苹果与「美光们」的权力再平衡:拆解iPhone背后的利润账单

- 核心观点:苹果iPhone的利润结构中,苹果本身占据主导(约25%净利润率),而内存等关键组件供应商长期以来利润微薄(<3%)。随着AI需求驱动内存价格暴涨,供需关系逆转,内存厂商开始掌握话语权,迫使苹果等终端企业面临成本压力并提价。

- 关键要素:

- iPhone利润分配失衡:苹果净利率常年在24%以上,占行业总利润约75%;而美光等内存厂商仅获取约3%的利润,台积电约为4%-5%。

- 内存成本从“边角料”变为“关键部件”:从2017年iPhone X的2%成本占比,升至2026年iPhone 17系列的12%-15%(约60-80美元),成本翻了近8倍。

- AI需求是涨价核心推手:AI服务器对DRAM需求是普通服务器的8倍,迫使三星、SK海力士等厂商将产能转向高利润HBM,导致消费级内存供应短缺。

- 库克与马斯克罕见表态:库克将内存涨价称为“40年未见”的冲击,苹果随后全线涨价;马斯克也公开表示这是“见过的最猛的价格跳涨”。

- 内存厂商盈利能力剧增:美光Q3财报毛利率达84.6%,营收同比增长346%。宏观数据上,2026年一季度DRAM合约价季增93%-98%,全年均价预计涨88%。

Original|Odaily Planet Daily (@OdailyChina)

Author|Wenser (@wenser2010 )

Have you ever wondered how much of the profit from selling an iPhone goes to each component supplier?

Recently, overseas tech blogger @BluthCapital, speaking in the tone of Micron's CEO, joked about the "business model" behind the iPhone: "For over a decade, Apple has been buying chips from us (MU) for $5, putting them in a metal box, and selling them to consumers for $99. When we tried to raise the price to $7, they went into mock mode. But now, when we charge them $50, they raise the product price by $250." The tone suggests a strong disdain for Apple's recent price hikes while blaming memory manufacturers.

The post quickly sparked discussions on social media. This morning, @BluthCapital continued the topic, sharing an iPhone 18 cost structure chart with specific figures to support his argument:

Previously, Micron's Chief Business Officer Sumit Sadana also stated in an interview with The Wall Street Journal, "During the memory industry downturn, some customers took advantage of the situation to drive down prices, resulting in negative profits for the company." Now, due to strong demand from the AI and tech industries, the memory sector has become the party with the upper hand. This has led to a dramatic shift in the entire supply chain.

Profit Structure of an iPhone: Apple Takes Nearly 25%, Memory Manufacturers Like Micron Get Less Than 3%

According to estimates, for each iPhone sold, Apple takes about a quarter of the profit, memory giants get only about one-thirtieth, TSMC, due to its monopoly, takes about 4%-5% of the profit, and the rest is covered by other hardware suppliers, distribution channels, R&D, and taxes.

Looking Back at Apple's Financial Reports: Net Profit Margin Consistently Above 24%, Capturing 75% of Total Industry Profits

According to data from agencies like Counterpoint, Apple has long held nearly 50% of the global smartphone market's operating profit. IDC data for 2025 shows that with an 18% market share, it captured about 75% of the total industry profits.

Based on Apple's latest Q2 2026 data, iPhone revenue was $57 billion, net profit was $34 billion, and estimated shipments were about 61 million units. From this, it can be calculated that Apple's net profit per iPhone is about $320-$340, with a net profit margin of 33%-36%.

Looking at the comparison of financial data over the past 5 years, we can clearly see that iPhone revenue has been relatively stable. Net profit has gradually increased from about $94 billion in 2021 to about $112 billion in 2025. The net profit margin has remained relatively stable, typically around 25%.

Looking at different models like the 2017 iPhone X, the 2023 iPhone 14 Pro, and the 2026 iPhone 17 series, the profit structure has changed due to varying memory costs.

From iPhone X to iPhone 17: Memory Costs Have Doubled

The role of memory costs in the iPhone has gone through three historical stages: from the initial "leftover material," to an "important component," and now to a "critical component."

2017 iPhone X Era: The "Leftover Material" Period

According to the teardown report data from Counterpoint at the time, during the iPhone X era, thanks to its long-standing brand advantage and upstream ecosystem position, Apple's net profit margin once approached 50%. In contrast, the profit share for memory manufacturers like Samsung and SK Hynix from South Korea was only about 135–195 RMB, accounting for approximately 1.6%–2.3% of the total selling price of 8,388 RMB.

This was the "weight" of memory in the iPhone X era: about 2% of the cost, almost the least of Apple's concerns among components.

2023 iPhone 14 Pro Era: The "Important Component" Period

In 2023, the iPhone 14 series launched. Apple's material costs increased slightly. For the Pro model, the BOM (Bill of Materials) cost reached about $464 (approximately 3,170 RMB), accounting for nearly 40% of the selling price. However, Apple's net profit margin still remained around 40%.

According to tech media reports at the time, the above data pertained only to the 128GB version. The cost increase for higher memory versions was not significant, but the selling price was considerably higher. This was a period of "camera and processor price increases," so the overall profit for the iPhone 14 Pro was 3.7% lower than that of the iPhone 13 Pro.

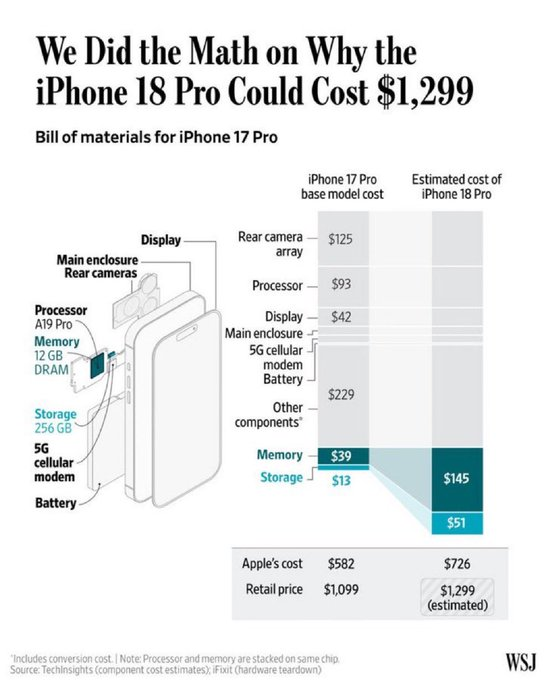

2026 iPhone 17 Era: The "Critical Component" Period

Fast forward to 2025-2026, the iPhone 17 series becomes Apple's main model, and memory costs have doubled compared to a few years ago. It is currently estimated that memory costs now account for 12%-15% of the BOM cost, approximately $60-$80.

In summary, the following table shows the cost and memory cost share data for different eras of the iPhone.

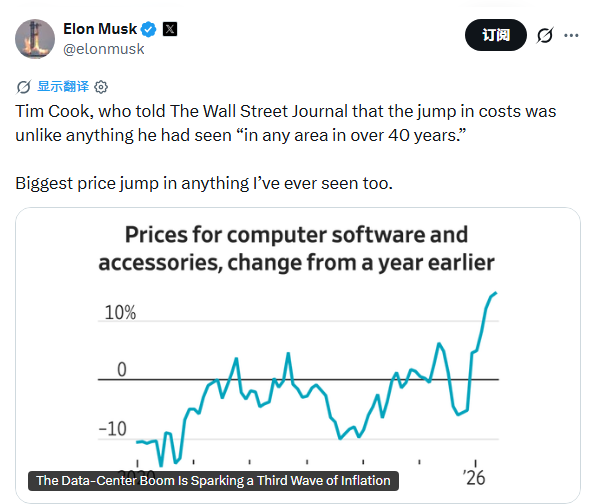

It is worth noting that TrendForce data shows that in the first quarter of 2026, contract prices for general-purpose DRAM increased by a staggering 93% to 98% quarter-on-quarter. Citigroup estimates that the average DRAM price for the full year 2026 will increase by 88%. This aligns with the overall trend of rising memory costs. This phenomenon has also been acknowledged by Apple CEO Tim Cook and Elon Musk.

Cook: Memory Price Hike, a Once-in-40-Years Event

On June 17, Apple CEO Tim Cook (Note from Odaily Planet Daily: He will step down as CEO this September and be succeeded by John Ternus, Senior Vice President of Hardware Engineering) mentioned the cost pressure from memory price increases in an interview with The Wall Street Journal. He said: "Supply is decreasing precisely when consumers need devices, and memory manufacturers are passing on huge price increase pressure. We absolutely need memory pricing and supply to return to a reasonable level for consumer products. This is the bottom line."

However, less than a week later, he quickly changed his tune.

On June 25, Cook spoke again with The Wall Street Journal, referring to the cost impact issue as a "once-in-a-century flood." He said: "In over 40 years, I have never seen anything like this in any field." Shortly after, Apple announced price increases across its product lines, including Mac, iPad, HomePod, Apple TV, and Vision Pro.

Upon the announcement, Apple's stock price fell 6%, erasing $263 billion in market value, marking its largest single-day decline since April 2025.

Musk: I Haven't Seen This Either

Cook's comments also resonated strongly with Elon Musk. Recently, he also posted: "Cook told the Wall Street Journal that this cost surge is something he 'has never seen in any field in over 40 years.' Me neither. This is the most brutal price jump I've ever witnessed."

Thanks to AI Data Centers and HBM, Memory Has Teeth Now

Looking closely at the "memory bull market" that started last year, the key driving force is the strong demand from the AI industry.

The industry generally estimates that each AI server requires 8 times the DRAM and 3 times the NAND flash memory compared to a standard server.

Based on this market demand, the three major memory manufacturers—Samsung, SK Hynix, and Micron—will naturally shift more advanced process capacity to high-margin HBM (High Bandwidth Memory) and high-end DDR5 products, proactively cutting back on consumer-grade production lines like DDR4, leading to a shortage of general-purpose DRAM.

Public information shows that the DRAM capacity per AI server is 8 to 10 times that of a traditional server. Combined with replenishment needs for general-purpose servers and the proliferation of AI PCs, the supply-demand gap for memory chips continues to widen.

Previously, Micron's stunning Q3 gross margin of 84.6% and its revenue scale of $414.6 billion, a 346% year-over-year increase, demonstrated the immense profit-generating power of monopolistic memory manufacturers. On the other side, SK Hynix recently announced plans for a U.S. listing, seeking to raise approximately $29 billion to further capitalize on memory demand.

It is no exaggeration to say that memory demand from the AI industry is squeezing and even consuming the memory supply for consumer electronics. According to statistics, the memory used in a single NVIDIA Vera Rubin AI server is equivalent to about 14,500 MacBook Neo units. The 1:14,500 ratio vividly illustrates the severe supply-demand imbalance in the memory market.

For memory manufacturers, who previously suffered from price suppression by giants like Apple, this is their moment. It's no wonder that there were reports that Apple is actively lobbying the Trump administration for approval to purchase memory chips from Chinese chip company ChangXin Memory Technologies (CXMT).

As for whether CXMT can replicate the wealth-creation miracles of star companies like SK Hynix and Micron in the capital markets, the answer may be revealed next month.

Related Reading

Super explosive spiral, Micron's earnings reignite the semiconductor bull run