泡沫之后,何去何从:2026 数字资产市场分析报告

- Quan điểm cốt lõi: Thị trường tiền điện tử hiện đang ở giai đoạn điều chỉnh sau khi bong bóng vỡ, có sự tương đồng cao với chu kỳ lịch sử của bong bóng Internet (2000-2002), không phải là "đã chết", mà đang trải qua quá trình trở về giá trị thực và tái cấu trúc cơ sở hạ tầng, đặt nền móng cho làn sóng tăng trưởng tiếp theo.

- Các yếu tố then chốt:

- Quy luật chu kỳ lịch sử: Các bong bóng công nghệ như đường sắt, vô tuyến và Internet đều trải qua bốn giai đoạn "mầm mống - hưng phấn - sụp đổ - điều chỉnh", giai đoạn điều chỉnh đi kèm với việc vốn tập trung vào các công ty đầu ngành, khung pháp lý hoàn thiện và mô hình kinh doanh chuyển từ "kể chuyện" sang "tạo lợi nhuận".

- Hiện trạng thị trường tiền điện tử: Tính đến tháng 3 năm 2026, tổng vốn hóa thị trường khoảng 2,5 nghìn tỷ USD, giá BTC dao động trong khoảng 65.000-76.000 USD, tỷ lệ thống trị của BTC ổn định ở mức 58-60%, đặc điểm thị trường tương tự như giai đoạn điều chỉnh sau bong bóng Internet (ví dụ 2002-2004).

- Quá trình thể chế hóa: Các quỹ ETF Bitcoin giao ngay tại Mỹ đã thu hút tổng cộng hơn 53 tỷ USD vốn ròng kể từ khi được phê duyệt vào năm 2024, tỷ lệ nhà đầu tư tổ chức chiếm hơn 30%, cho thấy BTC đang chuyển đổi từ tài sản đầu cơ thành tài sản phân bổ cấp độ tổ chức.

- Khung pháp lý được thiết lập: SEC và CFTC đã cùng ban hành khung phân loại tài sản số vào tháng 3 năm 2026, phân loại 16 loại tài sản là hàng hóa số, chấm dứt sự bất ổn định về quy định kéo dài, cung cấp sự đảm bảo về mặt thể chế cho việc tham gia của các tổ chức.

- Tập trung vốn và thanh lọc dự án: Năm 2025, vốn đầu tư mạo hiểm trong lĩnh vực tiền điện tử tăng khoảng 50% so với cùng kỳ, nhưng khối lượng giao dịch giảm 46%, vốn tập trung cao độ vào các dự án giai đoạn cuối; hơn 70% các dự án DeFi và Meme có TVL giảm hơn 90%, thanh khoản cạn kiệt.

- Khuyến nghị chiến lược: Các dự án nên tập trung vào thanh toán stablecoin và token hóa RWA; Quỹ đầu tư mạo hiểm cần chuyển sang đầu tư kết hợp vốn cổ phần + token; Nhà đầu tư nên ưu tiên phân bổ vào BTC, thận trọng với Altcoin, và chú trọng vào các nguồn doanh thu có thể kiểm chứng.

Foreword: The Certainty and Uncertainty of Crypto

At the dawn of 2026, amid a new bull-bear transition, the market is gripped by anxiety. After the 1011 event, market liquidity began to dry up. Going forward, aside from a handful of leading projects and companies that remain viable, most teams are choosing to shut down or pivot.

With the sudden emergence of Openclaw, a new wave of technology is sweeping through, adding immense uncertainty that exacerbates the panic. As market liquidity shrinks, countless crypto workers are pivoting to AI. Even media outlets once solely focused on Crypto have somehow found room for AI reports on their front pages. Furthermore, an OG with over a decade in the space is sounding the alarm that "crypto is dead."

The crypto bubble has burst. Is Crypto truly dead?

Throwing this question to AI yields countless answers. DeepSeek might tell you that the gravy train of the crypto market has left the station, and it's now a domain for professional, compliant players with no room left for retail. If you ask Grok, it might say this is just a normal bull-bear transition in Crypto that will weed out some players but ultimately steer the industry in a better direction. If you consult Gemini, it might argue that the development of AI will drive the synchronous development of Crypto.

There's too much noise. So we want to find our own answer to this question. There is nothing new under the sun. We have vague memories of similar pronouncements when the internet bubble burst in 2001. In fact, every bubble is met with the same chorus.

So this time, we chose to study bubbles.

Even if the answer turns out to be wrong, it's a certainty that belongs to us.

I. Exploring Historical Cycles: How Tech Bubbles Recur from Railroads to the Internet

The Glory of Railways and Radio: The Rise and Fall of Industrial Revolution Bubbles

On September 27, 1825, the world's first railway built in Britain – the Stockton and Darlington Railway – officially opened. Despite opposition from feudal aristocrats and the church three years prior, capitalists saw the future value of this steel behemoth, placed their bets, and ultimately succeeded. They believed this technology would bring them profits, but they didn't realize the impact it would have on the entire era.

Although the first railway was merely built as a branch line for the canal transport system, its convenience and cost-effectiveness spurred the industry to develop like bamboo shoots after a spring rain, attracting investors to join in. During the tail end of the South American mining speculation bubble of 1824-1825, these risk-takers shifted their investments to railway companies. Between 1836 and 1837, buoyed by a stronger overall stock market, railway company share prices doubled. Seeing an opportunity, the British Parliament approved 44 new railway companies in that single year. The total financing raised by these companies that year easily surpassed all the capital previously invested in the industry.

The Rise, Fall, and Rise Again of Bubbles

Like countless bubbles that followed, when a new technology gradually gains market acceptance, a bubble rapidly inflates and pops in a short time. Then, as infrastructure matures, a new, stronger bubble emerges, eventually guiding the industry back on track.

After these 44 companies were established, and before a comprehensive railway network was built, railways didn't seem much more convenient than traditional water transport. The railway stock index began to fall. However, by the early 1840s, valuations rebounded, approaching previous peaks. Before 1843, average annual capital investment in railway companies was about £1 million (roughly $3.5 billion today). In 1844, this figure became £20 million (20x); in 1845, it neared £60 million (60x); and in 1846, it ballooned to £132 million (equivalent to about $120 billion today). In that same year, the total length of new railways built reached a record 4,538 miles. Everything seemed prosperous.

The Bursting of the Bubble and the Return of Value

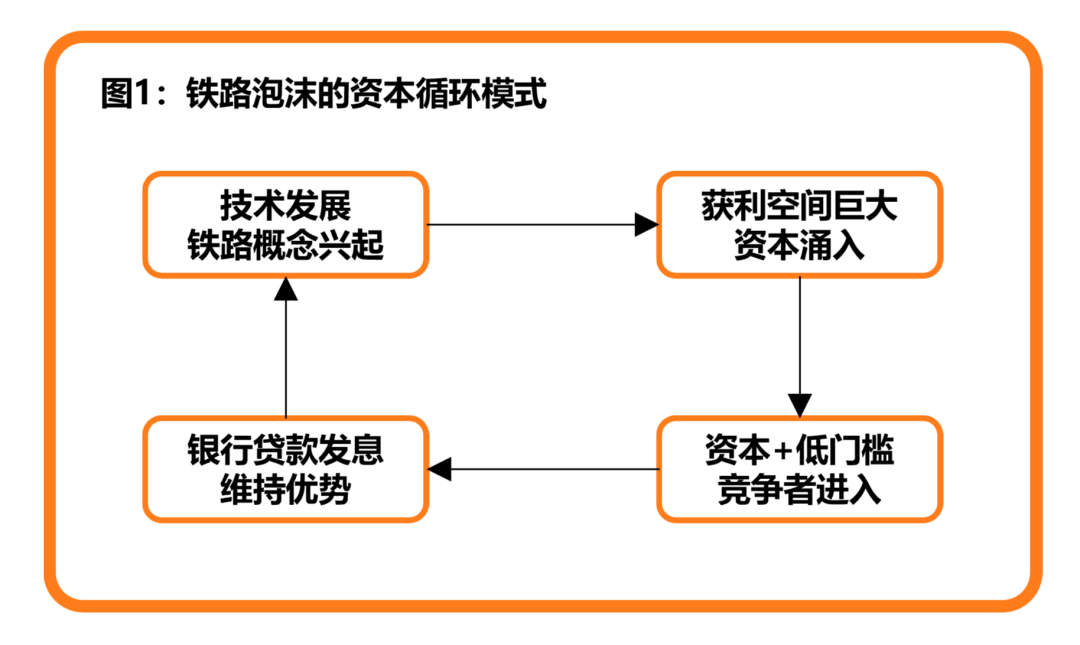

Undeniably, early railways were successful commercial projects. However, due to investor optimism, share prices quickly soared far beyond any rational valuation ceiling for railway stocks. The first railways had a first-mover advantage, but this disappears if there are no barriers to entry. Ample market capital combined with low technical/market barriers presented an excellent opportunity for subsequent competitors. This continuously compressed the profit margins of existing companies, creating an environment of diminishing returns across the entire industry, commonly known as "involution."

For market investors at the time, the first sign of the end of prosperity was the disappearance of huge premiums on newly issued shares. Only companies perceived as higher quality could maintain their stock prices. For surviving railway companies, expanding and securing prime locations was undeniably the best option to maintain valuation and competitive advantage. Using bank loans for leverage could accelerate this advantage. Worse still, being in a nascent industry, most railway companies subconsciously underestimated the difficulty of railway construction. Consequently, actual construction costs far exceeded the initial estimates in their prospectuses. Over time, these company stocks became pure financial games: railway dividends no longer came from corporate profits, but from capital funds and bank loans.

Within this vicious flywheel, bank interest rates kept rising. After a certain tipping point, railway companies could no longer sustain this capital cycle. The capital glow brought by technology suddenly vanished. Overnight, countless investors went bankrupt, and public praise for railway companies turned into accusations.

Faced with this situation, the British government was forced to pass an act of Parliament allowing the railway industry to consolidate and abandon nearly 20% of the approved new railway construction. As surviving firms regained profitability, a wave of mergers and acquisitions began. Afterward, the glory of British railways was no longer a blinding glare, but more like the gentle, slow morning sunlight warming the land. While the crazy capital bubbles were unlikely to reappear, they genuinely nourished the growth of the Industrial Revolution.

Ultimately, the same story played out again, slightly later, on the American continent.

Marconi and Radio

As a footnote to the development of the era, the story of railways ends here for now. With the continuous development of transportation, the world was shrinking. People could travel farther via these vehicles or use wired telephones and telegraphs to transmit information without leaving home.

Of course, the speed limit of information transmission should not stop there.

In 1865, after Scottish physicist James Clerk Maxwell systematically proposed the theory of electromagnetic waves, some inventors began experimenting with various radio waves. Eventually, in 1895, Lady Luck smiled upon the Italian inventor Guglielmo Marconi. When he successfully made a receiver ring a bell from a distance of 10 yards using his self-built signal transmitter, he believed this distance could be much greater.

Marconi keenly sensed the future commercial value of this technology. He filed a patent in 1896 and began promoting his technology to government agencies. Soon after, he founded the Wireless Telegraph and Signal Company to develop and sell wireless telegraph equipment. As consideration for waiving his patent rights, Marconi received £15,000 in cash (equivalent to about $6 million today) and £60,000 in shares (equivalent to about $28 million today), freeing him from financial worries. That year, Marconi was only 22 years old.

From War to the Market

As a rising star, Marconi quickly attracted attention from all sectors of society. In the company's early days, Marconi recognized the extensive communication needs of the British Royal Navy, which operated globally. In 1899, he secured contracts to provide wireless equipment sales and consulting services to the British and Italian navies. The first order was for £6,000 (about $2.5 million today), with subsequent annual revenues exceeding £3,000 (about $1.25 million today).

Despite securing national-level backing, the market remained skeptical about the technology's potential for regular commercial value. After several years of trial and error, Marconi adjusted his business model, switching his sales strategy from direct sales to leasing. The most significant feature of this approach compared to the traditional path was – ecosystem building. Through this type of partnership, he allowed any product or company to use wireless products by paying only a portion of the rent. The only restriction was that all customers could only communicate with other Marconi customers.

It was precisely this strategy that led to the birth of countless radio stations and similar competitors.

The Birth of Radio Concept Stocks

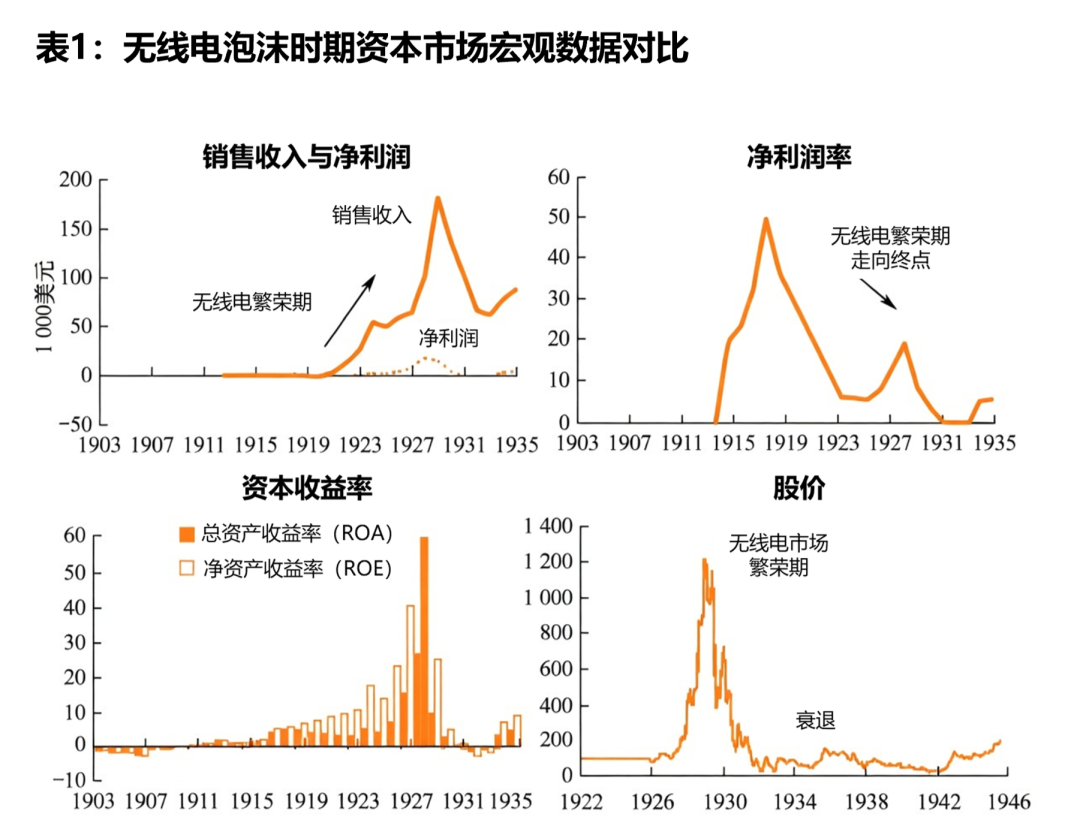

With Marconi's entry and other technological competitors joining the fray, the entire radio industry began to thrive, attracting a flood of capital. In Marconi's early days, despite the company showing losses in its financial reports, this did not deter investor enthusiasm: the technology and business model were still in their early stages, making losses acceptable. Later, Marconi's company was renamed RCA. The technical advantages and business networks meticulously built in the US over the years began to pay off. RCA consolidated the patents held by AT&T, GE, RCA itself, and Westinghouse Electric, forming an impregnable commercial fortress. This led to explosive growth in RCA's sales revenue and profits.

When one person gets to the top, even their chickens and dogs ascend to heaven. Upstream and downstream companies associated with RCA also enjoyed this technological dividend. At the most exaggerated point of the market, some people could easily raise funds and list their stocks simply by registering a company with the word "radio" in its name. The story that followed was identical to the earlier railway dividend: a flood of capital and companies rushing in; when the dividend began to fade, bank loans were used as dividends; eventually, the market collapsed, and the dividend vanished. A key difference from railways is that the commercial value of radio technology was so epoch-making that this technological boom lasted nearly two decades. After radio infrastructure was complete, the vast imagination space – from radios and broadcasting stations to televisions and radio media – was enough to keep the market prosperous for a long time.

Eventually, the Great Depression arrived. Capital games could no longer be sustained. People had to seek more difficult but practical means to try and improve their companies' and products' real sales revenue and net profit.

Atop the Internet Wave: A New Round of Technological Social Experiments

After IBM attempted to launch the personal computer, and Apple accelerated its adoption, PC penetration in the mass market reached new heights. This also meant that certain technologies previously confined to research labs began to emerge – namely, the Internet.

From the Ivory Tower to the Commercial Arena

The origin and birth of the Internet have become a cliché, so we won't dwell on it here. Compared to its birth, the journey of how the Internet became commercialized is far more worth studying.

The decisive factor in this transformation was the National Science Foundation's (NSF) decision to relinquish control over the National Research and Education Network (NREN) and allow it to transition to a privatized, self-sustaining operation. During this process, numerous key elements emerged that made the widespread, society-level application of the Internet possible: Apple PCs provided the hardware foundation, the World Wide Web provided the framework, and Mosaic provided the entry point. Combined with the commercialization of the NREN, a giant industry began its magnificent journey.

In the early stages of commercial open-sourcing, not everyone saw the opportunity. More related companies chose conservative approaches. On one hand, their knowledge base and insights didn't allow them to recognize the potential opportunities the Internet held. On the other hand, in the business environment of the time, industry giants primarily created revenue through land-grabbing and building their own ecosystems. Faced with this extremely open new environment, they were naturally resistant. Nevertheless, this wasn't necessarily bad for industry development: the resistance of giants provided ample market space and opportunities for new entrants.

Netscape: The First to Seize the Opportunity

As one of the earliest companies to seize the opportunity, Netscape's peak genuinely startled the entire market. In late 1994, Mosaic Communications got into a legal dispute over its name with Mosaic, leading it to change its name to Netscape Communications Corporation.

Although the company still had $12 million in the bank at the time, a cash burn rate of $1 million per month forced Netscape to consider a business model pivot. Through a series of moves, it changed its previous service model to a 30-day free trial followed by a $49 service fee. Leveraging the overwhelming performance advantage of its products, it quickly captured a large market share. Its intention was merely to make its market valuation look better through market share, but it didn't expect the strategy to be so effective. During its IPO in August 1995, Netscape raised $140 million, propelling it directly to its zenith.

However, what made it succeed also led to its downfall. The success of this sales strategy went to Netscape's head. Basking in the joy of its IPO, it failed to consider how to build its moat next. It neither solidified its upstream and downstream moats through acquisitions, nor deepened its products to make them better. It even looked down upon industry cooperation, instead opting for the most foolish approach: inaction.

Its end was also predictable: once the market discovered this huge cake, and Netscape, as the first mover, had verified its tastiness, a flood of competitors rushed in. Netscape was eventually acquired by AOL.

A Whale Falls, Everything Grows

Netscape's story is a cautionary tale, but broadly speaking, it was a meaningful development for the market. Countless profit-seekers and innovators joined the adventure, spawning a dizzying array of projects. Almost in the same year as Netscape's success, Jerry Yang and David Filo spent significant time studying browser needs and ultimately created a highly efficient information indexing system, which they named "Yahoo!". Meanwhile, at Stanford University, Sergey Brin and Larry Page began exploring information search engines, focusing on how to find desired information content faster on the Internet. When these ideas traveled across the ocean, a then-inspired Jack Ma began preparing the development and construction of "China Pages."

The Peak of Concept Bubbles

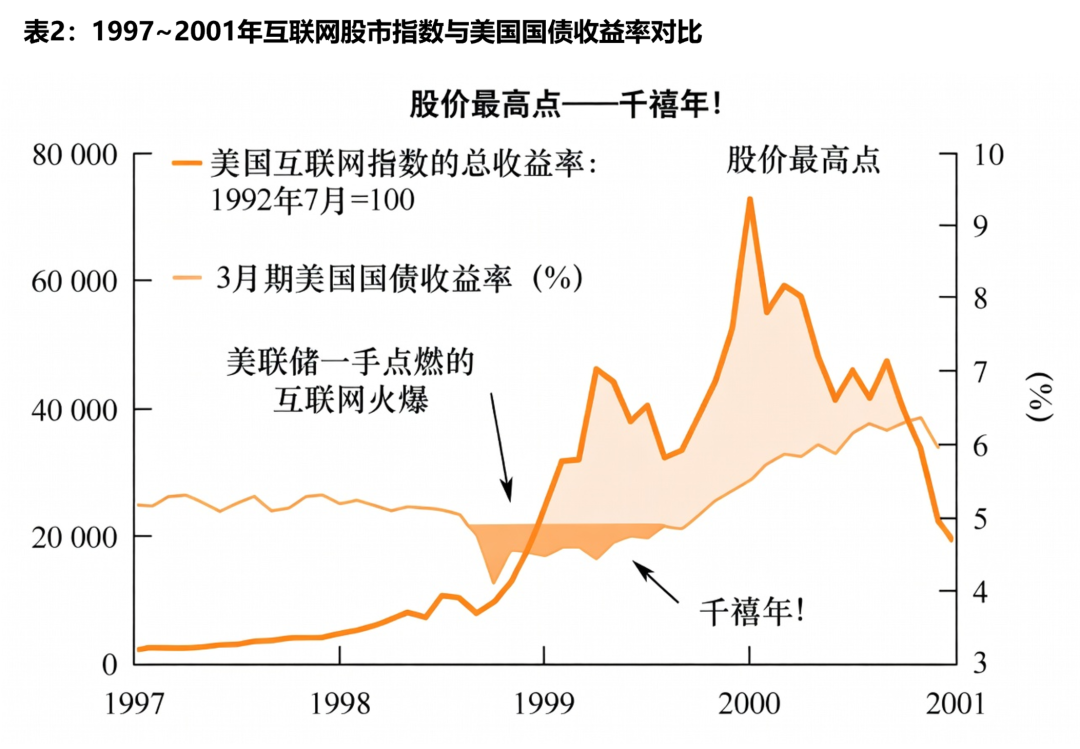

Compared to previous railway and radio technologies, the barrier to entry for Internet technology was clearly lower. It didn't require hiring workers to build railways or pull cables, nor did it need government permits. As long as you understood relevant Internet knowledge, you could do almost anything you wanted. The massive wealth effect combined with low entry barriers ignited a carnival in the capital markets.

At the very beginning of the bubble, the capital market maintained a degree of caution. But when they saw that rudimentary products born in "garages," like Yahoo and Google, could also rake in profits through innovative business models, they realized that previous market valuation logic seemed obsolete. Coupled with the rapid surge in internet tech stock prices, investors threw their earlier skepticism out the window. Ultimately, for fundamental investors, valuations in the TMT sector were being carelessly and indiscriminately inflated, and almost everyone thought it was perfectly fine.

As corporate valuations became increasingly bold, professional analytical standards began to distort. Typically, the higher the stock price, the higher the valuation derived by analysts relying on the income statement. To ensure valuation seemed reasonable, when the original profit anchor could no longer support the current price, the valuation benchmark gradually shifted from profitability to revenue. Then, revenue was further broken down into concepts like "click-through rates" and "retention rates" to analyze a company's market prospects for the next few years. The entire logic seemed reasonable, but the fatal flaw was: in the absence of past cases for reference, how could one ensure the validity of the business model analysis? The only prerequisite was to listen to the founding team's analysis, i.e., "storytelling."

Ultimately, people stopped paying for technological utility and started