SemiAnalysis vs 白毛股神:砸盤CPO報告暗藏哪些真金?

- 核心觀點:市場對CPO(共封裝光學)放量時間表的預期出現分歧,導致光學股回調。SemiAnalysis認為規模化量產可能延至2028-2029年,而分析師Serenity則反駁稱輝達的供應鏈執行力可能加速這一進程,爭議核心在於CPO商業化的斜率而非方向。

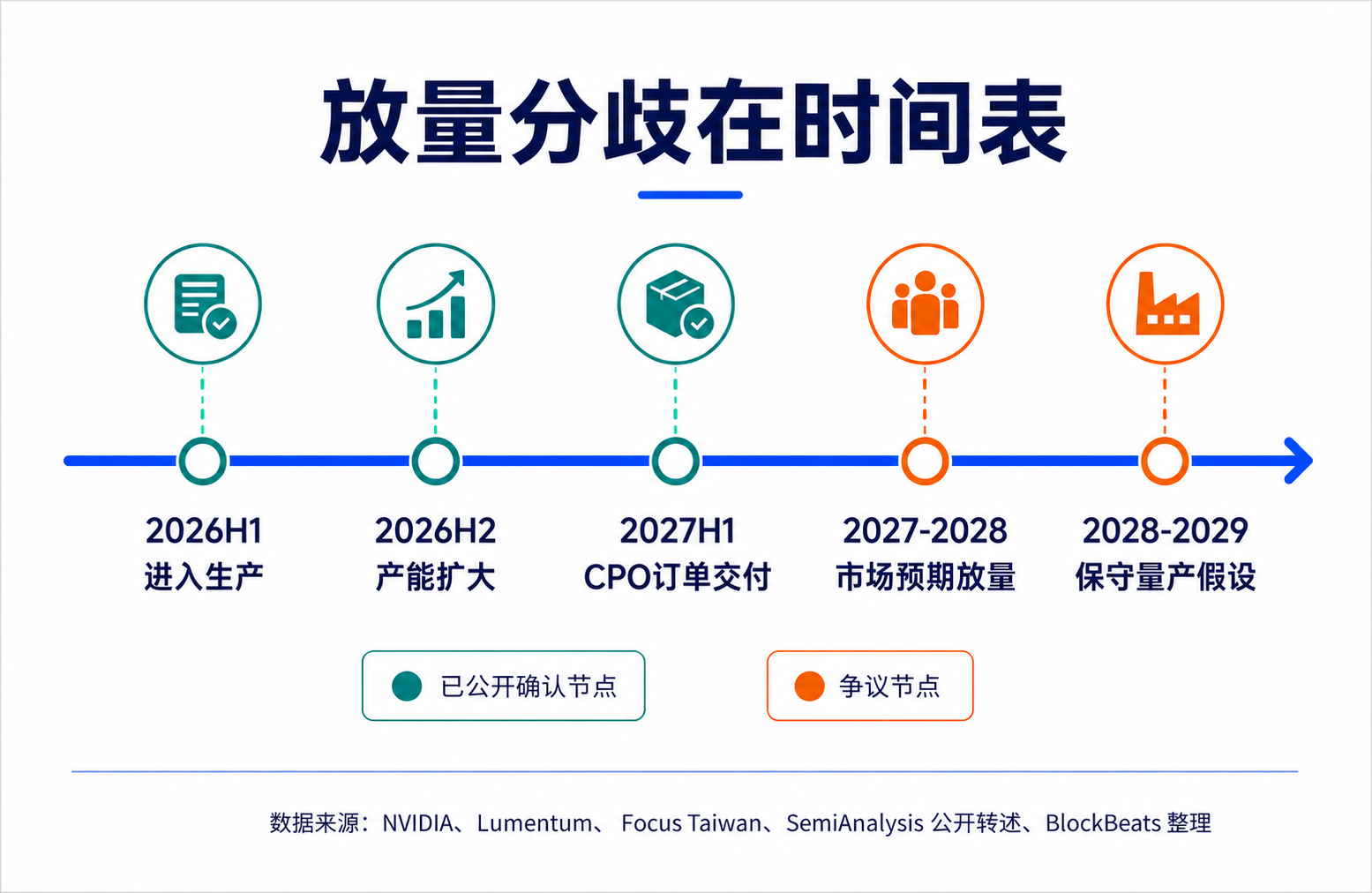

- 關鍵要素:

- SemiAnalysis 6月報告引發市場波動,其核心判斷是CPO大規模量產可能延至2028-2029年,而NPO(近封裝光學)項目可能加速,導致AAOI、LITE等光學股出現高個位數至雙位數回調。

- Serenity反駁SemiAnalysis的保守模型,認為其低估了輝達壓縮硬體週期的能力,援引Lumentum數億美元CPO增量訂單及Spectrum-X進入生產等訊號,堅持CPO仍在2026年下半年至2028年的爬坡軌道上。

- CPO的理論優勢在於通過將光學引擎靠近ASIC,解決高頻寬下的功耗與訊號完整性瓶頸,但其系統工程難度(如維修、良率、可靠性)可能導致規模化落地慢於市場預期。

- NPO因介於CPO與傳統可插拔模組之間,成為爭議焦點:若CPO延遲,NPO將獲得更長的市場窗口;若CPO加速,NPO也可能與CPO在不同網路層級並行存在,重塑技術路線間的價值分配。

- 市場此前過度交易「CPO終局」敘事,SemiAnalysis與Serenity的分歧本質是將估值錨從方向轉向時間表驗證,後續關鍵看2026下半年至2028年的生產級數據,特別是出貨口徑(小批量 vs. 大規模)與現場可靠性數據。

TL;DR

- SemiAnalysis believes the ramp-up of CPO will be slower than the market expects, potentially prolonging the transition window for NPO.

- The "White-Haired Stock God" disagrees with this assessment, arguing that Nvidia and the supply chain are pushing CPO forward more quickly.

- Related tickers: AAOI, LITE, COHR, GLW, MRVL, SIVE, AVGO, NVDA

The recent decline in optical stocks, ostensibly sparked by cold water being thrown on the CPO narrative, is essentially the market re-pricing a more sensitive issue: Will the volume ramp-up in 2027-2028 be a period of earnings realization, or merely a phase of introduction and validation?

CPO (Co-Packaged Optics) itself has not been negated. The pressure on bandwidth, power consumption, and switching density in AI data centers continues to increase, and the physical limitations of copper cables and traditional pluggable optical modules have not disappeared. The issue is that the previous rally in related stocks had already priced in an aggressive timeline: after Nvidia pushes CPO into the commercialization window, components like optical engines, lasers, silicon photonics, and switch ASICs would rapidly enter volume shipments in 2027-2028.

The June 9 report from SemiAnalysis precisely targeted this pricing assumption. According to public summaries, the report suggests that Nvidia's 800V DC and CPO mass production might be delayed until around 2028-2029, with 400V DC still ramping up in 2026, and some NPO (Near-Package Optics) projects potentially accelerating. The report triggered market volatility, leading to high single-digit to double-digit corrections in stocks like AAOI, LITE, COHR, GLW, and MRVL across the optical and related supply chains. The market is not trading on "whether the CPO direction is valid," but rather on "how quickly CPO can translate into orders."

However, this is not a one-sided bearish view. The "White-Haired Stock God" and AI supply chain analyst Serenity (@aleabitoreddit) subsequently countered SemiAnalysis, arguing that their view overly relies on conservative engineering models and underestimates Nvidia's ability to compress hardware cycles. Based on his interpretation of signals from Nvidia, Lumentum, Foxconn, and others, he emphasizes that CPO remains on track for ramps in the second half of 2026, the second half of 2027, and 2028.

The value of this debate is not about declaring a "winner," but about shifting the valuation anchor for the optical supply chain from an end-game narrative to timeline validation: CPO is coming, but the slope at which it arrives determines the value distribution among NPO, pluggable modules, light sources, and switch ASICs.

Timeline Reassessment Behind the Optical Stock Decline

Over the past few months, the core reason the market bought into the optical supply chain was not current revenue, but the migration of capital expenditure towards the next-generation network architecture of AI data centers.

As model training and inference clusters expand, the communication pressure between GPUs, racks, and within data centers continues to rise. The network is no longer just a supporting system outside the server; it increasingly resembles the efficiency bottleneck of the AI factory. Higher bandwidth density and lower power consumption raise the upper limit for scaling a unit of computing power cluster. This is why CPO has been brought to the forefront.

The theoretical appeal of CPO is straightforward: bring the optical engine as close as possible to the ASIC (dedicated switch chip), shortening high-speed electrical signal paths and reducing the power consumption, loss, and signal integrity issues caused by serial-deserialization circuits and copper traces. Compared to traditional pluggable modules, CPO offers better imagination space for power efficiency and density in the high-bandwidth era.

The market's problem is that it tends to prematurely trade "correct direction" as "confirmed volume." Nvidia's official press release stated that the Vera Rubin platform will introduce Spectrum-X Ethernet Photonics, with CPO switches already in production for scaling AI factories and cross-cluster deployment. A June 3 report quoted an Nvidia networking executive saying that Spectrum-X CPO switches have shipped to some partners, with production capacity expected to expand in the second half of 2026.

These signals are sufficient to prove that CPO is progressing, but they cannot be directly equated to risk-free realization of production-grade mass orders. For the capital market, there is a significant difference in valuation between "entering production," "shipping to some partners," "customer evaluation," and "mass production." The pullback triggered by SemiAnalysis's report is essentially the market starting to differentiate between these statements.

SemiAnalysis's Conservative Model: CPO's Difficulty Lies in System Engineering

SemiAnalysis is not saying CPO has no future. Its core judgment seems more like: CPO's theoretical advantages are clear, but its large-scale implementation will be slower than the market imagines.

The reason is not just that one or two components aren't ready, but that CPO concentrates the complexity previously scattered across modules, boards, and entire systems into a more deeply coupled system. The higher the integration, the better the point performance, but the pressure on manufacturing, testing, repair, and supply chain resilience also increases.

The advantage of traditional pluggable modules is modularity. If an optical module fails, you replace the module, and switching between suppliers is relatively easy. CPO is different. The optical engine is closer to the ASIC, even entering the same packaging system. The power and density benefits come from this close coupling, but the repair radius also expands. If an optical component fails, it doesn't just affect an easily swappable module; it can involve the higher-value switch chip and the entire system.

SemiAnalysis's previous CPO Book repeatedly emphasized serviceability, reliability, yield, and supply chain maturity. This is especially true in the hyperscaler cloud context, where performance is not the only metric. Major customers have high requirements for reliability and maintainability. If the failure rate, repair process, and replacement costs in a production environment are uncontrollable, even the best energy model risks being delayed for adoption.

InP lasers are also a point of contention. Lab-level port operating life data can prove technical feasibility, but it doesn't cover long-term operation, mass manufacturing, field maintenance, and supply chain redundancy in a large-scale data center. For investors, this distinction is critical: lab validation proves the direction, but field reliability determines the volume ramp-up.

In SemiAnalysis's framework, NPO and pluggable modules are not backward paths, but more realistic intermediate layers before engineering risks are fully resolved. CPO is theoretically superior, but if full deployment takes longer, the market must reprice these "less end-game but easier to manufacture and maintain" solutions.

Serenity's Rebuttal: Nvidia Could Compress Hardware Cycles

Serenity's rebuttal does not deny that CPO has engineering difficulties, but argues that SemiAnalysis underestimates Nvidia's organizational capability in the AI hardware cycle.

His logic is clear: normal hardware adoption is indeed held back by yield, reliability, and customer validation, but Nvidia is not a normal customer. It is both the definer of GPU cluster architecture and the core driver of networking, switches, system integration, and supply chain rhythm. When AI factory scaling is constrained by network power and bandwidth limits, Nvidia has strong economic motivation and industry leverage to compress traditional adoption cycles.

Serenity's evidence is two-fold. The first layer comprises publicly cross-verifiable company statements, including Nvidia's official information about Spectrum-X Photonics entering production, and Lumentum's Q2 FY26 commentary mentioning CPO orders and delivery schedules. Lumentum mentioned receiving hundreds of millions of dollars in incremental CPO orders, with delivery in the first half of 2027. Company materials also indicated that CPO-related business is expected to enter a broader ramp in the second half of 2026.

The second layer involves interpretation of supply chain signals, such as Foxconn's early delivery of optical switches to Nvidia. However, the specific scale of these signals—whether they are test prototypes or production-grade orders—still requires more public information for confirmation.

This is also the crux of the disagreement between Serenity and SemiAnalysis: SemiAnalysis believes system engineering variables will naturally lengthen the cycle, while Serenity believes Nvidia's supply chain execution capability will steepen the curve.

These two judgments are not entirely conflicting. Nvidia can bring CPO into production and customer validation sooner and may push adoption in certain scale-out scenarios first, but this doesn't automatically mean all AI data center networks will rapidly switch to CPO by 2027. The adoption pace will likely be tiered based on scale-out vs. scale-up, intra-rack vs. inter-rack, and different customers' tolerance for risk and cost models.

Serenity refutes the overly conservative conclusion that "CPO will be significantly delayed," not proving that "CPO is already completely risk-free." For the market, this is sufficient to support a dead-cat bounce logic, but not enough to immediately rewrite the aggressive 2027-2028 revenue curve back into certainty.

Why NPO Suddenly Became Important

NPO has suddenly become important in this debate because it sits right between the logic of SemiAnalysis and Serenity.

It is not the antithesis of CPO, nor a simple extension of traditional pluggable modules. NPO's basic idea is to place the optical engine on a pluggable base substrate near the ASIC, shortening the electrical signal path to gain some power and density benefits while retaining better testability, replaceability, and supply chain flexibility.

If SemiAnalysis's conservative model is closer to reality, and the deep packaging of CPO slows down due to yield, repair, and reliability issues, NPO will become the more realistic choice for a longer period. It allows hyperscalers to gradually gain operational experience with optical interconnects without fully bearing the risk of all-CPO, while also giving existing optical module and engine suppliers a longer window.

If Serenity's judgment on Nvidia's execution is more accurate, NPO may not disappear either. It is more likely that NPO, CPO, pluggable modules, and copper interconnects will coexist at different network layers. Nvidia's own roadmap also suggests scale-out CPO can go first, while some scale-up rack scenarios might still rely on copper or hybrid architectures in 2027-2028.

The implication for investors is that the optical supply chain cannot be priced solely on a "CPO wins, others lose" basis. Different technology routes benefit different segments: CPO favors highly integrated optical engines, laser light sources, silicon photonics, and the switch ASIC ecosystem. Prolonging the NPO and pluggable window might allow existing optical module makers, connector, material, and some light source suppliers to continue enjoying orders and gross margin support.

The market's previous problem was translating the technological end-game too early into the earnings slope of a single route. What is now being reopened is the valuation space for intermediate solutions.

Production-Level Data is the Next Verification Point

This debate will not be resolved in the short term by a single report or a set of posts. SemiAnalysis reminds the market that CPO's difficulty lies in system engineering. Serenity reminds the market that Nvidia's supply chain organizational capability could change traditional hardware adoption cycles. Their true disagreement can only be validated by production-level data from the second half of 2026 through 2028.

Going forward, the most critical aspect is not "whether shipments have happened," but the phrasing of the shipments. "Delivering to some partners," "customer evaluation," "initial production," "ramping up scale," and "large-scale deployment" are completely different stages. Nvidia's subsequent descriptions of Spectrum-X / Quantum-X Photonics production volume, and the commentary from optical suppliers like Lumentum, Coherent, and others in earnings calls regarding orders, capacity, and gross margins, will be more important than the wording of a single conference.

Similarly, field reliability and repair data need to be monitored. If failure rates, replacement processes, yield curves, and total cost of ownership (TCO) for CPO in production environments prove sufficiently stable, SemiAnalysis's conservative model will be revised. If these data points remain stuck at the lab or small-batch validation level, the window for NPO and pluggable modules will continue to be revised upward by the market.

The optical supply chain is currently trading not on the life or death of CPO, but on the slope of its timeline. The next verification point hinges on whether "entering production" can translate into sustainable volume, and the speed at which this volume is ultimately reflected in orders, gross margins, and customer deployment language.

While SemiAnalysis raised concerns about CPO technology's prospects over the next two years, they still highlighted five bullish semiconductor sub-sectors:

Copper / AEC / ACC ;

Pluggable Optics / DSP ;

CPO Test Equipment ;

Power Gray Space / UPS Continuation ;

Board-Level VRM / Silicon Power / Passive Components

The specific stocks within these sectors are compiled in the following image for readers' reference.