一个AI讀完SpaceX招股書,花12分鐘寫出這份投資備忘錄

- 核心觀點:AI代理自主完成對226MB SpaceX S-1文件的分析,生成包含多空論證、估值模型和風險矩陣的投資備忘錄,成本僅1.87美元。這標誌著AI能獨立付費獲取數據並決策,正重新構築華爾街傳統投行分析工作模式。

- 關鍵要素:

- AI代理通過Base鏈上6次付費API調用(花費1.87美元USDC)在12分鐘內完成市場數據獲取及分析,全程無需API金鑰或人工干預。

- SpaceX擁有三重核心優勢:商業航太近乎壟斷(佔全球入軌質量80%)、Starlink連接業務盈利(2025年收入114億美元,+49.8%)、以及垂直整合AI實驗室的軌道計算潛力。

- 空方核心風險包括:AI部門年燒錢超過60億美元、真實債務約420億美元(含200億美元過橋貸款)、196億美元EchoStar頻譜承諾及最高100億美元Cursor期權終止費。

- IPO定價存在承銷商利益衝突(主承銷商同為過橋貸款方),且公司治理上馬斯克持有多數投票權,依賴受控公司豁免。

- 估值錨點:連接業務獨立估值約840億美元(基於Iridium 7.4倍市銷率),但AI分部高燒錢導致整體GAAP營業虧損26億美元,調整後EBITDA美化約90億美元。

Original Author: Nick Prince

Original Translation: TechFlow

Introduction: An AI agent autonomously completed work that would take a team of investment analysts days: reading through the 226MB SpaceX S-1 filing, purchasing real-time market data on the Base chain using USDC, and generating an investment committee memo complete with multi-sided arguments, valuation models, and a risk matrix—all for a total cost of just $1.87. This is not a demo; it is a record of real, paid API calls. When AI agents can pay for their own data and decide their own analytical paths, the way Wall Street works is being reshaped.

An AI agent read Monday's 226MB SpaceX S-1 filing, used USDC on the Base chain to buy real-time market data, and generated this investment committee memo in 12 minutes. Total cost: 6 paid API calls, $1.87 USDC, no API keys required.

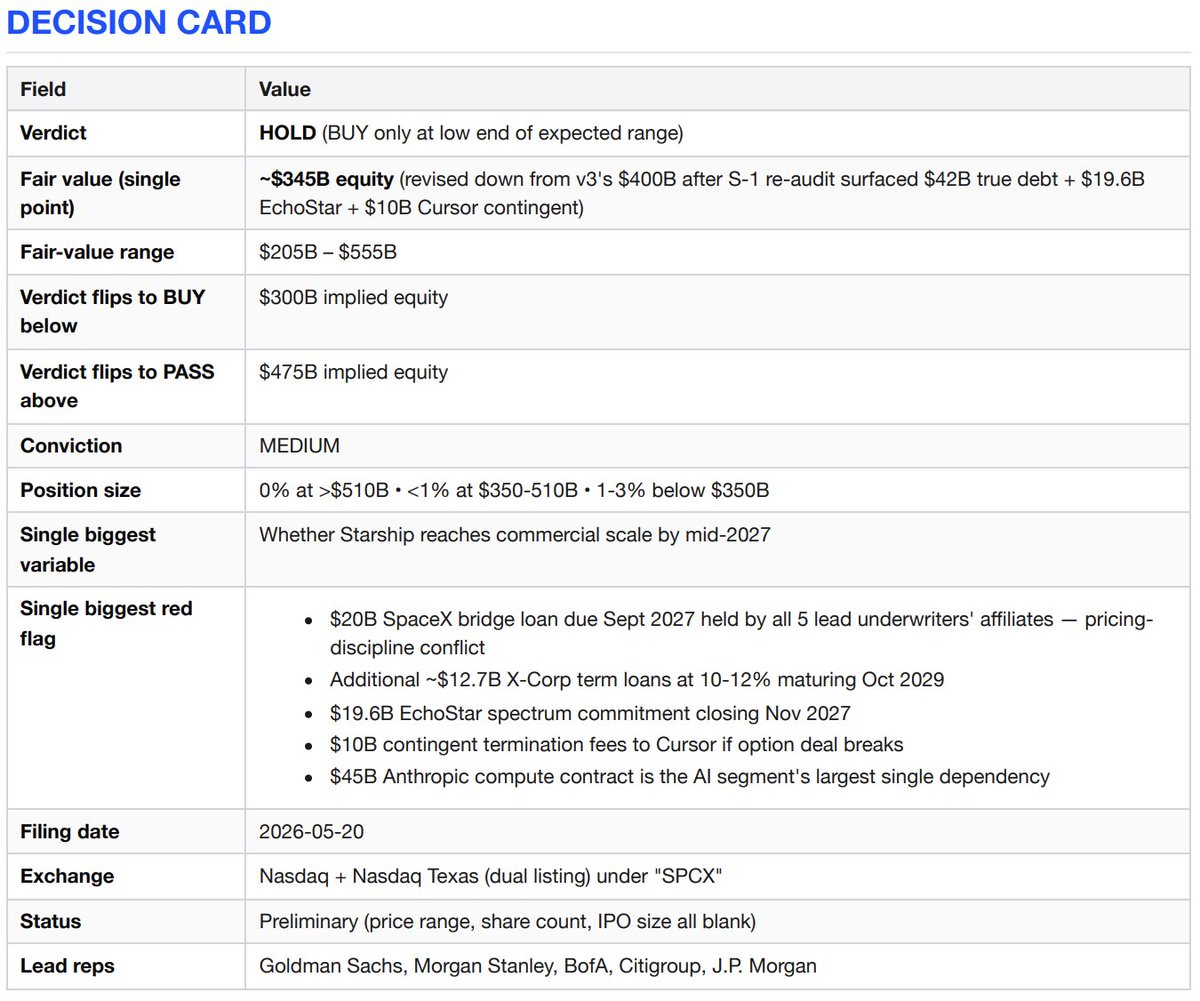

Decision Card (Conclusion: Hold/Watch)

Bullish Arguments

SpaceX possesses three businesses that competitors cannot replicate. First, a near-monopoly on commercial space access—accounting for 80% of global launch mass since 2023, a 99% Falcon mission success rate, and a 10-year lead in reusable technology. Second, the world's only deployed LEO broadband network—Starlink has 10.3 million subscribers across 164 countries, up 49.8% year-over-year, with segment-adjusted EBITDA of $7.2 billion. Third, with the acquisition of xAI since February 2026, it has become the only AI lab vertically integrated to the launch vehicle level, with plans to deploy orbital computing power. By any reasonable valuation method, this is a generational asset.

Bearish Arguments

The Connectivity business is real and profitable. But everything else is either burning cash at an alarming rate—the AI division lost $6.4 billion on $3.2 billion in revenue in 2025—or bets on Starship, which has completed 11 flight tests but has yet to deliver a payload to orbit. This IPO is, in part, a refinancing event. SpaceX took on a $20 billion bridge loan to acquire xAI, due September 2027, and the bridge lenders are exactly the underwriters of this IPO. If the valuation exceeds $500 billion, you are paying for unexecuted capabilities, corporate governance you have no say in, and a refinancing transaction the underwriters need to succeed.

Investment Thesis

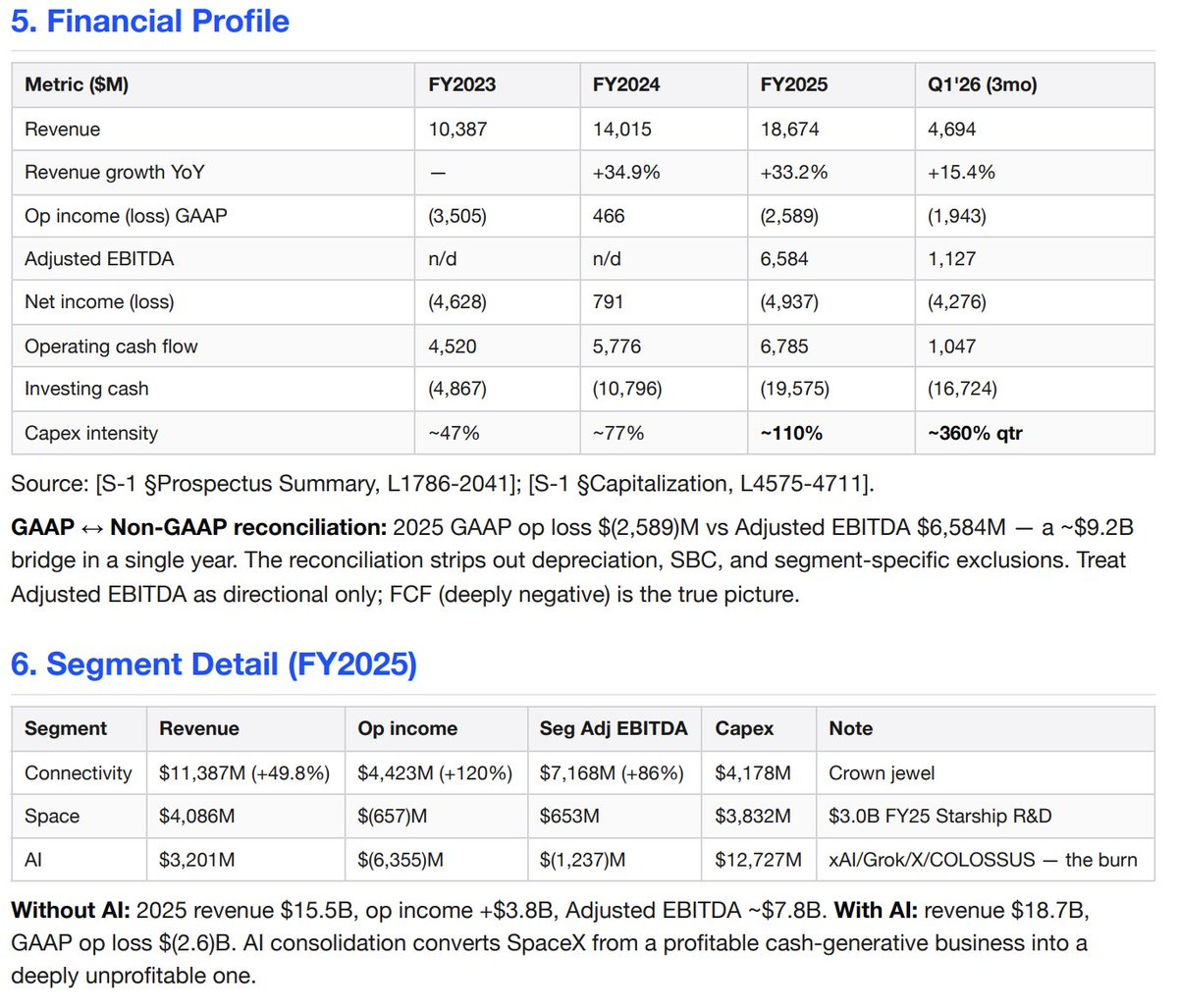

Starlink is an excellent standalone business. 2025 revenue of $11.4 billion (+49.8%), operating income of $4.4 billion (+120%), segment-adjusted EBITDA of $7.2 billion (+86%). High-value subscription services, 10.3 million paying users.

The launch business is unmatched. Accounting for over 80% of global launch mass since 2023, Falcon has a success rate exceeding 99%, with the Falcon 9 first stage flying up to 34 times.

Vertical integration is real and compounding. Rockets → Satellites → Spectrum (EchoStar AWS-4/H-band deal approved by the FCC) → AI computing power (two COLOSSUS clusters ~1GW).

Government dependency is a moat, not a risk. Primary launch provider for national security: executed 11 of 12 National Security Space Launch missions in 2025, and all 5 NASA crew and cargo flights.

Option value of orbital AI computing power, planned for deployment in 2028. If Starship achieves even 50% of its stated economics—reducing launch costs by 99%—the addressable market expands by an order of magnitude.

Counterarguments

The AI division is a cash furnace burning over $6 billion annually. 2025: $3.2 billion revenue versus $6.4 billion operating loss, negative segment-adjusted EBITDA of -$1.2 billion, capital expenditures of $12.7 billion. Q1 2026 alone: $818 million revenue versus $2.5 billion operating loss, $7.7 billion in capital expenditures. Annualized AI capex is now over $30 billion, while AI revenue is only $3.2 billion.

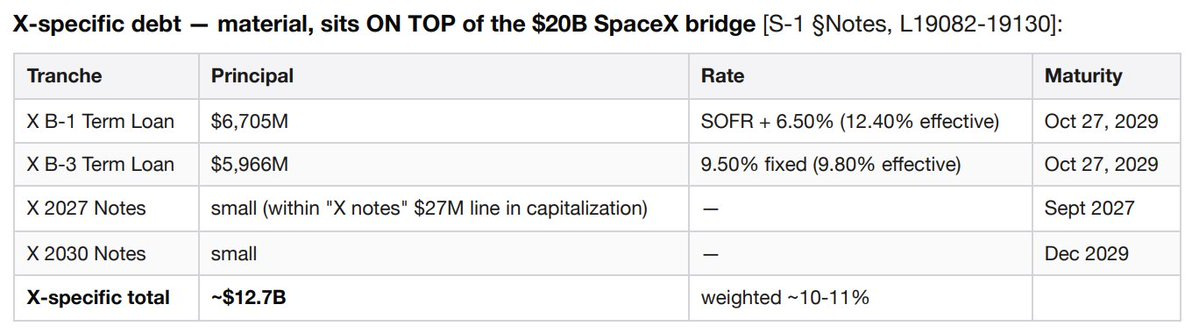

True debt burden is approximately $42 billion, not the headline figure of $29 billion. Breakdown: ~$20 billion SpaceX bridge loan (due September 2027), ~$6.7 billion X Corp B-1 term loan and ~$6 billion X Corp B-3 term loan (both due October 2029, effective interest rate 10-12%), and ~$9.1 billion in "other financing," including obligations from failed AI infrastructure sale-leasebacks. Interest expense on the X-related loans alone generates roughly $1.2-1.3 billion annually, booked under the AI division.

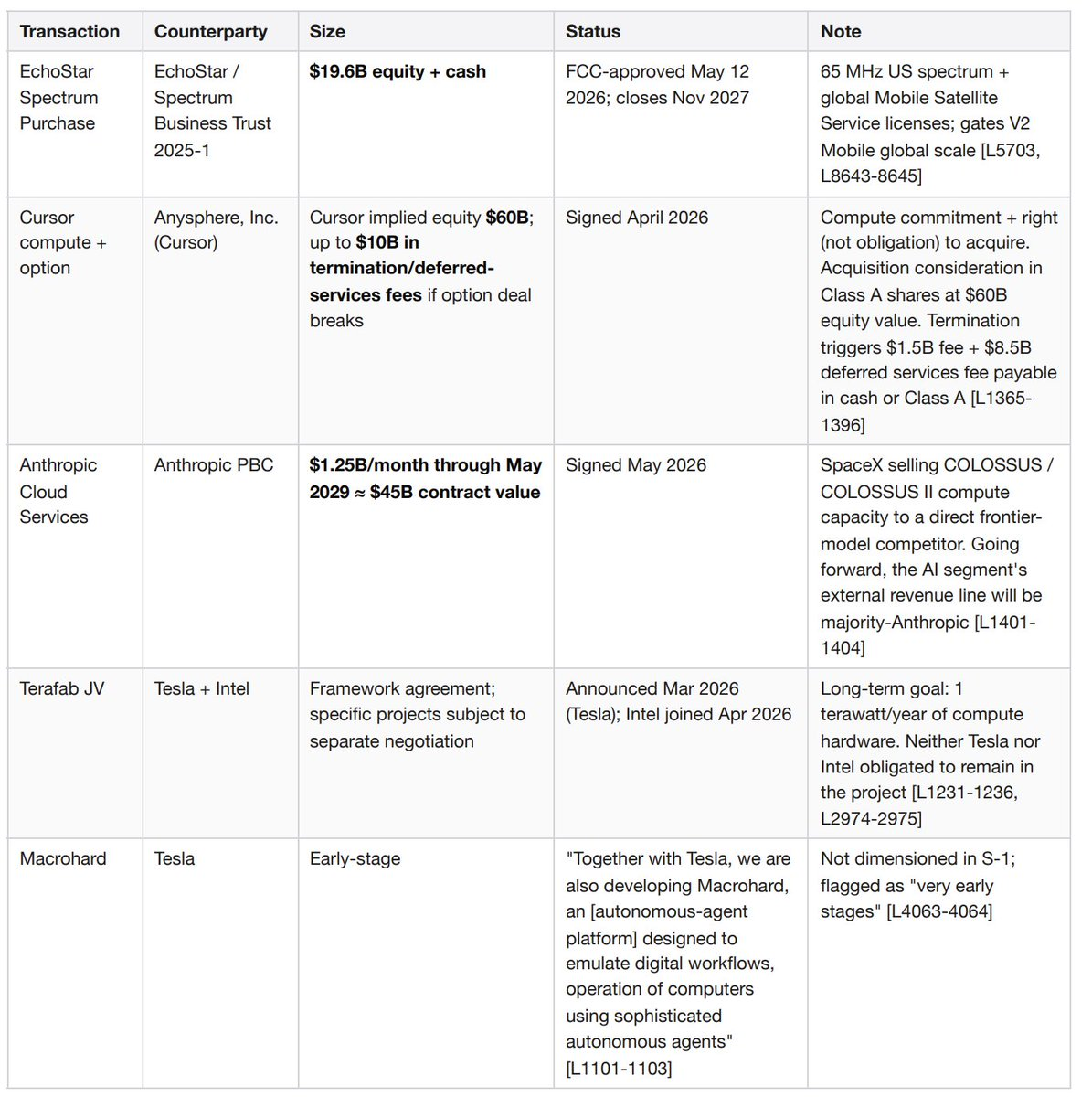

The $19.6 billion EchoStar spectrum commitment will close in November 2027. Consideration of equity and cash for 65MHz of US spectrum and global MSS licenses. This is a binding capital commitment on top of the bridge loan and FY2026 capex.

The option agreement with Cursor could trigger a termination fee of up to $10 billion. In April 2026—one month before this S-1 filing—SpaceX signed a compute and option agreement with Anysphere (Cursor), implying a $60 billion valuation for Cursor. If either party terminates, SpaceX must pay Cursor a $1.5 billion termination fee plus an $8.5 billion deferred service fee, payable in cash or Class A stock.

The $45 billion Anthropic contract is the single largest external revenue source for the AI division. A cloud services agreement signed in May 2026 requires Anthropic to pay $1.25 billion monthly until May 2029. SpaceX is selling its COLOSSUS compute power to a directly competing frontier model company, creating extreme counterparty concentration risk.

The balance sheet recognizes a $530 million litigation reserve for Grok image generation class actions—Jane Doe v. X.AI Corp. (January 2026), Jane Doe 1 (March), and Baltimore (March). Plaintiffs seek compensatory, statutory, and punitive damages. The S-1 explicitly states the range of additional losses is not estimable.

Q1 2026 revenue growth slowed to 15.4% ($4.69 billion vs $4.07 billion YoY), down from 33.2% for full-year 2025.

SpaceX will be a controlled company with four classes of equity. Musk will hold majority voting power post-IPO. The company will rely on Nasdaq's controlled company exemptions, foregoing requirements for independent compensation and nominating committees.

Adjusted EBITDA beautifies by approximately $9 billion. Management's 2025 headline figure is $6.6 billion in "adjusted EBITDA," while GAAP operating loss is -$2.6 billion. Adjustments exclude depreciation, stock-based compensation, and segment-specific exclusions.

Company Overview

SpaceX (Space Exploration Technologies Corp.; SEC CIK 0001181412) designs and operates reusable rockets, the world's largest LEO satellite constellation (~9,600 broadband satellites plus ~650 direct-to-cell satellites), and—following the February 2026 acquisition of xAI—gigawatt-scale AI training infrastructure. Three reportable segments: Space, Connectivity (10.3 million Starlink subscribers), and AI (Grok models, the X social platform with 550 million MAUs, and the COLOSSUS/COLOSSUS II compute clusters). 2025 revenue: $18.7 billion; GAAP operating loss: -$2.6 billion; Cash on hand: $15.85 billion versus $29.1 billion in long-term debt as listed on the cover of the capitalization table.

X (Social Platform) is a Business Unit, Not a Footnote

The corporate chain is worth retracing. SpaceX acquired xAI in February 2026. xAI acquired X Holdings in March 2025. X Holdings acquired Twitter in October 2022. Result: Twitter/X is now consolidated into SpaceX's AI segment, with its own balance sheet items, its own litigation, and its own debt structure.

Scale. Past 12 months supporting 1.3 billion accounts, 550 million MAUs (up from 520 million in December 2025), 350 million posts per day. Of these MAUs, 117 million use Grok features—X is the primary distribution channel for the model. Money products (payments, banking, financial services) launched in beta in November 2025 and are progressing towards general availability. X Ads Manager began phased rollout in April 2026.

Financial Contribution. The AI segment's 2023-2024 revenue was almost entirely from X—advertising, X Premium subscriptions, and data licensing. In 2024 alone, advertising revenue decreased $595 million YoY due to "X losing advertising partners," partially offset by a $157 million increase in X Premium subscription revenue and a $90 million increase in data licensing.

Add the $20 billion SpaceX bridge loan (September 2027) and the $9.1 billion "other financing" line item, and total long-term debt is approximately $42 billion—not the $29 billion headline figure on the capitalization cover.

X-specific risks SpaceX's other businesses don't have. EU Digital Services Act enforcement for VLOPs. Advertiser brand safety reversibility on short-term, cancellable ad contracts—the 2024 exodus could repeat within a single news cycle. Money products triggering payment/money transmission/banking regulation in all 50 US states and every foreign jurisdiction. Content moderation policy reversals could simultaneously trigger advertiser pauses and user migration.

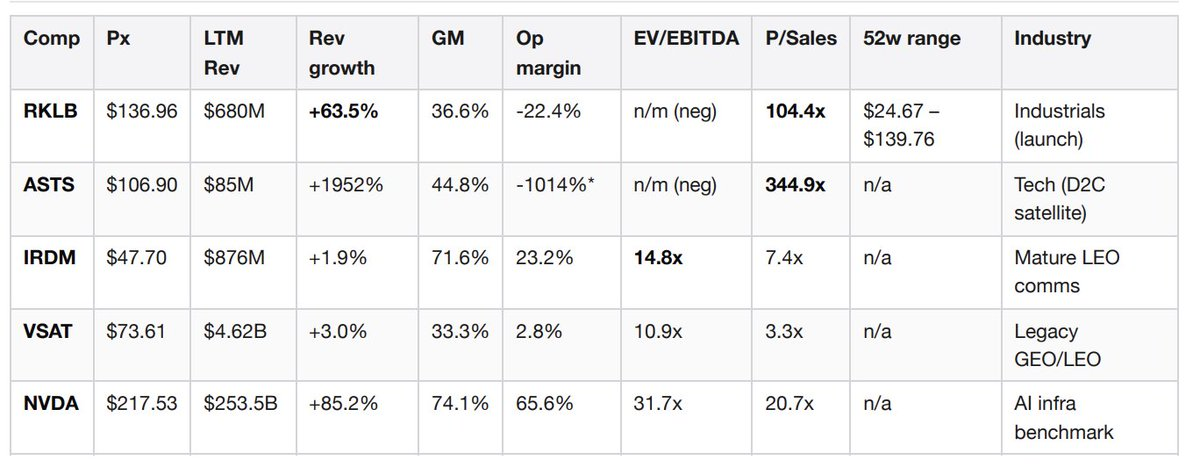

Market Position – Real-Time Comparable Data

This comparison table was assembled in real-time during the analysis, paying $0.10 to Jintel's GraphQL endpoint for batch fundamental data on all five comparable companies. No Bloomberg terminal, no FactSet contract needed.

ASTS operating margin reflects massive pre-revenue investment. Source: Jintel entitiesByTickers via x402 on Base chain, retrieved 2026-05-22.

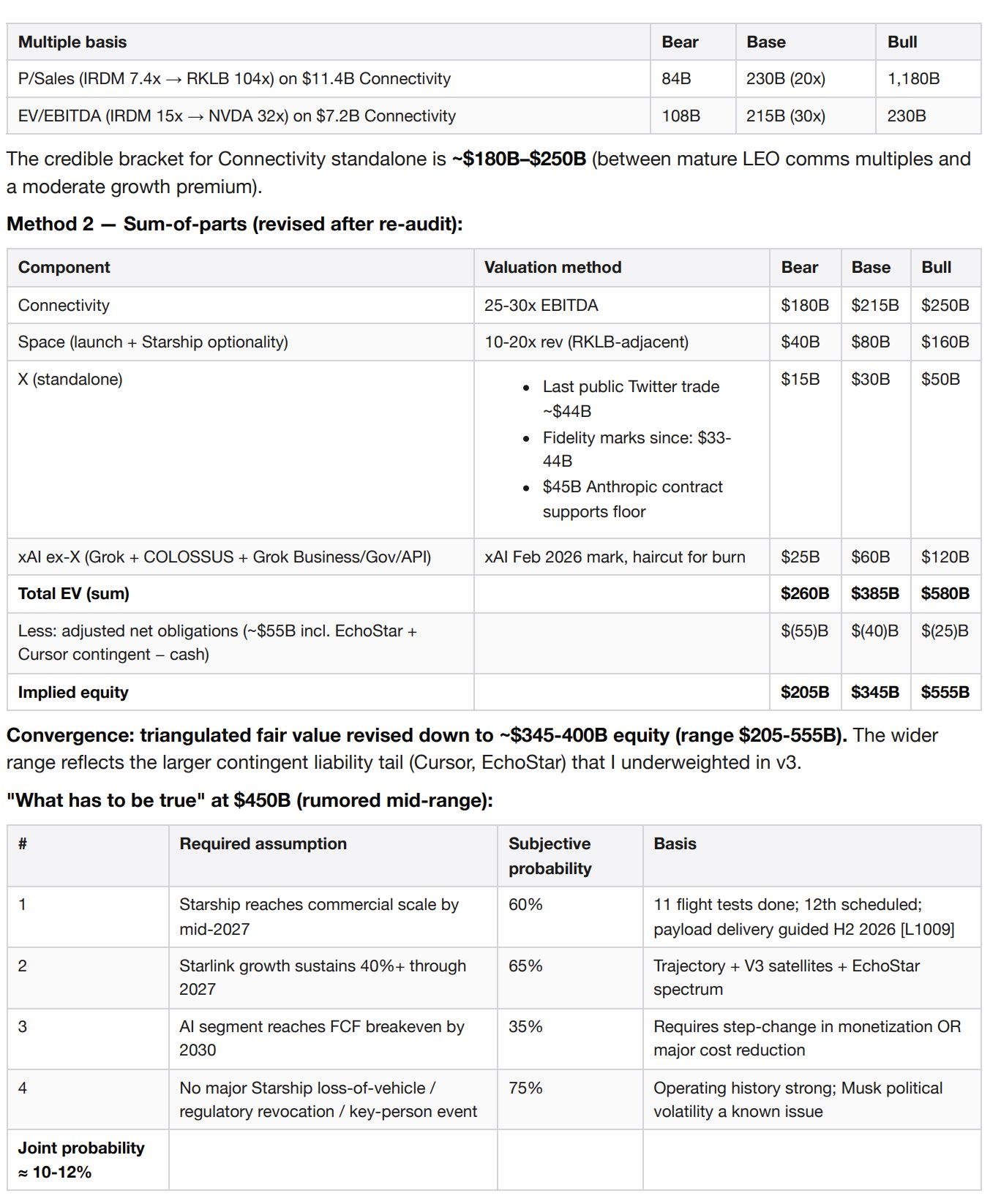

Reading the comp group. Rocket Lab's 104x price-to-sales is the closest narrative comp—investors are willing to pay extreme multiples for scalable reusable launch plus LEO option value, even with negative margins. SpaceX deserves a higher multiple than RKLB, but blindly applying 104x to SpaceX's $11.4 billion Connectivity revenue alone implies a $1.2 trillion equity value, which cannot be anchored to anything. AST SpaceMobile's 345x is purely pre-revenue narrative valuation, useful only as an upper bound for direct-to-cell optionality. Iridium's 7.4x sales and 14.8x EBITDA represent what mature, profitable LEO communications looks like—applying 7.4x to Starlink's $11.4 billion yields an $84 billion Starlink standalone value (bearish anchor). NVIDIA's 31.7x EV/EBITDA corresponds to 85% revenue growth, which is the level the AI segment needs to grow into to justify a fundamentals-based valuation. It's not there yet.

Notable signal. Rocket Lab filed a 424B5 prospectus supplement on May 20, 2026—the same day SpaceX filed its S-1. RKLB issuing secondary equity into the SpaceX news cycle suggests management believes the IPO window is open and competitive supply pressure is imminent.

Pending Material Transactions and Contingent Obligations

Each of these four is individually material and stack on top of each other. Two were signed within 60 days of this S-1 filing.

Why this matters for valuation. A clear "adjusted net obligations" view: $42 billion total debt + $19.6 billion EchoStar commitment + up to $10 billion Cursor contingent liability, minus $15.85 billion cash on hand, equals approximately $55 billion in net obligations, before accounting for any IPO proceeds. This is three to four times the number from a simple read of the capitalization cover page and materially changes the bear case.

Valuation

Method 1 – Based on Connectivity segment standalone trading multiple, as it is the only segment with positive standalone economics.

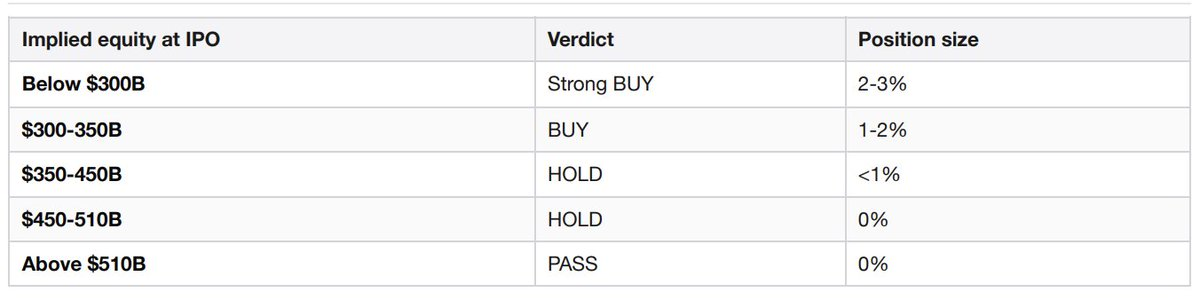

Position Sizing Ladder

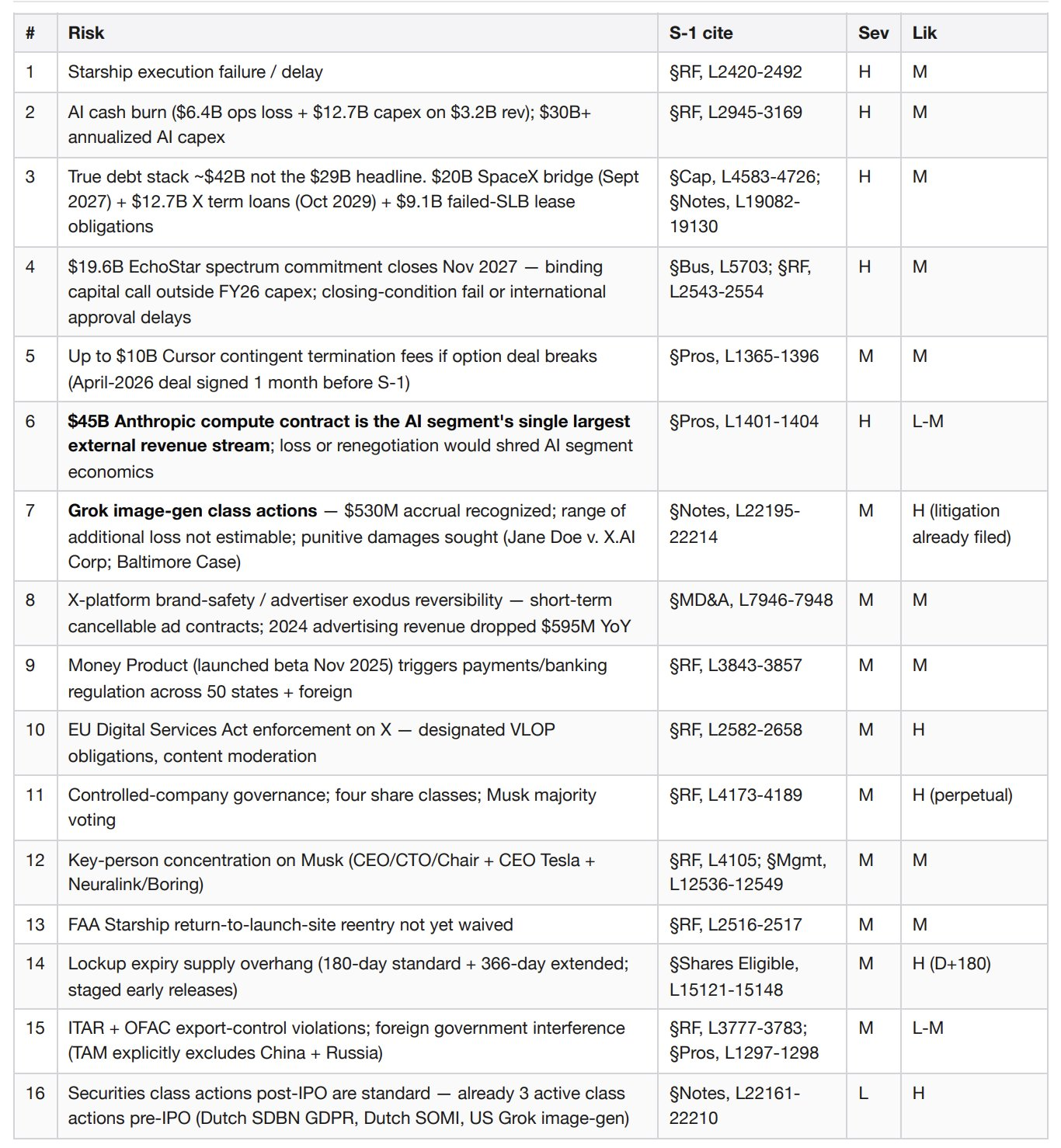

Key Risks (Severity × Likelihood)

Underwriter Conflicts of Interest

This is buried deep in the underwriting section, rarely covered by news, but it is material. Affiliates of the five lead underwriters (Goldman Sachs, Morgan Stanley, Bank of America, Citigroup, JPMorgan) plus five additional bookrunners (Barclays, Deutsche Bank, RBC, UBS, Wells Fargo) are all lenders on the $20 billion SpaceX bridge loan, and they are now pricing the IPO used to refinance that loan. Morgan Stanley additionally advised SpaceX on the acquisition of xAI (which the bridge loan financed). The syndicate has a direct financial interest in maximizing the IPO raise amount. This should keep the investment committee vigilant on pricing discipline.

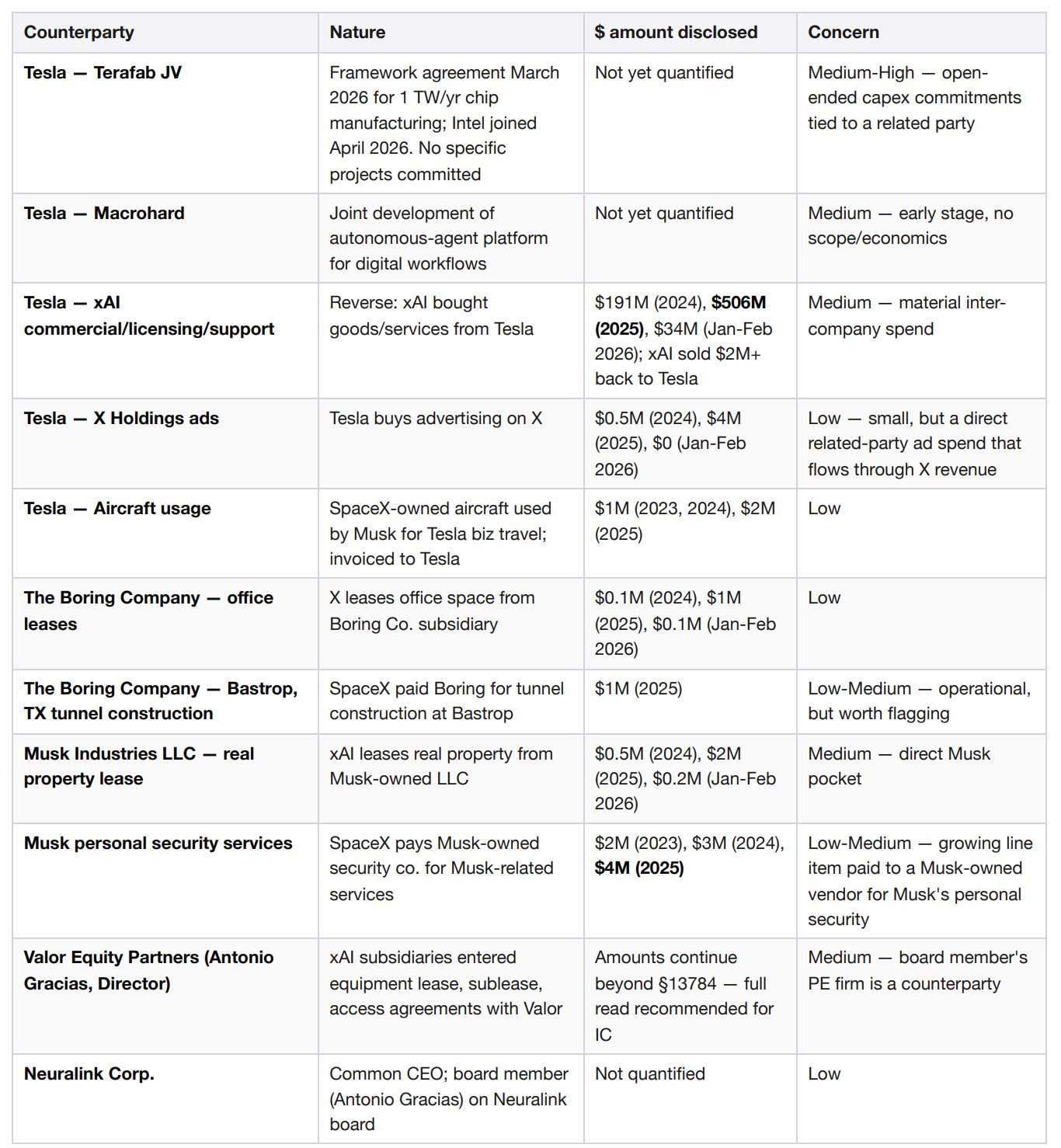

Related Party Density

No single item is alarming on its own. What is alarming is the density—Musk-controlled entities have at least nine distinct financial touchpoints with SpaceX. A public company governance committee would typically review one or two such relationships. Here, there is an order of magnitude more.

Decision Triggers

Upgrade to Overweight if the deal prices at an implied equity value of $350 billion or below, and Starship achieves commercial payload delivery per guidance in H2 2026, and Q2 2026 Connectivity revenue growth exceeds 40% YoY.

Downgrade to Avoid if the deal prices above $510 billion, or Starship suffers a vehicle loss event delaying V3 satellite deployment beyond 2027, or the AI division's cash burn accelerates to an annualized operating loss exceeding $8 billion in Q2-Q3 2026, or the FAA imposes a long-term grounding order on Starship.

First 180 Days + Multi-Year Watchlist

D+1: First-day performance benchmark against comparable IPOs

D+30: First quarterly earnings (Q2 2026) – triggers early release lock-up tranche (20% immediate release, additional 10% if stock is +30% above offer price)

D+70, +90, +