Oracle 财报背后:AI 云订单爆表后,钱从哪里赚回来?

- 核心观点:甲骨文(Oracle)的核心矛盾已从“有无AI故事”转向“AI故事的成本与回报”,其5530亿美元的RPO(剩余绩效义务)虽彰显强劲需求,但市场正密切关注巨额资本开支(CapEx)能否转化为高质量的利润和自由现金流。

- 关键要素:

- Q4财报市场预期:营收约191亿美元,调整后EPS约1.96美元;总云收入指引同比增长46%—50%。这是衡量业绩是否达标的基础。

- RPO达5530亿美元,同比增长325%:代表已签但未确认收入的合同规模,是未来收入的“能见度”指标,但高RPO也意味着巨大的交付压力和前置资本投入需求。

- 核心矛盾:AI云基础设施是重资产模式,需要提前投入数据中心、GPU及电力等,高CapEx正在改变公司财务结构,市场担忧其可能从高现金流软件公司变为资本消耗体。

- 财报关键看点:云收入是否接近指引上沿、RPO是否继续扩张、FY2027收入指引强弱,以及管理层对CapEx节奏、现金流改善路径的清晰阐述。

The problem with Oracle is not the absence of an AI narrative, but that this narrative has become expensive enough.

After the US stock market closes on June 10, Oracle will release its FY2026 Q4 earnings report. The market currently expects Q4 revenue of approximately $191 billion and adjusted EPS of around $1.96. In the previous quarter, Oracle provided Q4 guidance of total revenue growth of 19%-21% year-over-year, total cloud revenue growth of 46%-50%, and non-GAAP EPS of $1.96-$2.00.

Looking at these numbers alone, Oracle remains firmly within the AI cloud narrative.

At the same time, over the past year, OCI, AI cloud orders, large customer contracts, data center expansion, and market expectations surrounding clients like OpenAI, Meta, and NVIDIA have recast Oracle from a traditional database and enterprise software company into the trading framework of AI infrastructure.

But for this earnings report, what the market truly needs to see is no longer whether Oracle has an AI narrative, but whether the AI cloud orders are so large that they justify the substantial capital expenditures Oracle is undertaking.

1. By the Numbers, Oracle Has Already Taken Its Seat at the AI Cloud Table

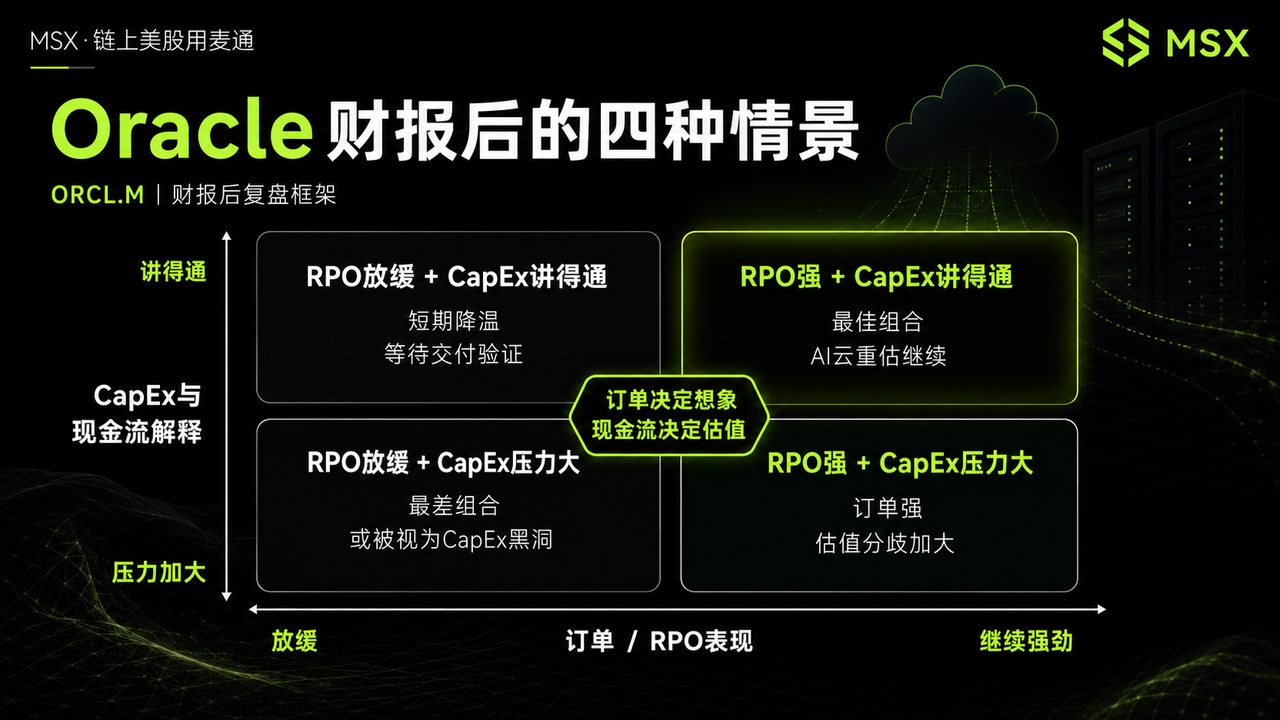

The most striking data from Oracle's previous quarter was undoubtedly its RPO reaching $553 billion, a year-over-year increase of 325%.

RPO can be simply understood as the total value of contracts signed but not yet recognized as revenue. For cloud computing companies, a larger RPO typically signifies higher future revenue visibility and, overall, serves as a concentrated indicator of demand sentiment and reserved computing capacity.

This is precisely why, after Oracle disclosed its RPO last quarter, the market quickly included it as a core player in the AI cloud infrastructure space.

However, it's important to note that RPO is not profit, nor is it immediate cash flow. Instead, it's more like a massive order book—the thicker the book, the stronger the demand, but investors will continue to ask three more pragmatic questions: When will these orders be delivered? How much capital needs to be fronted before delivery? Will the gross margins and cash recovery speed be satisfactory afterward?

This is the core divergence surrounding Oracle now.

- Bulls argue that the $553 billion RPO proves AI cloud demand is real, long-term, and secured by large clients, positioning Oracle as a key capacity provider during a period of tight AI computing supply.

- Bears, however, worry that if fulfilling these orders requires massive data center investment, GPU procurement, power resources, and long-term financing, then a higher RPO could increase pressure on short-term free cash flow and the balance sheet.

Therefore, Oracle's RPO itself is not the problem.

The real question is how quickly RPO can be converted into revenue, and at what profit margins and cash flow quality it translates into shareholder value.

This brings us to the first key focus of this earnings report: whether RPO continues to expand and whether management can provide a clearer timeline for order fulfillment. If RPO hits new highs, it indicates large AI cloud contracts are still flowing in, further enhancing Oracle's future revenue visibility. Conversely, a significant slowdown in RPO growth might lead the market to worry that the peak of AI cloud orders is temporarily passing.

Orders are the starting point of the story, not the endpoint.

For the current Oracle, the market acknowledges it has secured a ticket to the AI cloud. The next step is to see if it can turn that ticket into real revenue, profits, and cash flow.

2. The Expensive Story: The CapEx Pressure Behind OCI Growth

Oracle's most core label has historically been databases and enterprise software.

But now, the market is far more focused on OCI, or Oracle Cloud Infrastructure.

Last quarter, Oracle guided for Q4 total cloud revenue growth of 46%-50% year-over-year. If this quarter's cloud revenue meets or exceeds the high end of the guidance, it suggests AI cloud demand remains robust and OCI's growth trajectory hasn't slowed significantly. However, if cloud revenue falls short of expectations, the market will start to worry that despite the large RPO, the pace of order conversion and delivery might be slower than anticipated.

This also highlights the biggest difference between AI cloud and traditional software.

Traditional software companies have low marginal costs, making it easier for revenue growth to translate into profit. AI cloud infrastructure, however, is not a capital-light business. It requires building data centers in advance, procuring GPUs, and securing capabilities in power, land, cooling, networking, and operations.

Orders can be signed quickly, but data centers cannot be built overnight, GPUs do not arrive automatically, and power capacity is not always readily available.

Therefore, Oracle's biggest bottleneck now may not be a lack of demand, but rather a lack of sufficient capacity to meet that demand.

This is also why the market has become more critical of Oracle.

For a pure software company, new revenue typically generates high incremental margins. But as Oracle is increasingly priced by the market as an AI cloud infrastructure company, it must submit to a different set of evaluation criteria: capital expenditure intensity, asset turnover efficiency, depreciation pressure, financing costs, free cash flow, and long-term return on investment.

In other words, Oracle hasn't simply upgraded from a "software company" to an "AI company." It is more akin to transforming from a high-cash-flow enterprise software firm into a company that simultaneously operates a software business and a capital-heavy AI cloud business. The valuation logic has shifted, and the market will naturally reprice it accordingly.

This is a key reason for the pressure on Oracle's stock price over the past period. The market does not deny the existence of AI cloud demand; it worries about whether Oracle will take on excessive capital expenditure pressure in its pursuit of orders.

Therefore, in this earnings report, management must address several questions:

- How much higher will future CapEx go?

- Can data center construction keep pace with orders?

- Are the gross margins on AI cloud contracts solid enough?

- When will free cash flow improve?

- Are financing costs and balance sheet pressure manageable?

These questions are more critical than simple revenue and EPS figures. Oracle's trading focus has shifted from "Does it have AI orders?" to "Can these AI orders generate sufficient returns on capital?"

If management merely continues to emphasize strong orders, it may no longer be enough. What the market truly wants to hear is how quickly Oracle can turn these orders into revenue-generating cloud capacity and whether this cloud capacity can ultimately produce high-quality cash flow.

3. AI Cloud Dark Horse, or CapEx Black Hole?

This Oracle earnings report is, in essence, a test of AI cloud capital returns.

From a data perspective, the market will first look at whether Q4 revenue and EPS meet expectations. The market consensus is for revenue of approximately $191 billion and EPS of around $1.96. Merely meeting these estimates may not be enough to alleviate concerns about CapEx. A clear beat, especially with strong cloud revenue and earnings quality, would provide stronger support for the stock price.

Secondly, the focus will be on whether cloud revenue meets or exceeds the high end of the guidance. Last quarter, Oracle guided for Q4 total cloud revenue growth of 46%-50% year-over-year. This is a key metric to determine if OCI is still accelerating. Revenue near or above the high end would confirm AI cloud demand is materializing; lower-than-expected numbers would lead the market to re-evaluate the RPO conversion pace.

Thirdly, the market will watch for continued RPO expansion. New highs in RPO signal ongoing inflows of large AI cloud contracts, boosting future revenue visibility. A significant slowdown in RPO growth, however, might raise fears that the peak of AI cloud orders is passing.

Fourthly, the focus will be on whether FY2027 revenue guidance is strengthened. The market is highly focused on Oracle's revenue visibility for the coming year. If management can reinforce the growth trajectory of AI cloud and order conversion, Oracle's AI cloud logic becomes more stable. Conversely, weak forward guidance could lead the market to believe that current valuations already price in too much optimism.

Finally, and most importantly, is the explanation of CapEx and cash flow metrics. Oracle must demonstrate that its current high spending is not just chasing an AI trend but will ultimately translate into higher revenue, better margins, and more stable cash flow in the future.

If management can clearly articulate the CapEx cadence, data center delivery schedule, customer demand dynamics, financing arrangements, and the path to free cash flow improvement, market concerns about Oracle will likely ease. However, if these issues remain vague, the stock price may continue to fluctuate on the tension between "growth" and "cash burn."

This is the crux of the major disagreement surrounding Oracle.

Bulls believe Oracle is becoming a capacity provider for the AI cloud era. In the context of tight AI computing supply, the ability to provide stable and scalable cloud capacity secures large client orders and long-term revenue visibility. Oracle's advantage lies in its established enterprise client base, its portfolio of database and cloud services, and the substantial order book it has secured during the AI demand surge.

From this perspective, Oracle is no longer just a traditional software company but a crucial link in the AI infrastructure chain.

However, Bears worry that Oracle is trading growth for increasingly higher capital expenditures. AI cloud is not a capital-light business. Data centers face potential delays, power and GPU supply may be constrained, depreciation and financing costs can rise, and free cash flow may remain under pressure. If order delivery falls short of expectations or gross margins are lower than imagined, Oracle's AI cloud story could shift from "high growth" to "high spending, low returns."

Neither side is entirely without merit.

The bull case for Oracle rests on real AI cloud demand, extremely strong RPO, fast OCI growth, and long-term revenue visibility secured by large client orders. The bear case focuses on the capital-intensive nature of the AI cloud business altering the company's financial structure, requiring the market to reassess its cash flow quality and capital return capabilities.

This Oracle earnings report is not a proof of the AI story, but rather a proof of the return on capital expenditure.

If RPO continues to expand, cloud revenue maintains high growth, management strengthens future revenue visibility, and CapEx, cash flow, and financing plans are clearly addressed, then Oracle's AI cloud story can continue to be told.

But if growth remains primarily at the order level while delivery, cash flow, and CapEx pressures persist, the market will rightly question whether this is an AI cloud dark horse or a CapEx black hole.

In a nutshell, Oracle only needs to prove that these orders are worth the money it's burning.