Lithography machines are selling like hotcakes; ASML officially announces a 30% capacity expansion

- Core Insight: ASML's Q2 2026 financial results exceeded expectations, with total net sales of €9.326 billion and net profit of €2.918 billion. The company raised its full-year 2026 guidance for the second time this year to a range of €43-45 billion, primarily driven by a surge in chip demand fueled by the AI infrastructure arms race.

- Key Elements:

- Results Beat Expectations: Q2 net sales reached €9.326 billion, and net profit was €2.918 billion, both surpassing analyst forecasts. The gross margin of 54% exceeded the company's own guidance.

- Demand Drivers: Tech giants like Amazon and Google are investing hundreds of billions of dollars in AI infrastructure, accelerating expansion plans for memory and logic fabs. Revenue from memory customers is expected to grow by 75% in 2026.

- Capacity Expansion Plans: ASML plans to increase its EUV and immersion DUV capacity by 30% each in 2027, and is evaluating a further 30% increase in capacity for each technology in 2028.

- Regional Market Shifts: South Korea remains the largest customer (accounting for 43% of revenue), while China's share decreased from 19% to 14%. However, management expects China's full-year share to remain around 20%.

- High-Margin Business Growth: The installed base management and services business contributed €2.762 billion, up 11% quarter-over-quarter. It is expected to achieve over 30% growth in 2026, boosting overall profit margins.

Original author: Su Yang

Original editor: Xu Qingyang

Original source: Tencent Tech

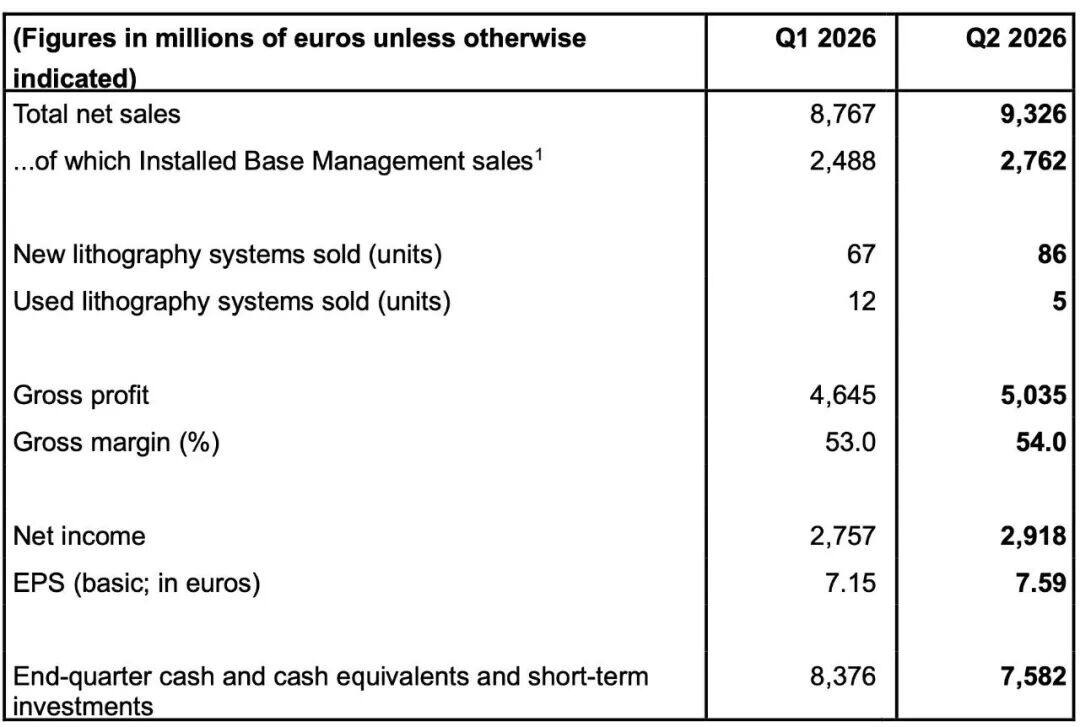

July 15 news, ASML announced its Q2 2026 financial results. Total net sales were €9.326 billion, with net profit of €2.918 billion, both core indicators exceeding Wall Street analyst expectations.

As the most critical lithography equipment manufacturer upstream in wafer fabrication, ASML's surging performance reflects an ongoing arms race across the entire tech industry.

Giants like Amazon, Google, and Microsoft have invested hundreds of billions of dollars in infrastructure, igniting massive downstream demand for high-end AI chips. Fabs, including logic and memory manufacturers, are accelerating capacity expansion, pushing lithography machine demand to a fever pitch.

Alongside its impressive Q2 results, ASML significantly raised its full-year guidance for the second time this year, boosting its 2026 full-year sales forecast sharply to €43 billion - €45 billion (approximately $49.1 billion - $51.4 billion).

Notably, ASML is also driving its own capacity expansion. Based on a 2026 capacity plan of approximately 65 Low NA EUV systems, it plans to increase capacity by 30% in 2027 and is studying a further 30% increase in 2028. Simultaneously, based on a 2026 capacity plan of approximately 130 immersion DUV systems, it plans to increase capacity by 30% in 2027 and is studying another 30% increase in 2028.

Driven by this, ASML has secured its position as Europe's largest listed company by market capitalization. Since the beginning of 2026, ASML's stock price has accumulated a gain of over 68%, doubling over the past 12 months.

Gross Margin Surges to 54%, Revenue Guidance Significantly Raised

ASML Key Financial Data

ASML achieved strong year-over-year and sequential growth across several key financial metrics in Q2, surpassing Wall Street analyst forecasts.

Total net sales for Q2 reached €9.326 billion, growing from €8.767 billion in Q1; a 21.3% year-over-year increase compared to €7.69 billion in the same period last year, significantly exceeding the average analyst estimate of €8.83 billion from Visible Alpha and the consensus estimate of €8.8 billion by LSEG.

By revenue breakdown, of the €9.326 billion total net sales, equipment revenue was €6.564 billion, and installed base management services were €2.762 billion.

Gross profit for the quarter increased to €5.035 billion, with a gross margin reaching 54%, up from 53% in Q1 and exceeding the company's own guidance. In terms of equipment deliveries, ASML sold 86 new lithography systems and 5 used lithography systems in Q2, a significant increase from the 67 new systems sold in Q1.

"Both net sales and gross margin exceeded expectations, primarily due to higher-than-expected revenue from installed base management services," said Christophe Fouquet, President and CEO of ASML.

Net profit performance was also outstanding. Net profit for the quarter reached €2.918 billion, a steady increase from €2.757 billion in Q1; a 27.5% year-over-year surge compared to €2.29 billion in the same period last year, significantly surpassing the market consensus estimate of €2.6 billion.

Driven by extremely strong order momentum in the first half of the year, ASML made the year's most aggressive forecast revision. The company sharply raised its 2026 full-year total net sales forecast from the €36 billion - €40 billion range provided last quarter to €43 billion - €45 billion; concurrently, it raised its full-year gross margin forecast from 51%-53% to 54%-56%.

Such a magnitude of adjustment is extremely rare in the semiconductor equipment industry, directly reflecting the urgency of downstream customers to pull in shipments. For the upcoming third quarter, ASML provided a highly optimistic outlook, forecasting single-quarter sales between €11 billion and €12 billion, with gross margin expected to climb further to 55%-57%.

Memory and Logic Fabs Scramble for Tools

ASML Business Breakdown

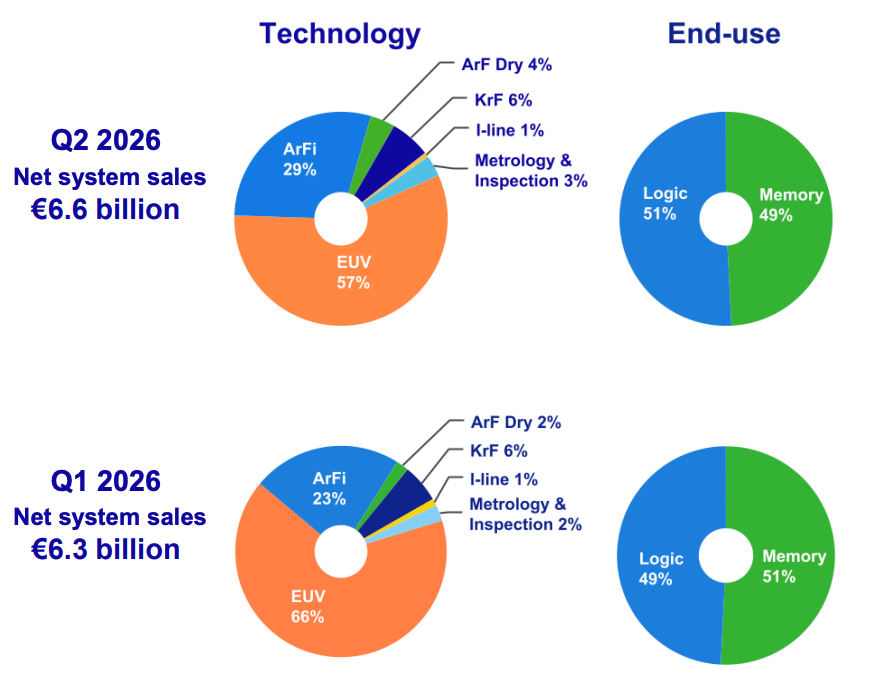

In the net system sales structure for Q2 2026, logic chips regained dominance, accounting for 51% of revenue versus 49% for memory chips. In the previous quarter, memory customer orders had historically surpassed logic customers at 51%.

From a technology structure perspective, although EUV systems revenue contribution moderated to 57% from 66% in Q1, it remains ASML's primary revenue pillar. In terms of shipments, ASML sold 16 EUV systems in Q2, flat compared to Q1.

In contrast, ArFi (immersion deep ultraviolet lithography) systems saw a rebound in Q2, with revenue contribution increasing from 23% in Q1 to 29%, and unit sales rising from 17 units in Q1 to 23 units, indicating restocking demand by fabs for DUV equipment.

South Korea Remains the "Largest Customer"

Influenced by a combination of export controls and a global wave of fab construction, ASML's global shipment destinations saw notable shifts in Q2.

For the second consecutive quarter, South Korea was the single largest market region, contributing 43% to ASML's revenue this quarter. This indicates that memory giants like Samsung Electronics and SK Hynix are maintaining extremely high levels of equipment procurement investment intensity domestically.

Meanwhile, the Taiwan market saw a strong rebound, with its revenue contribution jumping significantly from 23% in Q1 to 30%. In contrast, the China mainland market's revenue contribution fell back to 14% in Q2 from 19% in Q1. However, management expects the China mainland's contribution to full-year total revenue to remain around 20%.

"Incremental demand from the China mainland market primarily comes from the logic chip sector, driven by local demand," said Roger Dassen. Because ASML raised its full-year overall revenue base in Q2, maintaining the same percentage means the absolute procurement volume from the China mainland market actually increased correspondingly with the overall growth.

Since ASML raised its full-year overall revenue guidance in Q2, the absolute procurement value from the China mainland market for the full year is actually steadily increasing.

Among other regions, the U.S. market contributed 9% of revenue this quarter, compared to 12% in the previous quarter; Japan's market share was 4%.

EUV and DUV Lithography Capacity to Increase by 30%

In a video interview following the earnings release, ASML CEO Christophe Fouquet and CFO Roger Dassen provided an in-depth analysis of the underlying industry logic and regional market trends behind the performance.

Fouquet stated that due to continued supply constraints for DDR5 and HBM (High Bandwidth Memory), driving prices higher, major manufacturers are accelerating capacity expansion across the board. Furthermore, the most advanced memory nodes require significantly higher lithography intensity (including Low NA EUV and advanced immersion tools). This leads ASML to expect a massive 75% jump in revenue from memory customers in 2026.

At the same time, Fouquet emphasized that driven by AI demand, key customers are pushing for advanced process capacity expansion. Logic chips are performing strongly as well, with revenue from advanced foundry logic business expected to grow by about 25% in 2026.

Facing unprecedented pull pressure, Fouquet revealed that ASML plans to ship approximately 65 Low NA EUV systems in 2026, driving a 45% growth in full-year EUV business revenue; simultaneously, immersion system shipments are expected to reach 130 units.

"We plan to increase EUV capacity by 30% in 2027 compared to 2026. Looking ahead to 2028, we have already received a large volume of EUV orders from customers, prompting us to seriously evaluate the possibility of increasing EUV capacity by another 30% in 2028. Along with the growth in EUV orders, DUV is also growing, with immersion DUV continuing to play a vital role. We plan to increase its capacity by 30% in 2027 and are evaluating a further 30% increase in 2028," Fouquet said.

Regarding the standout performance of Installed Base Management services (mainly after-sales service and hardware/software field upgrades) this quarter, CFO Roger Dassen emphasized this is an incremental segment not fully appreciated by the market. This business generated €2.762 billion in revenue in Q2, achieving 11% sequential growth, a full €300 million higher than the company's previous expectations.

Dassen explained that in the current industry environment of extremely tight capacity, customers are accelerating the purchase of ASML's upgrade solutions to maximize production line efficiency in the shortest possible time.

Since many upgrades are software-driven and do not require equipment downtime or significant machine modification time, customers can immediately gain productivity improvements after installation. As the installed base of EUV systems continues to expand, the scale of corresponding Installed Base Management services is also growing. This high-margin business is expected to achieve over 30% growth in 2026, becoming a key contributor to boosting the company's overall profitability.