复盘美伊迷局四大正确预测案例:公开信息中的端倪

- 核心观点:本文通过分析Polymarket上美伊冲突预测市场的四个典型交易账户,揭示了在地缘政治高度不确定的时刻,通过系统性押注“降级”、“持续僵局”或“小概率事件”,可以获取高额回报,其背后逻辑是市场情绪往往高估了重大短期变革的概率。

- 关键要素:

- 案例一:全仓押停火,单日回报3,503%。账户以2.8美分均价买入“4月7日前停火”合约,利用极端赔率博弈,在停火宣布后获利45万美元,体现了“方向性押注”和“批量覆盖小概率事件”的策略。

- 案例二:连续亏损后全中,获利51万美元。账户在战争爆发前连续押注“美国会打伊朗”21次,亏损3.9万美元后,最终在2月28日空袭当天押中,单日回报684%,其策略是基于对地缘政治“最终会发生”的强判断,并通过“时间窗口全覆盖”执行。

- 案例三:大资本押注“什么都不会发生”,获利14.7万美元。账户投入210万美元,系统性购买所有重大合约的“No”选项,押注“永久和平”等事件不可能在短期内实现,捕捉市场因乐观情绪产生的“溢价”,核心策略是“利用时间不足”进行套利。

- 案例四:高频交易做空市场恐慌,盈利29.2万美元。账户通过2,000笔交易,持续识别因恐慌情绪被高估的“Yes”合约并做空,利用地缘政治市场“渐进僵局”被低估、而“重大变化”被高估的规律,实现稳定盈利。

- 共同启示:所有成功账户的核心逻辑并非预测具体日期或事件,而是利用市场情绪偏差。在低流动性合约中,市场定价系统性低估了地缘政治突发转折的概率(如停火)或高估了短期剧变的概率(如政权倒台)。

Original by Odaily (@OdailyChina)

Author: jk

On February 28, 2026, a joint US-Israel airstrike on Iran had already begun. This was less than two hours after Trump posted that 8-minute video on Truth Social, and Khamenei's death had not yet been officially acknowledged by Tehran.

But on Polymarket, the contract "Will the US strike Iran before February 2026?" was already trading at $0.98.

From February 28 to April 30, Polymarket contracts centered on the US-Iran conflict generated over $300 million in trading volume. During this period, the market experienced multiple high-volatility inflection points: the outbreak of war, the blockade of Hormuz, the announcement of a ceasefire, the breakdown of the ceasefire, and its extension. Each major event was accompanied by a sharp repricing of contract values.

In this article, Odaily breaks down 4 accounts that achieved significant profits during this period, focusing on one core question: What did the public information environment look like at the time they placed their bets, and was their judgment justifiable based on available data?

Case Study 1: All-In on Ceasefire, 3,503% in One Day, Over $450,000 Profit

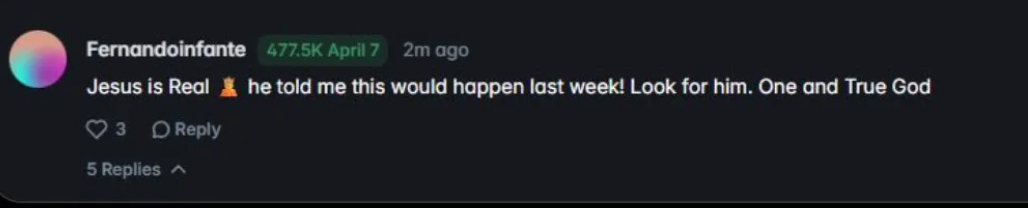

Account: Fernandoinfante

On April 7, Trump announced a US-Iran ceasefire on Truth Social. The contract "Will the US and Iran ceasefire before April 7?" jumped from single digits to nearly $1. The beneficiary of this trade was Fernandoinfante, who had previously purchased 477,543 Yes contracts at an average price of 2.8 cents, for a total cost of $13,200.

Single trade return: 3,503%, liquidated that day, profit of $450,000, equivalent to over 3 million RMB.

Before April 7, public information on ceasefire negotiations looked like this: On April 5, Pakistan proposed a two-week ceasefire draft, which Iran formally rejected and countered with a 10-point plan, including conditions such as troop withdrawal, reparations, and full lifting of sanctions. On April 6, Trump threatened to expand strikes to power grids and bridges, but then delayed for 5 days, stating "negotiations are ongoing." Early morning on April 7, the market's consensus price for a ceasefire was still extremely low. 2.8¢ implies the market thought the probability of reaching a ceasefire that day was less than 3%.

From a public information standpoint, Iran had just rejected the Pakistani draft, Trump was threatening more bombings, there were no formal negotiation channels, and Hormuz remained blocked. No mainstream media outlet reported that a ceasefire was imminent on the evening of April 6.

What was the basis for this judgment?

First, information asymmetry. Polysights pointed out on Twitter that this trade was placed two days before the ceasefire announcement. If true, the purchase time would be around April 5, when Trump had already begun to soften his rhetoric (delaying the attack on power grids by 5 days) and the Pakistani mediation channel was still open. Some Washington observers around April 5-6 had started discussing that "Trump needs a result." A trader consistently tracking negotiation channels might have been able to act faster than the market pricing based on Pakistani diplomatic moves, but this still requires extremely strong information acquisition capabilities or insider access.

Second, extreme odds gambling. At a price of 2.8¢, even if the probability of a ceasefire was only 10%, this still represented a positive expected value bet. The trader's strategy was: in the final stages of a geopolitical contract, systematically buy all cheap Yes contracts, covering multiple expiration dates with small capital, waiting for one of them to trigger.

Fernandoinfante also had other failed trades (e.g., predicting the Strait of Hormuz would normalize, a permanent peace agreement would be reached, the Iranian regime would collapse – all failed), reinforcing this logic. He was betting on multiple directions simultaneously; the ceasefire was just one that happened to hit.

Of course, his own explanation is "Jesus told him."

He claims he was divinely inspired

So, is there anything to learn?

This person wasn't betting on a single specific outcome, but rather on the broad direction of "conflict de-escalation in some way." He bought contracts for ceasefire, permanent peace, Hormuz normalization, and regime collapse, executing a diversified directional bet.

Ultimately, only the ceasefire event paid off; the others all lost money. But one 3,500% return was enough to cover all losses and generate hundreds of thousands of dollars in net profit.

The logic of this structure is that in low-liquidity tail-risk contracts, the market systematically underestimates the probability of sudden geopolitical turns. When the probability of an event is priced at 2-3%, but the actual probability might be 10-15%, buying a batch of such contracts is rational in expected value terms, even if most will go to zero.

Case Study 2: Consecutive Losses, Then Hitting the Jackpot on the Last Day: The "Steadfast Conviction" Strategy

Account: Vivaldi007

Vivaldi007 registered on Polymarket in February 2026, less than three weeks before the geopolitical conflict erupted. From day one of registration, he did only one thing: bet that the US would strike Iran.

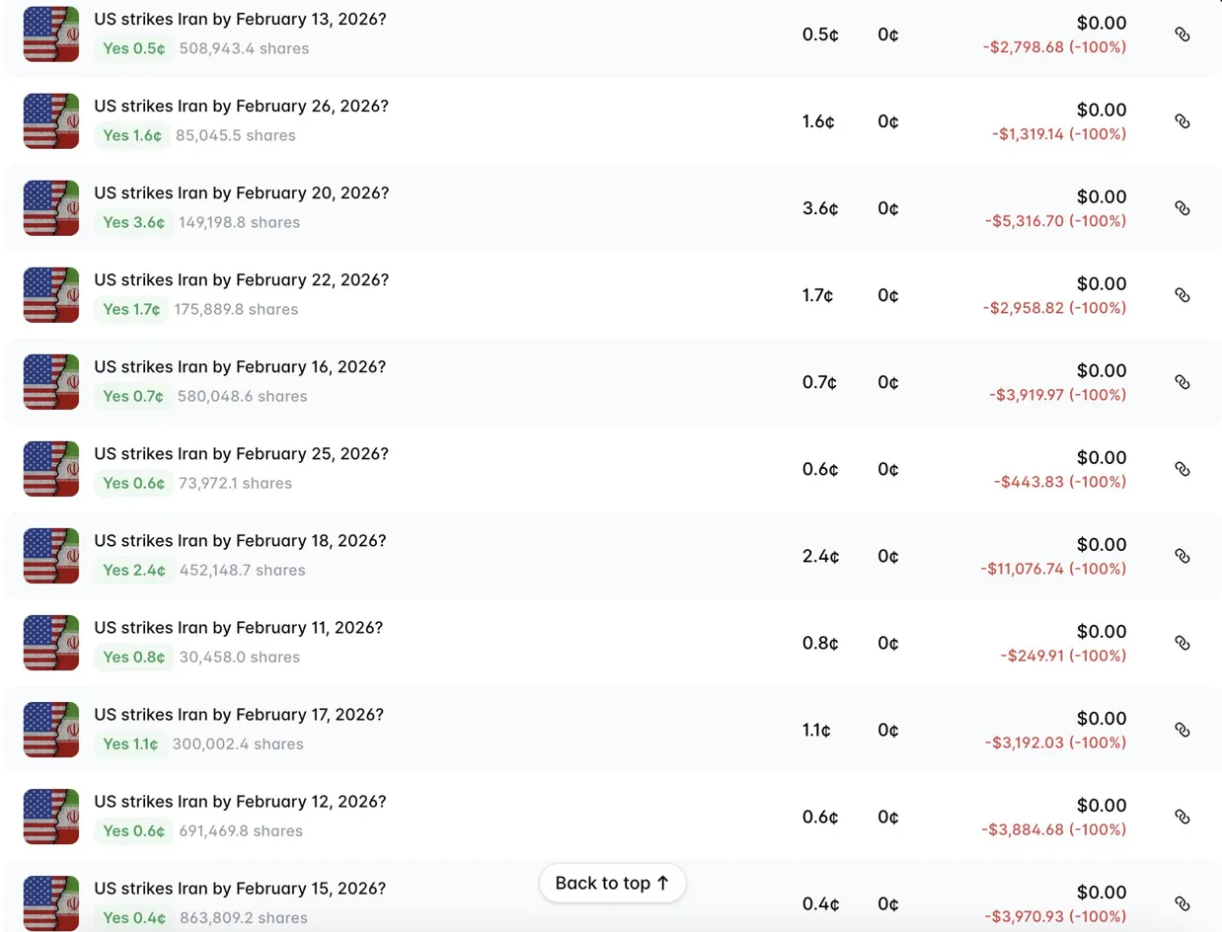

His trading record is quite remarkable: Starting February 11, for every deadline – the 11th, 12th, 13th, 15th, 16th, 17th, 18th, 20th, 22nd, 25th, 26th – he bought Yes contracts one by one, with average prices ranging from 0.4¢ to 3.6¢. Each trade went to zero. Total losses: approximately $39,000.

A strategy of sustained effort despite repeated failures

Then came February 28. The joint US-Israel airstrike began, and Khamenei was killed that same day.

On the contract expiring February 28, he held 504,416 Yes contracts at an average price of 12.7¢, investing $63,986. He ultimately profited $437,930, a 684% return. Combined with his holdings on the same day for "Will Khamenei step down?" (bought at 53¢, +88%) and "Will Israel strike Iran?" (bought at 14.9¢, +571%), his total profit from these three contracts on a single day was over $629,000, covering all previous losses and netting him $511,098.

Timeline Position and the Information Environment at the Time

When Vivaldi007 registered his account in early February, several important events were occurring in the public information domain:

On February 6, indirect US-Iran negotiations restarted in Muscat, with Witkoff, Kushner, and CENTCOM Commander Brad Cooper listed on the US delegation – military involvement in negotiations itself was an anomalous signal. On February 13, Trump ordered the USS Gerald R. Ford carrier strike group to the Middle East. On February 17, Khamenei publicly stated "The US Navy can be sunk." On February 20, Trump issued a 10-day ultimatum and publicly threatened military action. On February 24, in his State of the Union address, Trump claimed Iran had restarted its nuclear program. On February 26, the third round of Geneva negotiations collapsed, with the US delegation leaving "disappointed." On February 27, multiple embassies began evacuating non-essential personnel from Tehran.

Of course, the Trump administration had the precedent of Venezuela, which was also an indispensable factor to consider.

From February 11 to February 27, the market's pricing for "Will the US strike Iran in February?" never exceeded 15¢. The cost of buying across all these deadlines was extremely low because the market generally leaned towards negotiations continuing.

Logic of this Strategy

Vivaldi007's operation didn't predict a specific date but laid out positions across all deadlines within a time window, covering as many dates as possible with very low unit costs, waiting for one of them to trigger.

This strategy has several structural prerequisites: First, he had a strong conviction that "the US will eventually strike," otherwise he wouldn't have persisted from early February to the end of the month. Second, he accepted sustained losses, totaling up to $39,000. Third, his position on the February 28 contract was significantly larger than on other dates ($63,986 vs. $250–$11,000 per trade on other dates), indicating he increased his bet on this specific date at some point, rather than distributing evenly.

Case Study 3: Betting $2.1 Million on "Nothing Will Happen": The Capital-Preservation Strategy of Large Players

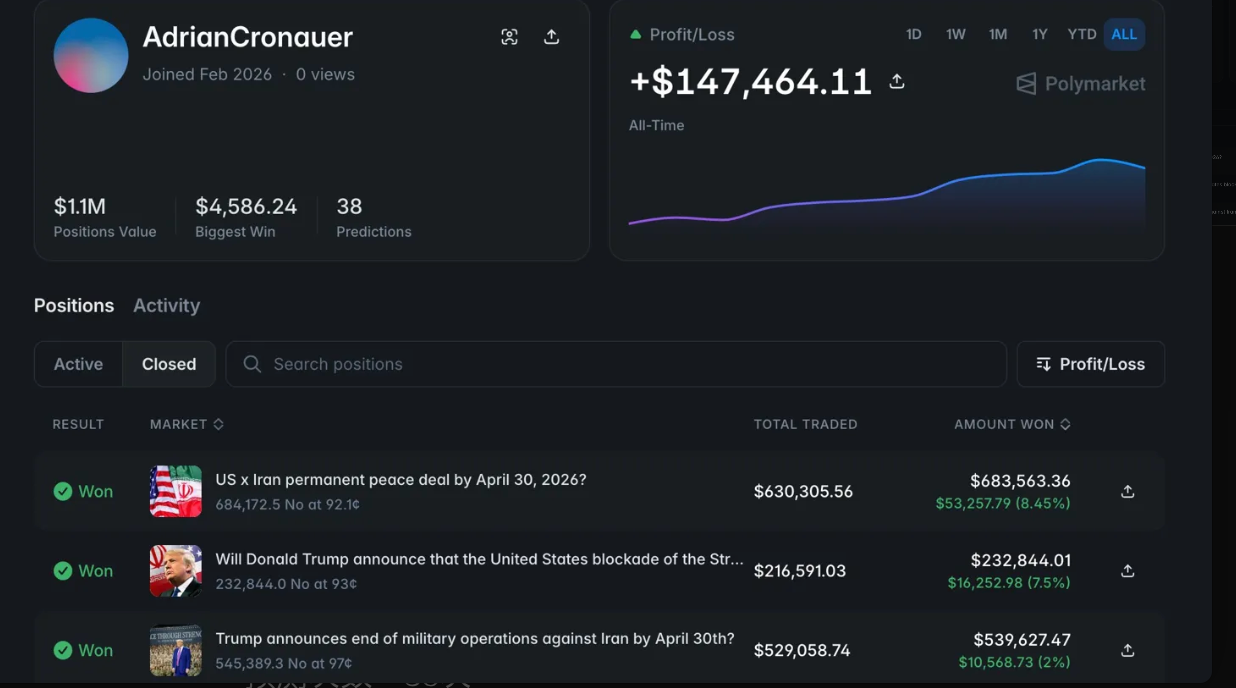

Account: AdrianCronauer

The operational logic of this account is completely different from the previous two cases. Fernandoinfante and Vivaldi007 bet on "something will happen," while AdrianCronauer bet on "nothing will happen."

He uniformly bet "No" on all major Iran contracts expiring before the end of April: a permanent peace agreement will not be reached, Trump will not declare an end to military operations, Iran will not hand over enriched uranium, the blockade of Hormuz will not be officially lifted by the US, and diplomatic meetings will not take place before the deadline. Every single bet was a "No," and every single one won.

The returns weren't very high compared to the first two; the highest was only 8.45%, and the lowest was 0.44%. But the principal size compensated for everything. On just the "Will a permanent peace agreement be reached before April 30?" contract, he invested $630,305 and profited $53,257. On "Will Trump stop military operations before April 30?" he invested $529,058 and profited $10,568. Across 38 predictions with a 79% win rate, he deployed over $2.1 million in principal, netting a cumulative profit of $147,464.

Timeline Position and Information Environment

These trades were concentrated in early to mid-April, after the ceasefire was announced but before the negotiations broke down.

When the ceasefire was announced on April 7, the market pricing for "permanent peace agreement" and "end of military operations" briefly rose. AdrianCronauer built his No positions partly during this window: When the market became optimistic due to the ceasefire news, pushing the Yes side for "permanent peace agreement before April 30" up to 7-8¢, he bought the No side at 92¢, locking in the optimistic premium from the counterparty.

On April 11-12, negotiations in Pakistan lasted 21 hours and ended with "no agreement." JD Vance publicly stated that Iran "refused to accept our terms." On April 13, the US announced a counter-blockade on Iranian ports. On April 17, Iran announced the reopening of Hormuz, only to close it again on April 18. By April 21, when Trump extended the ceasefire, there were only 9 days left until the April 30 deadline, and negotiations between the two sides were effectively deadlocked.

Against this informational backdrop, even pricing the Yes sides of "permanent peace agreement before April 30" and "Trump stops military operations before April 30" at 7-8¢ seemed overvalued to AdrianCronauer.

Core Judgment of This Strategy

AdrianCronauer's operation was based on a relatively simple but continuously verifiable judgment: In highly uncertain geopolitical stalemates, major breakthroughs by short-term deadlines are consistently overestimated by the market.

He wasn't betting on the specific outcome of negotiations, but rather on "not enough time." Even if events like a permanent peace agreement, a declaration ending military operations, or the transfer of enriched uranium were to happen eventually, the probability of them being completed within a few weeks was extremely low. When the market priced the Yes side of such contracts at 1-8¢, the corresponding No side was at 92-99¢, offering returns of only 1-8%, but with very low risk. He used scale to generate returns, spreading $2.1 million across a dozen related contracts, systematically harvesting the market's optimistic premium.

Where was the risk?

The fatal weakness of this approach is a single-event black swan. If Trump had actually declared an end to military operations before April 30, his $529,058 No position would have gone to zero. He bought the No at 97¢, implying he thought the probability of this event was less than 3%. Yet Trump's decisions have historically been unpredictable.

However, considering the information environment throughout April, this judgment was supported: negotiations had broken down, bilateral trust was extremely low, there was a split within Iran's leadership, and Hormuz kept opening and closing. Any one of these conditions made the probability of "reaching a formal agreement within 30 days" extremely low.

Case Study 4: How Small Capital Achieved Case Study 3's Effect? The High-Frequency Trading Strategy

Account: 0xcd7..0d127

This account doesn't have a story of a single massive win. 2,000 trades, $25.9M total volume, $7,900 average position, 75.5% win rate, cumulative profit of $292,000.

The PnL curve starts in June 2025, climbing slowly, steadily, nearly linearly upwards to the right, with no obvious jumps or major drawdowns.

Strategy Essence: Systematically Shorting Market Panic

Analyst Jay Godiyadada on X had a precise observation of this account:

The historical success rate of the Iranian regime in withstanding external shocks is about 95%, but in a state of panic, the market priced the Yes side for "regime collapse" at around 20%, causing the corresponding No side to be undervalued by 15-20¢. Whenever the market pushed up the Yes price due to an event (outbreak of war, leader killed, ceasefire breakdown), this account would take a large position on the No, harvesting that overflowing panic premium; then, as the situation stabilized, it would take profits.

Take "Will the Iranian regime collapse before June 30?" as an example. In the early days of the war, when the situation was most chaotic and uncertainty was highest, the No price was suppressed to around 91¢, implying almost a 10% probability of regime collapse. He bought at this point. As the ceasefire took hold and the situation stabilized, the market re-evaluated the possibility of regime collapse, the No price climbed from 91¢ to 95¢, resulting in a 4% unrealized gain.

In summary, this account was essentially swing trading within the prediction market.

Difference Between This Account and Case Study 3

While their strategies appear similar on the surface, there is a key substantive difference: AdrianCronauer is characterized by concentrated capital, low frequency, large positions – single trades of $500,000–$630,000, a few contracts, total 29 trades. 0xcd7 is characterized by dispersed capital, high frequency, medium positions – average $7,900, 2,000 trades spanning multiple market categories (Iran, Greenland, Fed Chair), operating continuously for nearly a year.

AdrianCronauer's approach is closer to a single arbitrage play. 0xcd7's approach is closer to a market maker logic: continuously identifying Yes contracts overpriced due to emotional sentiment, systematically shorting them, and accumulating returns through frequency and win rate.

$25.9M Volume, $7,900 Average Position, 2,000 Trades

This implies the account maintained a very high turnover rate most of the time. This style is very reminiscent of a Meme-style trader, who doesn't wait for settlement but continuously scans the market, intervening when pricing deviations offer a 5-10% profit margin. A 75.5% win rate over a sample of 2,000 trades is statistically significant and unlikely to be due to luck.

The core competitive advantage of this account, in Jay's words, is "status quo bias" – a systematic bet on the idea that "the current situation will persist." In geopolitical markets, major changes are always overestimated, while gradual stagnation is consistently