空降賽道第三,Rothera正攪亂預測市場格局

- 核心觀點:Robinhood自建預測市場Rothera上線僅半月即空降行業第三,單週交易量達5.59億美元,其崛起本質是透過截流原屬於合作方Kalshi的存量訂單,強化自身價值捕獲能力,並可能顛覆預測市場現有競爭格局。

- 關鍵要素:

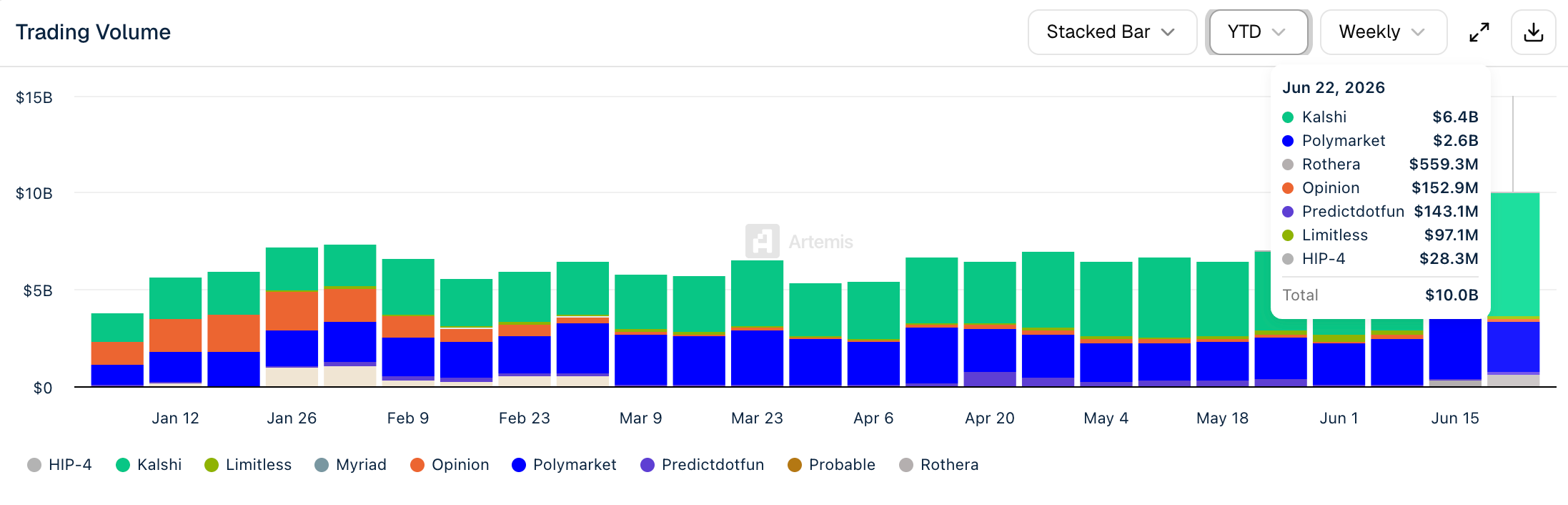

- Rothera上線三週內,週交易量從2190萬美元飆升至5.59億美元,僅次於Kalshi和Polymarket,增長迅速。

- Rothera的增長主要源於將原透過Robinhood渠道流向Kalshi的訂單轉移至自身平台,這是一場存量遷移而非增量用戶創造。

- Robinhood曾為Kalshi貢獻約25%-35%的交易量,現透過自有平台直接截流,減少與Kalshi的收入分成。

- Hood House估算,Robinhood預測市場業務單日收入約490萬美元,有望今年實現10億美元級別收入,超越其加密貨幣收入歷史峰值。

- Kalshi為應對競爭,正與投行接觸尋求IPO,並藉此要求投行對接其系統,以開拓銀行、券商等新分發渠道。

Original: Odaily Planet Daily (@OdailyChina)

Author: Azuma (@azuma_eth)

Last week, Odaily Planet Daily published an article titled "The First Stock in the Prediction Market Has Arrived!", which mainly discussed how Robinhood is intercepting orders that once required Kalshi to execute by building its own prediction market, Rothera. This allows Robinhood to reduce revenue sharing with Kalshi and keep profits within its own system.

Although we had anticipated that Rothera wouldn't face the cold-start problem common among other competitors, the platform's data performance over the past week has still far exceeded our previous expectations. After all, it's hard to imagine a platform that has only been online for two weeks suddenly breaking into the top three of this extremely competitive prediction market, behind only the two giants, Kalshi and Polymarket.

Artemis data shows that in the week ending June 8, Rothera, as a new platform, had a weekly trading volume of just $21.9 million, still significantly lagging behind second-tier platforms like Opinion, Predict, and Limitless. However, in the week ending June 15, Rothera's weekly trading volume directly jumped to third place in the industry, reaching $276 million. In the latest week ending June 22, Rothera's weekly trading volume increased to $559 million, nearly reaching one-fifth of Polymarket's volume.

An Atypical Growth Story (Readers of the previous article can skip this)

It's important to clarify: Rothera's rise is essentially not about creating new users (though some users may have joined due to the World Cup), but rather a migration of existing orders, not the creation of new users.

Over the past year, Robinhood has been one of Kalshi's most important distribution channels. Leveraging tens of millions of retail users and mature trading interfaces for stocks, options, and cryptocurrencies, Robinhood has funneled a large number of orders to Kalshi. Analysts at Piper Sandler estimated that trading volume executed through the Robinhood channel accounted for approximately 25%-35% of Kalshi's total trading volume.

The issue is that while these orders come from Robinhood users, they don't belong to Robinhood. Under the previous cooperation model, Robinhood acted more as a front-end traffic gateway, while Kalshi was the infrastructure provider responsible for matching, clearing, and settlement. Revenue generated from each transaction had to be split between the two parties.

Rothera is the weapon Robinhood uses to break this revenue-sharing model. Since the beginning of this month, Robinhood has started migrating some World Cup-related event contracts for execution on Rothera. This means a significant volume of orders that would have previously flowed to Kalshi now remains within Robinhood's own ecosystem.

Therefore, in a sense, the surge in Rothera's trading volume isn't so much a threat to other prediction markets like Polymarket, Predict, or Limitless, but rather a direct "drain" on Kalshi.

Robinhood's Value Capture

The most immediate impact of Rothera's rapid growth is the strengthening of Robinhood's ability to capture value from prediction market orders on its platform.

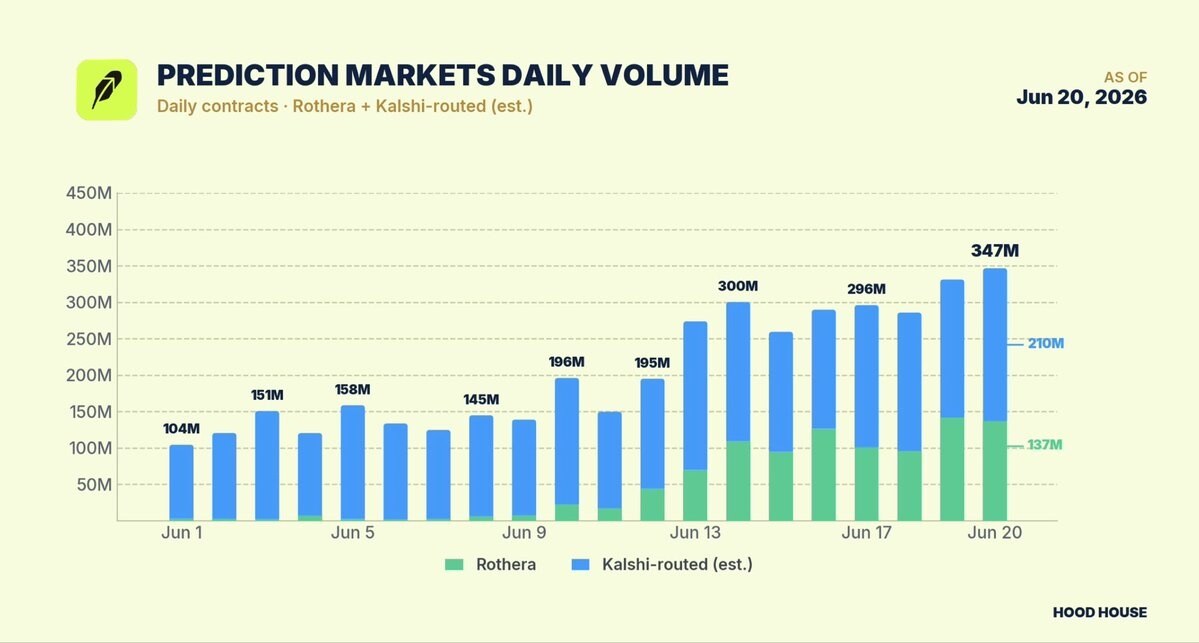

Hood House, a research and analysis自媒体 that has long tracked Robinhood, combined public data estimates that as of June 20, Robinhood's prediction market business executed a total of 34,700 contracts in a single day, corresponding to a daily revenue of approximately $4.9 million.

Hood House subsequently disclosed its statistical logic:

- Rothera (primarily hosting World Cup-related markets) had a daily trading volume of 137 million contracts, corresponding to a trading volume of approximately $47 million.

- In comparison, Kalshi's total daily trading volume was approximately 1.5 billion contracts, corresponding to a trading volume of about $416 million. Excluding World Cup-related markets, Kalshi's trading volume was about 1 billion contracts, corresponding to a trading volume of around $260 million.

- Considering that trading volume contributed by Robinhood users still accounts for roughly 20% of Kalshi's non-World Cup market volume (a conservative estimate), this means that of Kalshi's non-World Cup event contract volume, approximately 210 million contracts and $52 million in trading volume are executed through Robinhood.

Based on this, Hood House made a further aggressive estimate: If this growth rate continues, Robinhood's prediction market business has the potential to achieve an annual revenue scale of $1 billion this year. This figure even exceeds Robinhood's historical peak in cryptocurrency-related revenue, which was approximately $900 million in 2025.

Kalshi's Counterstrategy: Finding New Channels

Facing Rothera's rapid rise, Kalshi is clearly aware of the problem.

For Kalshi, Robinhood was both a partner and one of its most important traffic sources. However, as Robinhood begins migrating more and more orders to its own platform, the two have become direct competitors.

A recent report from The Information might reveal Kalshi's counterstrategy. Sources familiar with the matter revealed that Kalshi has begun contacting several investment banks for early, informal discussions regarding a potential future IPO. More notably, Kalshi has made a clear demand in these communications: if these institutions want to qualify for underwriting the future IPO, they need to prioritize completing technical integration with Kalshi's system so that their institutional clients can directly participate in trading event contracts on Kalshi's platform.

In other words, Kalshi is leveraging the IPO opportunity to find new distribution channels, integrating prediction markets into the customer networks of banks, brokerages, and other financial institutions. This might also signal a subtle shift in the competitive landscape of the prediction market industry. In the past, the market focused on who could offer more contracts and who could design better products. Now, as prediction markets gradually move into the mainstream financial system, the competitive focus is shifting to another dimension: whoever controls the user gateway can more effectively control the value.

Rothera's rise has already proven the significance of distribution capabilities. Breaking into the top three seemingly effortlessly, whether it can challenge Kalshi and Polymarket in the future doesn't seem like a difficult question.