Morgan Stanley Analysis: AI Network Market Headed Toward $70 Billion — Why Is Copper Still the First to Benefit?

- Key Perspective: Morgan Stanley has raised its estimate for the 2030 AI-scale networking market opportunity to approximately $70 billion, but notes that copper will still dominate in the short term (2026-2027). CPO (Co-Packaged Optics) technology is not expected to achieve meaningful penetration of 20-30% until 2029-2030.

- Key Factors:

- Market Opportunity Upgraded: Morgan Stanley projects the 2030 AI-scale networking market opportunity at around $70 billion, representing a more than 4x expansion from last year's estimate. The primary driver is the connectivity demand generated by multi-rack GPU clusters.

- Technology Roadmap Timeline: CPO penetration is near zero in 2026-2027, with small-scale introductions beginning in 2028. Meaningful penetration of 20-30% is not expected until 2029-2030. Copper retains cost and power consumption advantages for short-distance connections (within 7-9 meters).

- Clear Beneficiary Order: In the short term, chip and module companies (such as Astera Labs, Broadcom, Semtech) benefit first because they extend copper performance. In the medium to long term, the upside for optical component vendors (Corning, Lumentum, Coherent) depends on the pace of CPO adoption.

- NVIDIA Roadmap Is a Key Variable: Platforms like Vera Rubin Ultra NVL576 and Feynman Kyber NVL1152 will drive the number of optical engines required per GPU from around 2 up to 17-70. However, actual incremental demand hinges on the production ramp-up timeline of these platforms.

- Testing Equipment Vendors Have Strong Certainty: Keysight Technologies has received a rating upgrade from Morgan Stanley due to the diversification of AI network architectures (NVLink, UALink, etc.) and high-speed testing demands (800G/1.6T/3.2T), without needing to bet on a single technology path.

TL;DR

- Morgan Stanley expects the AI scale-out networking opportunity to be approximately $70 billion by 2030, expanding more than fourfold from last year's estimate.

- Copper cabling will still dominate scale-out networks in 2026-2027, with CPO not likely reaching meaningful penetration of 20%-30% until 2029-2030.

- Keysight, Astera, Broadcom, and Semtech are expected to benefit earlier, while the upside for Corning, Lumentum, and Coherent is more back-end loaded.

In its latest report, Morgan Stanley estimates the AI scale-out networking market opportunity at about $70 billion by 2030 and re-highlights the lifecycle of copper cabling within AI clusters.

This is not a story of an "immediate CPO explosion." AI clusters are evolving from single racks to multi-rack setups, requiring denser, higher-speed connections between GPUs, expanding the total addressable market for the back-end network. However, until power consumption, distance, and bandwidth density truly hit their limits, short-distance connections will maintain a strong inertia toward copper cabling.

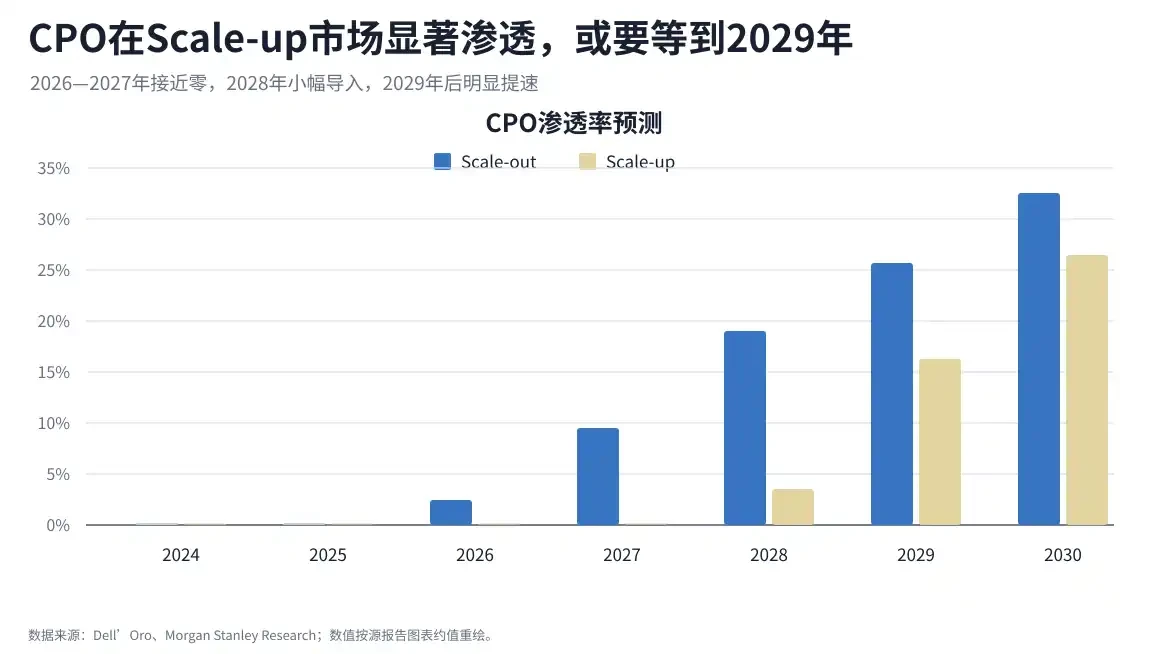

The report's timeline is measured: CPO penetration in scale-out networks will be near zero in 2026-2027; initial modest adoption begins in 2028; and meaningful levels of 20%-30% are not expected until 2029-2030. While the market opportunity has been significantly revised upward, optics will only capture a large share of scale-out networking when larger GPU domains and a more mature supply chain are both in place.

The $70 Billion Opportunity Comes from Multi-Rack Setups; Fiber Modules Are Not the First to Scale

The core driver of this upward revision is the significantly increased demand for intra-server and inter-rack connections as AI clusters expand.

In traditional single-rack scenarios, the distance between GPUs is short, giving copper cables an advantage in cost, latency, and power consumption. For short-distance connections, especially within 7-9 meters, copper remains the most straightforward solution. Over the past few years, advancements in SerDes, retimers, PAM4/PAM6, and other technologies have continuously extended the lifespan of copper, repeatedly delaying the tipping point for optical alternatives.

The change occurs as clusters grow larger. Training and inference clusters expand from one rack to multiple racks, requiring inter-rack communication between GPUs, and signal speeds progress from 100G to 200G and 400G. As distances increase and speeds rise, challenges related to electrical loss, insertion loss, and noise management escalate, pushing copper closer to its performance limits.

Back-end network revenue forecast for 2024-2030; scale-out network revenue rises rapidly, with market opportunity of ~$70 billion in 2030.

For investors, this determines the order of beneficiaries. The first to benefit may not be CPO suppliers, but chip and module companies that enable copper to run faster and further. Once multi-rack clusters become more common, the leverage for optical engines, passive photonics, lasers, and test equipment will become more apparent.

2026-2027 Remains a Copper Window; CPO Explosion Expected Only After 2029

CPO's appeal lies in bringing optical components closer to the switch ASIC or compute chip, reducing the distance high-speed electrical signals travel on the board, thereby improving power consumption and bandwidth density. The challenge is that this is not merely a cable swap; it involves changes in packaging, manufacturing, testing, maintenance, and supply chain responsibilities.

This is why CPO will not see a full-scale explosion in 2026. CPO penetration in scale-out networks will be near zero in 2026-2027, with minor introduction in 2028. Meaningful adoption is expected only in 2029-2030. By then, if the expansion of multi-rack GPU domains proceeds as planned, CPO penetration in scale-out networks could potentially reach 20%-30%.

CPO penetration forecast split by scale-out; CPO in scale-out networks only rises to 20%-30% by 2029-2030.

This leaves at least a two-year window for the copper cabling chain. Astera Labs' Scorpio X-Series has entered initial volume shipments, Broadcom has connectivity opportunities within the AMD MI400/Helios and custom ASIC ecosystem, and Semtech is participating in the transition phase with its CopperEdge low-power copper and linear optics solutions.

More importantly, copper and optics are not a simple replacement relationship. Hyperscalers will mix and match DAC, ACC, AEC, AOC, NPO, and CPO based on distance, power, cost, maintainability, and reliability. Short-distance, intra-rack, and near-rack connections may still extensively use copper, while CPO will handle denser, longer-distance, and higher-power segments.

Nvidia's Roadmap Drives Optical Demand, but Pace Depends on Platform Rollout

CPO becomes truly important in direct relation to Nvidia's next-generation AI platform roadmap.

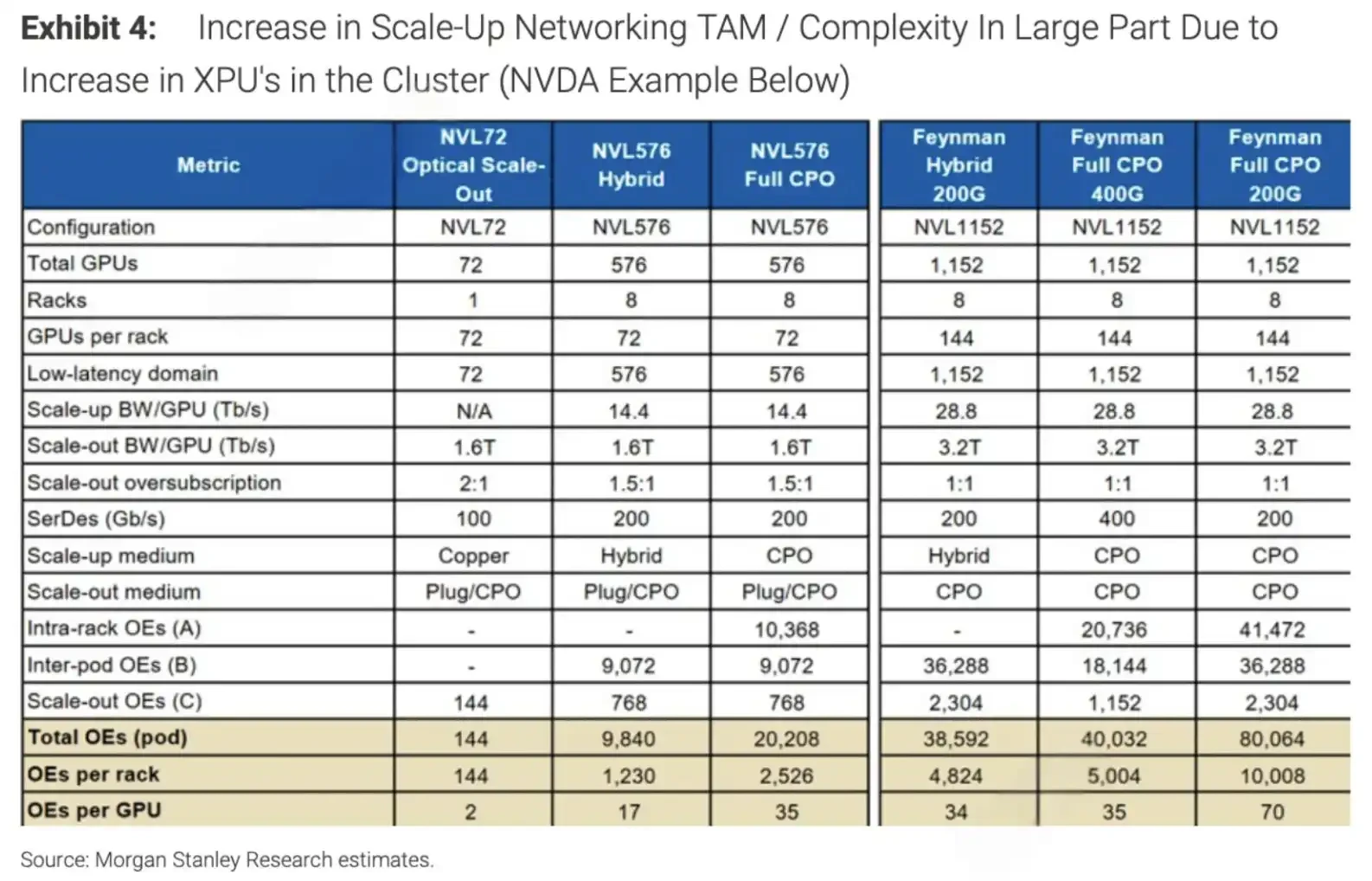

According to Nvidia's official technical blog, the Vera Rubin Ultra NVL576 will combine eight 72-GPU racks into a 576-GPU NVLink domain, using copper and direct optical connections. The Feynman-era Kyber NVL1152 targets even larger scale interconnects, also using similar direct optical solutions.

As GPU domains expand, the demand for optical engines will not just increase linearly. In this report's estimates, the number of optical engines per GPU could rise from the current ~2 to a range of 35-70. That means once the architectural shift occurs, optical content will increase significantly.

Comparison of XPU cluster size and OE demand; GPU domain expands from 72 to 576/1152, OEs per GPU rise from 2 to 17-70.

This is why Corning (GLW), Lumentum (LITE), and Coherent (COHR) are included in this narrative. Corning benefits from passive photonics and glass-based content, while Lumentum and Coherent are more tied to lasers, optical engines, and optical components. After incorporating the adoption rate of scale-out CPO into its model, Morgan Stanley finds that the earnings leverage for these companies depends more on the pace of adoption.

However, this is still leverage contingent on "if adoption occurs," not revenue already realized. Nvidia's roadmap itself faces market divergence, with some industry analysts suggesting potential delays in Kyber or specific Rubin Ultra configurations, while Nvidia maintains its roadmap is unchanged. For the optical chain, the key is not the name of a single product generation, but whether the large GPU domain enters mass production as planned and whether the non-Nvidia XPU ecosystem adopts a similar connectivity path.

Keysight is More Like a 'Pick-and-Shovel Seller'; Test Equipment Bets No Single Route

Within this narrative, Keysight Technologies' (KEYS) logic differs from optical module companies. It doesn't have to bet on whether copper or CPO ultimately wins, because the more diverse the AI network architectures, the higher the demand for test and validation.

The current AI back-end network lacks a unified standard. Nvidia has NVLink and its subsequent expansion roadmap, while the non-Nvidia camp includes UALink, SUE, PCIe, and various hyperscaler proprietary interconnect solutions. Each architecture requires testing for signal integrity, bit error rate, interoperability, power consumption, and reliability.

According to Investing.com, Morgan Stanley has upgraded Keysight from Equalweight to Overweight, raising the price target from $350 to $400, citing AI investments, diversification of network architectures, and increased demand for 800G, 1.6T, and 3.2T testing. Keysight's AI-related revenue accounts for roughly the mid-teens percentage of total revenue.

In contrast, the leverage for optical component companies is more concentrated on CPO adoption rates and the specific platform roadmap. If Nvidia's roadmap progresses smoothly, Corning, Lumentum, and Coherent will benefit more directly; if copper cabling continues to be viable in 2026-2027, the short-term certainty for Astera, Broadcom, and Semtech is actually higher.

CPO Will Eventually Enter a Core Position, but Hyperscalers Aren't Ready for a One-Step Jump

The counterintuitive aspect of this report is that it simultaneously acknowledges CPO will enter a core position long-term while emphasizing that copper cannot be underestimated short-term.

CPO faces significant hurdles. Hyperscalers worry about vendor lock-in; once optics are deeply integrated into switch or compute packages, subsequent replacements, repairs, and multi-vendor sourcing become more complex. Manufacturing yield, thermal management, maintainability, and quality risks also impact the pace of adoption. If the cost premium is not offset by power savings and bandwidth density improvements, adoption will be delayed.

Furthermore, architectural divergence exists. Nvidia's roadmap may drive a higher proportion of optical connections, but self-developed architectures like Google's TPU use different topologies that might reduce reliance on traditional CPO solutions. While the non-Nvidia XPU ecosystem creates opportunities for companies like Broadcom and Astera, the lack of standardization means the supply chain cannot rapidly scale with a single solution.

Therefore, the upward revision to a $70 billion market opportunity more likely reflects an expansion of the total back-end networking pie, rather than a single technology route already securing victory. In 2026-2027, copper will still dominate intra-rack and short-distance scenarios; post-2028, optics begin to enter more core positions; by 2029-2030, CPO may achieve truly meaningful penetration in scale-out networks. The easiest pitfall for the market is to equate "CPO will eventually arrive" directly with "CPO is about to explode."