BitMart VIP Insights | Tổng quan thị trường tiền mã hóa tháng 4 và phân tích điểm nóng

- Quan điểm chính: Thị trường tiền mã hóa tháng 4, trong bối cảnh căng thẳng địa chính trị hạ nhiệt và quy định được thúc đẩy, đã cho thấy sự cải thiện về cấu trúc với "vốn hóa thị trường bứt phá, khối lượng giao dịch đi kèm". BTC tăng 13% trong tháng, mạnh nhất trong năm, nhưng đang đối mặt với ngưỡng kháng cự quan trọng 80.000 đô la; Biến số chính của tháng 5 nằm ở tín hiệu chính sách sau khi Chủ tịch Fed thay đổi, tiến trình lập pháp của Đạo luật CLARITY và việc khắc phục lỗ hổng bảo mật DeFi.

- Các yếu tố then chốt:

- FOMC tháng 4 giữ nguyên lãi suất, nhưng việc Chủ tịch Fed Powell rời nhiệm sở và Wash kế nhiệm mang đến sự bất định về chính sách. Cuộc họp FOMC đầu tiên do Wash chủ trì vào ngày 6-7/5 sẽ là thời điểm then chốt; bất kỳ tín hiệu diều hâu nào hoặc lạm phát tăng trở lại đều có thể gây áp lực lên tài sản rủi ro.

- Vốn hóa thị trường tiền mã hóa tháng 4 tăng từ 2,43 nghìn tỷ đô la lên 2,70 nghìn tỷ đô la (+11,5%), với khối lượng giao dịch trung bình hàng ngày khoảng 98 tỷ đô la; Quy mô ETF BTC giao ngay vượt mốc 100 tỷ đô la (101,2 tỷ đô la), với dòng vốn ròng hàng tháng đạt 8,44 tỷ đô la, trong khi ETF ETH ghi nhận dòng vốn ròng 1,75 tỷ đô la.

- Việc Mỹ và Iran ngừng bắn là chất xúc tác chính của thị trường, đẩy BTC từ mức thấp 65.000 đô la lên gần 79.000 đô la, nhưng ngưỡng kháng cự 80.000 đô la vẫn chưa bị phá vỡ; SOL hoạt động tương đối yếu, bị ảnh hưởng bởi vụ tấn công Drift, cần quan sát ngưỡng kháng cự 90 đô la và sự phục hồi niềm tin hệ sinh thái.

- Tháng 4 chứng kiến nhiều sự cố bảo mật DeFi, với hai vụ tấn công nhắm vào Drift và KelpDAO gây thiệt hại tổng cộng hơn 600 triệu đô la, làm lộ rõ rủi ro hệ thống từ oracle và kiến trúc xuyên chuỗi, dẫn đến dòng vốn rút ra khoảng 13 tỷ đô la.

- Đạo luật CLARITY đã được hoàn tất đánh dấu tại Ủy ban Ngân hàng Thượng viện. Polymarket dự đoán xác suất được thông qua trong năm nay đã tăng lên trên 85%. Nếu được thông qua vào tháng 5, nó sẽ chấm dứt tranh chấp thẩm quyền giữa SEC và CFTC, thúc đẩy dòng vốn tổ chức gia nhập nhanh hơn.

- Tổng nguồn cung stablecoin tăng nhẹ lên 288,4 tỷ đô la, nhưng có sự phân hóa về cấu trúc: USDT dẫn đầu sự mở rộng (+3,2%), trong khi USDe giảm mạnh 37,7% do lợi suất giảm, phản ánh sự tái cân bằng của dòng vốn giữa lợi nhuận và rủi ro.

- Tháng 5 tập trung vào các động lực tăng trưởng trung và dài hạn như việc thực thi quy định tại châu Á - Thái Bình Dương (khuôn khổ cấp phép stablecoin của Hồng Kông), sự mở rộng liên tục của kho dự trữ BTC doanh nghiệp (MicroStrategy nắm giữ vượt quá 530.000 BTC) và việc mã hóa tài sản thực tế (RWA) (ví dụ: Quỹ BUIDL của BlackRock).

TL, DR

- The April FOMC held steady, but the leadership transition introduces policy uncertainty. Inflation rose due to the oil price shock, while job market recovery supported the economy. The U.S. stock market rebounded overall amid a restoration of risk appetite. In May, the market will focus on policy signals from the new Fed Chair, inflation, and oil price trends. Concurrently, crypto market momentum and legislative progress will also be key variables.

- April's crypto market trading volume exhibited a "low-open, volume-surge, high-level consolidation" structure. Driven by the ceasefire news, volumes surged multiple times, maintaining healthy levels as prices rose. Total market cap climbed from approximately $2.43 trillion to $2.70 trillion, reversing early-month declines under the ceasefire catalyst to oscillate upwards. Compared to March's pressured consolidation, April achieved structural improvement with "market cap breakthroughs accompanied by volume," clearly shifting the market's center of gravity upwards.

- Both BTC and ETH spot ETFs saw significant net capital inflows in April, driving synchronous price increases. Notably, the BTC ETF scale surpassed the $100 billion mark for the first time, signaling a new phase in institutional allocation. Overall, the market showed a "price-led rally with capital following" characteristic, with institutional funds still clearly favoring BTC over ETH. Meanwhile, the total stablecoin supply grew modestly, but internal structural divergence intensified, with USDT dominating expansion while USDe contracted sharply, reflecting a capital rebalancing between yield and risk.

- BTC recorded its strongest monthly performance this year in April, rebounding strongly on geopolitical easing but remaining constrained by the key $80,000 resistance level. ETH's trajectory largely synchronized with BTC, rebounding on institutional demand and upgrade expectations, but still facing short-term resistance testing around $2,400. SOL, while recovering with the market, underperformed, weighed down by ecosystem security incidents. Its subsequent trajectory hinges on confidence restoration and breaking the $90 resistance.

- The US-Iran ceasefire alleviated geopolitical risks, triggering a strong BTC rebound. BTC recorded an ~13% gain in April, driving a significant return of overall crypto market cap and ETF funds. Conversely, attacks on Drift and KelpDAO resulted in DeFi losses exceeding $600 million, triggering a massive capital exodus and exposing systemic risks in oracle and cross-chain architectures. On the policy front, the CLARITY Act completed key advancements, significantly raising expectations for passage within the year, signaling the accelerated formation of a crypto market regulatory framework.

- The core market focus in May will be the first FOMC meeting chaired by Kevin Warsh and potential shifts in policy signals, combined with inflation and oil price trends, directly impacting whether risk assets and BTC can sustain their strength. Meanwhile, the CLARITY Act enters a full Senate vote; if passed, it would significantly boost institutional capital inflows and reshape the crypto regulatory landscape. Asia-Pacific regulatory progress, coupled with corporate BTC treasury strategies and accelerating RWA tokenization, constitute key drivers for medium-to-long term capital inflows and industry development.

1. Macro Perspective

Policy Direction

The FOMC held its third policy meeting of the year on April 28-29, with the market expecting the federal funds rate target to remain unchanged at 3.50%–3.75%. This meeting did not include a dot plot update, making every phrase in the statement highly scrutinized. It was also Fed Chair Jerome Powell's final FOMC meeting before his term officially ends on May 15. His nominated successor, Kevin Warsh, completed a Senate Banking Committee hearing on April 21. On April 26, the final key opposing senator, Tillis, withdrew his objection, clearing the path for a confirmation vote. The market is closely watching whether Powell will provide forward guidance on the policy path in his final press conference and whether a shift in monetary policy signals will occur after Warsh takes over. Overall, the April FOMC brought no policy surprises on the "status quo," but the uncertainty premium introduced by the leadership transition will extend into May.U.S. Stock Market Performance

The U.S. stock market generally showed a pattern of initial decline followed by a recovery rebound, primarily driven by geopolitical easing. Late March saw lingering high oil prices and inflation concerns from the previous month, keeping the S&P 500 under pressure. On April 8, the US-Iran ceasefire agreement was finalized, leading to a partial resumption of shipping in the Strait of Hormuz. Market risk appetite quickly rebounded, with tech stocks and consumer discretionary sectors leading gains, and the S&P 500 rallied sharply within days of the ceasefire. The March CPI, released on April 10, jumped significantly to 3.3%, causing a brief pullback, but the market quickly absorbed the data, characterizing it as a supply-side shock rather than demand-pull inflation. The Q1 earnings season became the core driver in mid-to-late April. The S&P 500 recorded positive returns for four consecutive weeks, reaching a new cyclical high on April 24. Major tech company earnings generally exceeded expectations, with continued expansion in AI capital expenditure further boosting sentiment. Overall, the S&P 500 posted a positive monthly return in April, and the VIX volatility index fell from a high of 31.65 at the start of the month to around 18.5 by month-end, indicating a significant improvement in market sentiment.

Inflation Data

The U.S. Bureau of Labor Statistics released March 2026 CPI data on April 10: CPI grew 3.3% year-over-year, a sharp increase of 0.9 percentage points from February's 2.4%. The month-over-month change was +0.9%, the largest monthly increase since 2022. Core CPI (excluding food and energy) rose 0.2% month-over-month and was up ~2.6% year-over-year, relatively moderate. The main driver of the large inflation jump was the surge in energy prices due to the US-Iran war – gasoline prices rose 21.2% in March alone, the largest monthly increase since 1967, significantly boosting the overall energy component. Tariff pass-through effects also began to appear in imported goods categories. The market's mainstream interpretation was a supply-side shock rather than demand-pull inflation. The relative controllability of core CPI suggests the Fed is unlikely to change its policy path. However, if US-Iran tensions persist, keeping oil prices high, the risk of secondary pass-through effects to core inflation components cannot be ignored.

Employment Data

The U.S. Department of Labor released the March 2026 nonfarm payrolls report on April 3: Nonfarm payrolls increased by 178,000, significantly beating market expectations of 59,000, a substantial turnaround from February's revised figure of -133,000 (initially -92,000). The unemployment rate edged down to 4.3% from 4.4%, while the labor force participation rate dipped slightly to 61.9%. The main contributors to the job market recovery were the healthcare industry (+76,000, primarily due to medical workers returning after strikes), construction, and transportation/warehousing. Average hourly earnings grew 3.5% year-over-year and +0.2% month-over-month, indicating moderate wage inflation pressures. Overall, the March employment data alleviated previous market concerns about a rapid deterioration in the labor market, providing new support for the "soft landing" narrative and somewhat relieving pressure on the FOMC to cut rates quickly. However, the declining participation rate suggests that part of the employment improvement stems from workers leaving the workforce, so the underlying resilience of the job market remains to be seen.

Political Factors

Political factors influencing crypto and macro market sentiment were primarily centered on the US-Iran geopolitical situation. On April 8, under Pakistani mediation, the US and Iran announced a temporary ceasefire agreement. Shipping through the Strait of Hormuz gradually resumed partial operations. Brent crude oil, which had neared $120/barrel during the war, retreated significantly; on the day of the ceasefire, WTI crude fell over 16% in a single day. However, the ceasefire's progress was slow. In late April, Iran's Foreign Minister reiterated a hardline stance, and Brent crude climbed back to the $107-108/barrel range on April 26-27. The fragility of the ceasefire continues to pose a tail risk, with markets worried that if the Hormuz disruption lasts until the end of June, Brent could potentially hit $150. In the crypto space, the CLARITY Act was marked up in the Senate Banking Committee before the April 25 deadline. A substantive disagreement was resolved through the Tillis-Alsobrooks stablecoin yield compromise, significantly raising expectations for legislative passage by month-end. The uncertainty surrounding Powell's impending departure and Warsh's succession became a key new variable for the market at the end of April. Overall, the ceasefire was the most important positive catalyst, but the rebound in oil prices and uncertainty during the policy transition period are the main negative variables.

Next Month Outlook

Looking ahead to May, Kevin Warsh will chair his first FOMC meeting as Fed Chair from May 6-7 (Powell officially steps down on May 15). The market will be highly sensitive to interpreting the statement's language and Warsh's policy signals at the press conference – any notable deviation from Powell's phrasing could trigger significant volatility in risk assets. April CPI and PCE data will be released in May. A key observation point will be whether the March oil price shock leads to a secondary uptick in core inflation. If core components remain moderate (month-over-month ≤0.2%), rate cut expectations will likely stabilize. Following the April mark-up in the Banking Committee, the CLARITY Act enters the preparation phase for a full Senate vote in May. The timeline set by Senator Moreno for passage by the end of May keeps the legislative schedule very tight. For crypto assets, whether BTC can achieve a valid breakout above the critical $80,000 level and whether ETF inflows remain positive are key indicators for judging whether April's bullish momentum can extend into May. The direction of US-Iran negotiations and whether oil prices can retreat below $100 will be the core macro variables determining whether risk appetite can expand further.

2. Crypto Market Overview

Token Data Analysis

Trading Volume & Daily Growth Rate

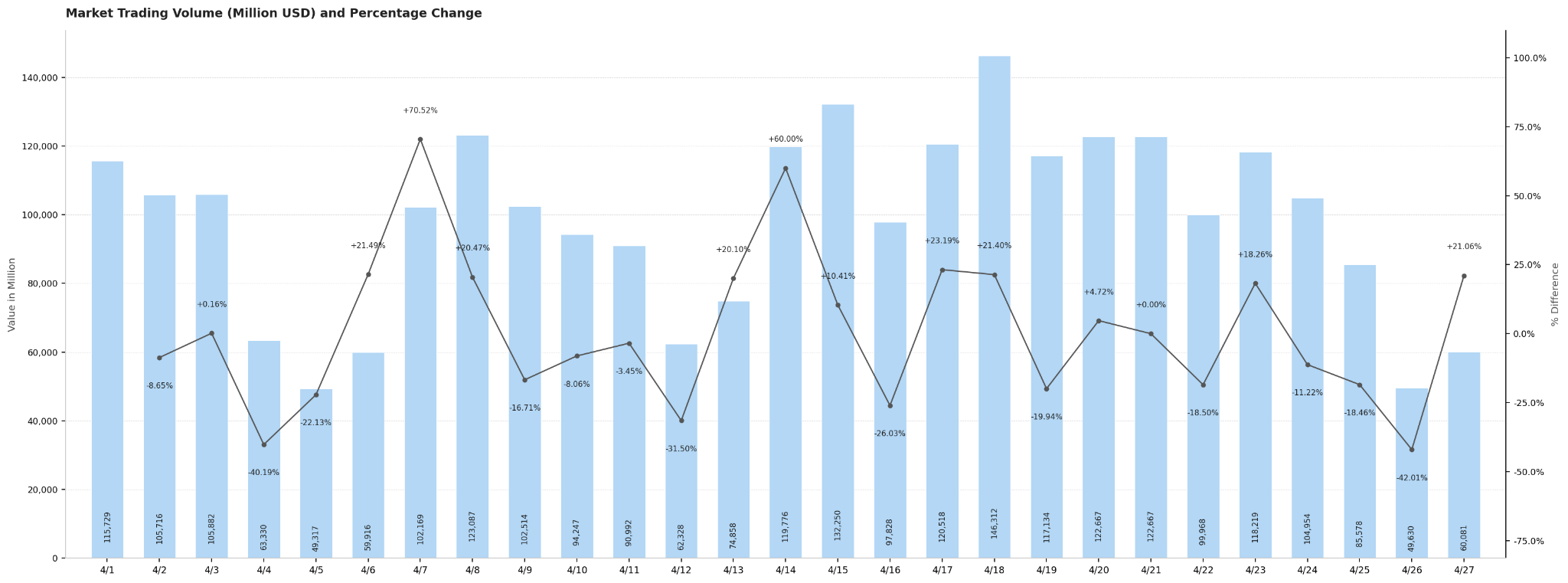

The average daily trading volume in the crypto market for April was approximately $98 billion, exhibiting a "low-open, volume-surge, high-level consolidation" fluctuation pattern. Trading volume started the month at around $115.7 billion on April 1 but fell due to the weekend effect, hitting a monthly low on April 4-5 ($63.3 billion and $49.3 billion, respectively), the lowest level of the month. Volume recovered quickly on the next trading day, surging 70.52% day-over-day to about $102.2 billion on April 7. The confirmation of the US-Iran ceasefire on April 8 further boosted trading volume to ~$123.1 billion, with market sentiment noticeably warming. As the market continued to rise on April 14-15, volume remained high for two consecutive days (~$119.8 billion and ~$132.3 billion, respectively). It peaked on April 18 at approximately $146.3 billion, the most active trading day of the month, coinciding with the crypto market cap hitting a new cyclical high – a significant price-volume resonance. At the month-end, April 25-26 saw a retreat to low levels due to the weekend ($85.6 billion and $49.6 billion, respectively), with a slight recovery to $60.1 billion on April 27. Overall, weekly trading volume generally ranged between $90 billion and $130 billion on trading days, while contracting regularly to $50 billion – $65 billion on weekends. Market activity showed a phased upward trend as the price rose, presenting a healthy volume structure.

Total Market Cap & Daily Change

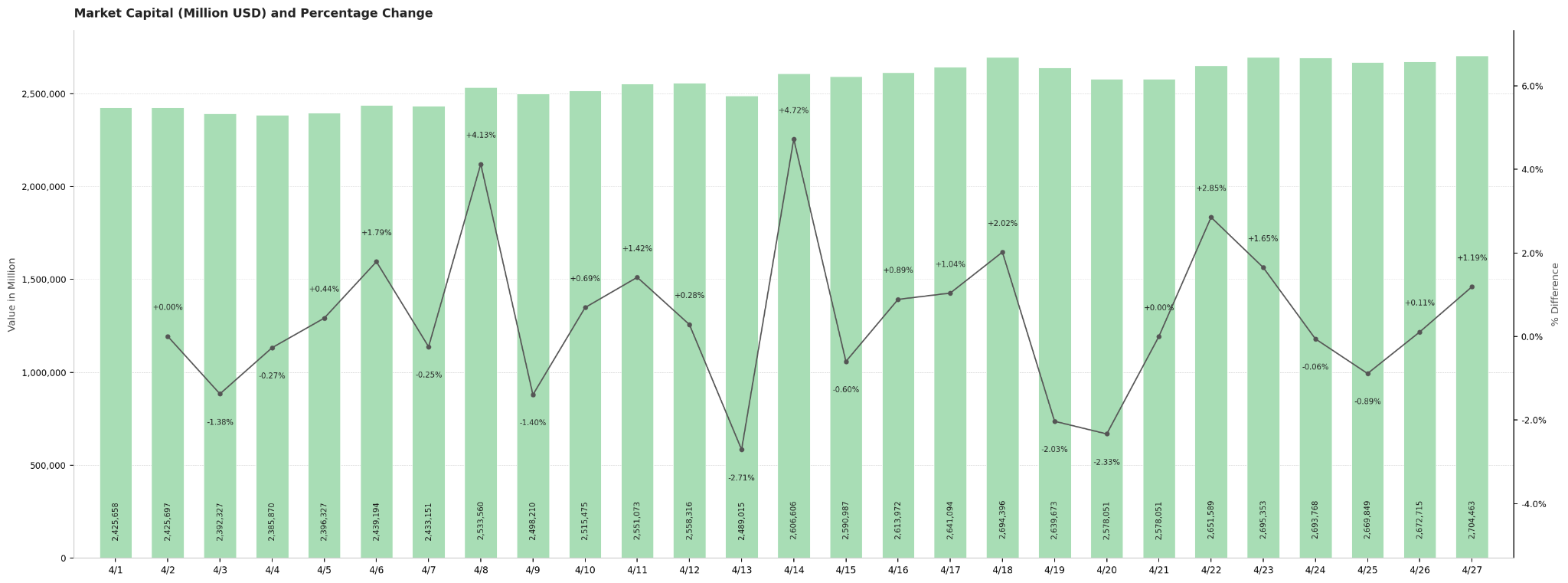

The total crypto market cap in April rose steadily from approximately $2.43 trillion at the start of the month to about $2.70 trillion at the end, a monthly gain of roughly 11.5%. The monthly trend formed a clear three-stage structure: "initial decline and bottom-finding, reversal on ceasefire, and oscillating upward." From the start of the month to April 5, weighed down by high oil prices and inflationary pressures, the market cap dipped slightly to around $2.39 trillion (monthly low). The US-Iran ceasefire agreement on April 8 was the most important turning point of the month. The market cap surged 4.12% day-over-day, breaking through the $2.53 trillion mark, signifying a substantial restoration of market risk appetite. Thereafter, the market cap entered an upward oscillating channel. Driven by sustained capital inflows, it rose another 4.73% day-over-day on April 14, reaching a cyclical high of about $2.69 trillion on April 18. At month-end, the market cap further strengthened to around $2.70 trillion on April 22-23, closing the last trading day of April at $2.70 trillion, the highest closing point for the month. Notably, April 13 saw the largest single-day decline of the month (-2.72%), corresponding to short-term panic caused by the KelpDAO security incident, but the market quickly digested this and continued its upward trajectory, demonstrating the resilience and dominance of bullish forces in this market cycle.

Comparison with March Data

Compared to March, the crypto market in April showed significant improvement in both market cap and trading volume dimensions. Regarding market cap, pressured in March by the combination of hawkish FOMC signals and high oil prices, the total market cap oscillated broadly in the $2.3 trillion to $2.6 trillion range without forming a valid breakout. In April, driven by the US-Iran ceasefire catalyst, it achieved a structural uplift, rising steadily from $2.43 trillion at the start of the month to $2.70 trillion, an intra-month gain of about 11.5%. The upper bound of the range expanded by approximately $100 billion compared to March, shifting the market's center of gravity upwards. In terms of trading volume, March saw average daily volumes around $80 billion to $100 billion, characterized by low activity and cautious capital. April's average daily volume remained at approximately $98 billion, roughly flat with March's average. However, April featured several high-activity periods with single-day volumes exceeding $120 billion (April 8, April 14-15, April 18). Particularly, the peak volume on April 18 of ~$146.3 billion far exceeded any single-day level in March, demonstrating a price-volume resonance structure that amplified as the price rose. Overall, March was a consolidation pattern of "market cap under pressure, volume shrinking," while April achieved a structural shift of "market cap breakout, volume following suit," presenting a stark contrast.

Popular Tokens in April

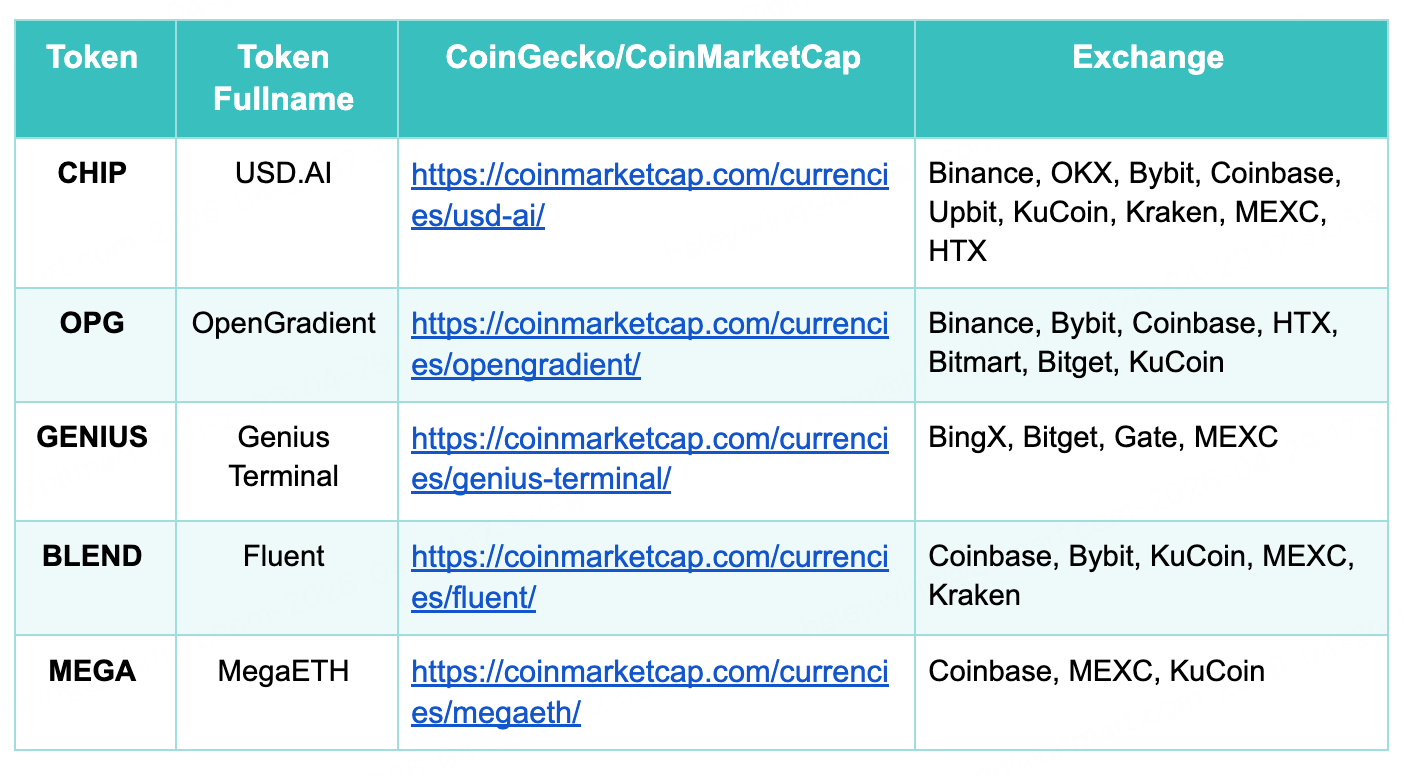

April 2026 saw the launch of several highly anticipated new tokens in the crypto market, with generally strong performance. In terms of launch scale, the first-day trading volumes for CHIP (USD.AI) and OPG (OpenGradient) exceeded $1.4 billion and $1 billion, respectively, setting the liquidity peaks for new tokens in April, indicating a simultaneous influx of institutional and retail capital. GENIUS (Genius Terminal) opened first on April 13. Backed by a multi-hundred-million-dollar investment from YZi Labs and the market effect of CZ acting as an advisor, its price surged over 65x on the first day, with 24-hour trading volume reaching $1.1 billion, rivaling the other two in popularity.

From a sector distribution perspective, the three leading projects cover AI lending infrastructure (CHIP), decentralized AI inference network (OPG), and on-chain trading terminal (GENIUS), all closely aligned with the AI narrative, confirming the market's continued pursuit of the AI+Web3 direction. BLEND (Fluent Network) and MEGA (MegaETH), as new Ethereum Layer 2 projects, completed their TGEs on April 24 and April 30, respectively, with relatively moderate trading volumes. However, Coinbase's backing provided them with strong compliance credibility. Overall, April's new token hotspots focused on the two main themes of AI infrastructure and Ethereum scaling. Top-tier projects had ample first-day liquidity and broad exchange coverage, reflecting the market's still-strong capacity to absorb high-quality new projects.

3. On-Chain Data Analysis

Analysis of BTC & ETH ETF Inflows and Outflows

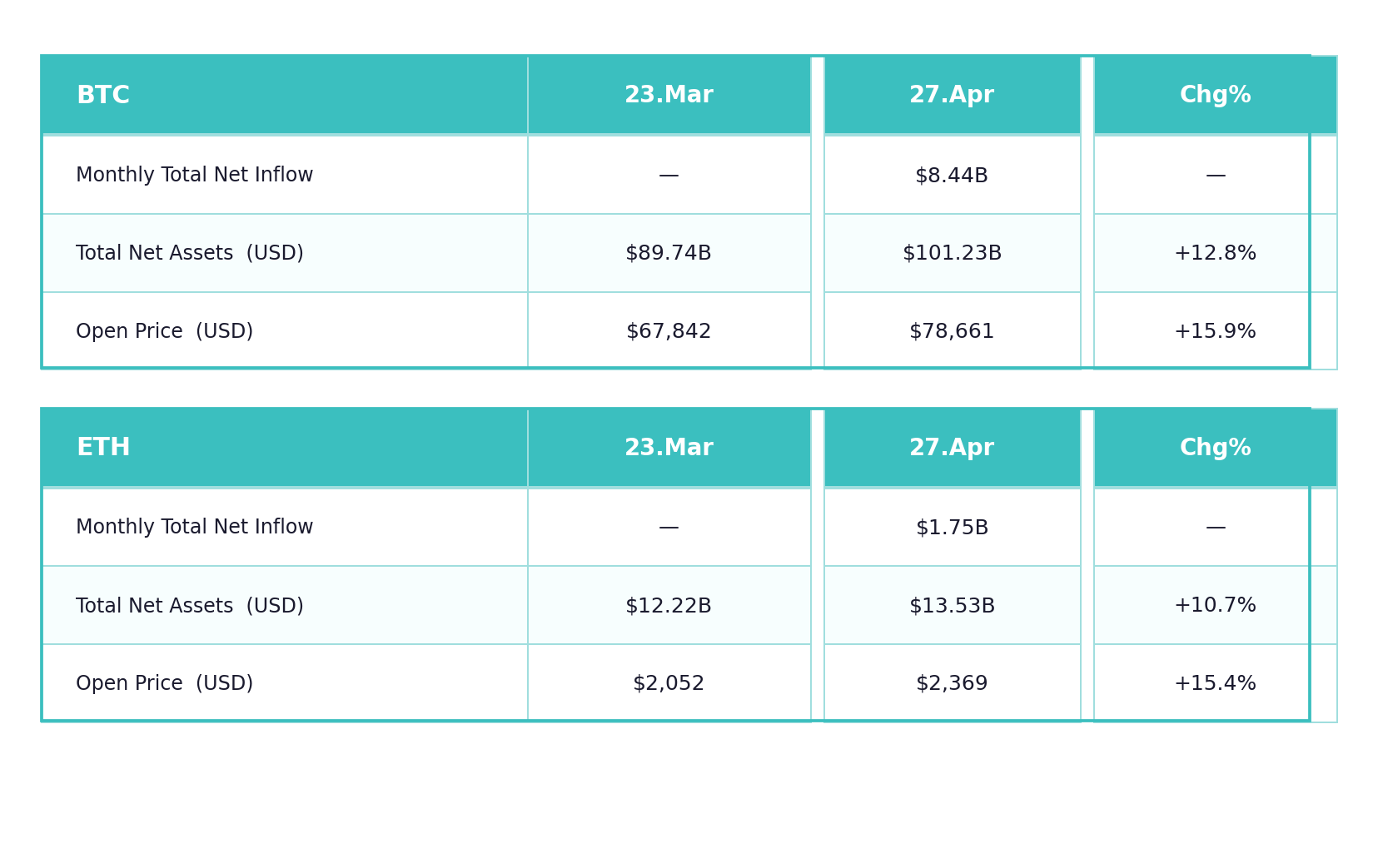

In April, both BTC and ETH spot ETFs continued their net capital inflow trends, with institutional allocation willingness significantly recovering. BTC spot ETFs saw a total monthly net inflow of $8.44 billion, pushing total net assets from $89.9 billion at the end of March to $101.2 billion, a month-over-month increase of 12.8%. This marks the first time it has surpassed the $100 billion mark, a new all-time high. The BTC opening price rose from $67,842 to $78,661 over the same period, a monthly gain of 15.9%, its strongest single-month performance in the past year. ETH spot ETFs also recorded a monthly net inflow of $1.75 billion, with total net assets rising from $12.2 billion to $13.5 billion (+10.7%). The ETH price increased from $2,052 to $2,369 (+15.4%), with gains largely synchronized with BTC.

Structurally, the increase in BTC ETF net assets (+12.8%) was slightly lower than the price