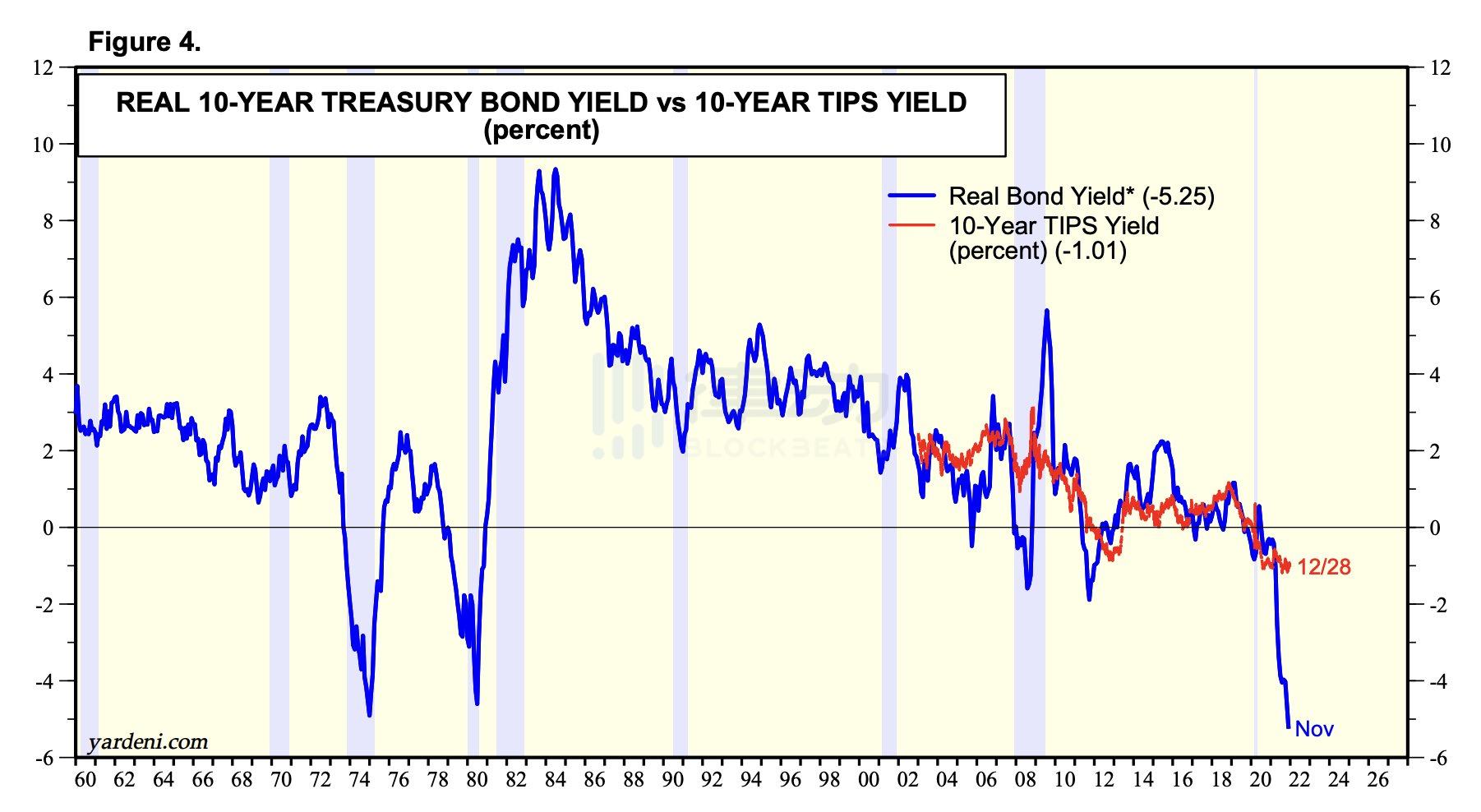

The reality is that dollar bonds with negative real yields are worth tens of trillions, meaning they are doomed to lose money. So when the Fed changes its tightening policy, Bitcoin is bound to skyrocket. Yes, "when" not "if".

In the long-term debt cycle, the outcome of economic development can only be binary. In a true deflationary scenario, there would be unlimited counterparty risk as fiat debt is discharged across the economy.

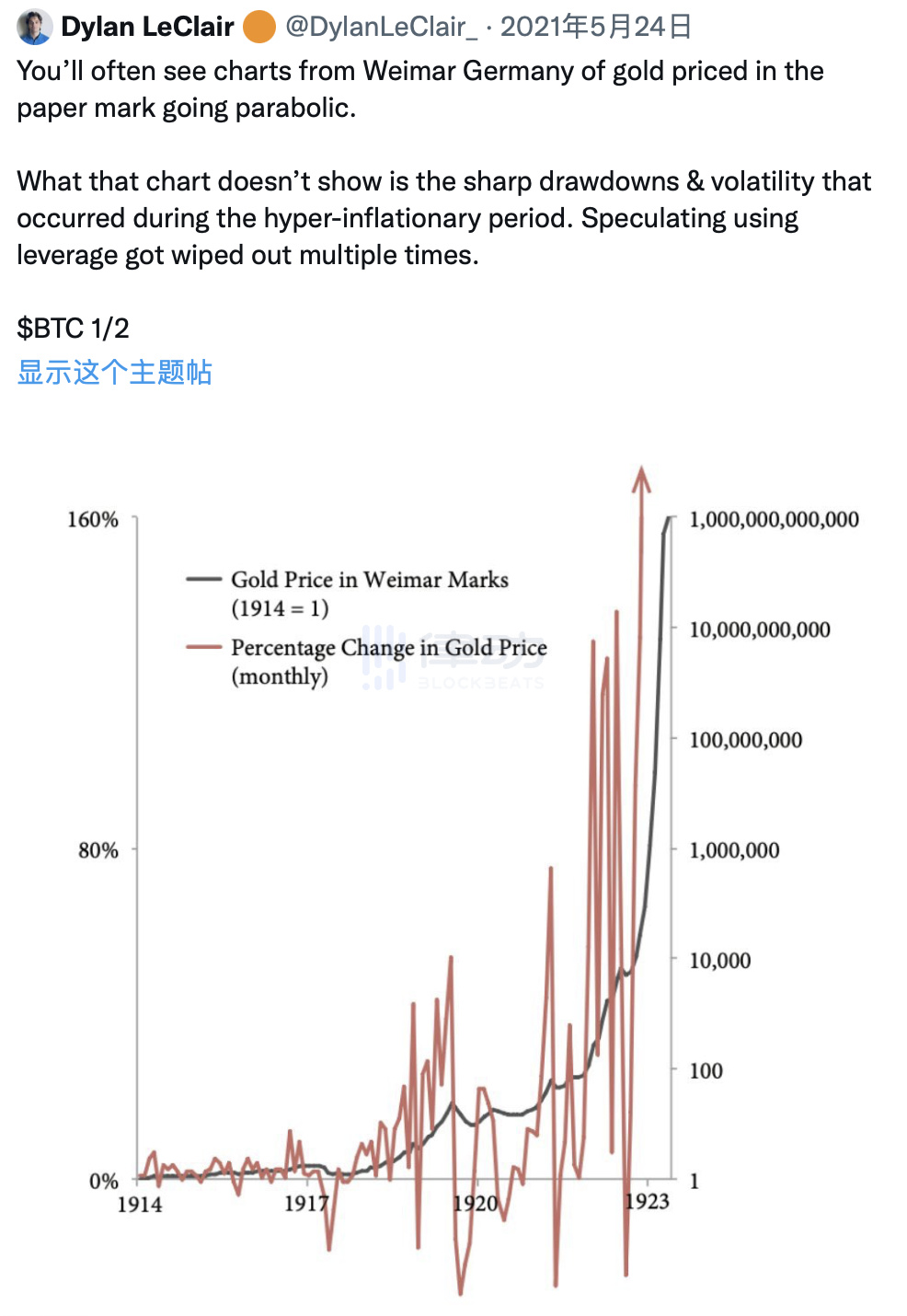

Will there be more disadvantages? Maybe, especially if the stock market decline continues and spills over into credit markets. If you were a leveraged gold holder during the Weimar Republic, this would have resulted in you being liquidated multiple times. Although the United States is not Weimar, we can still learn lessons from it.

Original link

Original link