芯片股「黑色星期二」:技术性回调,还是牛市拐点?

- 核心观点:2025年6月23日全球芯片股暴跌并非由韩国“小作文”单方面引发,而是AI板块交易高度拥挤、杠杆脆弱下的必然出清;高盛等机构认为AI叙事未变,此次更偏向技术性回调,但加息、回购静默等压力已积聚,需警惕中期风险。

- 关键要素:

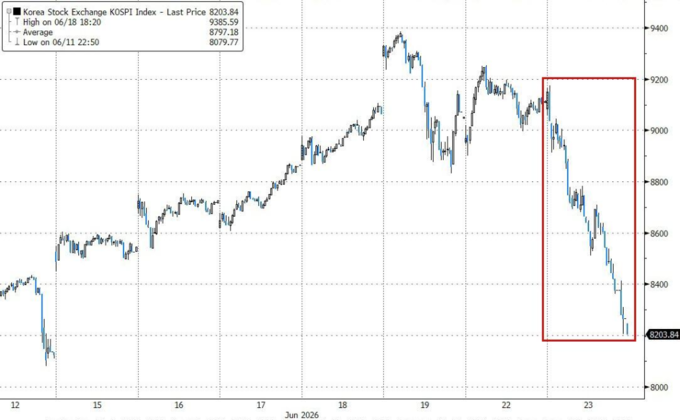

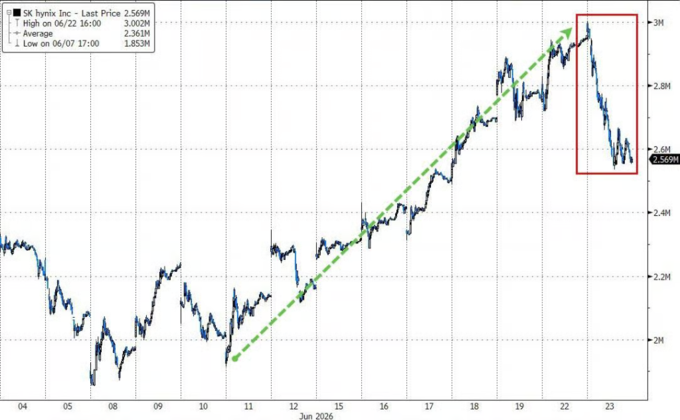

- 韩国KOSPI指数单日暴跌10%,SK海力士(HBM4扩产放缓传闻)与三星电子跌超10%,触发熔断;美股费城半导体指数(SOX)跌7.9%,30只成分股全跌,美光科技跌13%(年内涨超300%)。

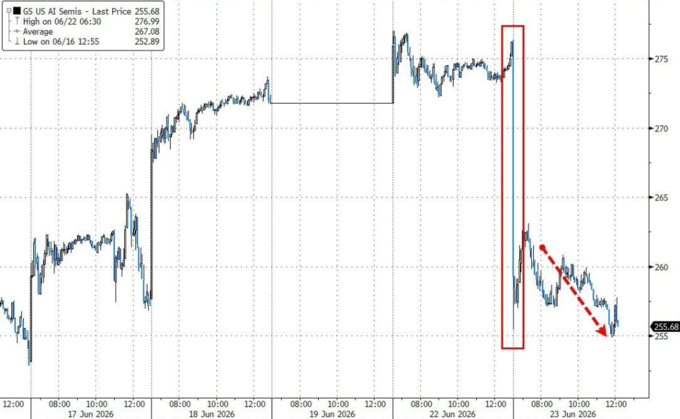

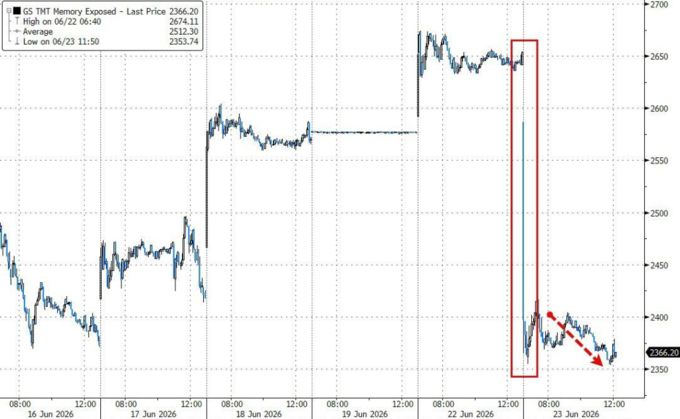

- 高盛指出当日抛售“有序”,成交量持平,投资者交流聚焦盘面而非AI叙事转变,未出现大规模换仓;跌幅集中在“拥挤多头”板块(如高盛存储股篮子跌10%,AI半导体篮子跌620个基点)。

- 结构性风险包括:纳指3月底至今涨超30%,6月费城半导体指数半数交易日波幅超±5%;65%公司处于回购静默期,缺失“托底”力量;美联储加息预期升温(7月概率升至50%),压制高估值科技股。

Original Title: "South Korea Triggers 'Black Tuesday,' Global Chip Stock Bull Market Dealt a 'Blow,' Just a 'Technical Correction'?"

Original Source: Wall Street Street

Behind this plunge in chip stocks is not an accident caused by South Korean 'rumors,' but an inevitable purge resulting from the extreme crowding and fragile leverage in the AI sector. Analysts at Goldman Sachs and others believe the AI narrative has not shifted, and the sell-off was concentrated in crowded long positions, looking more like a 'technical correction.' However, with rising expectations for interest rate hikes and 65% of companies in a buyback blackout period, multiple pressures are building, and the line between a correction and medium-term risk is blurred.

On Tuesday, June 23rd, global chip stocks were caught off guard by South Korea. One Wall Street strategist dubbed the sell-off a 'chip-wreck.'

The first to collapse was South Korea, this year's 'hottest stock market globally.' The country's KOSPI index plummeted 10% in a single day, triggering multiple circuit breakers, with SK Hynix and Samsung Electronics each falling over 10%.

Several 'rumors' ignited the storm: South Korean media reported that Nvidia's Rubin chip production might be cut, and that SK Hynix was slowing the expansion of its high-bandwidth memory (HBM4) production in favor of cheaper standard DRAM. Secondly, Yonhap News reported that lawmakers from multiple parties in South Korea are discussing a tax on unrealized gains from stocks, real estate, and other assets – meaning taxes would be owed even on paper profits not yet realized through a sale.

This 'chip earthquake' then spread to U.S. stocks.

Overnight, the Philadelphia Semiconductor Index (SOX) fell 7.9%, with all 30 component stocks declining without exception. Micron Technology fell 13% – before Tuesday, it was up over 300% year-to-date, making it the strongest component in the SOX. Micron, Nvidia, and AMD combined contributed roughly half of the S&P 500's total decline. The Nasdaq fell 3.3%, the Dow Jones edged down only 0.1%, and the S&P 500 fell 1.4%.

Jonathan Krinsky, Chief Market Technician at BTIG LLC, stated: "Regardless of a potential short-term rebound, we still see medium-term downside risk in the Tech/AI space." He believes the semiconductor sector still has 10% to 15% downside, describing Tuesday's action as a "Chip-Wreck."

However, Peter Callahan, TMT specialist at Goldman Sachs Global Banking & Markets, wrote in a flash note on June 24th: "Most of the investor conversations today were around the theme of 'what are you seeing on your side,' rather than signs of a broader narrative shift." This statement is crucial. It puts a boundary around the sell-off: the market looked ugly, but at least on that day, there was no evidence of capital fully abandoning the AI trade.

So, the issue isn't simply that "a rumor from South Korea crashed the global AI bull market." It looks more like an already crowded, fully-priced sector with significant leverage hitting a trigger and undergoing collective risk reduction. In the short term, it indeed bears the characteristics of a 'technical correction'; in the medium term, the vulnerabilities of the AI trade have not disappeared.

This is a Contagion, Not an Accident

South Korea's crash may seem sudden, but the logic behind it isn't complex.

The news of SK Hynix slowing its HBM4 expansion crushed its stock. Given SK Hynix's weight in the Korean stock market, similar to Apple's weight in the Nasdaq, its problems dragged down the entire index. More critically, Korean retail investors heavily use leveraged ETFs to participate in AI/semiconductor trades. When the market falls, these products are forced to sell to maintain their leverage ratios, creating mechanical selling pressure.

The news was the trigger; the leverage structure was the explosive. Meanwhile, some market observers asked: "Could leveraged South Korean retail investors be the terminators of the US tech bull market?"

While admittedly hyperbolic, the question points to a real vulnerability: AI/semiconductor trades are highly concentrated, and global investor portfolios are startlingly similar. Selling pressure at any one point can easily propagate along this chain.

According to Goldman Sachs' post-market data, both longs and shorts were selling that day: long-only funds (LO) showed a selling skew of -18%, while hedge funds (HF) also sold consistently throughout the day, with short positions accounting for 60% of sales volume (compared to a recent average of about 50%). The selling by both institution types exceeded $1 billion in notional exposure.

The US stocks that fell the most were the 'crowded longs,' the stocks that were 'most profitable this year': Goldman Sachs' memory stock basket (GSTMTMEM) fell 10%, its AI semiconductor basket (GSCBSMHX) dropped 620 basis points, its AI stock basket (GSTMTAIP) fell 440 basis points, and its basket of past 12-month momentum stocks (GSXHUHMOM) dropped 420 basis points.

Technical Correction? Goldman Sachs: Narrative Has Not Shifted

Given the magnitude of the sell-off, how does the market view it? Looking only at the decline, Tuesday resembles a repricing of the AI trade. However, the volume and capital flow data suggest a less definitive conclusion.

Goldman Sachs TMT desk expert Peter Callahan wrote in the post-market flash note that the day's feeling could be described as 'orderly' – despite significant declines, Nasdaq volume was roughly in line with the 20-day average, and the cash and vol desks operated normally.

More importantly, he described the investor conversations: "Most of the investor conversations today were around the theme of 'what are you seeing on your side,' rather than signs of a broader narrative shift. There was no material uptick in inquiries about 'new names' or 'laggards.'"

In other words, nobody was rotating. Nobody was looking for new investment directions. Everyone was just trying to get a sense of the situation.

Another Goldman Sachs strategist, Chris Hussey, provided specific data: Of the 12 tech stocks that fell over 8% on Tuesday, all but one are still up double-digits year-to-date, with many having more than doubled. His assessment:

"Today's sell-off feels more like a 'skimming off the froth' from a feverish stock price rally, rather than a fundamental reassessment of the AI infrastructure trade. Investors weren't broadly dumping the index; they were re-evaluating: for stocks that have doubled in six months, how much should one actually pay?"

Jack Janasiewicz, portfolio manager at Natixis Advisors, had a similar view:

"This looks more like a technical sell-off than anything else. Market breadth was decent at the open, despite many red numbers – a signal of a narrow sell-off." He also cautioned, "When you see such massive crowding in beta and momentum, it easily leads to an ugly deleveraging event."

The Flip Side of 'Technical Correction': Structural Concerns That Can't Be Ignored

The term 'technical correction' sounds reassuring, but it can explain everything and also mask real risks. The tape certainly had technical features: the decline was concentrated in winning stocks, volume didn't spiral out of control, and investor conversations didn't immediately flip the AI narrative. However, there isn't a clear wall between a technical correction and structural risk – the former, if severe enough, can easily morph into the latter.

Several background numbers are worth considering together.

First, the rally was too fast. The Nasdaq has risen over 30% from its late March low. In June alone, the Philadelphia Semiconductor Index had 8 trading days (out of 16) with single-day swings exceeding ±5% – meaning half of June's trading sessions saw wild chip stock volatility. Even after Tuesday's fall, the SOX is still up about 5% for the month, outperforming the Nasdaq and S&P 500 by roughly 8 percentage points. A pullback from these levels has both technical correction justifications and the fragility of lofty heights.

Second, positions are too crowded, and the usual support is absent. Julian Emmanuel, Chief Equity & Quant Strategist at Evercore ISI, told Bloomberg TV: "People are looking for reasons to hedge while simultaneously wanting to stay invested." This aptly describes the current market's ambivalence. Meanwhile, 65% of US-listed companies are currently in their buyback blackout periods. In past sell-offs, corporate buybacks were a critical support, but that lever is unavailable this time.

Third, the macro backdrop is shifting. Expectations for Fed rate hikes are rising rapidly – Bank of America expects three more hikes by year-end, and market pricing for a July hike has jumped from near zero to ~50%. The valuation logic for high-growth tech stocks relies on discounting future cash flows at low interest rates. As rates rise, the present value of distant earnings naturally contracts, hitting stocks reliant on future expectations the hardest.

Michael O'Rourke, Chief Market Strategist at JonesTrading Institutional Services, wrote: "Hyperscalers are the new software stocks. This group is dragging down the 'Magnificent Seven' but cannot escape their own troubles."

Torsten Slok, Chief Economist at Apollo, listed three key questions facing the market: What happens if AI companies start cutting their compute budgets due to insufficient ROI? If the Fed raises rates in September and December, what are the implications for equities and credit? These questions have no simple answers, but the market is shifting from 'willing to ignore these risks' to 'beginning to take them seriously.'

The reason a technical correction deserves serious attention is not the drop itself, but because it occurs when valuations, positioning, interest rates, and sentiment are all at extremes.

Historically, South Korean Crashes Are Brief – And the Next Test is Micron

Historical data show that sharp declines in the South Korean stock market, while severe, tend to be brief. This is the 'silver lining' that bulls often cite.

However, this time's context differs from purely domestic South Korean events: it touches the core nerve of the global AI trade – is memory chip demand really as strong as anticipated? Has the frenzy of data center construction already borrowed from the future?

These questions will be partially answered following Micron's earnings report on Wednesday. Micron was the strongest component in the SOX this year, up over 300% before Tuesday. The report will be a true test of the sector's resilience.

BTIG's Krinsky perhaps put it most succinctly: "Regardless of a short-term rebound or not, the medium-term downside risk for semiconductors remains."