It wasn’t carry trade unwinding that saved Japan’s stock market: Yen shorts remain crowded, AI-driven foreign capital is the real catalyst for new highs

- Core Thesis: Although the yen remains at low levels, short positions are crowded, and the Ministry of Finance has conducted the largest intervention in history, the Nikkei 225's new highs are primarily driven by foreign capital chasing the AI theme. This mechanism is fundamentally different from the market decline triggered by carry trade unwinding in August 2024, requiring a more nuanced deconstruction of the market narrative.

- Key Factors:

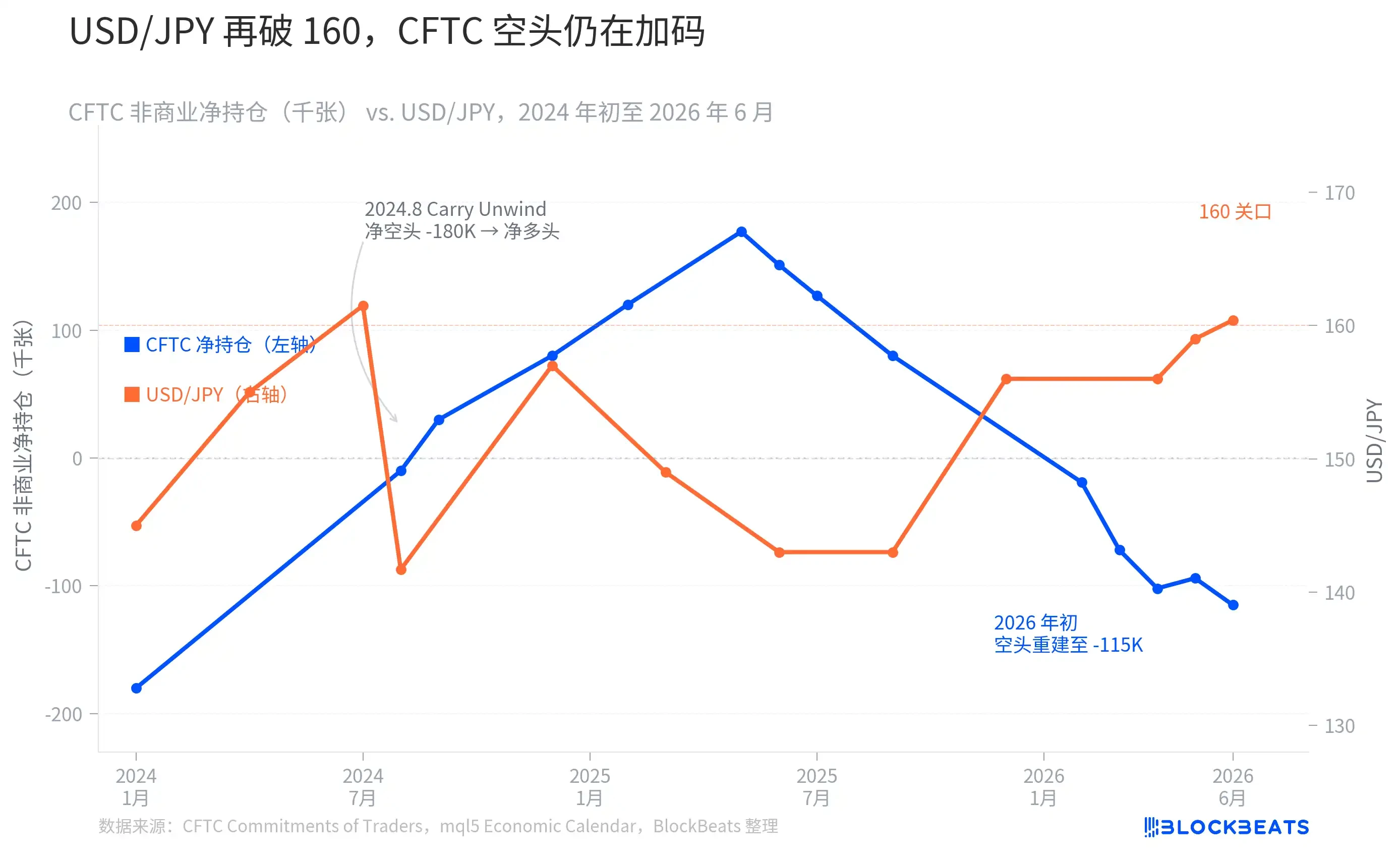

- As of May 26, CFTC data shows net short positions in yen futures reached 114,667 contracts, an increase of 27,152 contracts from the previous week, indicating speculative capital is increasing bets against the yen rather than withdrawing.

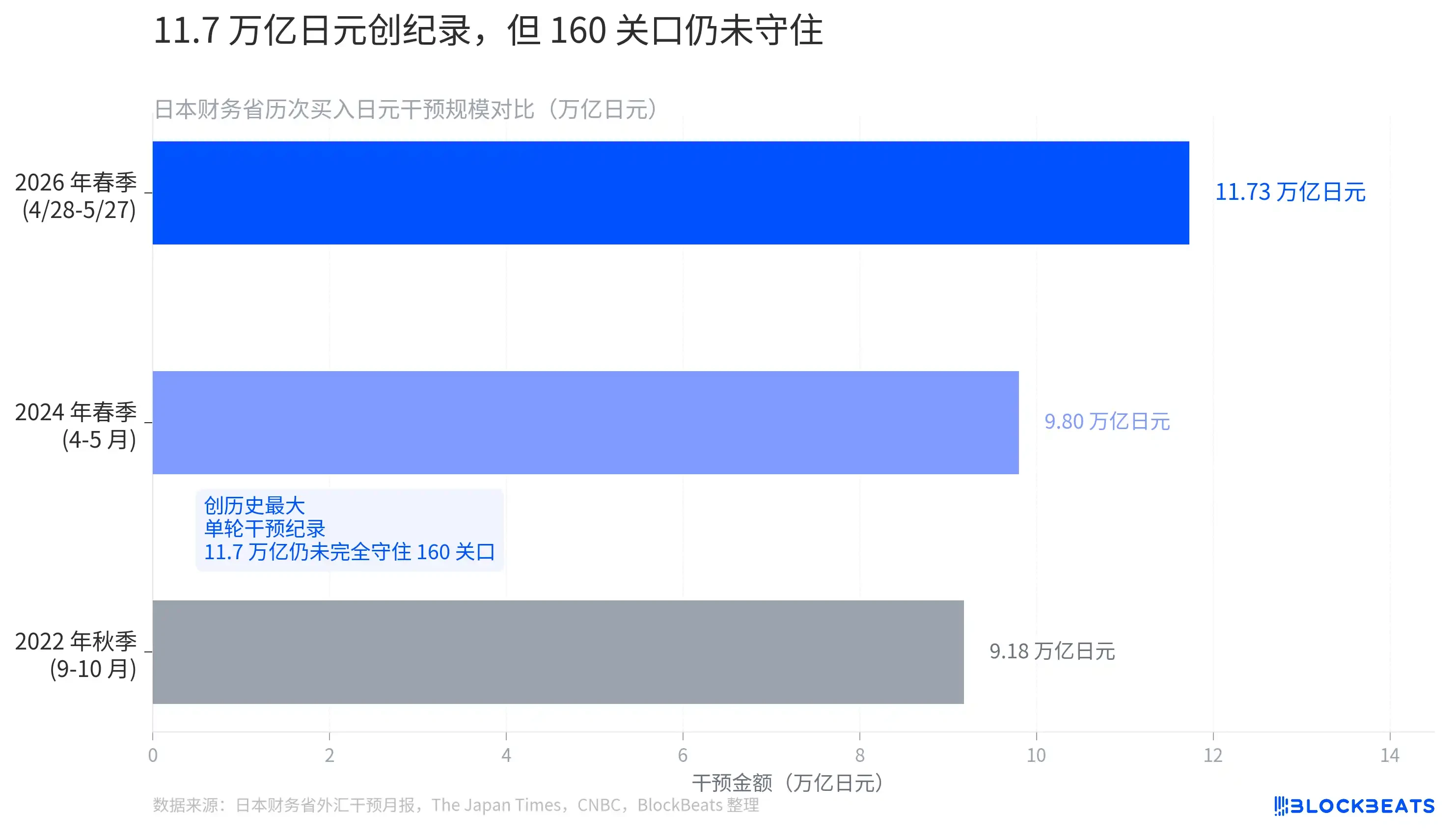

- From April 28 to May 27, Japan’s Ministry of Finance executed a record single-round yen-buying intervention amounting to 11.7349 trillion yen (approximately $73.6 billion), but failed to effectively defend the 160 threshold, highlighting the limited effectiveness of the intervention.

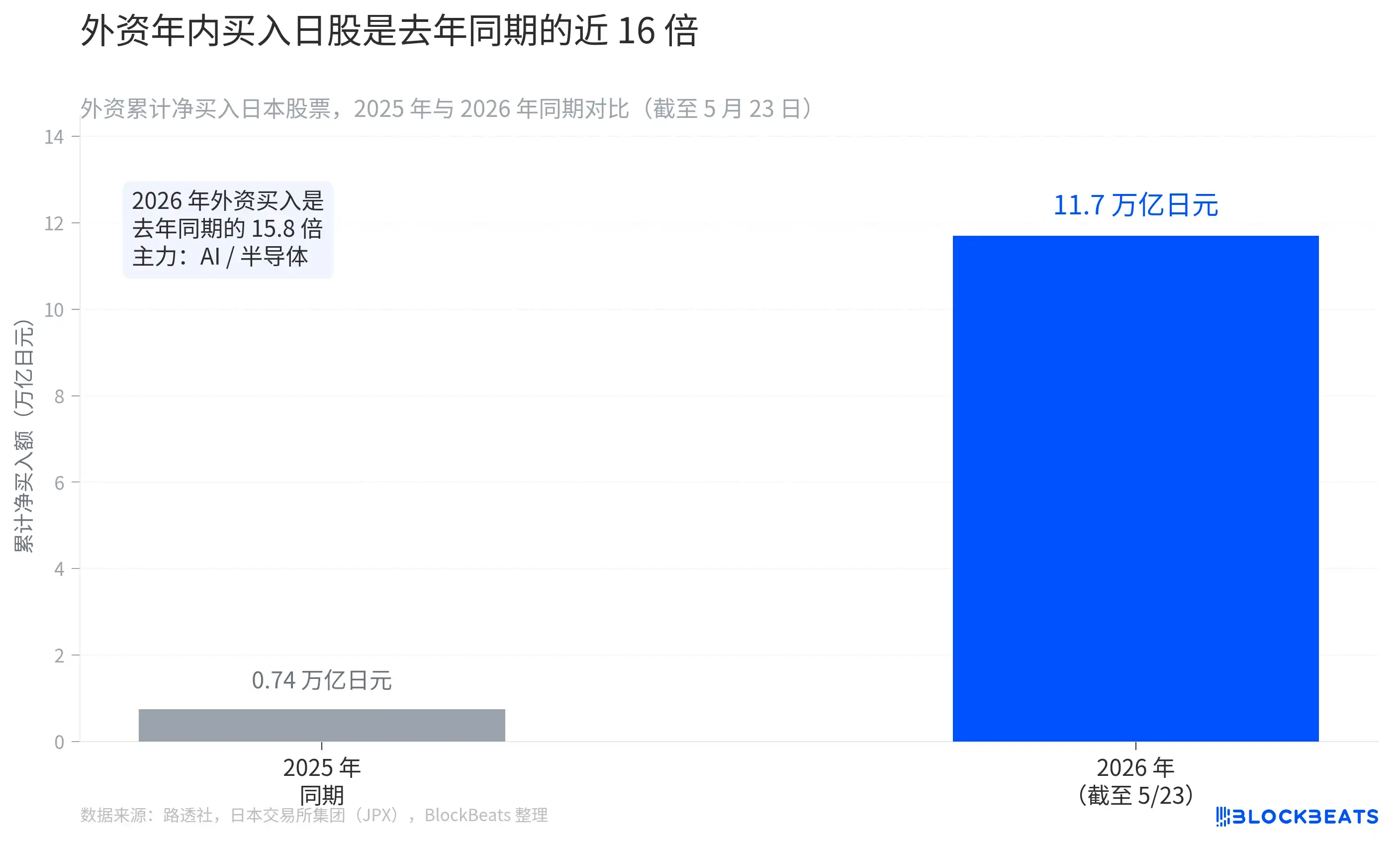

- In the week ending May 23, foreign investors were net buyers of Japanese stocks for the 8th consecutive week, with cumulative net purchases reaching approximately 11.7 trillion yen this year—15.8 times the amount during the same period in 2025. The buying logic was driven by AI demand boosted by Nvidia’s earnings.

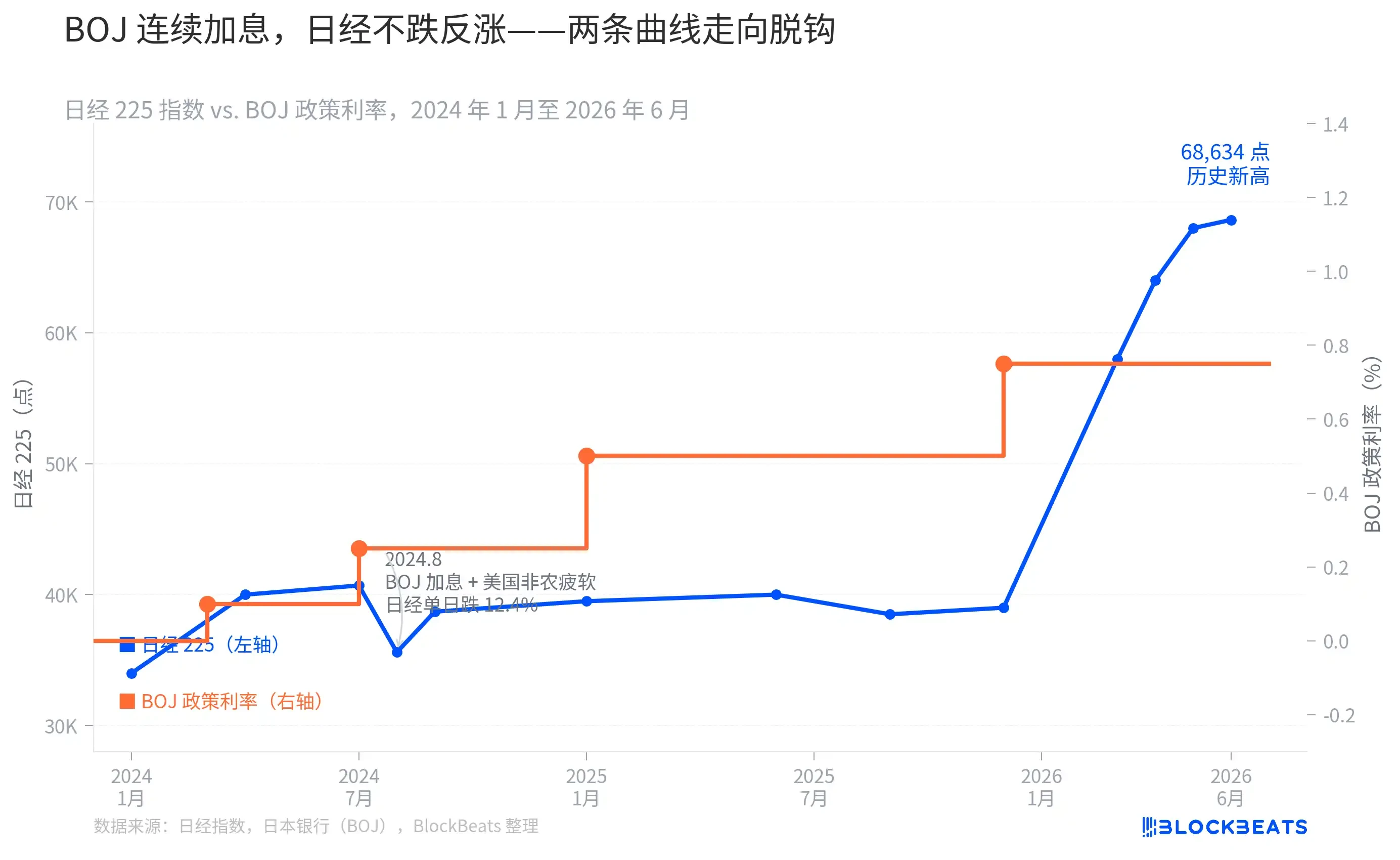

- The correlation between the Bank of Japan’s rate hike path and the Nikkei 225 trend has changed: the July 2024 rate hike triggered a sharp sell-off, but rate hikes in January and December 2025 were accompanied by stock market rises, as AI-related capital is less sensitive to yen interest rates.

- If the Bank of Japan raises rates to 1.0% at its July meeting, coupled with a weaker U.S. dollar, the current crowded yen short positions (approximately 114,667 net shorts) could face passive unwinding pressure similar to that seen in August 2024.

On June 3, the USD/JPY pair hit 160.44 during the session, a new high since July 2024. On the same day, the Nikkei 225 index broke through the 68,000-point mark for the first time, reaching a high of 68,634.74 points. With these two figures coinciding, a familiar narrative immediately emerged in the market: "The carry trade is about to collapse; August 2024 is set to repeat itself."

This narrative is half correct. The other half tells a completely different story, as indicated by the data.

Short Sellers Haven't Pulled Back; They Are Doubling Down

The most direct indicator for measuring the crowding of yen carry trades is the weekly non-commercial positions report published by the U.S. Commodity Futures Trading Commission (CFTC). It records the net long or net short positions of speculative traders in the yen futures market.

According to CFTC data, for the week ending May 26, non-commercial accounts held a net short position of 114,667 contracts in yen futures—112,993 long contracts against 227,660 short contracts. This represents an increase of 27,152 contracts in net short positions compared to the previous week.

The chart reveals a somewhat counterintuitive trend. In July 2024, USD/JPY touched a high near 161, at which point CFTC net shorts were around -180,000 contracts, an extreme historical level. Then, in early August, the Bank of Japan's (BOJ) surprise rate hike, coupled with U.S. non-farm payroll data significantly missing expectations, forced yen short positions to be liquidated within a few weeks. Net shorts sharply contracted from around -180,000 contracts and even reversed to a net long position of over +177,000 contracts by the second quarter of 2025—the carry trade did experience a systematic squeeze during that period.

However, the subsequent trajectory has been completely opposite to the "squeeze narrative." Starting from late 2025, net short yen positions began to re-accumulate, turning negative in February 2026 and rapidly expanding to -102,000 contracts by April. By May 26, net shorts had reached -114,667 contracts. As USD/JPY returned to near 160, global speculative capital was not fleeing; it was continuing to increase its bets.

This implies that if the BOJ signals a more hawkish stance at its July meeting, or if U.S. economic data again underperforms expectations, these -114,667 net short positions could face passive liquidation pressure highly similar to August 2024. The Japanese Ministry of Finance is also aware of this—between April 28 and May 27, it used a record 11.7349 trillion yen to buy yen and sell foreign currencies in an attempt to suppress the short sellers.

Largest Single Intervention Fails to Hold the 160 Line

The Ministry of Finance's history of foreign exchange intervention dates back to 1998. In the fall of 2022, when the yen fell to around 152, the ministry conducted its first "yen-buying" operation since 1998: 2.84 trillion yen was spent in September, followed by an additional 6.34 trillion yen in October, totaling about 9.18 trillion yen. That intervention temporarily pushed USD/JPY from 152 back to around 127, but the effect lasted only a few months.

In the spring of 2024, USD/JPY again approached and briefly broke through 160, prompting the ministry to deploy about 9.80 trillion yen. This was the largest single operation since 2022 at the time and marked the "first confirmed yen-buying intervention since 2022."

According to monthly intervention data released by the Japanese Ministry of Finance on May 29, 2026, the operation between April 28 and May 27 amounted to 11.7349 trillion yen (approximately $73.6 billion). This is the largest single intervention on record, surpassing the entire total for 2022 and nearly 2 trillion yen more than the intervention in spring 2024.

Yet, less than a week after the ministry disclosed this figure, USD/JPY still broke back above the 160 mark. The largest intervention could not fully hold this psychological threshold.

Foreign Buying of Japanese Stocks Is Chasing AI, Not Safe-Haven Funds from Carry Unwinding

If the carry trade remains crowded, why is the Nikkei 225 still hitting new highs?

According to Reuters, citing data from the Japan Exchange Group (JPX), foreign investors were net buyers of Japanese stocks for the eighth consecutive week as of the week ending May 23, with net purchases reaching 1.08 trillion yen in a single week. Cumulative net purchases for the year are close to 11.7 trillion yen.

During the same period in 2025, cumulative net buying by foreign investors was only 742.1 billion yen. In 2026, this figure is 15.8 times higher.

The destination of this capital is highly concentrated. Among the top-gaining stocks during the same period, AI investment platform SoftBank Group rose 17.62% in a single week, while chip design company Socionext gained 12.26%. Reuters reports directly identify the driving force: Nvidia's earnings outlook boosted demand prospects for AI and semiconductors, prompting foreign capital to chase this theme through the Japanese market.

This is in stark contrast to the logic of "carry unwind triggering a sell-off" seen in August 2024. That event was characterized by forced liquidation and indiscriminate selling, with capital exiting the Japanese market. In contrast, the net foreign buying in 2026 represents an active choice to enter the Japanese market to chase the AI reflation trade. The driving mechanisms are different, and their implications for the Nikkei index are also distinct.

Rate Hikes Don't Suppress Stocks, But This Relationship Is Becoming More Fragile

Another counterintuitive aspect of the Nikkei 225 is its sustained rise amid consecutive BOJ rate hikes.

According to the BOJ's policy meeting announcements, the rate hike path over the past two years is as follows: ending the negative interest rate policy in March 2024 by raising the policy rate from -0.1% to 0.1%; another hike in July 2024 to 0.25%; a hike in January 2025 to 0.5%; and a hike in December 2025 to 0.75%, the highest level since 1995. The April 2026 meeting kept the rate unchanged at 0.75%, but the vote passed 6 to 3—three board members (Hajime Takata, Naoki Tamura, Junko Nakagawa) explicitly advocated for a hike to 1.0%.

The chart clearly shows that the correlation between rate hike points and stock market trends differs significantly across phases. The July 2024 rate hike triggered a historic crash in the Nikkei 225, which fell 12.4% in a single day—this was because the BOJ rate hike coincided with weak U.S. non-farm payroll data, directly igniting the carry unwind. However, the two rate hikes in January and December 2025 were accompanied by the Nikkei 225 rising from around 40,000 points to its current new high of 68,634 points.

The reason behind this is not complicated: when the logic for foreign buying is chasing the AI reflation theme rather than relying on low-cost yen funding, small BOJ rate hikes have a relatively limited impact on this capital. Of course, this relationship is not fixed—if the BOJ's July meeting actually pushes the rate to 1.0%, and the dollar weakens due to other factors, the funding cost for carry trades would rise sharply, potentially causing the two trends to recouple.

Looking at the three charts together provides a relatively complete framework for understanding: yen short positions are still crowded, the Ministry of Finance's largest-ever intervention failed to hold the 160 line, but the new highs in Japanese stocks are driven by foreign AI capital. These three things are simultaneously true, are not contradictory to each other, and none alone can predict what will happen next.