SemiAnalysis vs. The White-Haired Stock Oracle: What Hidden Gold Lies in the CPO Report Selloff?

- Core Thesis: A divergence in market expectations regarding the CPO (Co-Packaged Optics) volume ramp schedule has led to a pullback in optical stocks. SemiAnalysis suggests that mass production may be delayed until 2028-2029, while analyst Serenity counters that Nvidia's supply chain execution could accelerate this process. The crux of the debate is the slope of CPO commercialization, not the direction.

- Key Elements:

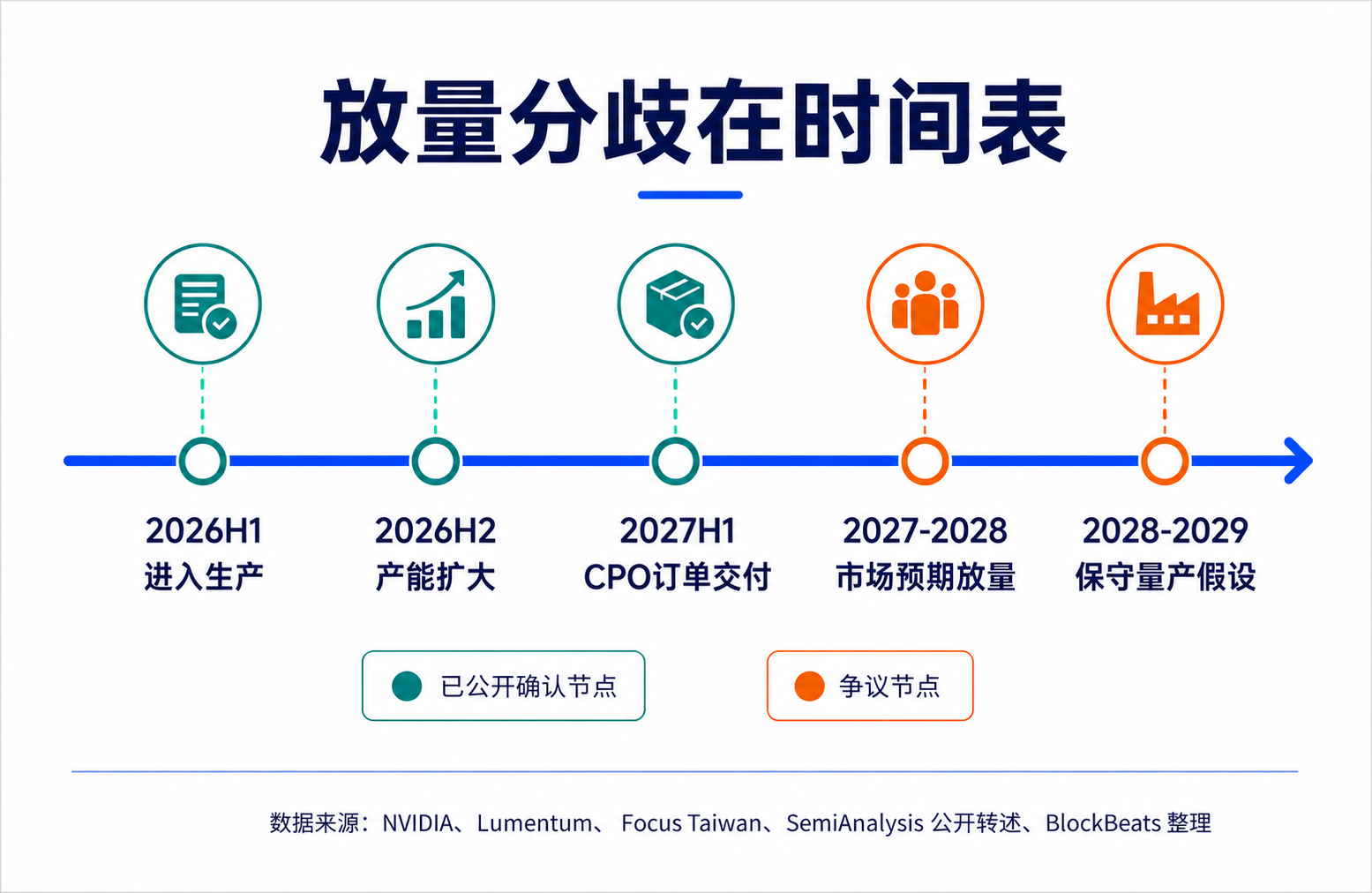

- SemiAnalysis's June report triggered market volatility, with its core judgment that mass production of CPO could be delayed until 2028-2029, while NPO (Near-Packaged Optics) projects may accelerate. This led to high-single-digit to double-digit corrections in optical stocks like AAOI and LITE.

- Serenity refutes SemiAnalysis's conservative model, arguing it underestimates Nvidia's ability to compress hardware cycles. Citing signals such as Lumentum's hundreds of millions of dollars in incremental CPO orders and Spectrum-X entering production, Serenity maintains that CPO remains on track for a ramp-up from the second half of 2026 to 2028.

- The theoretical advantage of CPO lies in addressing power consumption and signal integrity bottlenecks at high bandwidth by moving the optical engine closer to the ASIC. However, its system engineering challenges (e.g., repair, yield, reliability) may cause scaled deployment to be slower than market expectations.

- NPO, being an intermediate between CPO and traditional pluggable modules, becomes a focal point of the debate: if CPO is delayed, NPO will enjoy a longer market window; if CPO accelerates, NPO may still coexist with CPO at different network tiers, reshaping the value distribution between the technology routes.

- The market had previously over-priced the "CPO endgame" narrative. The fundamental difference between SemiAnalysis and Serenity shifts the valuation anchor from direction to timeline validation. Key future catalysts will be production-level data from the second half of 2026 to 2028, particularly shipment volumes (small batch vs. mass production) and field reliability data.

TL;DR

- SemiAnalysis believes CPO volume ramp-up will be slower than the market expects, potentially extending the transition window for NPO.

- Serenity disagrees with this assessment, arguing that Nvidia and the supply chain are pushing CPO forward faster.

- Related tickers: AAOI, LITE, COHR, GLW, MRVL, SIVE, AVGO, NVDA

The recent downturn in optical stocks, on the surface, is a cold shower for the CPO narrative. In essence, it's the market re-evaluating a more sensitive issue: Will the volume ramp-up in 2027-2028 be a period of performance realization, or merely a phase of introduction and validation?

CPO (Co-packaged Optics) itself is not being negated. The pressure on bandwidth, power consumption, and switching density in AI data centers continues to mount, and the physical limitations of copper cables and traditional pluggable optical modules haven't disappeared. The problem is that previous rallies in related stocks already implied an aggressive timeline: after Nvidia pushes CPO into the commercial window, components like optical engines, lasers, silicon photonics, and switch chips would quickly enter volume shipments in 2027-2028.

The report from SemiAnalysis on June 9th hit precisely this pricing assumption. According to public summaries, the report suggests Nvidia's 800V DC and mass production of CPO might be delayed until around 2028-2029, while 400V DC still ramps in 2026, with some NPO (Near-packaged Optics) projects potentially accelerating. Following the market volatility triggered by the report, stocks like AAOI, LITE, COHR, GLW, and MRVL, along with other optics and related supply chain names, saw high single-digit to double-digit corrections. The market isn't trading on "whether the CPO direction is valid," but rather "how quickly can CPO translate into orders."

However, this is not a one-sided bearish story. "Serenity," an AI supply chain analyst (@aleabitoreddit), subsequently countered SemiAnalysis, arguing that they overly relied on conservative engineering models and underestimated Nvidia's ability to compress hardware cycles. Based on his interpretation of signals from Nvidia, Lumentum, and Foxconn, he emphasized that CPO remains on track for ramps in H2 2026, H2 2027, and 2028.

The value of this debate isn't determining who "won," but rather pulling the valuation anchor for the optical supply chain back from an end-game narrative to timeline validation: CPO is coming, but the slope at which it arrives determines the value distribution among NPO, pluggable modules, light sources, and switch chips.

Timeline Reassessment Behind the Optical Stock Decline

Over the past few months, what the market bought into with the optical supply chain wasn't current revenue, but the capital expenditure shift towards next-generation network architectures in AI data centers.

As model training and inference clusters scale up, the communication pressure between GPUs, racks, and within data centers continues to rise. Networking is no longer just a supporting peripheral system for servers; it's increasingly becoming the efficiency bottleneck of AI factories. Higher bandwidth density and lower power consumption raise the upper limit for scaling computing clusters, which is why CPO has come to the forefront.

CPO's theoretical appeal is straightforward: bring the optical engine as close as possible to the ASIC (dedicated switch chip), shortening the high-speed electrical signal path, and reducing the power, loss, and signal integrity issues associated with serial-parallel conversion circuits and copper traces. Compared to traditional pluggable modules, CPO offers better power efficiency and density potential in the high-bandwidth era.

The market's problem is its tendency to prematurely trade "correct direction" as "confirmed volume." Nvidia's official press release states that the Vera Rubin platform will introduce Spectrum-X Ethernet Photonics, and CPO switches have entered production for AI factory scale-out and cross-cluster deployment. Reports from June 3rd indicated Nvidia's networking business executives said Spectrum-X CPO switches have been shipped to some partners, with production capacity expected to expand in the second half of 2026.

These signals are sufficient to prove CPO is progressing, but they cannot be directly equated to risk-free mass production orders. For capital markets, there's a significant valuation gap between "entering production," "shipping to partners," "customer evaluation," and "mass production." The correction triggered by the SemiAnalysis report is essentially the market beginning to differentiate between these statements.

SemiAnalysis's Conservative Model: CPO's Challenge Lies in System Engineering

SemiAnalysis isn't saying CPO has no future. Its core judgment is more like: CPO's theoretical advantages are clear, but scaled implementation is slower than the market imagines.

The reason isn't just that one or two components aren't ready, but that CPO concentrates the complexity previously distributed across modules, boards, and whole systems into a more deeply coupled one. Higher integration yields better single-point performance, but it also increases pressure on manufacturing, testing, repair, and supply chain resilience.

The benefit of traditional pluggable modules is modularity. If an optical module fails, you replace the module; switching between suppliers is relatively easy. CPO is different. The optical engine is much closer to the ASIC, even entering the same package. The power and density benefits come from this close coupling, but the radius of repair also expands. If an optical component fails, the impact isn't just an easily swappable module; it could involve the higher-value switch chip and the entire system.

SemiAnalysis's previous CPO Book repeatedly emphasized serviceability, reliability, yield rates, and supply chain maturity, especially in hyperscale cloud scenarios. Performance is not the only metric. Large customers have very high requirements for reliability and maintainability. If the failure rate, repair process, and replacement costs are uncontrollable in a production environment, even the best power model might face delayed adoption.

InP lasers are also a point of contention. Port run-time data at the lab level can prove technical feasibility, but it doesn't cover long-term operation, mass manufacturing, field maintenance, and supply chain redundancy in large-scale data centers. For investors, this difference is critical: lab validation proves the direction, but field reliability determines the volume.

In SemiAnalysis's framework, NPO and pluggable modules are not outdated paths but more realistic intermediate layers before engineering risks are fully resolved. While CPO is theoretically superior, if full adoption takes significantly longer, the market must reprice these "less end-game but easier to manufacture and maintain" solutions.

Serenity's Rebuttal: Nvidia May Compress Hardware Cycles

Serenity's rebuttal does not deny the engineering challenges of CPO. Instead, it argues that SemiAnalysis underestimates Nvidia's organizational capability in the AI hardware cycle.

His logic is clear: normal hardware adoption is indeed hampered by yield rates, reliability, and customer validation, but Nvidia is no ordinary customer. It is the definer of GPU cluster architecture and the core driver of networking, switches, system integration, and supply chain rhythm. When AI factory expansion is bottlenecked by network power and bandwidth, Nvidia has strong enough economic incentives and industry influence to compress the typical adoption cycle.

Serenity's cited evidence comes in two layers. The first layer consists of publicly verifiable company statements, including Nvidia's official information on Spectrum-X Photonics entering production, and Lumentum's mention of CPO orders and delivery cadence in its Q2 FY26 update. Lumentum stated it received several hundred million dollars in incremental CPO orders for delivery in H1 2027, and company materials also mentioned that CPO-related business is expected to enter a broader ramp in H2 2026.

The second layer involves interpreting supply chain signals, such as Foxconn's early delivery of optical switches to Nvidia. However, the specific scale of these signals and whether they are test units or production-level orders still require more public information for confirmation.

This is the key divergence between Serenity and SemiAnalysis: SemiAnalysis believes system engineering variables will naturally lengthen the cycle, while Serenity believes Nvidia's supply chain execution will steepen the curve.

These two judgments aren't entirely contradictory. Nvidia can bring CPO to production and customer validation sooner and may push for earlier adoption in some scale-out scenarios, but this doesn't automatically mean all AI data center networks will quickly switch to CPO by 2027. Scale-out, single-rack scale-up, intra-rack, inter-rack, and different customers' reliability tolerance and cost models all differ, leading to potentially layered adoption timelines.

Serenity refutes the overly conservative conclusion that "CPO will be significantly delayed," not proving that "CPO is fully risk-free." For the market, this is enough to support a short-term oversold bounce rationale but insufficient to rewrite the aggressive 2027-2028 revenue curves back into certainty.

Why NPO Suddenly Became Important

NPO suddenly became important in this debate because it sits right between the logic of SemiAnalysis and Serenity.

It is not the antithesis of CPO, nor is it a simple continuation of traditional pluggable modules. The basic idea of NPO is to place the optical engine on a pluggable base substrate near the ASIC, shortening the electrical signal path to gain some power and density benefits while retaining better testability, replaceability, and supply chain flexibility.

If SemiAnalysis's conservative model is closer to reality, and CPO's deep packaging slows down due to yield, maintenance, and reliability issues, NPO will become the more realistic choice for a longer period. It allows hyperscale cloud providers to gradually accumulate operational experience in optical interconnects without taking on the full risk of CPO, while also giving existing optical module and engine suppliers a longer window.

If Serenity's judgment on Nvidia's execution is more accurate, NPO may not disappear either. A more likely scenario is that NPO, CPO, pluggable optics, and copper interconnects will coexist at different network layers. Nvidia's own roadmap also shows that CPO for scale-out can proceed first, while some single-rack scale-up scenarios might still rely on copper or hybrid architectures in 2027-2028.

The implication for investors is that they cannot simply price the optical supply chain with a "CPO wins, others lose" mentality. Different technical routes benefit different segments: CPO favors highly integrated optical engines, laser light sources, silicon photonics, and the switch chip ecosystem. An extended window for NPO and pluggables, however, allows existing optical module makers, connector, material, and some light source suppliers to continue enjoying orders and margin support.

The market's previous problem was translating the technological end-game too early into a single-route performance slope. What is now being reopened is the valuation space for intermediate routes.

Production-Level Data is the Next Verification Point

This debate won't be settled in the short term by a single report or a series of posts. SemiAnalysis reminds the market that CPO's difficulty lies in system engineering. Serenity reminds the market that Nvidia's supply chain organization may alter traditional hardware adoption rhythms. The true divergence between them must be verified by production-level data from H2 2026 to 2028.

The most critical thing going forward isn't "whether there are shipments," but the nature of those shipments. Delivering to some partners, customer evaluation, initial production, volume ramp-up, and large-scale deployment are completely different stages. Nvidia's subsequent descriptions of Spectrum-X / Quantum-X Photonics mass production, and statements from optical suppliers like Lumentum and Coherent regarding orders, capacity, and gross margins in earnings reports, will be more important than the wording of any single meeting.

Field reliability and maintenance data also need close monitoring. If CPO's failure rate, replacement process, yield curve, and total cost of ownership in a production environment prove sufficiently stable, SemiAnalysis's conservative model will be revised. If this data remains stuck at the lab or small-scale validation level, the window for NPO and pluggable modules will continue to be upgraded by the market.

The optical supply chain is now trading not on CPO's survival, but on the slope of its timeline. The next verification point lies in whether "entering production" can translate into sustainable volume, and the speed at which this volume is ultimately reflected in orders, gross margins, and customer deployment metrics.

Although SemiAnalysis raised concerns about CPO technology over the next two years, they still identified five semiconductor sub-sectors they are bullish on:

Copper / AEC / ACC;

Pluggable Optics / DSP;

CPO Test Equipment;

Power Gray Space / UPS Continuation;

Board-level VRM / Silicon-based Power / Passive Components

Specific tickers within these sectors are compiled in the image below for readers' reference.