45 ngày vốn hóa giảm một nửa, Circle thực chất là 'Phong vũ biểu DeFi'?

- Quan điểm cốt lõi: Lưu thông USDC giảm đồng bộ với giá cổ phiếu Circle, cho thấy nó phụ thuộc nhiều vào hoạt động DeFi, chứ không phải nhu cầu thanh toán thực tế; ngược lại, USDT nhờ được hỗ trợ bởi các trường hợp sử dụng thực tế như kinh tế ngầm, lương xuyên biên giới, mức độ thu hẹp thị trường thấp hơn.

- Các yếu tố then chốt:

- Lưu thông USDC giảm xuống còn 73,6 tỷ, giảm khoảng 7 tỷ USD (khoảng 8,7%) so với mức đỉnh; cùng kỳ, USDT chỉ giảm 4,7 tỷ (khoảng 2,5%), cho thấy khả năng chống chịu tốt hơn.

- Giá cổ phiếu Circle từng giảm một nửa xuống còn 63 USD, trùng với thời điểm xảy ra các sự kiện bảo mật DeFi (như Kelp DAO bị tấn công) và TVL sụt giảm, các nhà phân tích gọi nó là 'phong vũ biểu của hoạt động DeFi'.

- 75% USDC lưu chuyển trong các sàn giao dịch và giao thức DeFi, chứ không dùng cho tiêu dùng hàng ngày; trên Ethereum, 100 địa chỉ hàng đầu nắm giữ hơn 50% USDC, mức độ tập trung cực kỳ cao.

- USDC cùng với Coinbase thúc đẩy trở thành stablecoin thanh toán của Hyperliquid, nhưng phải nhường 90% lợi nhuận từ dự trữ, phản ánh sự bất đắc dĩ khi phải tự tìm kiếm tăng trưởng sau khi DeFi thu hẹp.

- 'Khối lượng chuyển hữu cơ' của USDC trong năm 2025 đạt 18,3 nghìn tỷ, cao hơn 13,2 nghìn tỷ của USDT, nhưng tăng trưởng khối lượng phát hành thực tế vẫn phụ thuộc vào hoạt động đầu cơ trên chuỗi, chứ không phải thanh toán thực tế.

Original Author: Eric, Foresight News

In June 2026, Circle's seemingly promising rebound story came to an abrupt halt. As of June 25th local time in the US, USDC's circulating supply had dropped to 73.6 billion, down approximately $7 billion from its peak, while Circle's stock price also halved to around $63.

On the surface, $7 billion is less than 10% of the $80 billion mark. However, for comparison, USDT's circulating supply once peaked at around $191 billion and currently stands at approximately $186.3 billion, a decrease of only $4.7 billion, representing a reduction of less than 3%.

While there is no direct evidence proving a causal link between the decline in USDC's circulating supply and Circle's falling stock price, the simultaneity of these events, coupled with the coincidence of prior DeFi security incidents and the timing of Circle's stock price decline, inadvertently validated a point made by Compass Point analyst Ed Engel back in January:

Circle is a barometer of DeFi activity.

Engel argued at the time that Circle's trading behavior resembles cyclical stocks. From October 2025 to January 2026, the correlation coefficient between USDC's circulating supply curve and ETH's price trend reached 0.66. The core reason is that 75% of USDC circulates within cryptocurrency exchanges, DeFi protocols, and similar environments. The amount of USDC actually used for everyday consumption, cross-border payments, and other real-world applications is far lower than commonly perceived.

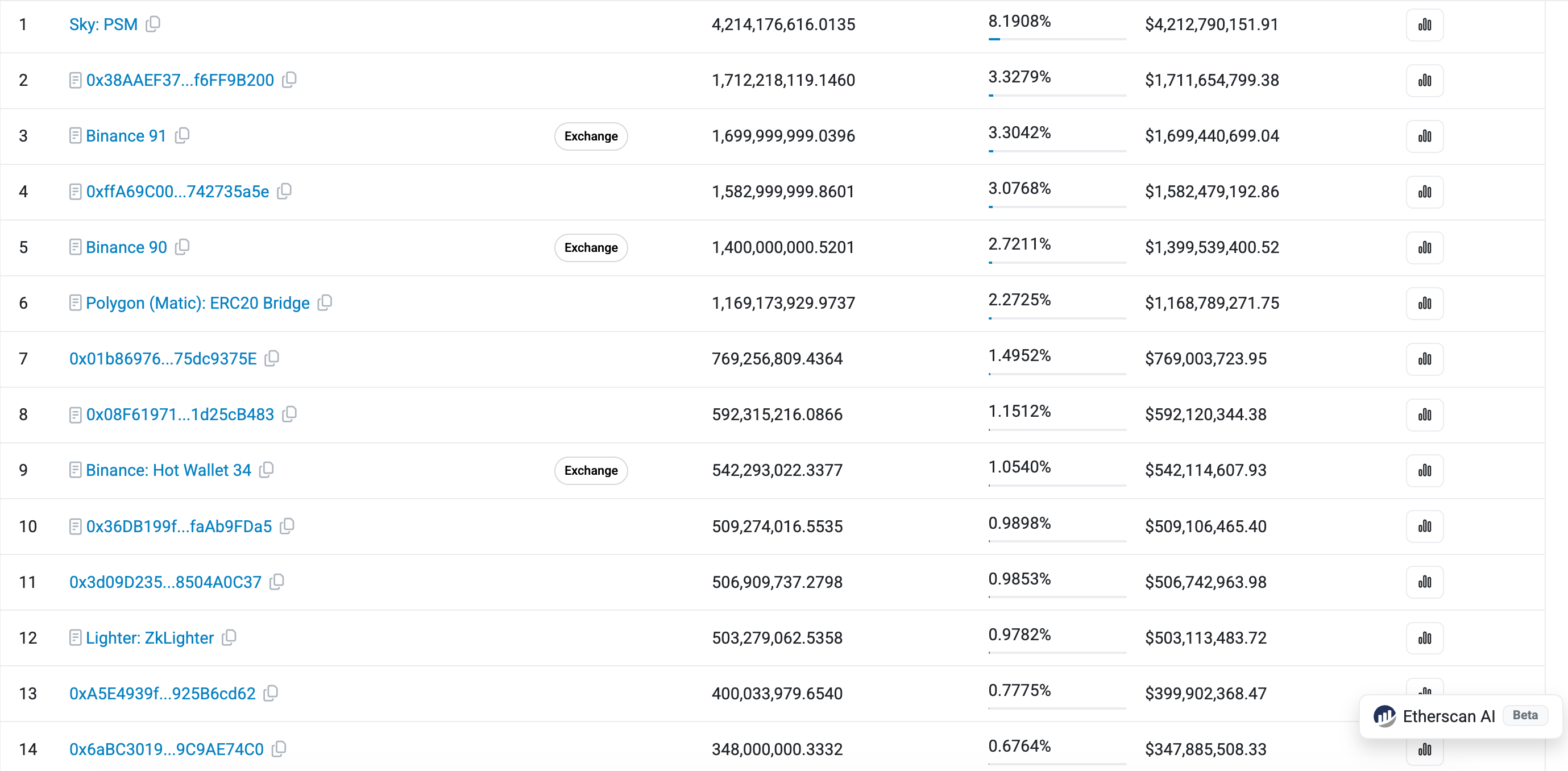

Looking at the top USDC holder addresses on Etherscan reveals a large number of contract addresses on the first page. These USDC tokens reside in DeFi protocols, exchange multi-signature wallets, cross-chain bridges, and other smart contracts or addresses. Furthermore, the top 100 USDC holding addresses on Ethereum control over 50% of the total supply; just 0.32% of addresses hold 93.55% of the entire supply. A vast amount of USDC is parked in protocols to earn yields higher than traditional bank deposits.

This level of data concentration is hardly fitting for a "digital dollar" intended for daily circulation. You might counter by pointing out USDT's even higher concentration on Ethereum, but USDT has very established real-world use cases. The Web3 industry uses USDT for payroll, international trade is settled with USDT, grey and black market actors use it to evade regulation, and individuals in third-world countries leverage it to protect their savings.

Although perhaps less "glamorous" than USDC, these scenarios form USDT's fundamental base. Consequently, USDT – the stablecoin most used as a cryptocurrency trading pair – has shrunk less than the more compliant USDC during this bearish market. News today showing that USDT commands an 8% premium in India compared to its standard price further corroborates this point.

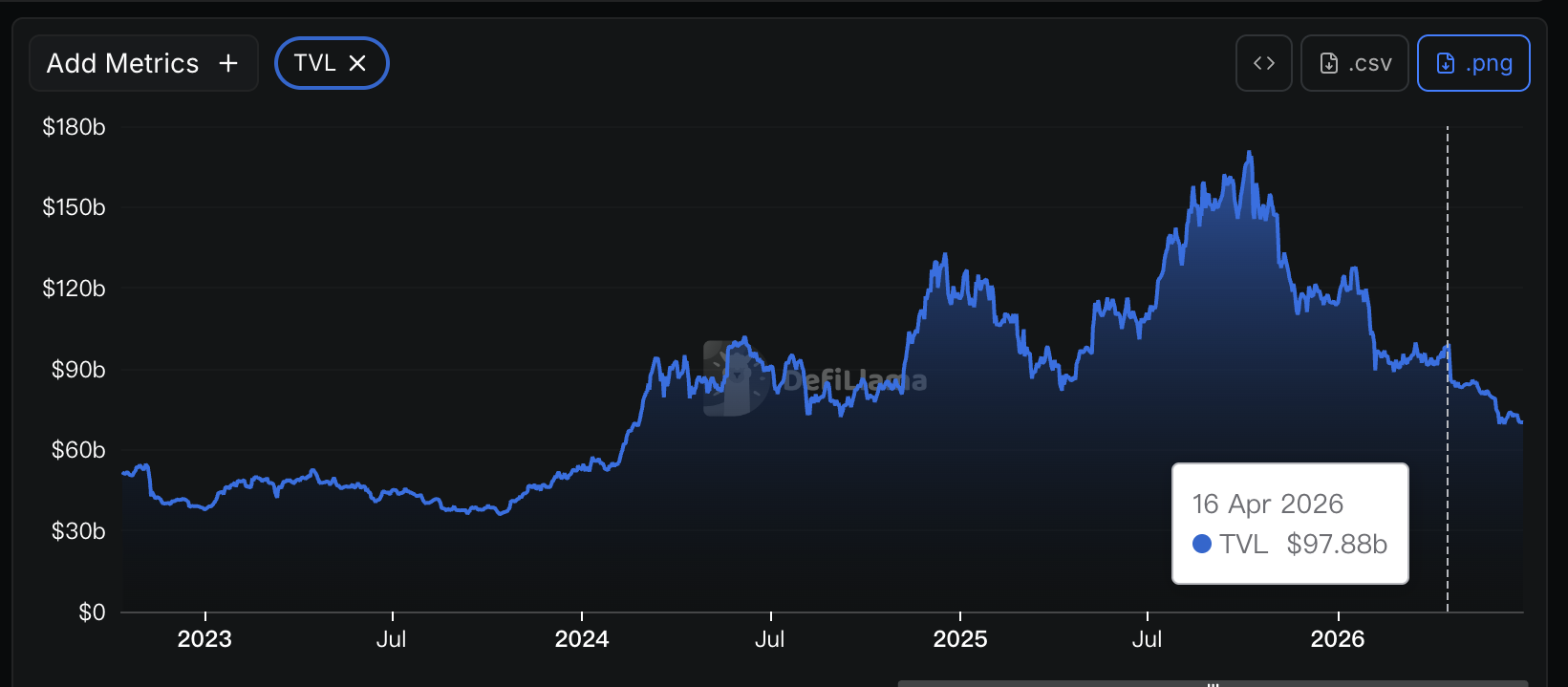

DeFi's overall Total Value Locked (TVL) began declining in mid-April, coinciding with the Kelp DAO attack incident. Circle's stock price started falling in mid-May. Although the decline started at different times, the subsequent trajectories were broadly similar.

Just last month, Circle partnered with Coinbase to push USDC into the position of Hyperliquid's settlement stablecoin. The price tag included not only staking 500,000 HYPE tokens each but also relinquishing 90% of the earnings generated from the reserve assets backing USDC on Hyperliquid. Behind this seemingly "win-win-win" situation lies Circle's underlying predicament: its primary battleground, DeFi, is rapidly contracting. The Kelp DAO incident severely damaged DeFi's credibility. Waiting for organic DeFi activity to naturally boost USDC supply has hit a bottleneck, forcing Circle to take matters into its own hands.

If you look closely, you'll notice USDC is not only the settlement asset for Hyperliquid but also for platforms like Lighter. Beyond the cryptocurrency realm, Circle is tirelessly promoting USDC to be "used like the US dollar." According to Artemis data, USDC's "organic transfer volume" (excluding wash trading, high-frequency trading, exchange wallet consolidation, etc.) was $18.3 trillion in 2025, compared to USDT's $13.2 trillion.

It's undeniable that USDC is widely used in institutional and compliant payment scenarios. However, the amount of USDC required for these uses isn't as high as one might think. Funds may not always circulate as USDC; instead, USDC acts as an "intermediate state," reducing the time and capital costs associated with transfers between banks or financial institutions.

In other words, adding another 10 billion USDC might correspond to trillions of dollars in actual real-world fund flows, but on-chain, it could simply be driven by a few large DeFi protocols, meme coin trading platforms, or prediction markets. No matter how fast USDC circulates or how high its utilization rate is in the real world, if its overall issuance doesn't increase, revenues and profits won't grow either.

Of course, none of this is a death sentence for Circle. If Circle can eventually reduce its dependency on DeFi, or demonstrate that real-world usage significantly drives USDC issuance growth, then Circle's investment narrative could be rewritten. However, in the short term, the key focus may remain on whether DeFi can break free from the "unbalanced risk-reward" shackles and restore greater confidence to the market.