CEX กำลังหันไปหุ้น เหรียญ Altcoin ถูกทอดทิ้งแล้วหรือ?

- มุมมองหลัก: การแลกเปลี่ยนคริปโตเคอเรนซีชั้นนำของโลก (Binance, Bybit, Coinbase, Kraken) กำลังเปลี่ยนแปลงรูปแบบเป็นแพลตฟอร์มการเงินแบบครบวงจรที่ให้บริการทางการเงินแบบดั้งเดิม เช่น หุ้นและตราสารอนุพันธ์ เนื่องจากการลดลงของปริมาณการซื้อขาย การไหลออกของสภาพคล่องบนเชน (เช่น Hyperliquid) และกฎระเบียบที่ผ่อนคลายลง ซึ่งอาจทำให้โปรเจกต์ Altcoin สูญเสียการสนับสนุนสภาพคล่องจากการแลกเปลี่ยน และเร่งให้เกิดการแบ่งแยกในอุตสาหกรรม

- ปัจจัยสำคัญ:

- ปริมาณการซื้อขายสปอตเฉลี่ยรายวันของ Binance ลดลงจากจุดสูงสุดประมาณ 45,000 ล้านดอลลาร์ในเดือนตุลาคม 2025 เหลือ 7,700 ล้านดอลลาร์ ลดลงเกือบ 80% ซึ่งเน้นย้ำว่ารูปแบบค่าธรรมเนียมแบบดั้งเดิมถึงจุดอิ่มตัวแล้ว

- ใน 30 สินทรัพย์ที่มีปริมาณการซื้อขายสัญญาซื้อขายล่วงหน้า (Perpetual) สูงที่สุดบน Hyperliquid นั้น 23 รายการเป็นหุ้นและสินค้าโภคภัณฑ์ ซึ่งแสดงให้เห็นว่าสภาพคล่องบนเชนกำลังเปลี่ยนจากคริปโตเคอเรนซีไปสู่สินทรัพย์แบบดั้งเดิม

- Binance ให้บริการซื้อขายหุ้นสหรัฐฯ โดยอ้อมผ่านนายหน้า Nest Trading ที่มีใบอนุญาตในอาบูดาบี เพื่อหลีกเลี่ยงกฎหมายหลักทรัพย์ และได้รับส่วนแบ่ง 50% ของค่าธรรมเนียมคำสั่งซื้อขาย

- Coinbase เข้าซื้อ Deribit ด้วยมูลค่า 2.9 พันล้านดอลลาร์ ได้รับส่วนแบ่งตลาดออปชันคริปโตประมาณ 85% และเปิดตัวการซื้อขายหุ้นแบบไม่มีค่าคอมมิชชั่น เพื่อเสริมความแข็งแกร่งให้กับบริการสำหรับสถาบัน

- Kraken เข้าซื้อ NinjaTrader และ Bitnomial ได้รับใบอนุญาตนายหน้าซื้อขายฟิวเจอร์ส และยื่นขอใบอนุญาตทรัสต์แห่งชาติกับสำนักงานผู้ควบคุมเงินตราแห่งสหรัฐอเมริกา (OCC) โดยมีเป้าหมายที่จะเป็นธนาคารคริปโตที่ได้รับอนุญาตจากรัฐบาลกลาง

- กลยุทธ์หลักของแต่ละการแลกเปลี่ยนล้วนแสดงให้เห็นว่า Altcoin ไม่ได้อยู่ในตำแหน่งสำคัญของแผนการพัฒนาอีกต่อไป ทรัพยากรของแพลตฟอร์มกำลังเปลี่ยนไปสู่การเงินแบบดั้งเดิมและการกระจายรายได้อย่างเต็มรูปแบบ

Original Author: Henry Kim, Ryan Yoon

Original Translation: Chopper, Foresight News

TL;DR:

- The growth model for crypto spot trading fee revenue has peaked. The rise of decentralized perpetual exchanges like Hyperliquid, combined with a looser regulatory environment under the Trump administration, has prompted leading global crypto exchanges to realign their development strategies.

- Exchanges are now expanding into traditional financial sectors like stocks and financial derivatives, with their operational models increasingly resembling traditional financial institutions.

- However, a problem arises: centralized exchanges have always been the core liquidity providers for the entire crypto ecosystem. If exchanges gradually de-emphasize their core crypto business, the existing operational order of the broader crypto market could be fundamentally disrupted.

- Crypto projects will henceforth enter a phase of self-reliance. Whether they can operate independently without exchange support will become a defining watershed, leading to a clear divergence in the industry landscape.

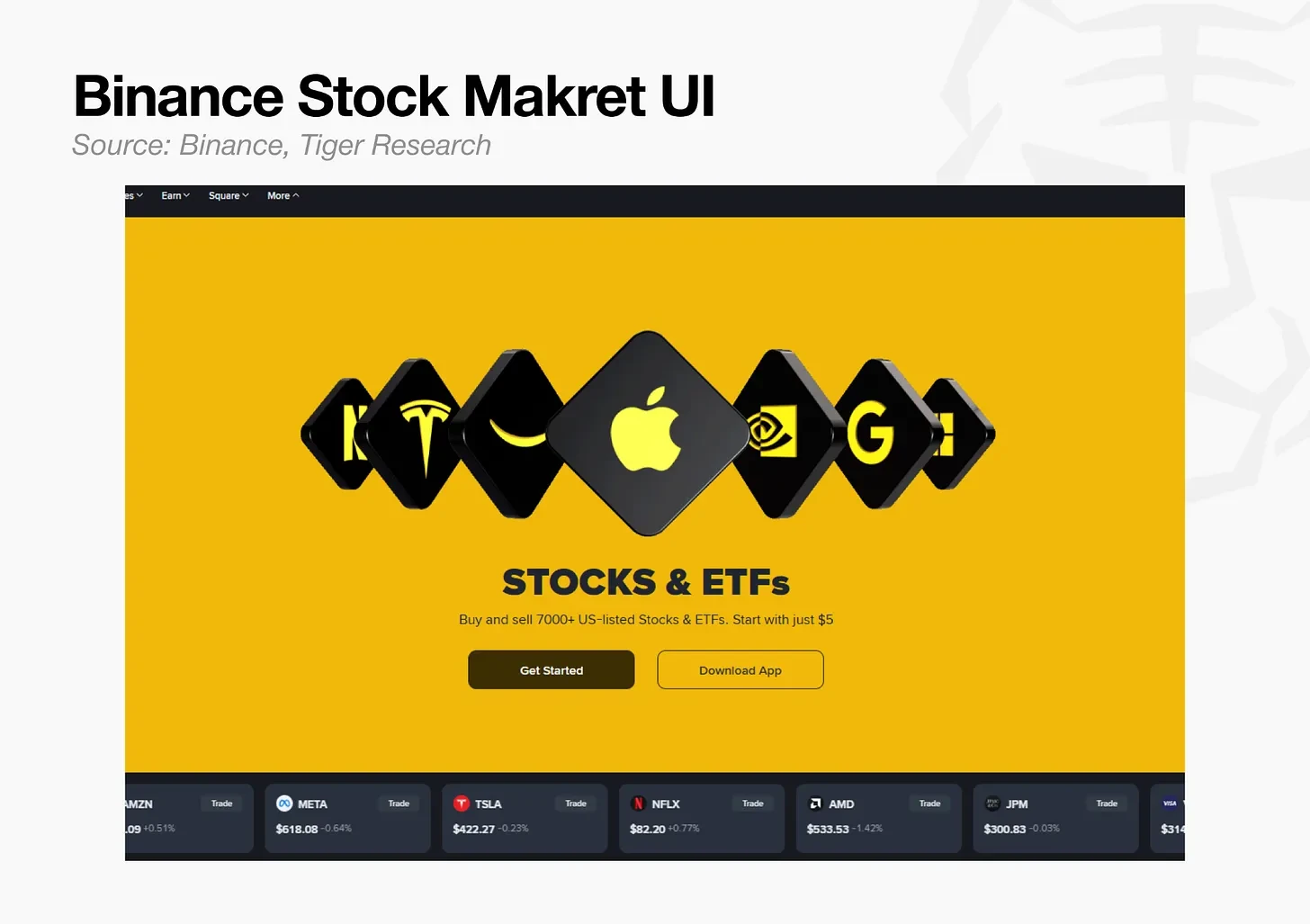

Trading Apple Stock on Binance

Starting June 1st, users can directly trade US stocks like Apple (AAPL) and Alphabet (GOOGL) through the Binance App. The following day, Binance announced the addition of trading for components of the Korea Composite Stock Price Index, including the three most actively traded Korean stocks: SK Hynix, Samsung Electronics, and Hyundai Motor.

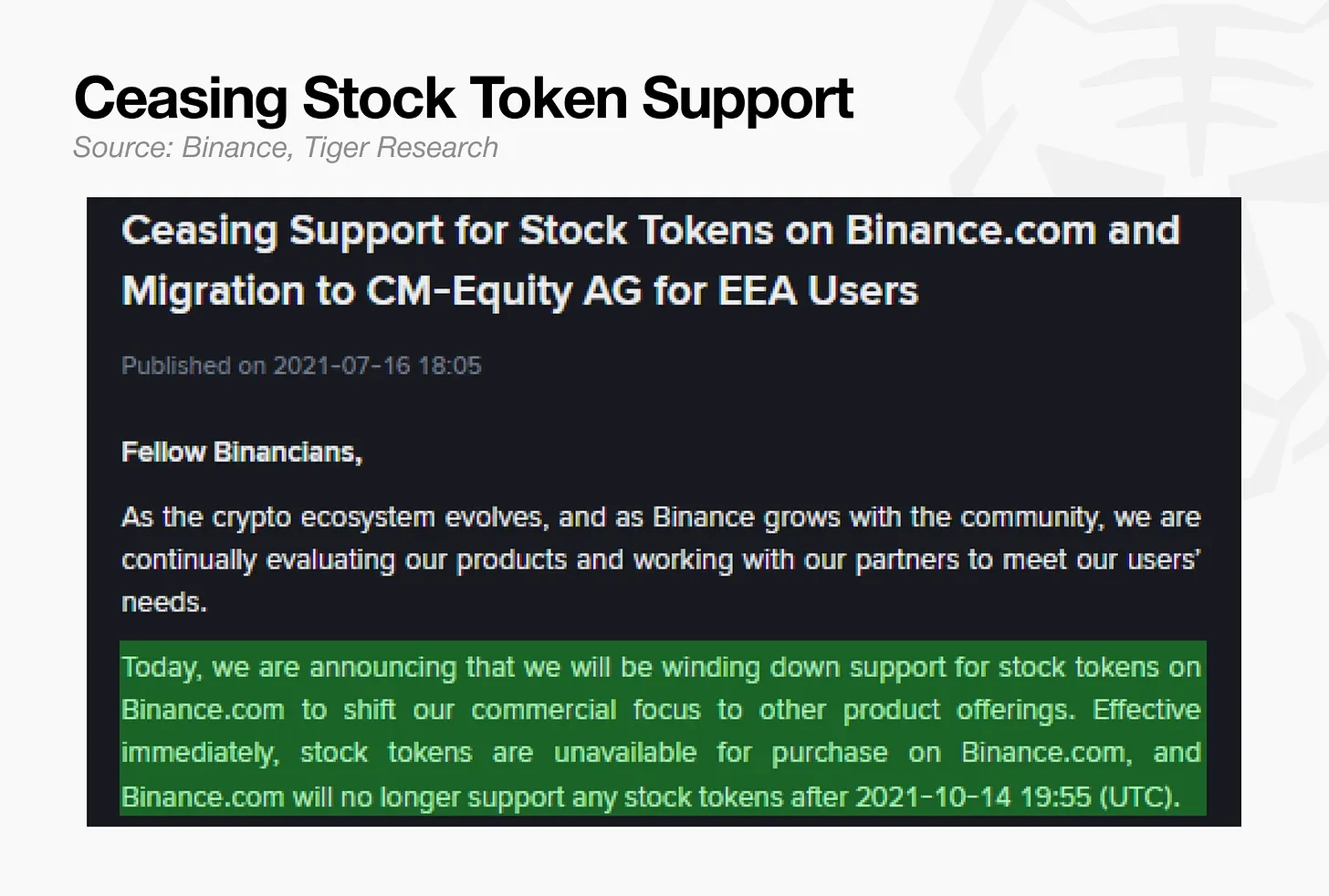

Binance's ambition to offer stock trading dates back to 2021. In April of that year, the platform launched tokenized stock trading, supporting stocks like Tesla (TSLA), Apple (AAPL), and Microsoft (MSFT). However, due to intensifying regulatory pressure, this service was fully discontinued in July of the same year. The business faced three major structural hurdles that made it unsustainable: the legal classification of stock tokens – whether securities or derivatives – remained ambiguous; the products lacked an investor prospectus as required by EU regulations; and Binance itself did not hold the direct licenses to operate such a business. Regulators including Germany's BaFin, the UK's FCA, and Hong Kong's SFC all raised objections based on these issues.

With the re-launch of stock trading services, the overall structure has been significantly revamped. Binance now executes orders through a licensed broker in the Abu Dhabi Global Market. The service is explicitly defined as a securities brokerage, completely bypassing the previous legal controversies. The core conflict that led to the 2021 shutdown – the ambiguity surrounding the issuer of the underlying assets – has also been largely resolved.

This wave of industry action shows a clear temporal overlap. Concurrently, Bybit launched perpetual contract markets for traditional financial instruments, listing contracts not only for Korean stocks like SK Hynix and Samsung Electronics but also for SpaceX (SPCX). Coinbase quickly followed suit, announcing support for SPCX contract trading.

The collective pivot by major crypto exchanges – moving away from a single-crypto trading model towards comprehensive traditional financial service platforms – warrants a deeper look into the underlying reasons.

Three Drivers of the Transformation

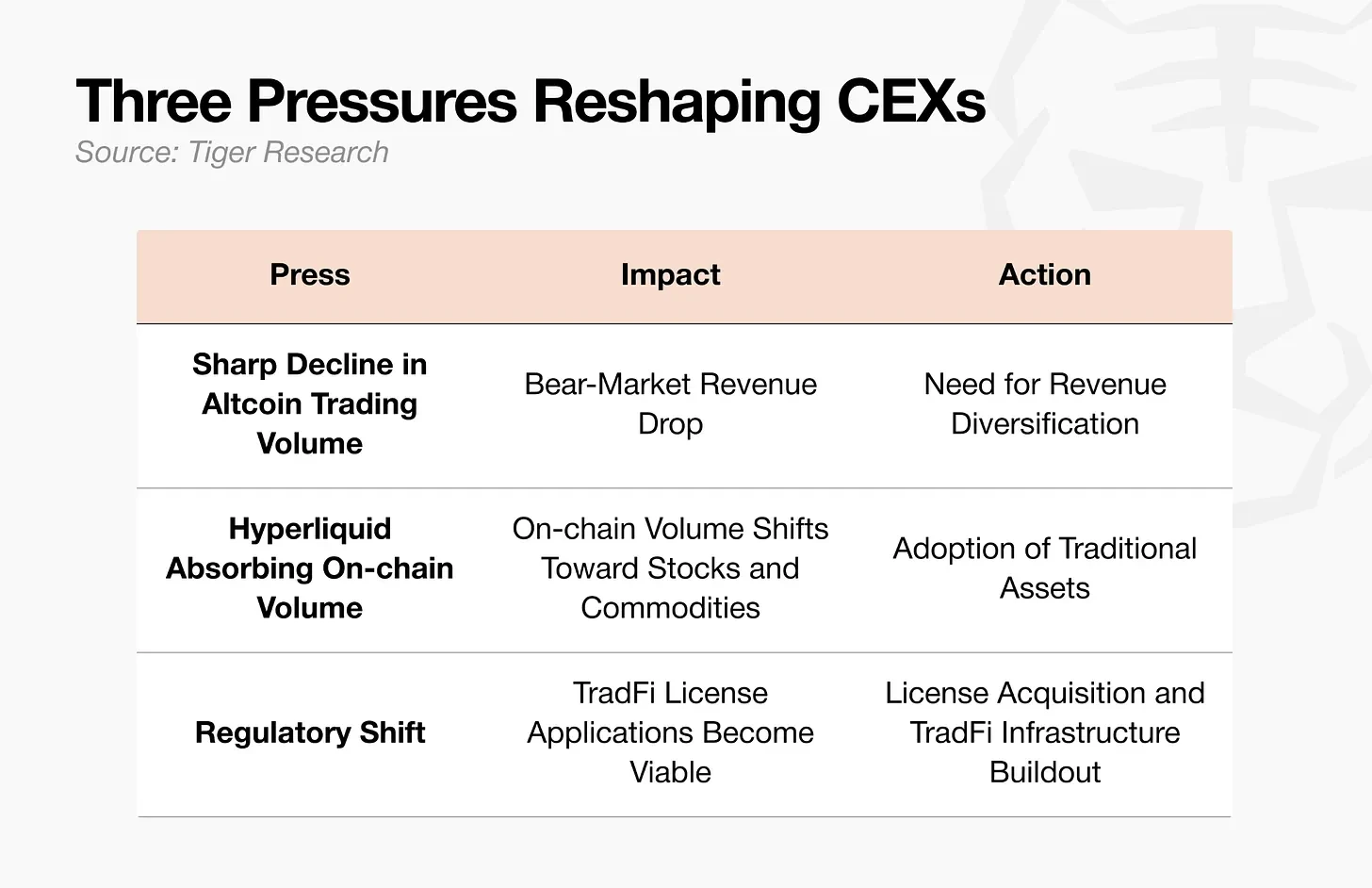

Three external pressures are collectively pushing exchanges away from a pure crypto operational model.

Declining Crypto Trading Volume

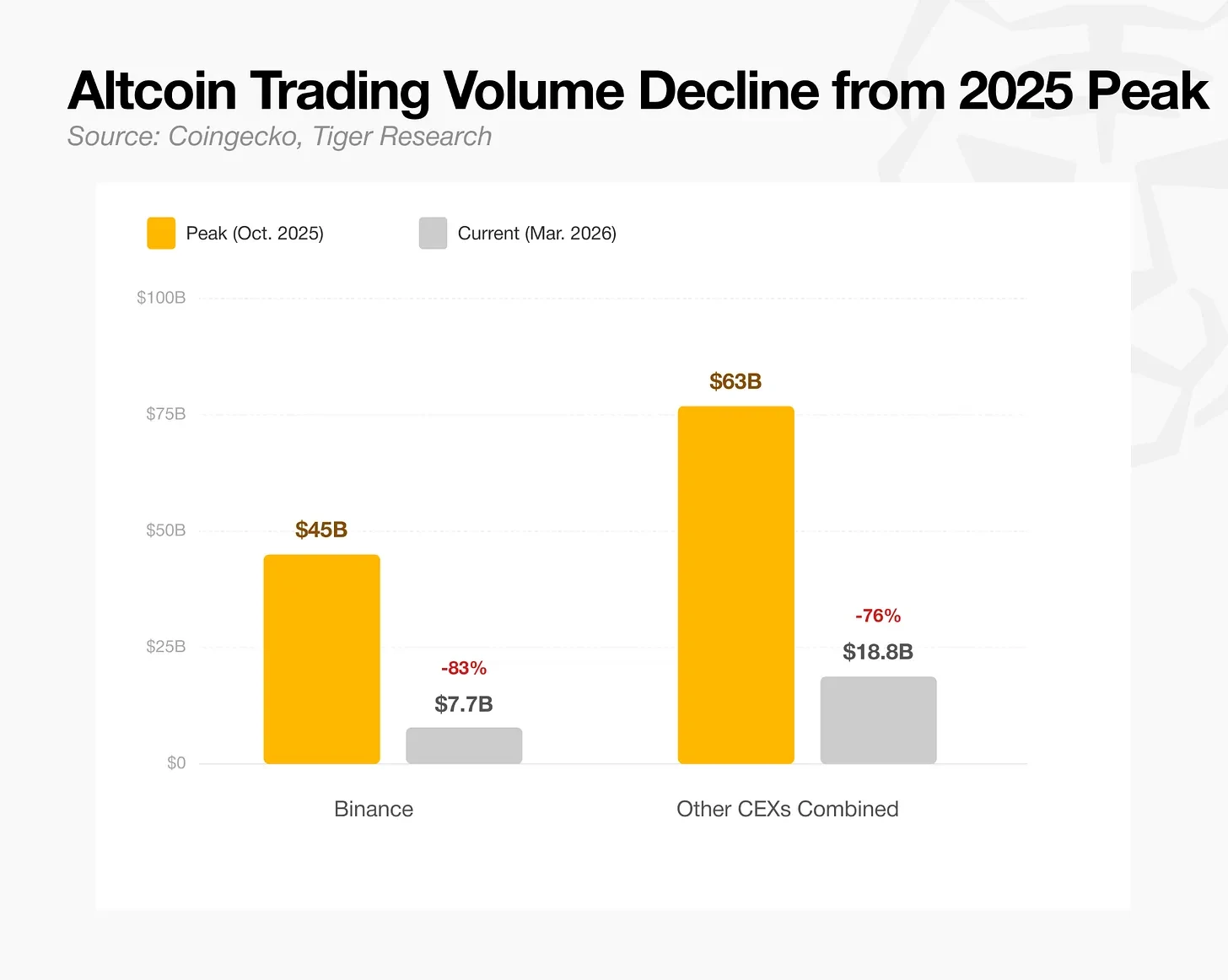

The primary pressure stems from the contraction in overall crypto trading volume. An exchange's core revenue comes from crypto trading fees, and trading volume is entirely determined by market sentiment.

Binance's average daily spot trading volume has plummeted from a peak of ~$45 billion in October 2025 to currently just $7.7 billion, a decline of nearly 80%. The combined spot volume of all other centralized exchanges has also dropped from a peak of $63 billion to $18.8 billion today, a decline of about 70%. This continuous shrinkage in volume means the business model reliant on trading fees is becoming unsustainable. Exchanges have long realized that relying solely on crypto trading fees cannot build a sustainable revenue system.

Hyperliquid Diverts On-Chain Liquidity

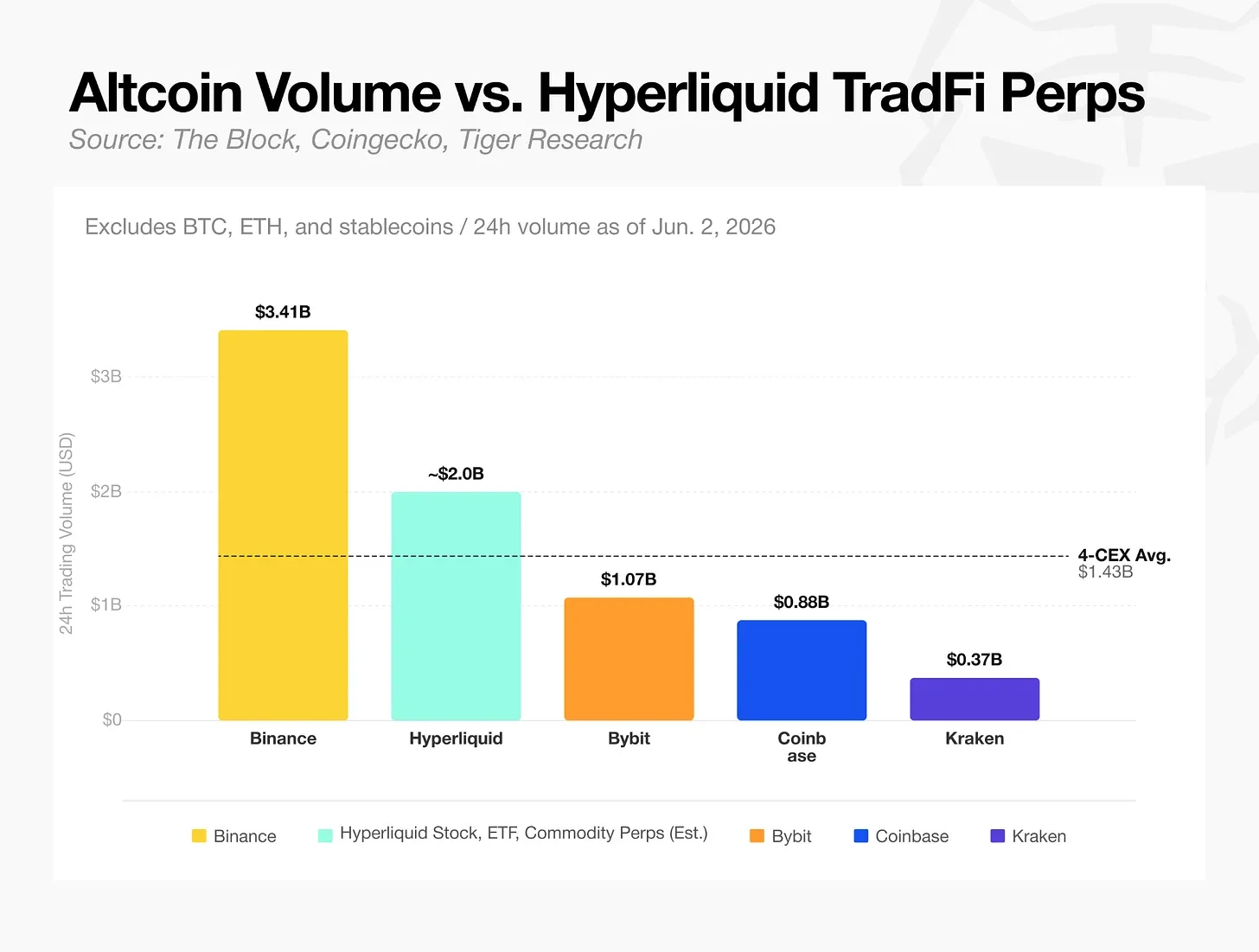

A comparison of data clearly reveals the current market landscape: comparing the trading volume of altcoins (excluding Bitcoin and Ethereum) with the volume of real-world assets like stocks and commodities on the Hyperliquid platform, the gap is evident.

Hyperliquid continuously absorbs on-chain liquidity by listing perpetual contracts for stocks and commodities. As of mid-2026, among the top 30 trading pairs by perpetual contract volume on the platform, 23 are stocks and commodities, making crypto assets a minority.

The on-chain market is no longer exclusive to crypto. The trading volume of a single decentralized exchange can now rival that of traditional centralized exchanges, serving as a wake-up call for major CEXs.

Shifting Regulatory Landscape

The third pressure comes from the overall shift in regulatory direction following the Trump administration's assumption of office. The SEC dropped lawsuits against Coinbase and Kraken. During periods of strict regulatory stance, applying for traditional financial licenses carried significant compliance risks. Now, with regulatory boundaries becoming clearer, holding various financial licenses not only serves as a seal of compliance but also becomes a competitive advantage for platform differentiation.

Within a clear regulatory framework, exchanges can leverage their existing strengths to explore new development paths. These three pressures converging simultaneously, coupled with rising demand for stocks and various financial derivatives, force leading exchanges to accelerate their transformation to survive long-term and forge new growth trajectories.

Strategies of Major Centralized Exchanges

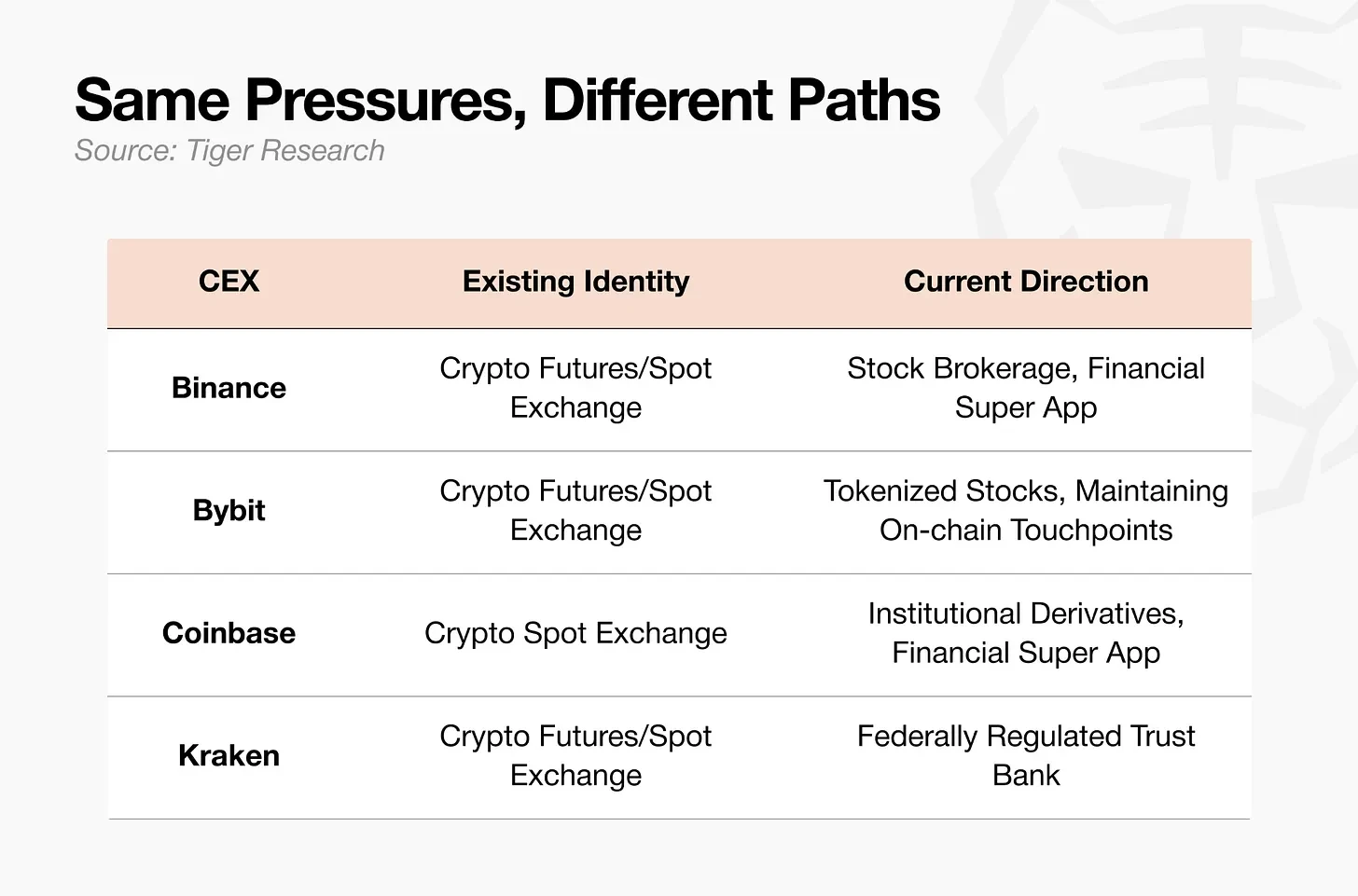

Facing the same industry challenges, different centralized exchanges have chosen divergent development paths.

Binance: Building a Comprehensive Financial Super App

Binance's development philosophy is clear: build a one-stop comprehensive trading platform that retains all user trading activities within its own ecosystem, preventing user churn.

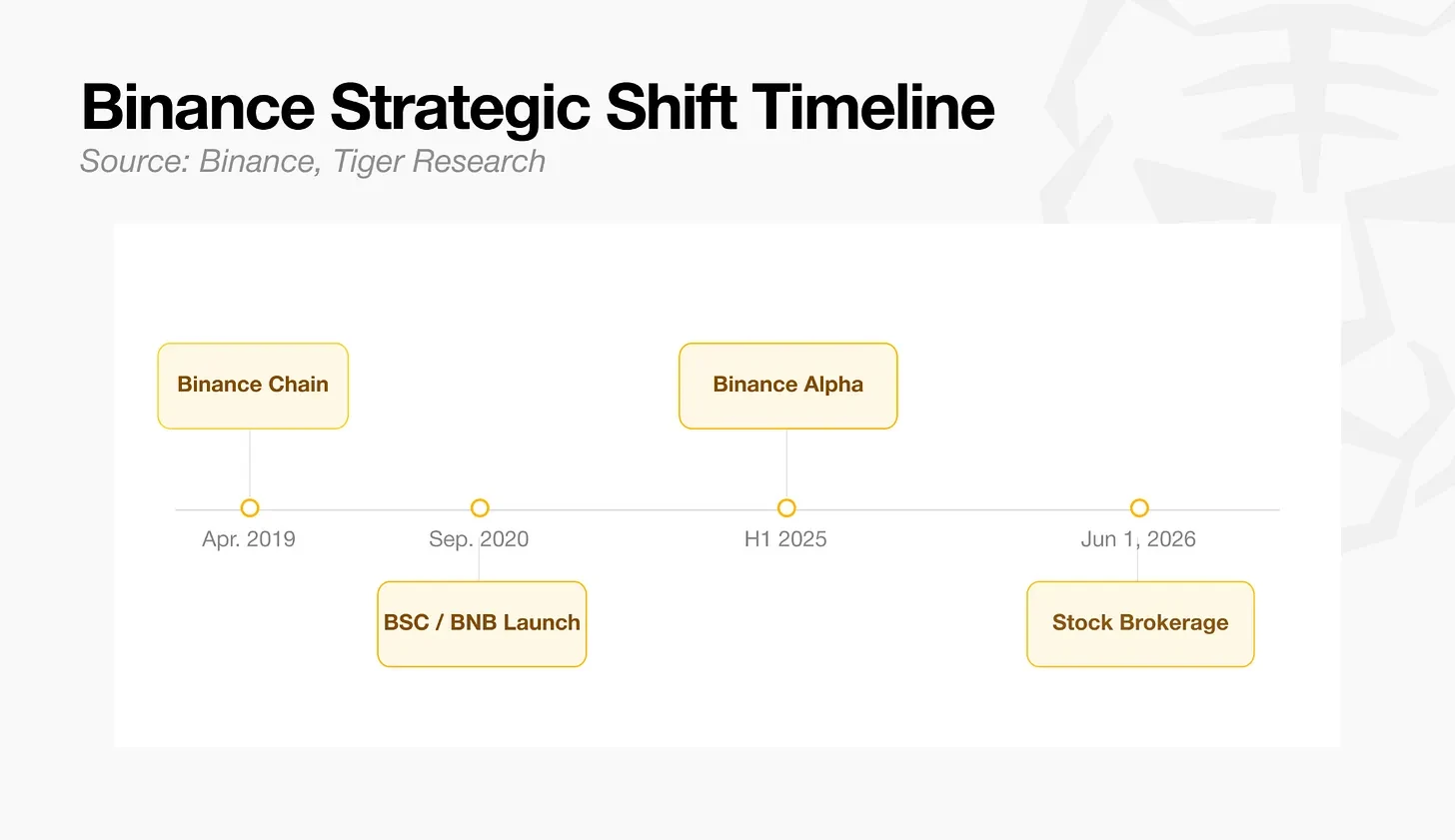

Binance had already ventured into the on-chain arena early on and achieved notable success. The platform first established its centralized exchange business, then launched Binance Smart Chain in April 2019 to enter the on-chain ecosystem. In the first half of 2025, it launched the Binance Alpha product, capturing a significant share of the on-chain market.

However, entering 2026, on-chain liquidity began shifting towards stock categories. Hyperliquid took the lead, continuously capturing liquidity with stock and commodity-related products, directly impacting Binance's user base cultivated over years. In response, Binance chose not to compete head-on with Hyperliquid in the on-chain space but instead took a different approach, launching stock trading services targeting its own user base of over 200 million. Compared to fighting on the opponent's turf, retaining existing users is evidently the safer bet.

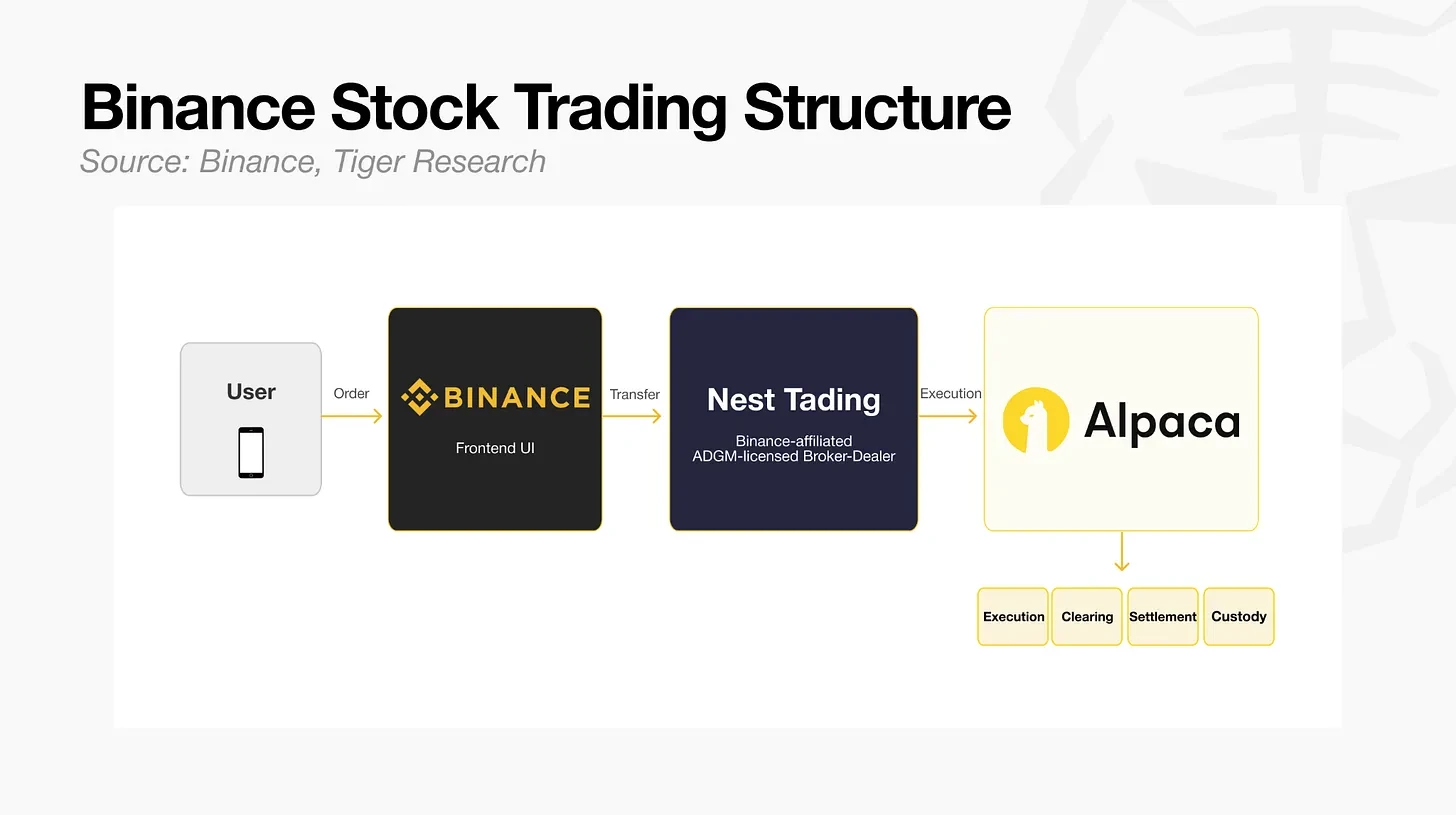

The specific operational model is as follows: Trade orders submitted by users on the Binance frontend are first received by Nest Trading, a broker licensed in the Abu Dhabi Global Market, which then forwards them to Alpaca Securities to complete the subsequent process. Alpaca handles order execution, clearing, settlement, and asset custody. Binance does not directly hold the related securities assets. This structural design allows it to avoid the jurisdiction of direct securities regulation.

Notably, Nest Trading has been confirmed as an entity affiliated with Binance, and Binance also holds a minority stake in Alpaca. Both parties have signed a revenue-sharing agreement, with Nest Trading receiving 50% of the order flow fees and 65% of the securities lending income.

Currently, Binance is independently building a full suite of supporting infrastructure, fully transforming into a financial super app. Before altcoin liquidity further flows to Hyperliquid and the stock market, the platform is making every effort to consolidate its existing user base.

Bybit: A Dual-Track Development Model

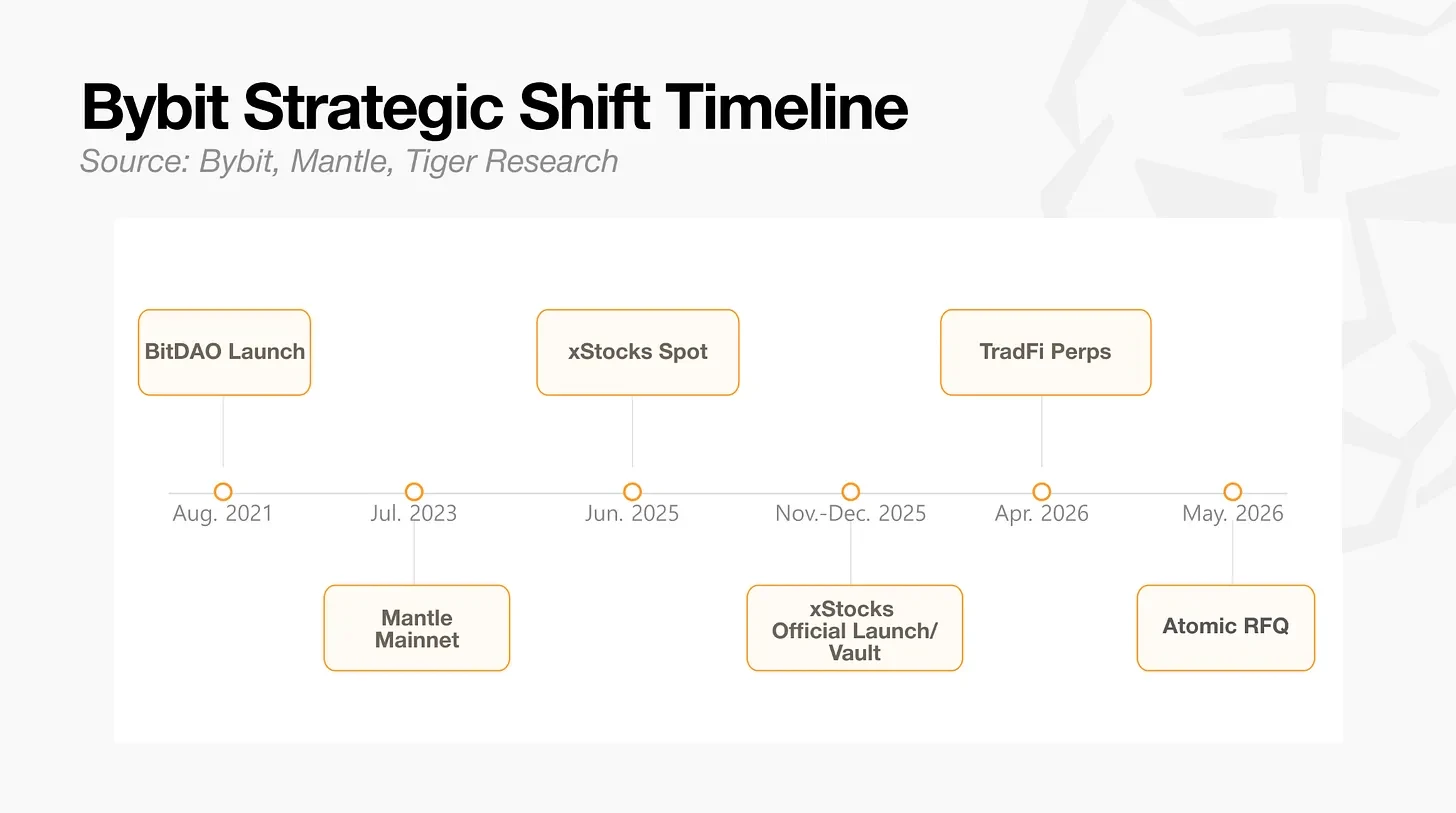

Founded in 2018, Bybit started in the derivatives trading space, achieving rapid expansion through high leverage (up to 100x) and low fees. The platform now employs a dual-track strategy encompassing both centralized and on-chain operations: on one hand, migrating liquidity from its centralized exchange to the blockchain network, and on the other, directly listing traditional financial asset derivatives on its centralized platform.

The platform's布局 (layout/strategy) began with its on-chain business. In June 2025, Bybit listed tokenized stock products launched by Backed on its spot market, formally taking its first step into tokenized stocks. In November of the same year, Bybit partnered with the Mantle public chain and Backed in a three-way collaboration to officially launch xStocks products on the Mantle blockchain, covering mainstream US stocks like Nvidia (NVDA) and Apple (AAPL).

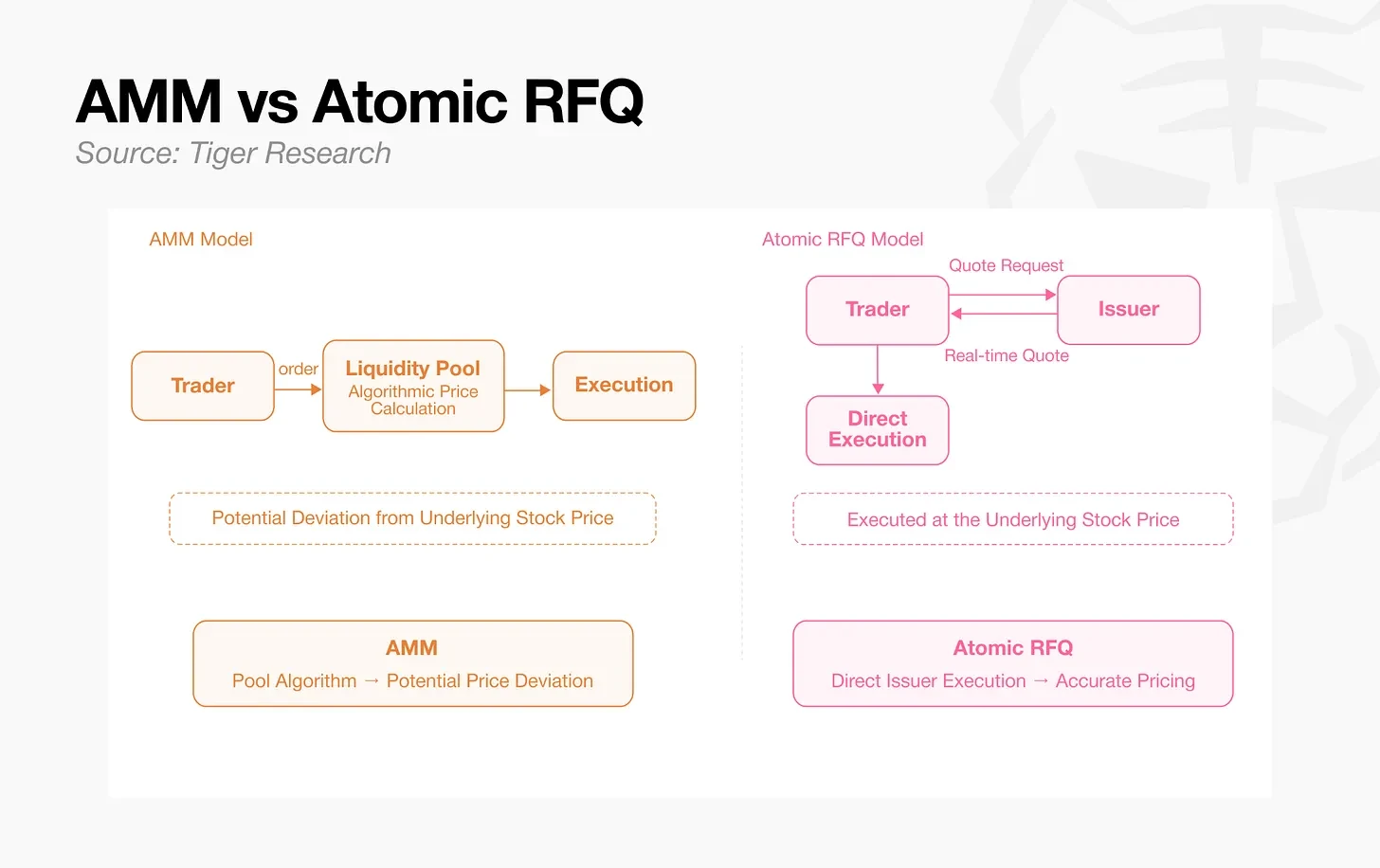

In May 2026, Bybit launched an Atomic Quote function on Fluxion, a DEX within the Mantle ecosystem. This function bypasses the Automated Market Maker for order matching, instead fetching quotes directly from asset issuers, allowing on-chain transactions to meet the execution standards required by traditional financial institutions.

On the centralized business front, Bybit has also been active. Facing similar industry pressures as Binance, the platform launched perpetual contracts for traditional financial categories in April 2026 and has been adding new underlying assets weekly since then. Currently, mainstream US stocks like Tesla (TSLA), Nvidia (NVDA), Apple (AAPL), and commodities like gold, silver, and crude oil are all available for 24/7 trading settled in USDT. On June 4th, perpetual contracts for Samsung Electronics, SK Hynix, and Hyundai Motor were officially listed, and the platform also opened trading for SpaceX pre-IPO shares.

The ultimate goal of both business tracks is to build robust infrastructure, bridge on-chain and off-chain scenarios, and enable sophisticated trading of traditional financial assets. Unlike Binance, Bybit hasn't bet everything on its centralized platform but continues to deepen its on-chain ecosystem via Fluxion and the Mantle public chain.

Coinbase: The Most Trustworthy Exchange in the US Market

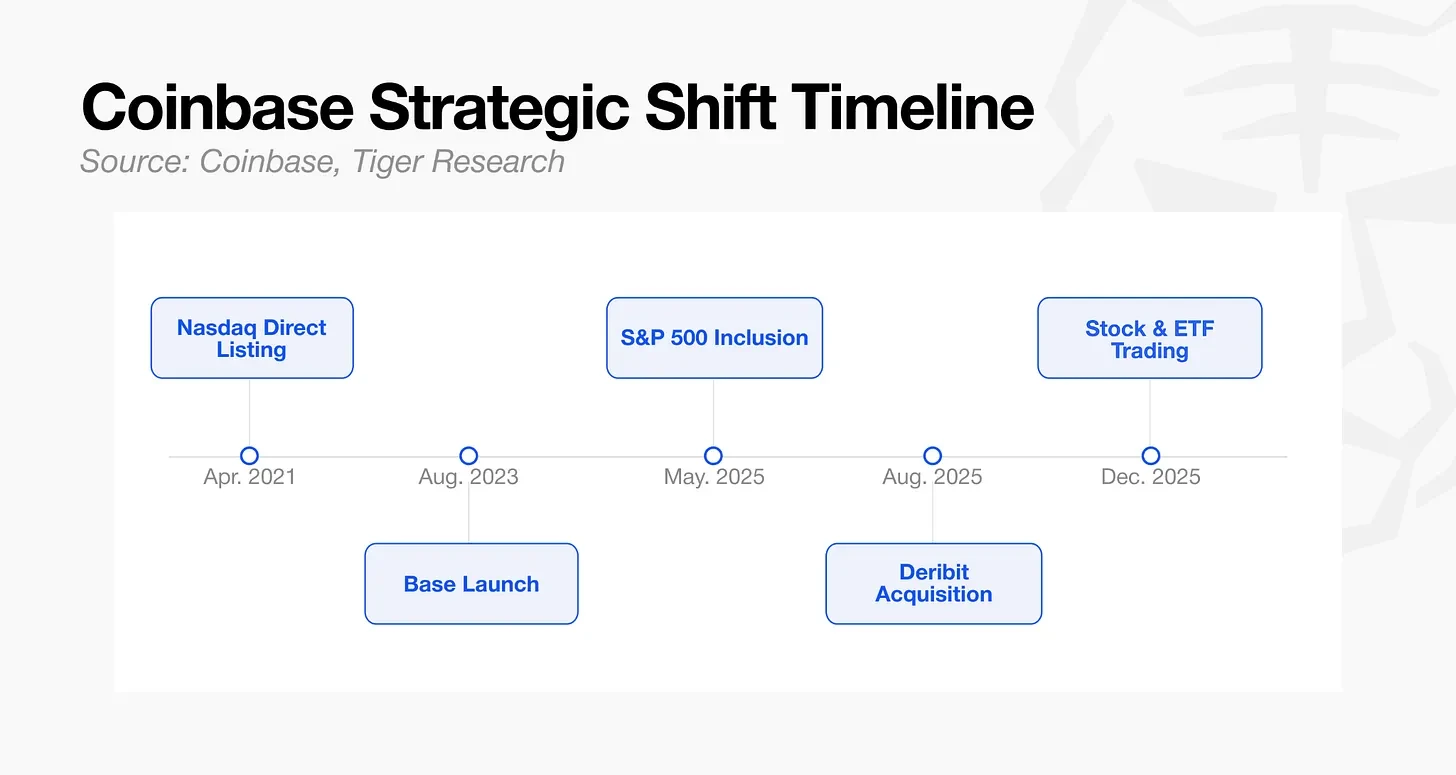

Coinbase went public on Nasdaq in 2021 and was added to the S&P 500 index in May 2025. Backed by Wall Street capital, it is currently the most institutionally recognized centralized crypto exchange globally.

Coinbase also maintains an on-chain business layout. It launched its Ethereum Layer-2 network, Base, in 2023. Base grew rapidly, at one point accounting for nearly half of the total value locked in Layer-2 networks in 2025. However, entering 2026, Base's growth has stagnated and is no longer the company's core development focus.

Coinbase's current strategic focus is squarely on institutional clients. In August 2025, the company completed the acquisition of Deribit for $2.9 billion, capturing roughly 85% of the global crypto options market. Subsequently, it obtained a Futures Commission Merchant license from the US Commodity Futures Trading Commission and launched cross-margining functionality, integrating spot, futures, and perpetual contract positions into a single margin account to further expand its institutional client base. That year, loan balances from hedge funds and asset management firms on the platform hit a quarterly record high.

In December 2025, Coinbase launched commission-free stock and ETF trading services within its own App. While Binance uses an indirect operational model via an external broker, Coinbase, leveraging its years of accumulated compliance licenses, conducts stock trading directly. On June 4th, the platform announced support for trading SpaceX pre-IPO shares.

While Hyperliquid continuously enriches its products and accumulates liquidity in regulatory gray zones, Coinbase's early move into stock trading gives it more initiative to cope with the industry's transformation.

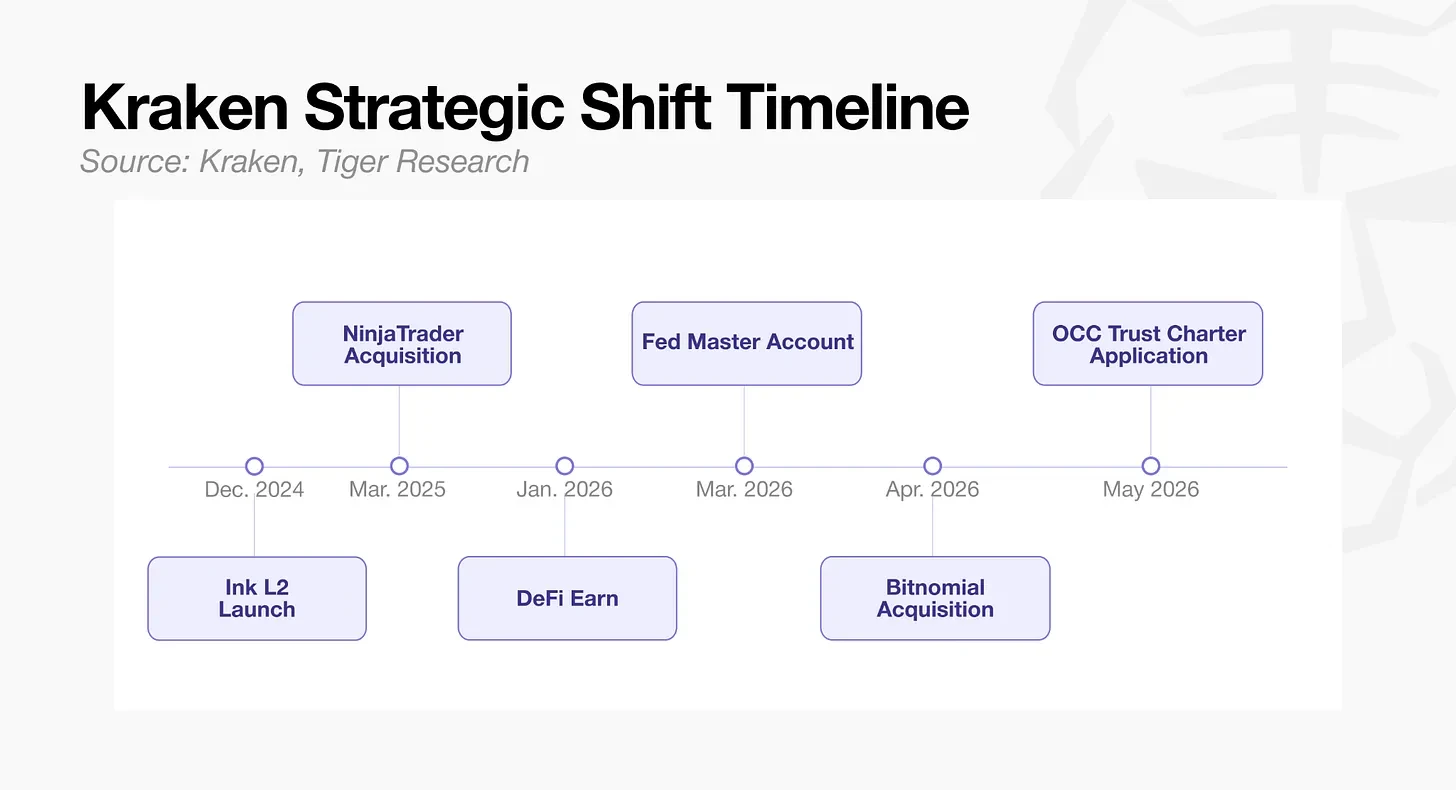

Kraken: Marching Towards a Federally Chartered Crypto Bank

Founded in 2011, Kraken is one of the longest-standing exchanges in the crypto industry. Its core strategy is to continuously consolidate various financial licenses and build proprietary infrastructure, ultimately aiming to become a federally regulated crypto asset custodian bank in the United States.

Acquiring compliance qualifications is Kraken's top priority. In March 2025, the company spent $1.5 billion to acquire the trading platform NinjaTrader, securing a CFTC FCM license and taking over the platform's 20,000 retail traders. In April 2026, it acquired Bitnomial for $550 million. After a decade of operation, Bitnomial was the only native crypto platform holding all three core CFTC licenses – Designated Contract Market, Derivatives Clearing Organization, and FCM. In March 2026, Kraken successfully obtained a Fed master account; in May of the same year, it submitted an application for a National Trust Charter to the US Office of the Comptroller of the Currency.

While pushing its compliance strategy, Kraken hasn't neglected the on-chain ecosystem. The platform launched its proprietary Layer-2 network, Ink, in December 2024, and subsequently built the lending protocol Tydro and the decentralized perpetual exchange Nado on this network. In January 2026, it launched the on-chain wealth management product DeFi Earn, followed by the Bitcoin custody service Bitcoin Vault in May. The design logic for all on-chain products revolves around assets whose value proposition can be clearly articulated to institutional clients. Altcoins are also not part of its on-chain roadmap.

While other exchanges rush to list stock trading to retain users, Kraken has chosen a different path, aspiring to become a trusted native crypto bank for institutional clients.

Although the specific strategies of each centralized exchange differ, they share one commonality: altcoins no longer hold a significant place in the future plans of any platform.

Where is the Crypto Industry Heading?

For a long time, centralized exchanges have been the liquidity backbone of the crypto ecosystem. Exchanges list tokens and drive trading activity, and the vast majority of crypto projects have relied on this support to survive.

The deep-seated issue is that almost no crypto project can prove its true value through actual business revenue. The support logic for token prices has never been the project's fundamentals, but rather initial traction methods like exchange listings and liquidity mining. This operational model can only persist as long as exchanges and traders maintain enthusiasm for the crypto sector.

Now, with retail trading volumes shrinking and hype fading, the listing support and marketing resources from exchanges will also tighten. The original ecosystem model is destined to be unsustainable.

Market sentiment has shifted. Capital is beginning to flow towards projects that can generate value through real product revenue, rather than tokens dependent solely on exchange support. Hyperliquid's platform token, HYPE, is the most typical example. Even though this very platform diverted on-chain liquidity originally belonging to crypto towards stock categories, HYPE remains one of the best-performing crypto assets. This phenomenon indicates that the once mutually beneficial symbiotic relationship between centralized exchanges and crypto projects is gradually dissolving.

The strategic choices of major exchanges also confirm this trend. Retail trading volume and user base are the foundation of an exchange's survival. If they stubbornly stick to a pure crypto trading track, that foundation will only continue to erode. The market has long lost its former enthusiasm for newly listed crypto tokens. Exchanges have no choice but to actively seek new revenue sources while safeguarding their existing platform architecture and user base.

This is the core reason why major platforms are collectively pivoting towards stock derivatives, wealth management value-added services, and asset custody. In the process of fully reallocating resources, exchanges are effectively letting altcoin projects fend for themselves in the market.

In past downturns, centralized exchanges would bear the pressure together with the entire crypto industry and weather the bear market side-by-side. But now, exchanges are exploring paths to growth that are decoupled from crypto. This suggests that the current industry downturn could be more severe for the crypto sector than any previous bear market.