「We Are Not TradeXYZ」: The Harsh Truth Behind the Closure of the First HIP-3 Platform

- Core Insight: Hyperliquid's HIP-3 mechanism allows anyone to deploy on-chain perpetual contract markets, but a pronounced Matthew effect exists within its ecosystem. The first deployer, TradeXYZ, leveraged its first-mover advantage, USDC pricing, the number of trading pairs, and airdrop expectations to monopolize over 95% of the trading volume, forcing other participants, such as Felix, to shut down due to high costs and thin profit margins.

- Key Elements:

- HIP-3 requires staking approximately 500,000 HYPE (valued at around $30 million) as collateral, along with bidding for Tickers (each pair costs about $30,000), creating an extremely high barrier to entry.

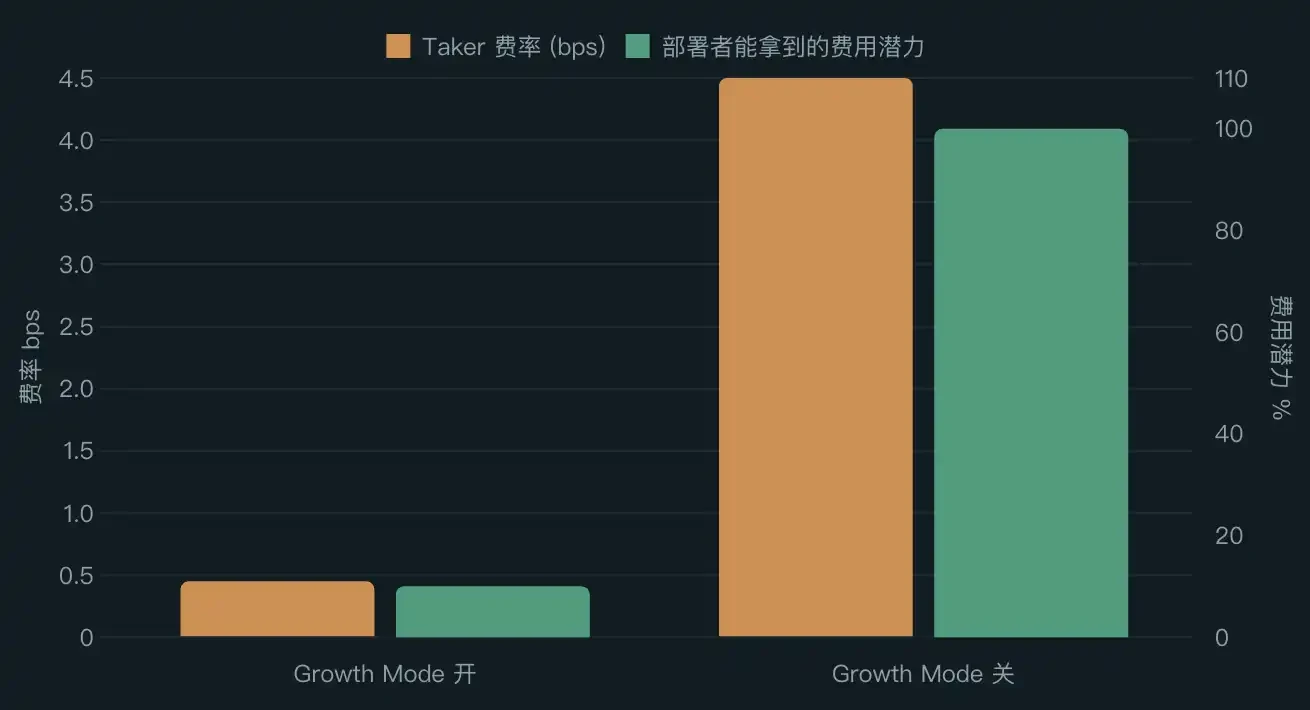

- Growth Mode significantly lowers trading fees, resulting in deployers earning only about 10% of the fee revenue, making it difficult for monthly income to cover the $60,000 opportunity cost of staking.

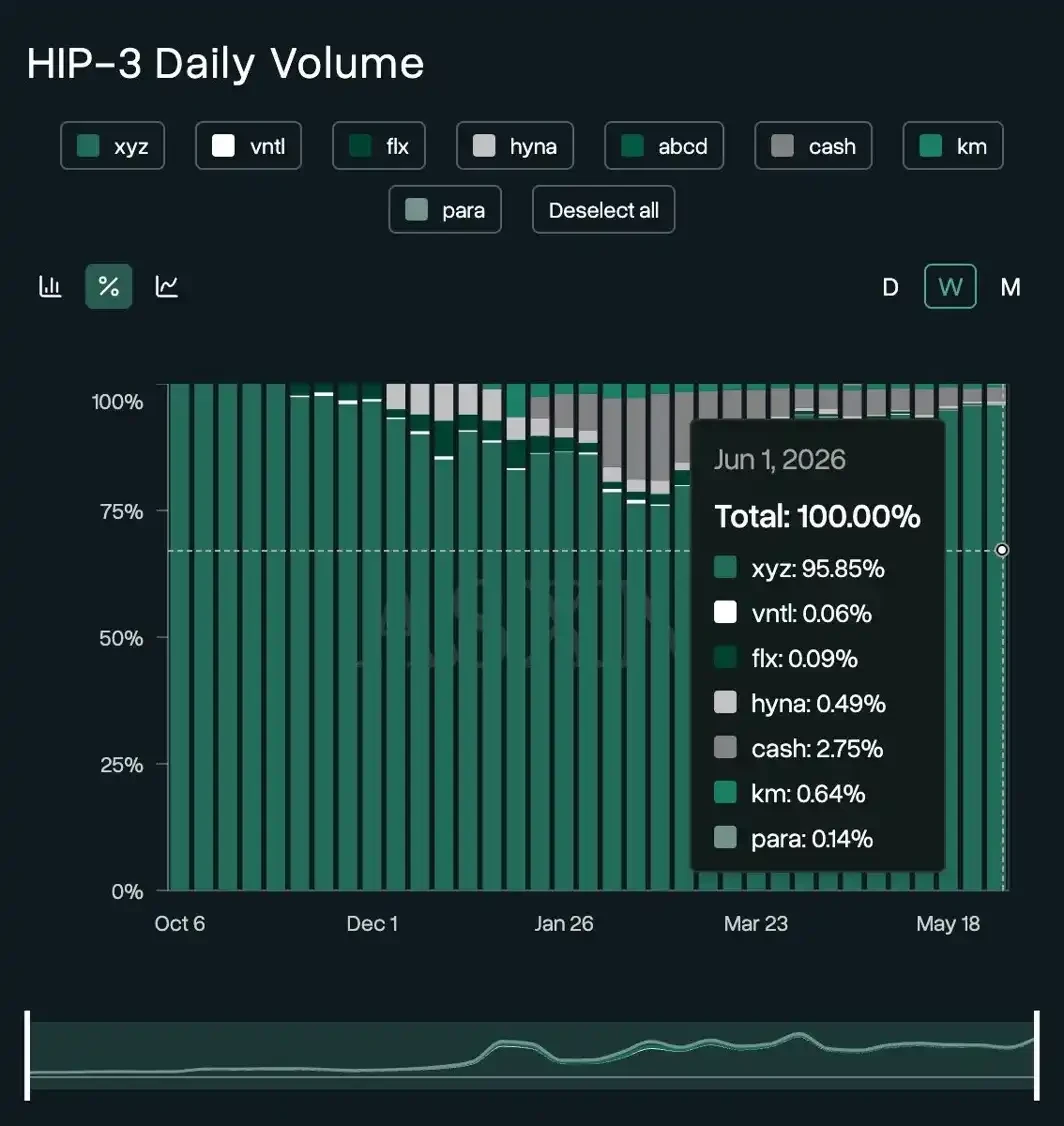

- TradeXYZ accounts for 95.85% of trading volume and 96.81% of open interest. Its single trading pair, XYZ100/USDC, contributes $4.53 billion in weekly trading volume.

- Felix's choice of USDH as the quote asset led to liquidity fragmentation. Users had to exchange currencies, and market makers were reluctant to participate. Subsequent policy changes by Hyperliquid further eroded its advantages.

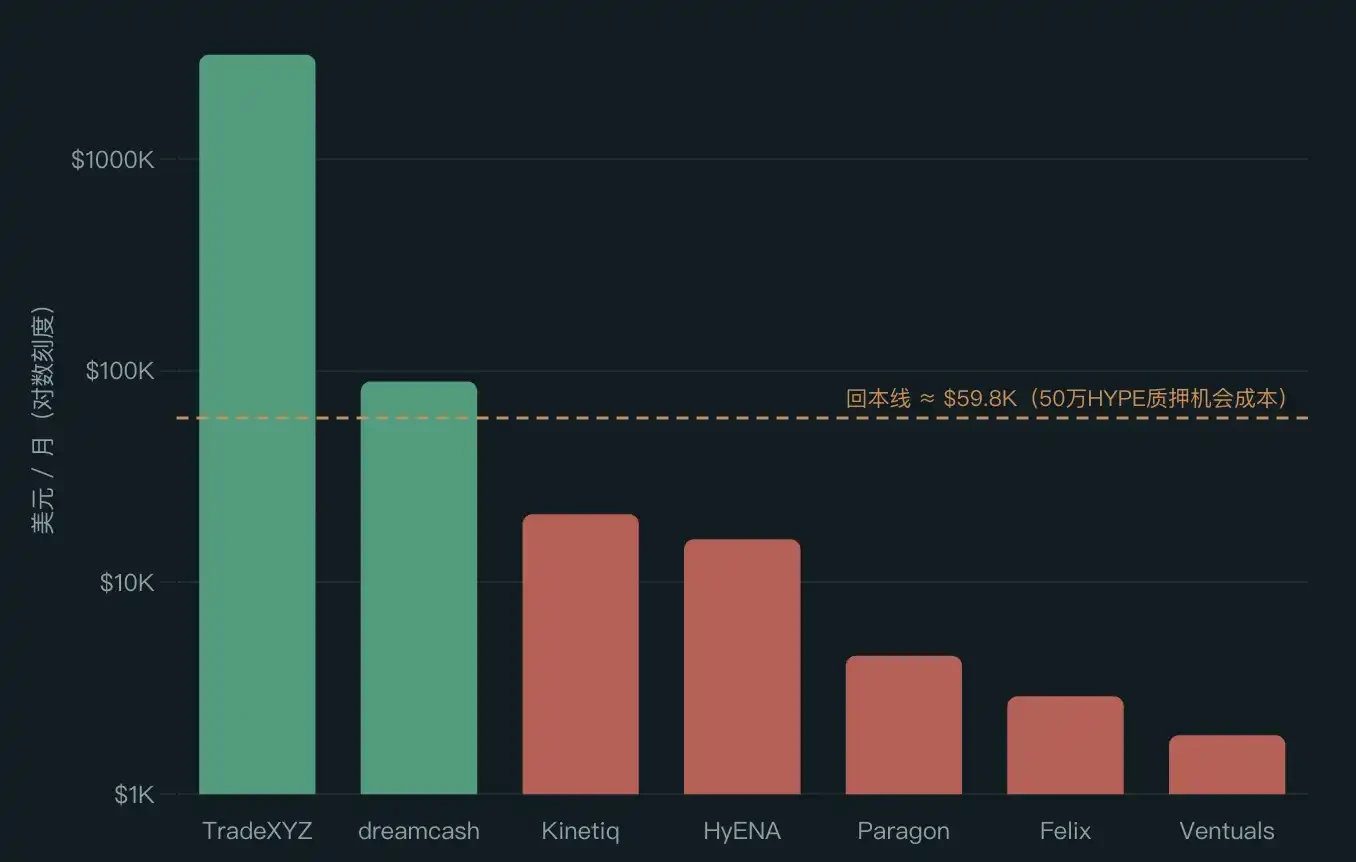

- Among non-TradeXYZ players, only DreamCash is barely profitable, benefiting from approximately $867,000 in monthly incentives provided by Tether. The monthly revenue of all other platforms remains below $5,000.

The opening pricing of a new IPO company on the US stock market, combined with the movement of hungry capital continuing to trade after the weekend close, led to an epic price discovery for Hyperliquid . HYPE’s all-time high caught the attention of traders worldwide, showcasing the capabilities of this 24/7 platform and the strength of a team called TradeXYZ.

Hyperliquid is a high-performance blockchain designed specifically for derivatives, featuring a fully on-chain order book. HIP-3 is its third improvement proposal: anyone who stakes approximately 500,000 HYPE as collateral can open their own perpetual market on this chain, trading US stocks, indices, commodities, and even companies without an IPO. Hyperliquid provides matching, margin, and on-chain settlement, while the deployer defines which trading pairs to list, which oracle to use, and how much leverage to offer.

TradeXYZ was the first trading platform deployed under the HIP-3 framework. Through weekend market pricing and pre-IPO contract trading, TradeXYZ attracted Wall Street’s attention within less than a year of its launch.

Besides TradeXYZ, several other HIP-3 trading platforms have been deployed sequentially, each attempting to replicate HIP-3's success through their own advantages.

However, the results have been disappointing.

Recently, Felix, a project within the Hyperliquid ecosystem, announced that its HIP-3 trading platform will begin shutting down on June 19, with all markets being liquidated one by one.

Felix was the first HIP-3 trading platform on Hyperliquid to list silver and crude oil trading pairs. The OIL, GOLD, and SILVER trading pairs generated considerable fees and approximately $3 billion in trading volume for it from December last year to January this year. Now, it has become the first formal HIP-3 deployer to exit.

Why would a once-leading player be the first to close its doors?

"We Are Not TradeXYZ"

Felix founder 0xBroze reviewed the reasons for this failed attempt.

First, the choice of quote asset was wrong. HIP-3 trading platforms need to select a stablecoin for their perpetual contracts. The earliest platform, TradeXYZ, chose USDC. At the time, this wasn't a deeply considered decision, as Hyperliquid hadn't yet launched its stablecoin bidding process. Felix, launching later, naturally chose USDH because using it offered fee discounts.

However, they didn't anticipate that Hyperliquid would later activate "Growth Mode," which drastically reduced trading fees. This eroded USDH's advantage, turning it into a "burden of liquidity fragmentation." Users holding USDC had to swap to USDH to use Felix, and market makers were unwilling to provide liquidity for USDH-related markets. In 0xBroze's post-mortem view, USDH seemed more like a pawn used by Hyperliquid to pressure Circle into sharing revenue.

Second, TradeXYZ arrived first. It launched on the very day HIP-3 went live, about a month earlier than Felix. This wasn't just a time gap; the early entrant captured user mindshare and had ample time to continuously launch subsequent markets.

Furthermore, TradeXYZ had more trading pairs. As the only deployer using USDC, TradeXYZ quickly built a moat with its sheer number of pairs. 0xBroze believes this likely reflects a balance sheet advantage – TradeXYZ could afford Ticker auction fees and liquidity costs. Felix, with limited capital, had to be more selective in choosing which pairs to open.

Finally, there was the "airdrop hint." Early users of TradeXYZ speculated that it would launch a token because the team behind TradeXYZ had previously won the spot ticker UNIT in a Hyperliquid auction. This airdrop expectation progressively boosted TradeXYZ's early user numbers, volume, open interest, and liquidity, creating a flywheel effect that Felix could never catch up with.

To sum it up in one sentence: We failed because we are not TradeXYZ.

The Matthew Effect

Let's look at the trading volume. In the week leading up to early June, TradeXYZ alone accounted for 95.85% of all HIP-3 volume. The remaining 7 platforms combined had less than 5%. Second-place dreamcash held 2.75%, third-place Kinetiq Markets held 0.64%, and HyENA held 0.49%.

Source: ASXN

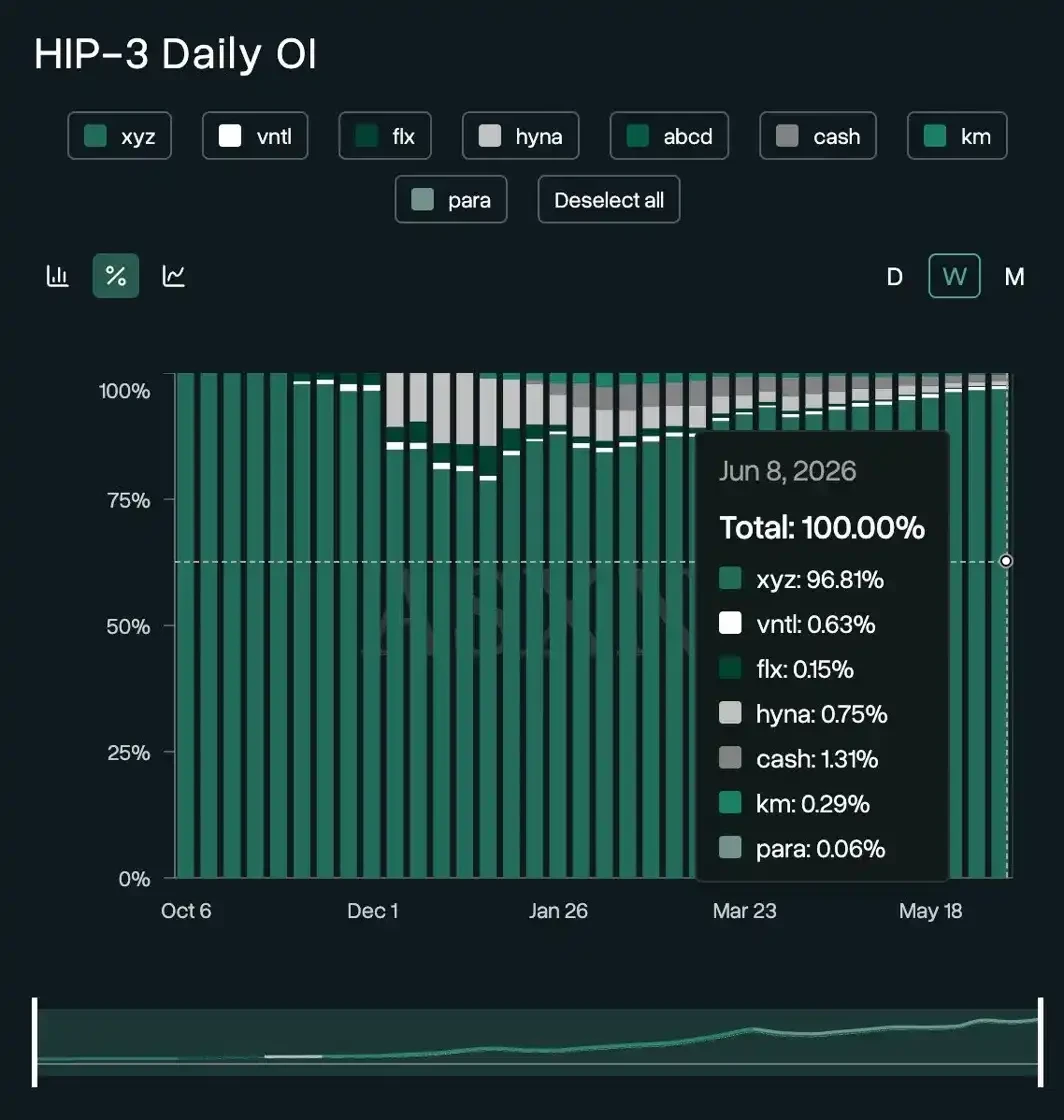

The concentration in open interest was even higher, with TradeXYZ accounting for 96.81%.

Source: ASXN

This monopolistic structure has been persistent. From the launch of the HIP-3 proposal in October last year to May this year, TradeXYZ's volume share never fell below 60%.

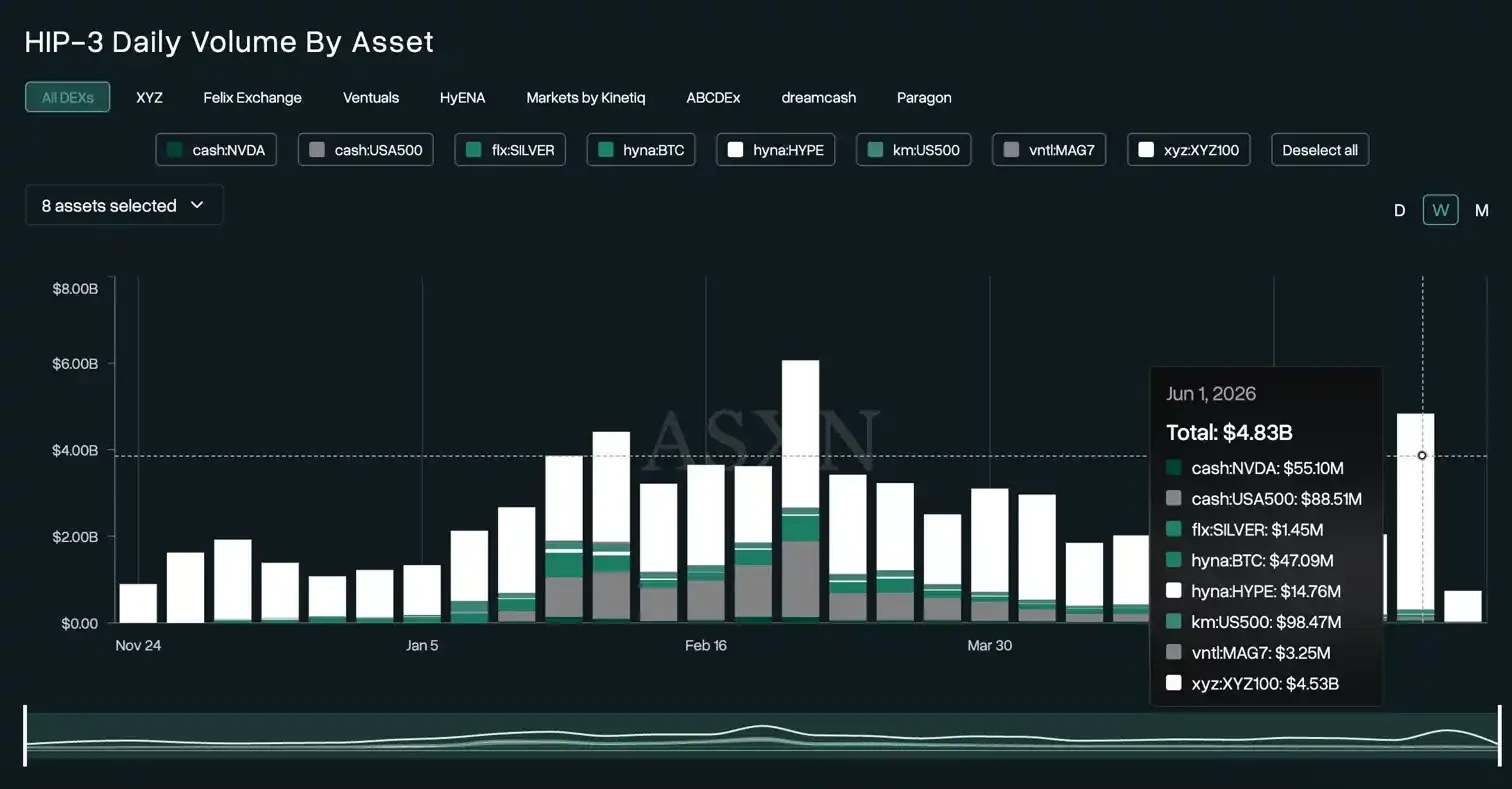

In the first week of June, total HIP-3 trading volume was $4.8 billion. A single pair, TradeXYZ's XYZ100/USDC, contributed $4.53 billion.

Source: ASXN

High Costs, Low Returns

To understand why other deployers struggle, one must analyze the economics of running a HIP-3 trading platform.

Two costs are fixed. Deploying a HIP-3 platform requires staking 500,000 HYPE, currently worth approximately $30 million (assuming HYPE is priced at $60).

Source: HypurrScan

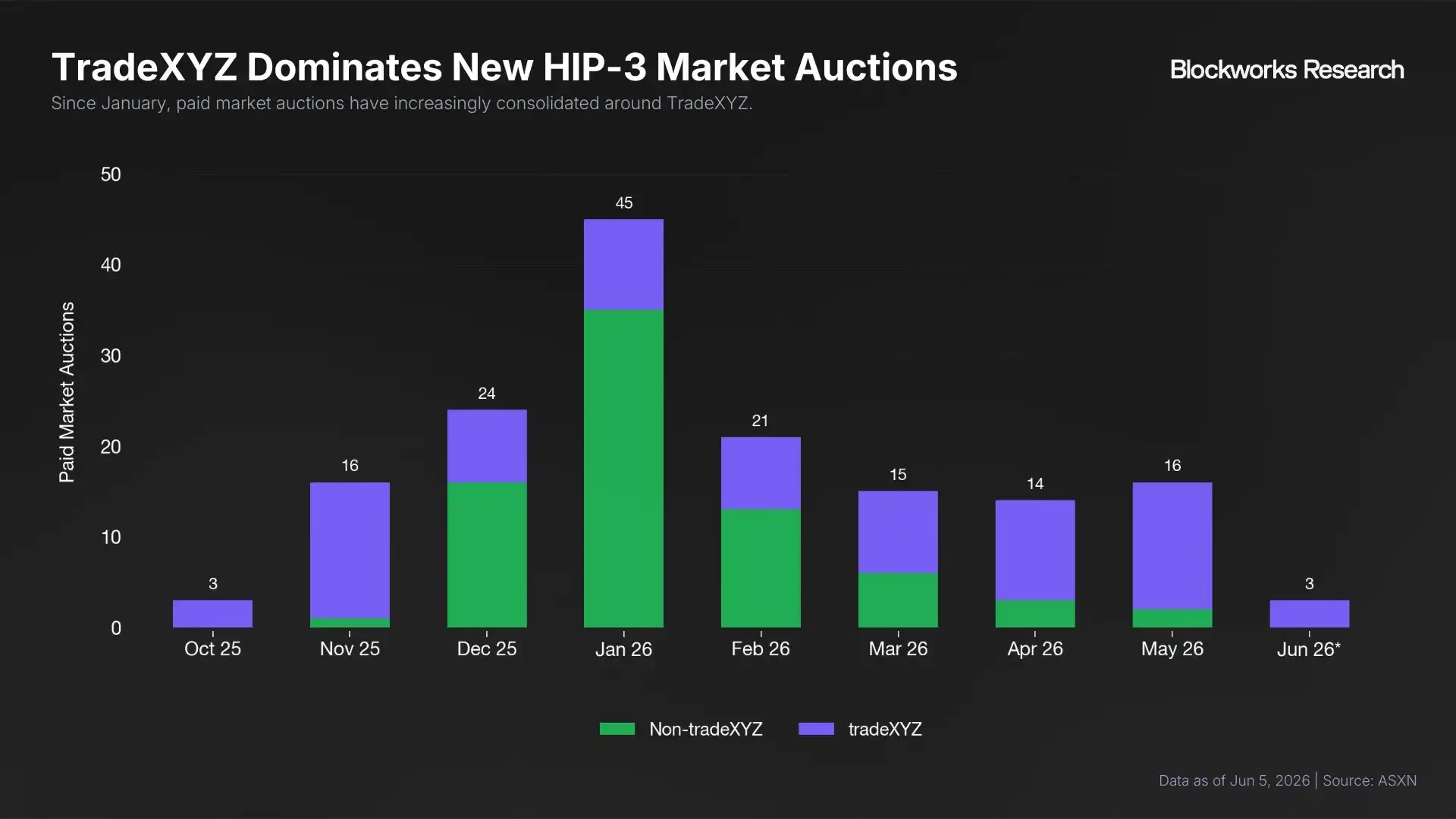

The second cost is the Ticker auction. Each new trading pair requires purchasing a Ticker via auction, with the average winning bid around 500 HYPE ($3,000). Currently, this auction market is also dominated by TradeXYZ. Since February, the enthusiasm for auctions from non-TradeXYZ participants has waned significantly.

Source: Blockworks Research

Running a HIP-3 platform involves not only high costs but also thin profit margins.

To make its perpetual contract fees competitive with traditional brokerages, Hyperliquid introduced "Growth Mode." When activated, taker fees are slashed to extremely low levels, making opening an NVDA position cheaper on Hyperliquid than on Interactive Brokers. The trade-off is that deployers receive only about 10% of the potential fee revenue.

If a deployer chose not to run a trading platform and simply staked their 500,000 HYPE at an approximate 2.3% annualized yield, they would earn about $60,000 per month. This means that just to break even against the "do nothing" opportunity cost, a platform's monthly fee income must exceed $60,000.

Here is the revenue situation for various platforms in May: TradeXYZ earned approximately $3.1 million, dreamcash around $89,000, Kinetiq about $21,000, and HyENA roughly $16,000. Those further down the list earned less than $5,000.

Apart from TradeXYZ, only dreamcash barely covered its costs. All other deployers failed to cover even the opportunity cost of the 500,000 HYPE stake. This calculation doesn't include harder-to-quantify expenses like market making, oracle fees, team salaries, and liquidity incentives.

Source: Blockworks Research

A Spectrum of Survival Strategies

The few remaining platforms each have their own survival tactics.

dreamcash uses USDT0 as its quote asset, backed by Tether. Tether provides it with approximately $200,000 in trading incentives weekly, translating to about $867,000 per month – far exceeding its platform fee revenue. Combined with a layer of airdrop anticipation, dreamcash sits securely in the second position by volume.

Kinetiq Markets boasts a novel "crowdfunding mechanism." Kinetiq developed a platform called Launch. Founder Omnia describes it as a combination of "Shopify + Kickstarter," allowing others to deploy their own customized HIP-3 trading platforms using crowdfunded 500,000 HYPE. Kinetiq Markets itself serves as a proof-of-concept for this model, aiming to validate Launch's viability rather than competing directly with TradeXYZ for volume.

The Road Ahead

Felix certainly won't be the last HIP-3 trading platform to shut down. There is limited room for other players to adjust their strategies.

Perhaps they could target niche or new markets that TradeXYZ is unwilling to touch. However, Felix has already proven the outcome: "Once you generate volume, TradeXYZ will copy it and siphon off your liquidity."

Alternatively, they could explore different distribution channels, building a user base in net-new markets away from the red ocean of native Hyperliquid traders. Kinetiq's Launch is an attempt in this direction, but hasn't proven successful yet.

Unless there is a change on the cost side, the current scenario of one dominant player is likely to persist.

Some community members have proposed lowering the 500,000 HYPE staking threshold and implementing a lower, floating auction price tied to HYPE's value. From this perspective, a decline in HYPE's price might not be entirely negative, as it could allow more projects to build on Hyperliquid at a lower cost.

```