Bitget CEO Gracy:AI 倒逼 Crypto 去泡沫化,交易所進入全資產競爭

- 核心觀點:Bitget 正在推進 UEX(全景交易所)戰略,透過其自研 RWA 協議 Reality 實現美股代幣化,旨在解決傳統股票代幣流動性差和分紅機制不透明的問題,從而提升用戶資金效率,將 Crypto 作為底層金融基礎設施擴展至傳統資產市場。

- 關鍵要素:

- Reality 透過直接對接美國持牌經紀商 Alpaca,使訂單能直通納斯達克和紐交所,流動性對標傳統券商,解決了價格脫節問題。

- Reality 代幣(rToken)支援 1:1 拆股同步和現金股息自動兌換為 USDT 空投,彌補了行業在分紅和拆股處理上的不足。

- 用戶可將美股代幣(如 rNVDA)作為合約保證金在 Bitget 交易 BTC/ETH,或透過 Arbitrum 等公鏈轉入 DeFi 場景,盤活資產利用率。

- Reality 的底層資產由 Alpaca 託管於獨立 SPV,實現 1:1 全額儲備,並接受第三方美國持牌機構每日審計,官網已上線即時審計看板。

- 數據顯示,非加密貨幣交易已佔 Bitget 總交易量的 40%,美股永續合約累計交易量突破 100 億美元(全球第二),反映用戶從 Crypto 向傳統資產遷移的趨勢。

- Bitget 內部全面推行 AI 使用,已為全體 2167 名員工訂閱企業版 Claude,鼓勵透過 AI 工具提升生產力,並開發了如 GetAgent 等交易輔助 AI 產品。

Throughout June, major exchanges have been intensively rolling out US stock products. As the earliest and most aggressive player in this track, Bitget has also launched its own RWA platform, Reality, and made significant upgrades to its US stock products. Today, we've invited Bitget CEO Gracy to discuss this trend and other hot topics in the industry.

Bitget previously integrated stock token solutions like Ondo. What is the biggest difference between that and the current switch to Reality for US Stocks 2.0? What key issues is this upgrade mainly intended to solve?

Gracy: We started collaborating with Ondo in the third quarter of last year, at one point accounting for nearly 90% of their stock token market share. We’ve also worked with xStocks to list US stock tokens. But throughout this process, the most common feedback we heard from users was: liquidity isn't good enough, and the settlement mechanism for dividends and stock splits isn't clear or transparent enough.

So, we decided to step in and solve this ourselves. Reality is the compliant RWA protocol we launched. Its biggest difference lies in directly connecting with the US licensed broker Alpaca, allowing orders to go straight to NASDAQ and the NYSE. Simply put, when trading Reality's US stock rToken, users get the exact price of Apple or Tesla on the US stock market, with liquidity directly benchmarked against traditional brokers.

Furthermore, Reality solves the pain points of dividends and stock splits. Cash dividends are automatically converted to USDT and airdropped to users. Stock splits are also synchronized 1:1, eliminating the disconnect between token prices and actual stock prices.

Will users be able to use rTokens of stocks like Nvidia and Tesla as margin to trade BTC, ETH, or other futures contracts in the future?

Gracy: This feature was already launched on June 4th. This is also the core reason we insist on tokenization, rather than just offering "direct broker connections." The rNVDA (Nvidia rToken) users purchase can be used directly as futures margin on Bitget, or transferred out to DeFi scenarios via public chains like Arbitrum and Morph. Our goal is to truly activate the US stock tokens our users hold, enhancing overall capital efficiency.

Recently, many exchanges have been upgrading their US stock-related products. Compared to stock products on other platforms, what are the core differences in Bitget's latest upgrade?

Gracy: Indeed, many platforms are entering the US stock space lately. But looking around, most competitors are still stuck on the "direct broker connection" model. That means users deposit stablecoins, open an account with a traditional broker, and trade there. Bitget recently launched US Stocks 2.0. A key upgrade point is our choice of a more crypto-native path: RWA stock tokens.

The core difference is that stocks bought through a "direct broker connection" usually just sit in the user's US stock account. But on Bitget, the rTokens issued via Reality are real on-chain assets, currently integrated with Arbitrum and Morph public chains. This means users can not only use them as margin within Bitget but also withdraw them to their own wallets. In the future, they could even be used in DeFi protocols for staking, generating yields, etc.

We've specifically solved two long-standing industry problems. First, liquidity: our orders go directly to NASDAQ and the NYSE, synchronizing prices, order books, and depth with the real market. Second, dividend distribution and stock splits: cash dividends are directly converted to USDT and automatically airdropped; stock splits are also synchronized 1:1, preventing the token price from disconnecting from the actual stock price.

More importantly, within the UEX environment, these rTokens can truly realize higher capital efficiency. For example, a user holding rNVDA (Nvidia rToken) can use it directly as margin to continue trading BTC or ETH futures, allowing the same asset to function in two markets simultaneously. This is a truly native on-chain experience, something a direct broker connection cannot achieve.

A long-standing criticism of stock tokens is: Are users buying a tokenized representation of real stock equity, or just a price tracking tool? How will Reality prove to users that the underlying stocks truly exist, are auditable, and traceable? Will it offer things like proof of reserves, custodian disclosures, audit reports, or broker structure explanations in the future?

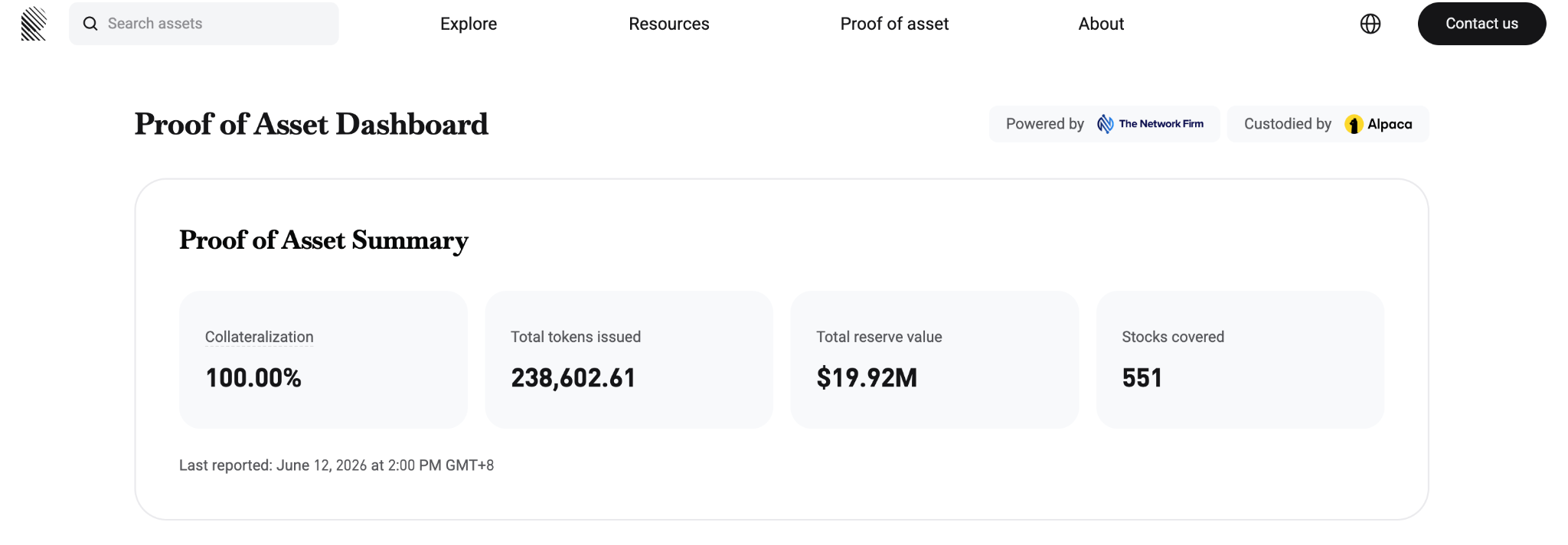

Gracy: That's an excellent question. Indeed, if it's just a "synthetic asset" tracking a price, it has no soul. Reality's rTokens are backed by actual underlying assets. Our underlying stocks are custodied by the US licensed broker Alpaca and held in a separate SPV, completely isolated from the platform's proprietary assets. We achieve 1:1 full reserve backing.

Simultaneously, we undergo daily audits by a third-party US licensed auditing firm. The Reality official website already features a live audit dashboard where users can check the reserve ratio anytime. We expect to add the CPA licensed audit firm's reports to this dashboard around August once they're ready. Combined with Bitget's User Protection Fund of over $300 million, this forms a triple layer of protection.

(Source: Reality PoR Dashboard Screenshot, June 12, 2026, 2:00 PM GMT+8)

If a stock undergoes a stock split, reverse split, special dividend, merger, acquisition, or delisting in the future, how will Reality handle it?

Gracy: Handling Corporate Actions is another area where we are stronger than many products on the market. Take stock splits, for example. Last year, when Netflix had a 1-for-10 split, some platforms' tokens didn't rebase synchronously, causing certain stock token prices to diverge tenfold from the actual stock price, confusing users. But with Reality, stock splits are synchronized automatically. A user holding 1 token ends up with 10, with the unit price matching the real stock price, leaving the total asset value unaffected.

Cash dividends are also directly converted to USDT and automatically airdropped to the user's Bitget account, ensuring clarity and transparency. Whether for individual retail investors or institutions we support later, especially those needing to hedge, value, liquidate, and manage portfolios, this structure where "price is price, dividend is dividend" aligns much more closely with traditional financial system practices.

In the past few years, the main narratives for crypto users have been BTC, ETH, DeFi, NFTs, Meme coins, L2s, and public chain competition. But recently, it's clear that assets and companies like AI, US stocks, Nvidia, OpenAI, and SpaceX are attracting massive amounts of capital and attention.

Have you observed this migration in your platform data? What is the current share of non-crypto trading on Bitget? How fast is it growing?

Gracy: We have indeed observed this trend. As early as late 2024 and early 2025, we noticed altcoins performing weakly, while user enthusiasm for assets like AI, US stocks, gold, and silver began to rise. This is why I proposed the vision of UEX (Universal Exchange) back in September last year.

In December last year, the cumulative trading volume of our US stock perpetual futures surpassed $10 billion, ranking second globally. Earlier this year, the daily trading volume of our TradFi sector, including gold and forex, also exceeded $2 billion for the first time. Currently, 40% of Bitget's trading volume comes from non-crypto assets.

The reason is simple: capital is profit-seeking. Where there is more certain growth and wealth effects, capital flows. US AI giants deliver tangible revenue and profits, while many crypto projects are still in the storytelling phase.

As for whether this will reverse, I don't believe it's a zero-sum game. Crypto assets, like BTC as digital gold, and US tech stocks can completely be complementary components in a user's investment portfolio. What we need to do is allow users to smoothly buy different asset classes within a single account using stablecoins like USDT and USDC.

Looking at the macro environment, US stocks, especially AI-related assets, have seen significant gains over the past six months, with many appreciating tenfold. For many crypto users, they might only start paying attention to US stocks after the diminishing profit effect in the crypto market. Entering at this point, they might actually face the risk of buying high.

What is your take on the current position of the US stock market? What is the biggest mistake users transitioning from crypto to US stock trading need to avoid?

Gracy: The biggest pain points for crypto users are capital efficiency and asset fragmentation. Leaving capital on an exchange to earn interest might mean missing out on stock market gains. Opening a traditional brokerage account makes it difficult to get funds back to the exchange for futures trading. Our rToken product is designed to solve this: while users buy US stocks, their holdings can still be used as futures margin, keeping the capital active the whole time.

Whether US stocks are expensive depends on the user's investment timeframe. Crypto users engaging with US stocks must first realize that the US stock market, like crypto, doesn't only go up. Especially hot areas like AI, semiconductors, and tech stocks have already seen significant gains recently. Short-term volatility and valuation pressures need comprehensive assessment.

Stepping outside my CEO role, as an investor managing my personal account, I recently shared some judgments on Twitter about Bitcoin's potential cycle bottom in this cycle. I faced criticism from some netizens: "As an exchange CEO, you shouldn't be bearish on your own industry." But I want to say, every industry has its cycles. I simply laid out the data and logic, pointing out potential cyclical changes. We are, of course, long-term bullish on the crypto industry and believe tokenized assets will bring new opportunities. However, being "long-term bullish" doesn't mean "always be bullish." Trading opportunities arise from volatility. For increasingly mature investors, both ups and downs can be opportunities.

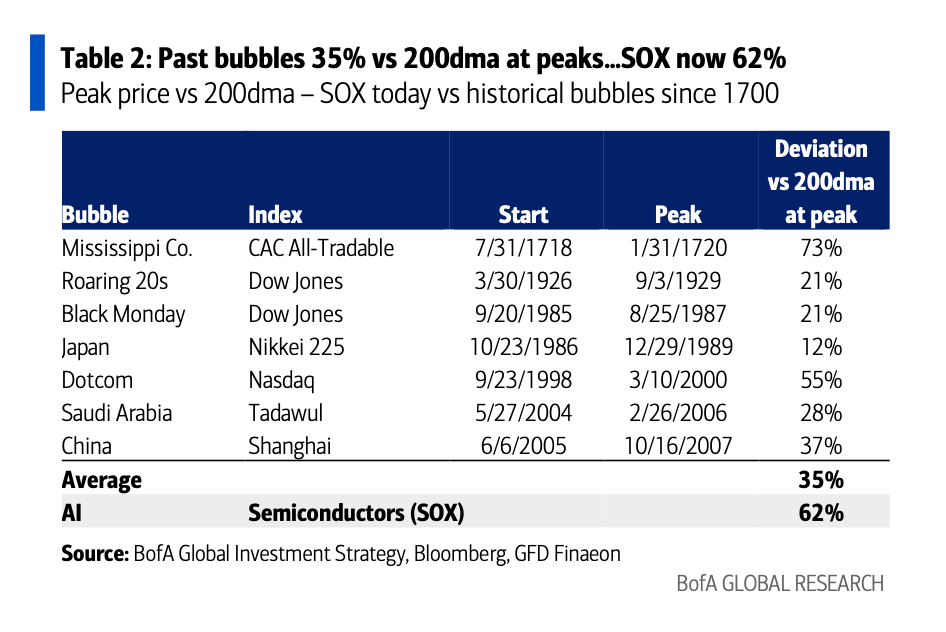

Technically speaking, there are some extreme deviations in the current market. A Bank of America (BofA) report and related charts show that the Semiconductor Index (SOX) has risen 62% above its 200-day moving average. Historically, during the peaks of major market bubbles, the average deviation of relevant indices from the 200-day moving average was about 35%. The current deviation has already exceeded the 55% level by which the NASDAQ Index was above its 200-day moving average before the dot-com bubble burst in 2000.

(Source: BofA The Flow Show Report, May 14, 2026, 10:45 PM EDT)

Additionally, the current US stock market rally is heavily reliant on a few tech giants. If mega IPO projects like SpaceX or Anthropic go public, they could further divert market liquidity.

Crypto users are accustomed to high volatility, high leverage, and short-term trading. Although US stocks also have volatility, they fundamentally place more emphasis on fundamentals, earnings, valuations, interest rates, and macro cycles. What trading habits do you think they need to change the most?

Gracy: For users transitioning from crypto to US stocks, my most important advice is: Don't trade US stocks like Meme coins. In the crypto space, users might be used to following sentiment, community hype, and using high leverage for short-term trades. But the US stock market is a highly institutionalized market that values financial reports, EPS (Earnings Per Share), interest rate environments, and macro cycles.

Users accustomed to the crypto market need to learn to closely monitor Treasury yields and inflation data. For example, when the 10-year US Treasury yield approaches 5%, it can pressure high-valuation tech stocks.

Furthermore, users moving from crypto to US stocks need to change another trading habit: reduce leverage and lengthen their investment horizon. Blue-chip US stocks have real earnings, cash flow, and business moats behind them. They are more suitable for asset allocation and long-term dollar-cost averaging, rather than going all-in today expecting a double tomorrow, like trading a "shitcoin." Be patient and be a friend of time. To help crypto users adapt better to the US stock market rhythm, Bitget will continue to launch US stock-related educational content. Welcome everyone to follow along and learn to become "distinguished US stock traders."

In the past, crypto was one of the most concentrated areas for young talent, venture capital, tech narratives, and speculative money. But now, AI has clearly become a stronger main theme: top talent goes to AI, VCs invest in AI, secondary market funds chase AI, and US tech giants deliver real revenue and growth.

How significant do you think AI's impact is on crypto? How is AI used internally at Bitget? Is it mandatory or part of performance reviews? Which AI products do you use?

Gracy: The impact is definitely there, but I prefer to see it as a touchstone for the "de-bubbling" of the crypto industry. In the past, making money in crypto was too easy. Now, AI siphoning away capital and talent will force the crypto industry to settle down and find truly valuable real-world applications, like stablecoin payments and RWAs.

Internally at Bitget, we require all employees to fully embrace AI. AI-driven innovation is one of our three core strategies for 2026. We don't rigidly make AI usage a mandatory performance metric, because if a tool is useful, people naturally use it. For instance, I frequently use tools like Manus and NotebookLM to summarize materials – it's quite addictive.

At the same time, we provide organizational support for employees to use AI. Bitget has purchased enterprise-level access to Claude for all its 2,167 employees, costing $200 per person per month. This isn't because of external requirements, but because we observed employees using AI tools and saw real productivity gains, so we want to ensure our team doesn't fall behind in the AI application wave.

Even our design team, which may not have a strong technical background, has learned to use tools like Google AI Studio and developed 6 or 7 AI tools to assist business operations, such as automatically auditing UI compliance in external materials. On the product side, we've also launched AI tools specifically designed for traders, like GetAgent and GetClaw.

We hold AI-related training almost daily. Just this week, I attended a "Data Team AI Product Special Sharing Session" and a "Digital Employee Plan and BG Agent Platform Introduction Sharing Session."

AI is a productivity lever. Those who use it well will run faster in the next cycle. The present and future are undoubtedly an era where silicon-based and carbon-based life work together.

More and more crypto exchanges are now offering US stocks, gold, forex, stock tokens, and Pre-IPO products. Optimistically, this is crypto infrastructure expanding into global assets. Pessimistically, it might mean crypto itself lacks quality native assets, forcing exchanges to bring in US stocks to maintain growth.

How do you see this issue? When crypto exchanges start offering US stocks, does it enhance the value of crypto as financial infrastructure, or does it simply channel crypto user traffic towards traditional finance, ultimately becoming an outsourced market for US stock liquidity?

Gracy: I don't see this as a black-and-white issue. On the surface, crypto exchanges integrating US stocks, gold, forex, and Pre-IPO products looks like "bringing traditional financial assets into Crypto." But on a deeper level, it's actually testing a question: Is Crypto just an asset class, or is it a new set of financial infrastructure?

My judgment is that the answer depends on how the exchange does it. If it simply packages US stock price exposure into a trading product, then it might indeed become just a distribution channel for traditional financial liquidity, maybe even just funneling crypto user traffic to US stocks.

But if it can reorganize asset issuance, trading, clearing, custody, and risk management based on stablecoin accounts, on-chain settlement, global accessibility, fractional trading, and 24/7 markets, then it enhances not just a specific US stock, but the value of Crypto as the next generation of financial infrastructure.

Moreover, if users have experienced many traditional financial platforms, they know the user barriers are very high: difficult account opening, high entry thresholds, and slow capital movement. Our goal is to connect underlying real-world assets through stablecoin settlement and on-chain RWA protocols, allowing Bitget's 120 million global users to trade top global assets with just a phone and an email.

I don't think this is outsourcing. Rather, it's using Crypto's high efficiency and low friction to disrupt and improve the traditional broker experience in a vertical sense. We aren't losing users; instead, through tokenization solutions like Reality, we are pulling real-world assets onto the chain, making them part of DeFi. This is expanding Crypto's territory. I believe that as the industry develops, the definition of Crypto is also evolving. Initially, Crypto meant only Bitcoin. Later, Crypto was also the memecoins everyone talked about. In the future, much of Crypto will be RWA. Regardless of the asset type, underlying technologies like blockchain are the cornerstone driving this new financial system. Our long-term bullishness on the industry stems, to some extent, from our confidence in the technology.

Bitget's proposition of UEX essentially allows users to trade cryptocurrencies, stocks, gold, forex, ETFs, and other assets within a single account. This sounds like an expansion of exchange capabilities, but it could also be interpreted as: relying solely on Crypto can no longer satisfy user needs, so exchanges must become comprehensive asset platforms.