AI cơ sở hạ tầng ba đường dây, ai tăng trước, ai mạnh nhất, ai còn có thể theo kịp?

- Quan điểm cốt lõi: Sự bùng nổ của ngành công nghiệp AI thể hiện một chuỗi truyền dẫn rõ ràng: đầu tiên có lợi cho chip (nhu cầu tính toán cơ bản), tiếp theo là lộ ra nút thắt năng lượng (trung tâm dữ liệu tiêu thụ điện cao), và cuối cùng là nâng cao nhu cầu lưu trữ trong dài hạn (hệ thống AI liên tục xử lý dữ liệu). Logic này đã được xác nhận rõ rệt qua mức tăng trưởng của các tài sản liên quan trên thị trường chứng khoán Mỹ và A trong năm qua.

- Các yếu tố then chốt:

- Lớp chip: Nhu cầu AI đầu tiên chuyển thành đơn đặt hàng GPU (NVIDIA), HBM và quy trình sản xuất tiên tiến. Doanh thu năm tài chính 2026 của NVIDIA dự kiến tăng 65% so với cùng kỳ, các thiết bị (ASML, Lam Research) đã tăng 27%-30% kể từ đầu năm.

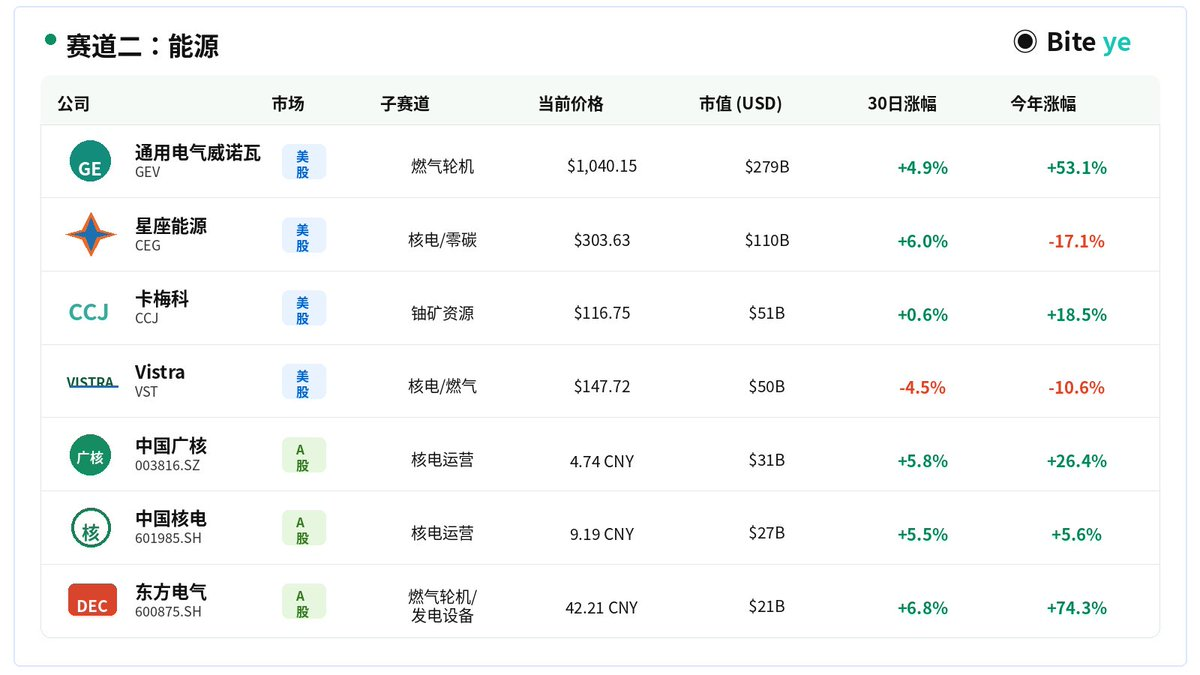

- Lớp năng lượng: Công suất một tủ của trung tâm dữ liệu AI tăng lên 50-100 kilowatt (truyền thống là 5-15 kilowatt). IEA dự đoán đến năm 2030, điện năng tiêu thụ của trung tâm dữ liệu sẽ đạt 945 TWh, tăng gấp đôi, thúc đẩy việc định giá lại các tài sản như tuabin khí (GE Vernova, tăng 167% trong năm) và các nhà vận hành điện hạt nhân.

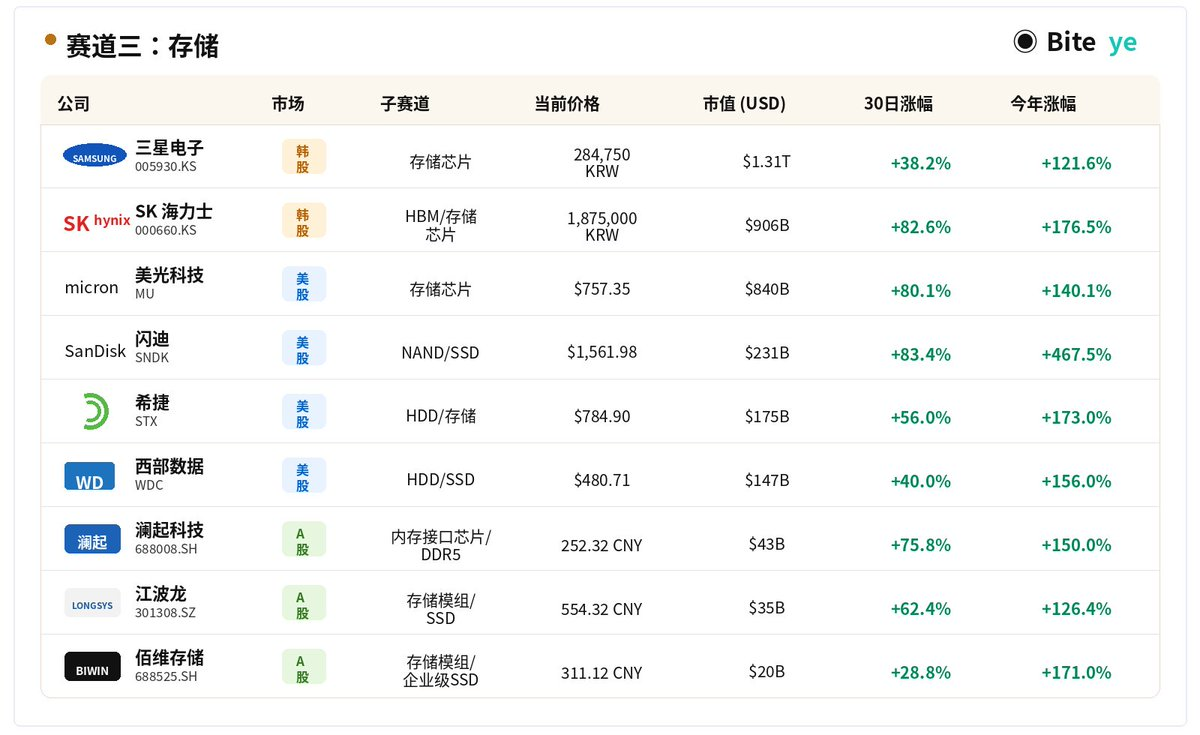

- Lớp lưu trữ: AI tạo ra áp lực đọc/ghi dữ liệu thường xuyên, gọi tức thời và bộ nhớ cache. Các nhà sản xuất chip lưu trữ gốc (doanh thu quý 1 của SK Hynix tăng 198%, lợi nhuận tăng 406%) và các nhà sản xuất HDD (SanDisk tăng 350% trong năm) có hiệu suất nổi bật.

- Ba đường dây chip, năng lượng và lưu trữ được Justin Sun đề cập trong bài đăng hồi tháng 11 năm ngoái, nếu mua các cổ phiếu khái niệm lưu trữ Mỹ như Micron, SanDisk vào thời điểm đó, đến nay mức tăng đã đạt 180%-552%.

- Về tài sản trong nước, doanh thu năm 2024 của Haiguang Information đạt 9,162 tỷ NDT, tăng 52,4% so với cùng kỳ. Các doanh nghiệp thiết kế chip tính toán và lưu trữ nội địa (GigaDevice, Puya Semiconductor, v.v.) cũng được hưởng lợi đồng thời.

Original Author: Changan I Biteye Content Team

In November last year, Justin Sun posted a tweet:

If we treat this statement as an industry judgment rather than a catchy phrase, looking back now reveals:

These three lines are almost the real profit path of the AI market trend.

If, after that tweet came out, someone bought US-listed storage concept stocks, what would the result be today?

• Micron: +214%

• Seagate: +180%

• Western Digital: +190%

• SanDisk: +552%

This article breaks down along these three lines:

Why does AI first benefit chips, then create an energy bottleneck, and finally drive long-term storage demand? Which assets have already emerged in this structure?

I. Chips: The First Thing AI Boom Delivers is Not Narratives, but Orders

What AI burns first is not the application layer, but the underlying computing power.

Whether it's training large models, daily inference, agent calls, or multimodal processing, the first step is to get the computing running. And all this computing ultimately relies on GPUs, HBM, high-speed interconnects, and advanced manufacturing processes.

In other words, the growth in AI demand doesn't first trickle down to the later stages. Instead, it translates into a more immediate reality:

Need more chips, need stronger chips, need higher bandwidth chips.

This is why AI demand is first reflected in the chip sector.

Industry data already makes this very clear. Based on the fiscal year 2026, NVIDIA's revenue grew 65% year-over-year, indicating that demand for high-end computing chips continues to be released.

🌟Assets in this Direction

Core Computing Layer: NVIDIA (NVDA), AMD, Broadcom (AVGO), TSMC (TSM)

Domestic Computing Layer: Haiguang Information (688041.SH), Cambricon Technologies (688256.SH), etc. Haiguang Information is one of the representative domestic x86 server CPU companies, with 2024 revenue of 9.162 billion yuan, up 52.4% year-over-year.

Semiconductor Equipment Layer: ASML, Applied Materials (AMAT), Lam Research (LRCX). The ADR price of lithography giant ASML hit an all-time high at the start of 2026, surging over 8% on January 2nd, gaining 27% since the start of 2026. Lam Research has gained 30% year-to-date, and Applied Materials has gained 28% year-to-date. All three major semiconductor equipment giants have significantly outperformed the S&P 500 index.

🌟Performance Over the Past Year

The chip sector was the earliest to launch and has seen the largest gains in this AI wave. NVIDIA, as the leader, has accumulated gains of over 1000% since early 2023. Equipment makers continued to hit new highs in early 2026, and the overall sector remains in a strong upward cycle. Citigroup released a research report predicting that the global semiconductor equipment sector will enter a "Phase 2 bull market upcycle," with the main chip stock narrative in 2026 clearly focused on ASML, Lam Research, and Applied Materials.

II. Energy: After AI Scales Up, the Bottleneck Shifts from Chips to Electricity

No matter how many chips you have, they won't run without power.

Buying chips is just the beginning. The long-term operation of large models, data centers, and inference services requires continuous power supply and additional cooling loads. Traditional data center racks typically consume 5 to 15 kW, while AI data centers have significantly raised this to 50 to 100 kW, making the power consumption and heat dissipation pressures entirely different scales. An IEA analysis this year mentioned that data center electricity consumption could reach about 945 TWh by 2030, roughly doubling from current levels, with AI being the primary driver. The US Department of Energy has also explicitly stated that the growing power demand from data centers is putting significant pressure on regional grids.

🌟Assets in this Direction

Gas Turbines: GE Vernova (GEV): Gas turbine orders are booming, totaling $59 billion for the full year 2025, with a backlog growing to $150 billion. Management raised the 2026 revenue guidance to $44-$45 billion.

Independent Power Producers: Constellation Energy (CEG): The largest zero-carbon power operator in the US, with nuclear assets directly signing long-term Power Purchase Agreements (PPAs) with tech giants. Vistra (VST): Holds both nuclear and gas assets, with the midpoint of its 2026 EBITDA guidance up approximately 30% from 2025.

Uranium Resources: Cameco (CCJ): The world's largest publicly traded uranium miner, a beneficiary of nuclear restart upstream.

🌟Performance Over the Past Year

GE Vernova's stock price rose 167% over the past year. Its 52-week low was $408, and it hit a high of $1181, nearly doubling from the low. Constellation Energy hit an all-time high in 2025 but then corrected about 28% from its peak due to regulatory policy disruptions, currently trading at a relatively lower level. Vistra remained strong overall, with long-term power supply contracts with data centers continuously being signed. The energy sector, in general, has repriced from a traditional defensive position to a core beneficiary of AI infrastructure.

III. Storage: The Most Easily Overlooked, but Long-Term Beneficiary Direction

The core logic favoring storage is simple: AI is not a one-time call; it is essentially a system that continuously consumes, stores, and retrieves data.

Training requires reading vast amounts of data, saving checkpoints during the process, inference requires loading models and cache, and RAG and Agents constantly access knowledge bases, logs, and memory.

Consequently, AI brings not just "more data," but:

• More frequent data reads and writes

• More real-time data calls

• More complex data management

• Greater pressure on data migration and caching

Looking deeper, the more expensive the GPU, the less it can be idle. So the industry will increasingly focus on how to deliver data faster and more stably to the computing endpoint.

In other words, the more AI develops, the more storage becomes not just a "data warehouse," but the data foundation ensuring the entire AI system runs continuously.

🌟Assets in this Direction

Memory Chip Manufacturers: SK Hynix (000660.KS), Samsung Electronics (005930.KS), Micron Technology (MU)

NAND / SSD / HDD Vendors: SanDisk (SNDK), Seagate (STX), Western Digital (WDC)

Domestic Storage Design: GigaDevice, Puya Semiconductor, ESMT, Ingenic Semiconductor, Montage Technology, and storage module makers like Longsys, Netac Technology, Biwin Storage, etc.

🌟Performance Over the Past Year

Since the beginning of 2026, the storage sector has been one of the strongest branches in the AI industry chain. In the US market, driven by AI infrastructure investment and high-capacity storage demand, Seagate, SanDisk, and Western Digital have all surged significantly this year. Reuters mentioned in late April that Seagate and Western Digital have more than doubled year-to-date, while SanDisk has surged about 350%. Memory chip manufacturers also strengthened in sync. Micron has risen sharply this year, while SK Hynix continues to benefit from the HBM shortage and capacity grabs by major players, reporting Q1 revenue up 198% year-over-year and operating profit up 406%, further strengthening profitability.

Final Thoughts: Chips Rallied First, Energy Followed as a Bottleneck, Storage Comes Last

The first payoff from AI is chips; the second bottleneck is energy; the third long-term beneficiary is storage.

Correct logic doesn't always mean a comfortable entry point. There are structural opportunities, but this isn't about blindly chasing highs.

What's truly valuable isn't the hype itself, but which layer of the industry chain you're positioned on.

Disclaimer: The above is merely an industry chain review and does not constitute investment advice. Especially since some targets have seen very exaggerated gains since the beginning of 2026, a correct logic does not equate to a comfortable entry point.