长鑫IPO在即,韩国国家队入场:存储产业链的钱还能往哪流?

- 核心观点:当前“长鑫概念股”已普涨,但逻辑分化明显:普通DRAM扩产链(设备材料)股价已近历史高点,资金博弈激烈;HBM封装链兑现需待2026年底,位置相对较低。长期资金在高位减持,短线热钱接棒,短期追高风险大于收益。

- 关键要素:

- 长鑫科技2026年Q1营收增长主要靠平均售价(ASP)环比涨57%驱动,位元出货量仅增11%,盈利依赖行业周期而非技术突破。

- 普通DRAM扩产链(如北方华创、华海清科)股价普遍贴近52周高点,逻辑最硬但已充分定价;HBM封装链(如联瑞新材、盛合晶微)距高点仍有约18%空间,兑现节奏更晚。

- 产业资本与国家队在高位减持:兆易创新实控人朱一明减持约633万股,国家大基金对沪硅产业套现约38.82亿元,中央汇金减仓宽基ETF。

- 短线热钱主导定价:北向资金年内加码约4000亿,融资盘规模约2.8万亿,芯片类ETF溢价一度超30%,监管已启动降温措施。

- 中期关注信号:DRAM现货价拐点、长鑫上市后资本开支落地节奏、产业资本减持是否扩大、芯片ETF溢价能否收敛。

Original Author: David, Tide Research

These past two days, good news for the storage sector has been coming one after another.

On June 29, South Korea launched a semiconductor mega-plan totaling over 1,000 trillion won (approximately $650 billion), with an official goal of doubling DRAM production capacity within five years.

Meanwhile, Chinese DRAM leader CXMT has passed its listing review. The market expects it to be listed between mid-July and early August, with institutional valuations ranging from 2 trillion to 4 trillion yuan. Combined with the view that memory manufacturers' supply shortages will persist until 2028, the reasons to be bullish on memory and semiconductors have never been as clear-cut as they are now.

This sentiment has even spilled over to overseas markets.

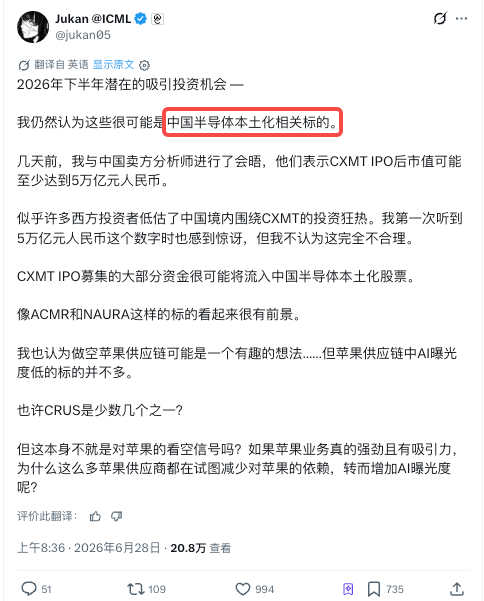

Well-known tech investment blogger Jukan (@jukan05) on X posted that the most worthwhile direction to bet on in the second half of 2026 might still be Chinese semiconductor self-sufficiency targets.

Citing discussions with Chinese sell-side analysts, he claims that CXMT's market cap after its IPO will be at least 5 trillion yuan. Most of the funds raised will flow into stocks related to domestic semiconductor self-sufficiency, so he believes targets like ACMR and NAURA still have prospects.

However, rushing in with this wave isn't necessarily always the best timing.

Currently, nearly 30 CXMT concept stocks on the A-share market have a combined market cap exceeding 1.9 trillion yuan. Most leading stocks across the industrial chain are generally trading near their 52-week highs. Blindly rushing in is certainly not the optimal strategy.

After one round of gains, there are not many segments left where expectations haven't been fully priced in by the market.

Prices Are Rising, But Sales Volume Has Barely Budged

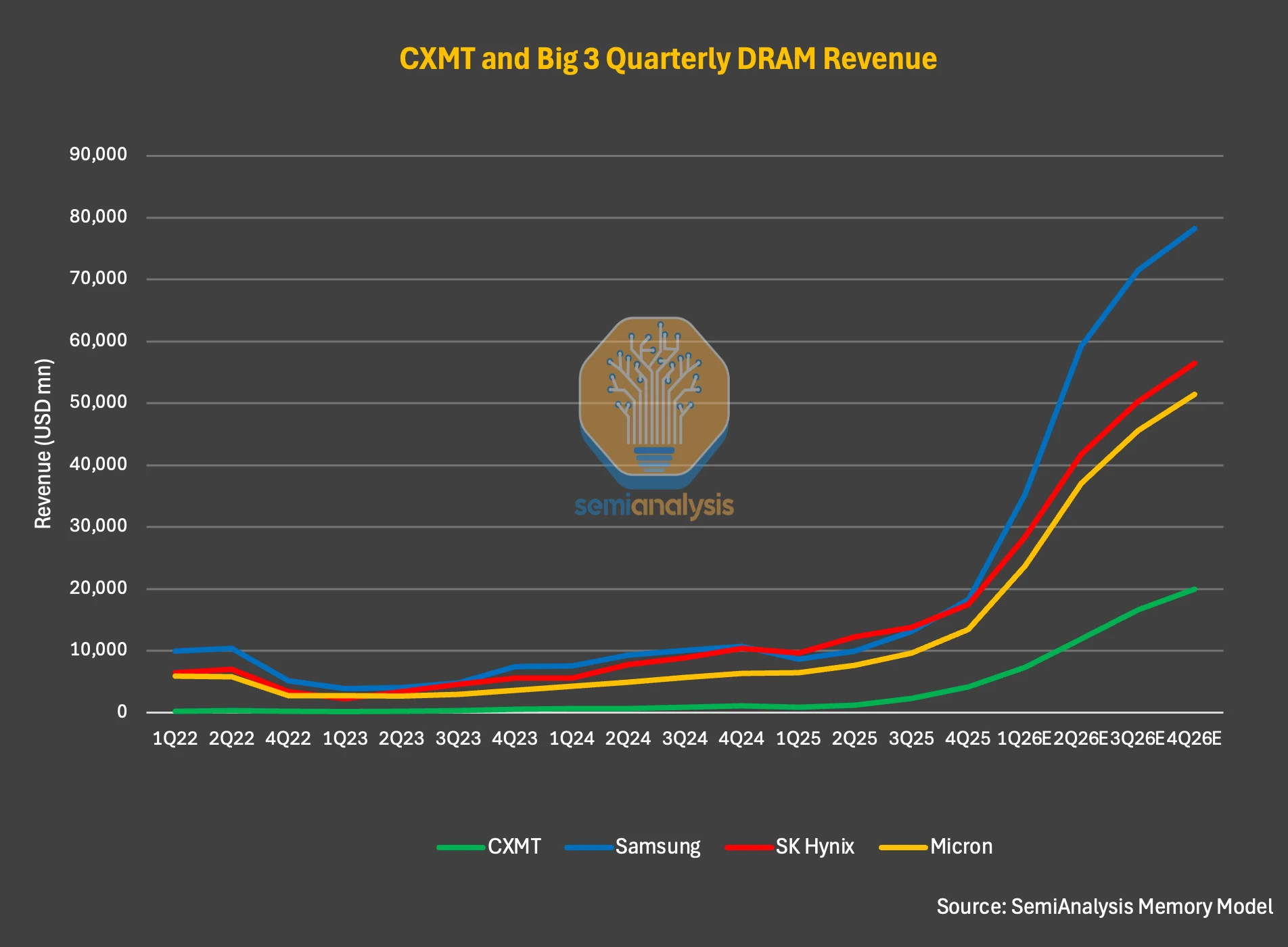

In its June 23 report, "China's CXMT Is Set to Challenge DRAM Incumbents," US semiconductor research firm SemiAnalysis broke down a set of data:

CXMT's bit shipments in Q1 2026 increased only 11% quarter-over-quarter, while its average selling price (ASP) surged approximately 57% quarter-over-quarter. Bit shipments measure the actual sales volume by memory capacity (how much was sold), while ASP measures how expensive it was sold.

Putting these two numbers together means that in this quarter, CXMT sold almost no additional volume; it simply sold its products at a higher price.

Therefore, SemiAnalysis concludes that CXMT's recent profit surge is driven by the industry cycle itself, rather than a breakthrough in technology or market share.

In a pricing cycle, the first to benefit are the original manufacturers selling chips directly – Samsung, SK Hynix, Micron, and CXMT itself. Their profits scale linearly with ASP, making them the group that has risen the most over the past year.

SK Hynix's stock price once surged over 350% this year. But after such gains, expectations for the original manufacturer chain are already well-priced: Samsung and SK Hynix currently trade at forward P/E ratios of only 3 to 5 times. While seemingly cheap, this reflects that the market has already priced in the AI-driven demand and profits expected from 2026 to 2027.

The profits realized through price increases are generally recognized by the market. The situation is similar for the batch of memory original manufacturer and module stocks on the A-share market; their gains have been substantial, leaving little room for new entries. As for the upstream expansion chain (like equipment and materials) and whether it has been bought up to the same levels, we'll examine that using data later without drawing conclusions here.

Overall, CXTM seems to be at a subtle crossroads:

On one hand, selling DRAM and reaping profits from price increases makes it a beneficiary of this cycle. On the other hand, using the 29.5 billion yuan raised in its IPO to expand capacity, buying equipment and materials from upstream suppliers, makes it a spending client.

In the past month or two, a popular sentiment in the market has been to directly "buy CXMT's upstream and downstream." In hindsight, blindly going all-in has indeed generated significant returns. However, at this current level, if one believes the memory and semiconductor rally will continue, it's still necessary to clarify a few things.

First, what exact position does your target occupy in the industry chain, and how does it benefit? Second, is its current price still at the foothills, or has it already climbed halfway up the mountain, or even reached the summit?

Let's address the first question first.

"CXMT concept stock" is an overused label. Breaking it down, the demand driven by CXMT follows two paths, benefiting different sets of companies with different realization timelines.

The first path is the expansion chain for standard DRAM. Currently, 99% of CXMT's shipments are standard DDR and LPDDR. Of the 29.5 billion raised in the IPO, over 22 billion is explicitly allocated for purchasing equipment for wafer lines and technology upgrades. This money first goes to front-end equipment (chip-making machines), the largest portion of expansion investment. Once the lines are running, they continuously consume materials.

Representative companies for the equipment segment include NAURA (002371), AMEC (688012), Piotech (688072), Hwatsing (688120), and ACM Research Shanghai (688082). The materials segment includes Anji Microelectronics (688019), Konfoong Materials (300666), Yoke Technology (002409), and NSIG (688126). This chain benefits from the money CXMT is spending *now*, making their orders the most certain.

The second path is the HBM chain, involving a different group of companies. HBM is the high-bandwidth memory required for AI servers, technically more challenging than standard DRAM. CXMT's HBM technology is still catching up; its production line won't be operational until the end of 2026, lagging behind the standard DRAM expansion. More critically, the value in HBM lies not in front-end etching and deposition, but in the packaging stage – stacking, bonding, and molding multiple chip layers. Therefore, HBM benefits a different set of companies:

Testing equipment (Jingzhida, 688627), packaging materials (Huacheng Technology, 688535; Lianrui New Materials, 688300; Shanghai Xinyang, 300236), and advanced packaging & test firms (SJ Semiconductor, 688820; Tongfu Microelectronics, 002156).

Upstream & Downstream: Is It Lonely at the Top?

Spreading out the targets from the two chains above and sorting them by their current price relative to their one-year highs clearly shows the path capital has swept through. The data below is as of the intraday trading on the 29th.

There's a clear dividing line in the table.

Virtually all equipment and materials for standard DRAM are trading near their 52-week highs, with the distance from their one-year peak mostly within 3%. On June 29, Hwatsing hit its daily limit up, reaching an all-time high. Yoke Technology also hit a new high. Stocks like AMEC, Anji Microelectronics, and NSIG all saw gains around 10%.

This segment is the market's recognized "pick-and-shovel sellers for CXMT's expansion," with the most solid logic and highest certainty. Consequently, capital has priced them most fully. In other words, the certainty of the expansion chain is already reflected in the price.

Lagging behind is the HBM packaging segment.

Lianrui New Materials is still about 18% away from its 52-week high and closed down on June 29. SJ Semiconductor is also about 18% from its high. The packaging/testing firm Tongfu Microelectronics is about 9% from its high. Their gap relative to equipment and materials isn't because they are cheaper or overlooked, but more because their realization timeline is later:

CXMT's HBM production line won't start until the end of 2026. Orders and earnings for these companies will only be truly released after the line runs and yields improve. Their current lower positions correspond to "it's not their turn yet." Viewing them purely as a "bargain" might incur time cost and opportunity cost.

As for the overall conclusion, it's quite clear.

The so-called "buy CXMT's upstream and downstream" strategy at this level is no longer about whether to get on board. We need to see if they are actually at the summit.

Looking purely at prices, the equipment and materials on the standard DRAM side are mostly at their one-year highs. There are no cheap entry points left. The HBM packaging segment is slightly lower, but that requires willingness to wait.

Furthermore, price only answers half of the "is it expensive?" question. The other half, which price itself can't explain, depends on whose money is buying and selling at this level.

Hot Money Supports, While Others Withdraw

The essence here is that pricing power has shifted from long-term, fundamentals-focused capital to short-term hot money riding sentiment.

On one side, industrial capital, the National Integrated Circuit Big Fund, and the "national team" are systematically reducing positions at high levels. On the other side, hot money and retail investors are rushing in, leveraging the AI theme. The former, possibly the most knowledgeable about this business, are selling; the latter, aiming for buying low and selling high, are buying.

Let's look at the side that's withdrawing. We've compiled a list from public information:

- Zhu Yiming, the actual controller of GigaDevice, reduced his holdings by approximately 6.33 million shares from May 11 to 25 (company announcement). He is also the founder and chairman of CXMT. The person most likely to be bullish on the CXMT supply chain reduced holdings of this related leading stock at a high.

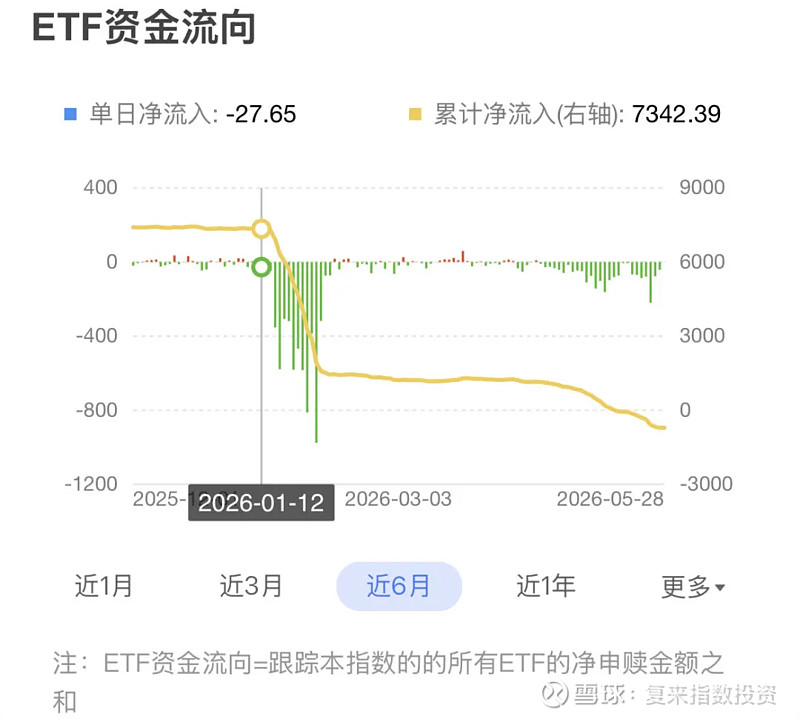

- The National Integrated Circuit Big Fund has been continuously reducing its stake in NSIG since January, cashing out approximately 3.882 billion yuan by early June (company reduction announcement).

- Shareholders of several semiconductor heavyweight stocks, such as Montage Technology, Hygon Information, and Piotech, have reduced their holdings after stock prices surged in 2026 (various company announcements).

- The "national team" (Central Huijin) has sold holdings in broad-based ETFs like the CSI 300 at high levels (according to Caijing's estimates based on Central Huijin's holdings and fund circulation data). They aren't reducing semiconductors specifically, but executing a counter-cyclical retreat from high overall market levels. Semiconductors happen to be the segment with the biggest gains and the most profits to realize.

Source: Fulai Index Investing's Xueqiu Column

The motivations for these reductions are not uniform. The Big Fund inherently has an exit cycle; reducing holdings upon maturity to recoup capital is a standard operation. The national team adjusting its broad-based holdings might be counter-cyclical rebalancing rather than bearishness on a specific sector. Reasons for industrial capital and executive reductions vary.

Interpreting these as "collective bearishness" would be an overstatement, but one thing is certain:

At the current price level, these long-term holders have collectively chosen to realize some profits. Regardless of the motivation, the message conveyed by this action itself is that the current price has reached a level where long-term capital is willing to cash out.

Now, let's look at the side that's buying.

According to market data cited by Sina Finance, the main force behind this tech rally is hot money:

Northbound capital has added approximately 400 billion yuan year-to-date, and the margin trading balance has expanded to about 2.8 trillion yuan. This type of money bets on themes and momentum. Whether a stock is near its 52-week high or has a high P/E ratio doesn't affect their entry; they buy the rise itself.

Regulators have also sensed the overheating and applied the brakes by raising margin requirement ratios and suspending trading for consecutive-limit-up stocks for investigation. Chip ETFs have been frequently suspended due to their market prices far exceeding net asset values, with premiums once exceeding 30%.

Putting the buyers and sellers together, the conclusion is straightforward:

At the current price level, long-term capital related to memory and semiconductors is cashing out in batches, while short-term hot money is taking over. The marginal pricing power is increasingly falling into the hands of sentiment-driven capital.

Note: This does not necessarily mean the rally is topping out immediately. The memory shortage extends to 2028, and CXMT's expansion is real investment. However, most institutions' judgment is that the sector will digest profit-taking through volatile fluctuations and enter a "ranking race" where performance delivery matters more, rather than experiencing a trending decline.

Author's Opinion

Combining the two layers of analysis above with the capital flow dynamics, my inclination is as follows:

Short-term (around CXMT's listing period), sentiment still has inertia. IPO subscription hype and concept fermentation on the listing day could give the sector another surge. However, this is the final leg driven by sentiment; the further it goes, the more it becomes a game of "passing the parcel," where the risk of chasing highs outweighs the reward.

Medium-term (waiting for CXMT's HBM production line to deliver), what's truly worth waiting for is the differentiated delivery between the standard DRAM expansion chain and the HBM chain. Equipment and material orders depend on the speed of capital expenditure deployment post-CXMT listing. The batch of HBM packaging stocks with lower current positions won't see their turn until the production line starts at the end of 2026 and yields improve. Positioning now is a bet on timing.

Key Signals to Watch:

- Inflection point in DRAM spot prices. The foundation of this cycle is price increases. If spot prices turn downward, the original manufacturers and module makers eating the price rise will react first.

- CXMT's capital expenditure pace post-listing. Most order deliveries depend on this data. Only if money is spent quickly can equipment and materials sustain their high valuations.

- Whether reductions by industrial capital and the Big Fund expand. Smart money continuing to exit is