当 Crypto「藏」進傳統金融:預測市場、穩定幣與代幣化股票,如何走向主流?

- 核心觀點:加密貨幣的「大眾採用」路徑正發生逆轉,不再要求用戶先理解區塊鏈,而是將其作為底層基礎設施,透過預測市場、穩定幣和代幣化股票三大賽道,主動嵌入並改造傳統金融與大眾應用場景。

- 關鍵要素:

- 預測市場破圈依賴低認知門檻的公共事件,如世界盃,將複雜風險定價轉化為直觀的機率,正逐步從事件交易工具演變為金融基礎設施。

- 穩定幣競爭重點從鏈上存量轉向合規支付與清算場景,如 Open USD 透過向渠道夥伴傾斜儲備收益,正成為傳統企業可調用的資金流轉元件。

- 傳統交易所(如 ICE)與加密平台(如 OKX)合作推出代幣化股票,標誌著傳統資產正式進入鏈上帳戶,推動錢包成為管理全球資產的統一入口。

- 代幣化股票需明確法律差異(如所有權與受益權),其最終用戶權利仍依賴於鏈下的發行主體和託管機構,並非自動等同於傳統股東權益。

For a long time, when the crypto industry talked about "mass adoption," it usually pointed to a few relatively familiar metrics:

For example, how many people hold Bitcoin, how many addresses interact with on-chain protocols, and how many users have started using wallets, exchanges, and DeFi.

This implies a relatively linear imagination: that ordinary users first need to understand Crypto, then purchase crypto assets, create wallets, and finally gradually enter the on-chain world.

However, recent changes may be reversing this path. Users don't necessarily need to understand blockchain first before starting to use crypto infrastructure. Instead, existing demands like prediction markets, cross-border transfers, and stock trading are actively absorbing crypto technology. Although these seem to belong to three different tracks and the penetration doesn't happen along the same path, they all point to the same change:

Crypto is transitioning from a new financial system that requires users to actively enter, into infrastructure that traditional finance and mainstream applications can directly call upon.

1. Prediction Markets: From On-Chain Event Trading to Probability Pricing Tools

As we all know, prediction markets are not a new concept.

Especially in the crypto world, early in Ethereum's development, the prediction market Augur was the first DApp on Ethereum, initially verifying that any event whose outcome can be objectively verified can be turned into an on-chain contract, and through real capital buying and selling, project the market's judgment of the future.

However, for a long time afterward, prediction markets were simply summarized as "on-chain gambling" and never really broke out of the crypto-native circle. Early users of platforms like Polymarket were indeed mainly crypto-native groups familiar with wallets, stablecoins, and on-chain trading:

On one hand, the barriers to using wallets, stablecoins, and on-chain trading limited ordinary users' participation; on the other hand, even though Polymarket once broke through to the mainstream thanks to events like the US election, its core participants were still mainly traders familiar with Crypto.

But the 2026 FIFA World Cup in the US, Canada, and Mexico provides a more mainstream observation window for prediction markets (see also: World Cup Frenzy, Prediction Markets Join the Table: How are Polymarket and Others Cracking the Mass Adoption Nut?).

Compared to monetary policy, economic data, and political elections, football matches require almost no additional knowledge education. Questions like who will advance from the group stage, which team will reach the semi-finals, or whether a certain player will become the top scorer are exactly what fans discuss every day.

What prediction markets do is simply turn these scattered opinions into a price that can change in real time. This is why it is said that for prediction markets to truly break through to the mainstream, regulatory changes alone are not enough; they also need a sufficiently large and intuitive public event, and the World Cup perfectly fits this condition.

Many of Crypto's past breakthrough moments often occurred when "high-knowledge-barrier technology" combined with "low-knowledge-barrier scenarios." For instance, NFTs once broke through because they tied on-chain assets to avatars, art, and community identity; Memes spread quickly because they compressed complex financial behaviors into simple emotions and cultural symbols.

Similarly, the entry point for prediction markets to reach a wider user base may not necessarily be macroeconomic data or complex political contracts, but more likely scenarios like sports, entertainment, and events that the public is already willing to discuss.

The uniqueness of the World Cup lies in its inherent possession of three conditions:

- First, it has broad global consensus. Even non-hardcore fans can understand basic questions like who wins, who loses, who advances, and who will become champion.

- Second, it has a high-frequency information flow. Pre-match lineups, player form, injury reports, tactical changes, and the match process itself all continuously change market expectations.

- Third, it has strong social attributes. Watching a game is not an isolated act; it comes with group chats, sharing, discussions, debates, and emotional resonance.

At the same time, the competitive boundaries of prediction markets are constantly expanding. Especially recently, it is not only limited to vertical platforms like Kalshi and Polymarket but is increasingly integrated into traditional brokerages, crypto trading platforms, and even media products.

The reason is not complicated. Although traditional financial markets already have numerous risk pricing tools like options, futures, and interest rate swaps, these products usually have high barriers to understanding. It is also difficult for ordinary users to directly read market judgments from prices. Prediction markets compress complex problems into a more intuitive probability.

This is also key to how prediction markets might enter traditional financial infrastructure. They provide not just another way to bet, but a low-barrier, real-time updated expectation pricing tool.

Of course, this path still comes with significant controversy.

How events should be defined and settled, whether insiders can participate, whether financial event contracts constitute insider trading, and whether sports contracts should be subject to federal derivatives regulation or state gambling regulation – none of these are clearly defined yet. As the market scale grows, some Wall Street institutions have also begun to restrict employees from participating in prediction market trading involving economic data and company events.

However, regardless, the process of prediction markets gaining mainstream recognition is also the process of them gradually transforming from "open event trading experiments" into financial market infrastructure.

2. Stablecoins: From Crypto Assets to Payment and Settlement Infrastructure

If prediction markets are about bringing a crypto-native product into the mainstream, then stablecoins are taking a different path. They are gradually becoming hidden behind traditional payment products.

For most crypto users, stablecoins have long served as a medium of exchange. Users buy and sell other tokens with USDT or USDC, transfer funds between different exchanges, or put them into DeFi protocols to earn yields. Therefore, the issuance scale has long been considered a primary metric for measuring a stablecoin's competitiveness.

But entering the next phase, the competition for stablecoins may no longer focus only on on-chain存量. Instead, the key is who can complete regulatory positioning first and penetrate real-world scenarios like payments, settlements, and cross-border transfers.

One of the most discussed cases recently is Open USD, launched by the Open Standard, which involves over 140 payment, banking, technology, and crypto enterprises.

Unlike the traditional model where a single issuing entity primarily controls the reserve income, Open USD allows partner companies to mint and redeem for free and plans to distribute the income generated by the reserves to the partners driving its use, after deducting management fees.

Descriptions from Visa and Stripe also define OUSD as shared infrastructure for global capital flow. What is truly noteworthy about this design is not that another dollar stablecoin has been added to the market, but that it attempts to adjust the long-standing profit distribution model for stablecoins – in the past, issuers typically captured most of the income from reserve assets, while wallets, exchanges, payment companies, and fintech platforms bore the costs of user acquisition, product integration, and actual distribution.

If reserve income can be tilted more towards channels and usage scenarios, the competitive logic of stablecoins will change accordingly. This also explains why the entry of institutions like Stripe, Visa, Mastercard, and Zelle is more noteworthy than simply adding another on-chain asset.

Ultimately, stablecoins are transforming from a crypto product that users need to actively hold and manage into a capital flow component that traditional enterprises can directly invoke. What users see might be cross-border remittances, merchant settlements, corporate payments, payroll, or a payment card, but behind the scenes, the network used might be stablecoins and a public chain settlement network. Users may not even need to know stablecoins exist to benefit from the settlement capabilities they provide.

At the same time, some stablecoin products lacking actual distribution channels and use cases are also being phased out. This further illustrates that completing an issuance does not automatically give a stablecoin value.

As the underlying technology becomes standardized, the true moats will come more from licensing and regulatory adaptability, and the ability to embed into a business scenario that continuously generates transaction demand.

This also means that in the future, stablecoins' ultimate competition may not necessarily be against other stablecoins, but potentially against bank card networks, cross-border remittance systems, bank deposits, and corporate treasury infrastructure.

3. Tokenized Stocks: Traditional Assets Entering On-Chain Accounts

Compared to prediction markets and stablecoins, tokenized stocks present a more direct integration direction.

It's not about introducing a crypto product to traditional users, but moving stocks, ETFs, funds, and other traditional assets into accounts primarily designed for storing and trading crypto assets.

Over the past six months, almost all major crypto trading platforms have been rushing in. Meanwhile, ICE, the parent company of the New York Stock Exchange, has made a strategic investment in OKX. The two parties plan to collaborate on US-regulated crypto futures, ICE market products, and tokenized stocks associated with the New York Stock Exchange. As of press time, OKX has just announced plans to launch tokenized US stock products.

From a market structure perspective, this collaboration holds strong symbolic significance. In the past, crypto exchanges tried to provide users with stock price exposure through synthetic assets, perpetual contracts, or third-party issuers. Now, the operators of traditional exchanges are directly participating in product design, price data, compliance, and on-chain market infrastructure construction.

Similar changes are already happening on the user-facing side. Besides vertical applications, from trading platforms to wallets to on-chain DEXs, from Robinhood to Interactive Brokers, everyone is trying to expand into comprehensive financial accounts that can simultaneously handle crypto assets, stocks, and even commodity trading.

However, tokenized stocks are also the most prone to conceptual confusion.

A token with a name containing Apple, Nvidia, or Tesla does not necessarily equate to the user directly holding common stock in the corresponding company. Different products may represent direct ownership of genuine stocks, beneficial interests formed by an SPV holding the stocks, debt instruments promised for redemption by the issuer, or merely derivatives tracking the stock price.

These models can differ significantly in terms of dividends, voting rights, redemption rights, bankruptcy remoteness, and investor protection. Even if the token circulates on a public chain, the legal relationships determining the user's ultimate rights often still exist in off-chain issuers, custodians, and legal contracts. Currently, most RWA systems also adopt a hybrid architecture.

Therefore, tokenization does not automatically equal liquidity, nor does it automatically mean users have the exact same rights as traditional shareholders. But these limitations do not prevent tokenized stocks from becoming an important entry point.

Once issues related to compliance, custody, and shareholder rights are gradually resolved, stocks will no longer be confined to brokerage accounts. They can coexist with stablecoins in the same on-chain account, can be divided into smaller units, can be traded across different regions and time zones, and could further be used for collateral, lending, automated investing, and programmatic asset allocation.

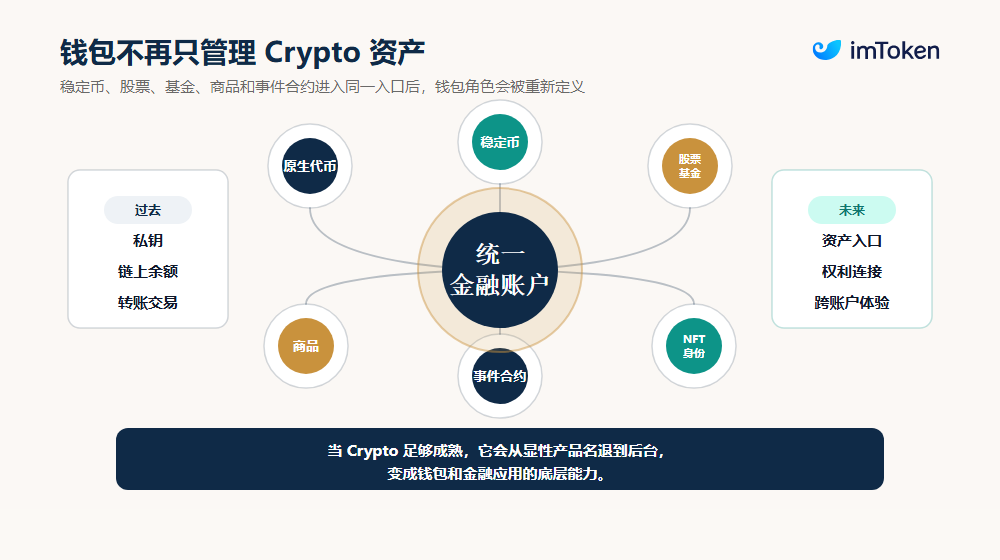

By then, wallets and trading platforms will no longer just compete on storing and trading crypto assets, but on who can become the unified entry point for users to manage global assets.

Final Thoughts

To be honest, this is a bit like the scene in "The Heaven Sword and Dragon Saber" where Zhang Sanfeng teaches Zhang Wuji Tai Chi. He repeatedly asks Zhang Wuji how much he remembers, until Zhang Wuji answers that he has completely forgotten it all – only then is it considered true mastery.

The mainstreaming of crypto might go through a similar process. The true sign of maturity is not that everyone remembers the concepts of blockchain, wallets, and stablecoins, but that users gradually become unaware of the existence of these technologies, allowing Crypto to disappear behind the products.

Of course, upon closer examination, from prediction markets to stablecoins to tokenized stocks, the ways crypto technology enters traditional finance are not the same:

- Prediction markets bring the product logic developed in the crypto world to the mass market, turning events and uncertainty into real-time tradable probabilities.

- Stablecoins embed on-chain settlement capabilities into payments, remittances, and corporate capital flows, allowing users to use a new financial network without understanding blockchain.

- Tokenized stocks bring traditional assets into on-chain accounts, gradually making wallets, exchanges, and public chains new issuance, trading, and settlement channels for traditional securities.

These correspond to penetration at three levels: product, capital, and assets. For the industry, this might signify a new path to mass adoption, one that no longer requires every user to become a Crypto user first, but instead lets on-chain technology actively adapt to the financial needs users are already familiar with.

Accordingly, the role of the wallet will also change.

After all, when a wallet no longer only contains native tokens and NFTs, but gradually includes stablecoins, stocks, funds, commodities, and event contracts, it needs to handle not just private keys and on-chain balances, but also how to lower the barrier to using different assets and better connect on-chain and off-chain account systems.

Imagine when someone can use imToken to instantly send money to overseas relatives, trade the probability of an event happening on imToken, or buy a small portion of US stocks – they may not necessarily think they are "using Crypto."

It is precisely in this state, where it no longer needs to be repeatedly emphasized, that crypto technology can truly move from a relatively independent niche market into the broader financial and commercial world.