How far is the current US stock bull market from the peaks of historical bubbles?

- Core Viewpoint: Goldman Sachs' latest assessment shows that the current level of exuberance in the US stock market has risen to the 86th historical percentile, approaching but not yet reaching the peaks of the 2000 internet bubble and the 2021 bull market. The bull market still has room to run, but risks are accumulating.

- Key Elements:

- The S&P 500 index has surged 15% in the past two months, with its return/volatility ratio approaching 4, marking the strongest rebound in over 50 years.

- This rally is primarily supported by a significant upward revision in near-term earnings expectations, rather than emotional frenzy, with relatively solid fundamentals.

- Goldman Sachs' comprehensive assessment framework shows market exuberance at the 86th percentile, lower than the 2000 (100th percentile) and 2021 (95th percentile) levels.

- Speculative trading volume, call option volumes, and retail margin balances are all on the rise but have not reached historical peak levels.

- None of the four major risk signals (speculative frenzy, deteriorating growth, stock issuance, Fed tightening) have been fully triggered, but each is closer to the threshold than it was a few months ago.

- The pick-up in IPO activity, pressure on corporate profit margins, and the rise in implied probability of rate hikes reflected by the interest rate market are potential risk points.

Original Author: Zhao Ying

Original Source: Wall Street Sights (華爾街見聞)

According to the latest assessment by Goldman Sachs' chief U.S. equity strategist, the current market euphoria has risen to the 86th percentile historically, approaching but not yet touching the extreme levels seen at the peak of the 2000 internet bubble and the 2021 bull market peak.

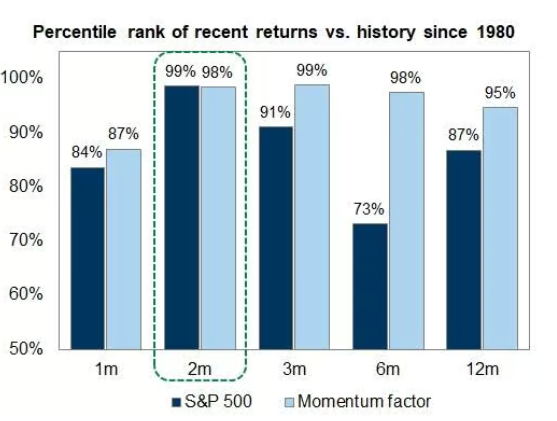

In the past two months, the S&P 500 Index surged 15% before Friday's pullback, placing this rally at the 99th percentile in historical data since 1980. In his latest report, Goldman Sachs' chief U.S. equity strategist Ben Snider pointed out that although the four major signals of past bull market peaks—speculative frenzy, deteriorating growth, massive equity issuance, and Fed tightening—are not fully present now, each one is closer to the trigger threshold than it was a few months ago.

For the market, this assessment means the current bull run still has room to run, but risks are accumulating. Snider explicitly stated, "We're not there yet," while warning that the market does not need to reach extreme investor euphoria before a downturn occurs, and historical patterns may not repeat in this cycle.

The Ferocity of the Rally: The Strongest Volatility-Adjusted Rebound in 50 Years

The speed of this rebound has left its mark on history. According to Goldman Sachs data, the S&P 500's 15% gain in about two months has a return/volatility ratio near 4, the highest level in over 50 years.

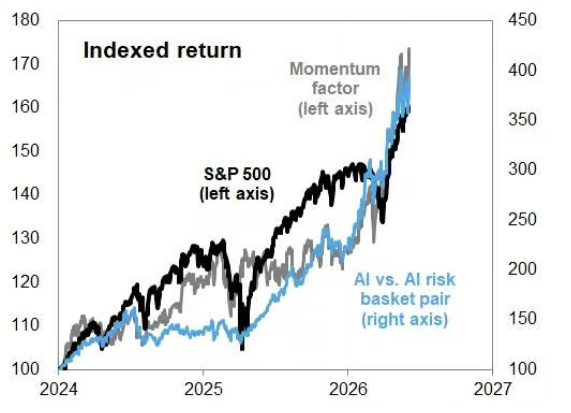

Artificial intelligence is the core theme driving this rally. AI concept stocks, momentum factors, and the broader market index have risen in tandem, creating a high degree of resonance.

Snider noted that unlike similar momentum-driven rallies (such as late 1999 and late 2021), this rally's primary support comes from a sharp upward revision in recent earnings expectations, rather than pure sentiment泡沫. This, to some extent, gives the current uptrend a more solid fundamental foundation.

Euphoria Indicator: 86th Percentile, Below Two Historical Peaks

To quantify the current market sentiment, Snider constructed a comprehensive assessment framework covering four major categories and a total of nine indicators. Historical data shows that at the peak of the 2000 internet bubble, the median ranking of these indicators was at the 100th percentile; at the 2021 bull market peak, it was at the 95th percentile. The current reading is at the 86th percentile—above historical averages but still significantly behind the previous two extreme peaks.

Specifically, Goldman Sachs' speculative trading indicator has risen in recent months but remains below late 2025 levels and far below the peaks of 2000 and 2021. Among various speculative trading activities, trading volume in high-valuation stocks has recently increased significantly, while trading activity in loss-making stocks has been relatively moderate. Additionally, both stock call option volume and retail margin balances are trending upward, indicating investor sentiment is heating up.

Notably, the breadth of this rally is extremely narrow but has not yet reached the extreme concentration seen during the internet bubble era.

Four Risk Signals: Not Yet Triggered, but the Distance is Shrinking

Goldman Sachs' analytical framework attributes the end of historically high-valuation, high-concentration bull markets to four factors: speculative frenzy, deteriorating growth outlook, an extreme surge in equity issuance, and Fed tightening. Snider points out that while none of these four conditions perfectly matches the current environment, each is closer to a warning line than at the beginning of the year.

IPO activity is picking up, putting pressure on the equity issuance side; rising input costs are compressing corporate profit margins, posing a potential threat to the growth outlook; pricing in the interest rate market has begun to reflect an increased probability of Fed rate hikes, although Goldman Sachs economists believe an actual rate hike is unlikely.

Snider also emphasized that market declines do not require extreme investor euphoria as a prerequisite, and the euphoric characteristics seen at past bull market peaks may not reappear in the same form in this cycle. This means that even if current indicators have not yet reached historical extremes, investors should not regard this as a sufficient guarantee of a safety margin.

Overall, Goldman Sachs' assessment offers a cautious but not pessimistic judgment: the level of euphoria in this bull market is "getting closer" to the historical peak zone but has not yet arrived. The key support for this judgment is that the current rally still has improving earnings expectations as a fundamental backing, rather than being purely driven by sentiment. However, with momentum factors remaining strong, market concentration high, and some risk signals quietly heating up, Snider's report essentially suggests to investors: the window is still open, but it is slowly narrowing.