HYPE hits new highs—should you buy $PURR, the "HYPE version of MicroStrategy"?

- Core Thesis: Hyperliquid Strategies (PURR) is a "DAT" company with no actual business operations. It operates solely by holding and staking HYPE tokens, meaning its stock value is entirely dependent on HYPE's price performance. Despite recent attention driven by HYPE's surge and institutional involvement, the argument comparing its capital efficiency to that of MicroStrategy (Strategy) is misleading. For investors, PURR essentially serves as a compliant channel for traditional finance to gain HYPE exposure, rather than a superior investment target.

- Key Elements:

- PURR's business model consists only of purchasing, staking, and holding HYPE. It currently holds approximately 20 million HYPE tokens and $113 million in cash, with no actual business operations, making its stock price entirely dependent on HYPE's price.

- PURR was formerly a biotech company, restructured by institutions such as Paradigm and Atlas Merchant Capital through a SPAC merger. Its management team largely comprises traditional finance veterans, including a former Barclays CEO and a former NYSE COO.

- HYPE has surged over 150% year-to-date, rising from around $25 to over $62, making it one of the strongest crypto assets of 2025 and directly driving PURR's gain of over 100%.

- Institutions like Goldman Sachs, 21Shares, and Bitwise have recently disclosed holdings of PURR shares or have launched HYPE spot ETFs. This, combined with Cantor Fitzgerald raising its price target, forms a positive market catalyst.

- The comparison suggesting "capital efficiency surpassing MicroStrategy" is misleading: PURR's cost basis for HYPE is around $7 (a nearly 9x gain), while MicroStrategy's cost basis for BTC is around $75,000 (hardly any gain). The return difference stems from the performance of the underlying assets, not management skill.

- PURR currently trades at an approximately 11%-23% discount to its coin holdings value (mNAV), but this could turn into a premium after accounting for newly issued shares. Dilution risk, incomplete pass-through of returns, trading time restrictions, and counterparty risk are the main disadvantages compared to directly holding the token.

- For investors capable of directly purchasing HYPE, PURR's stock wrapper layer introduces additional costs (e.g., dilution, taxation, transaction friction) without offering excess returns. Its core value lies solely in providing a compliant channel for traditional accounts (like IRAs) that are restricted from holding the token directly.

Author: Deep Tide TechFlow

On May 24, a tweet about Hyperliquid Strategies (NASDAQ: PURR) sparked considerable discussion in English crypto Twitter:

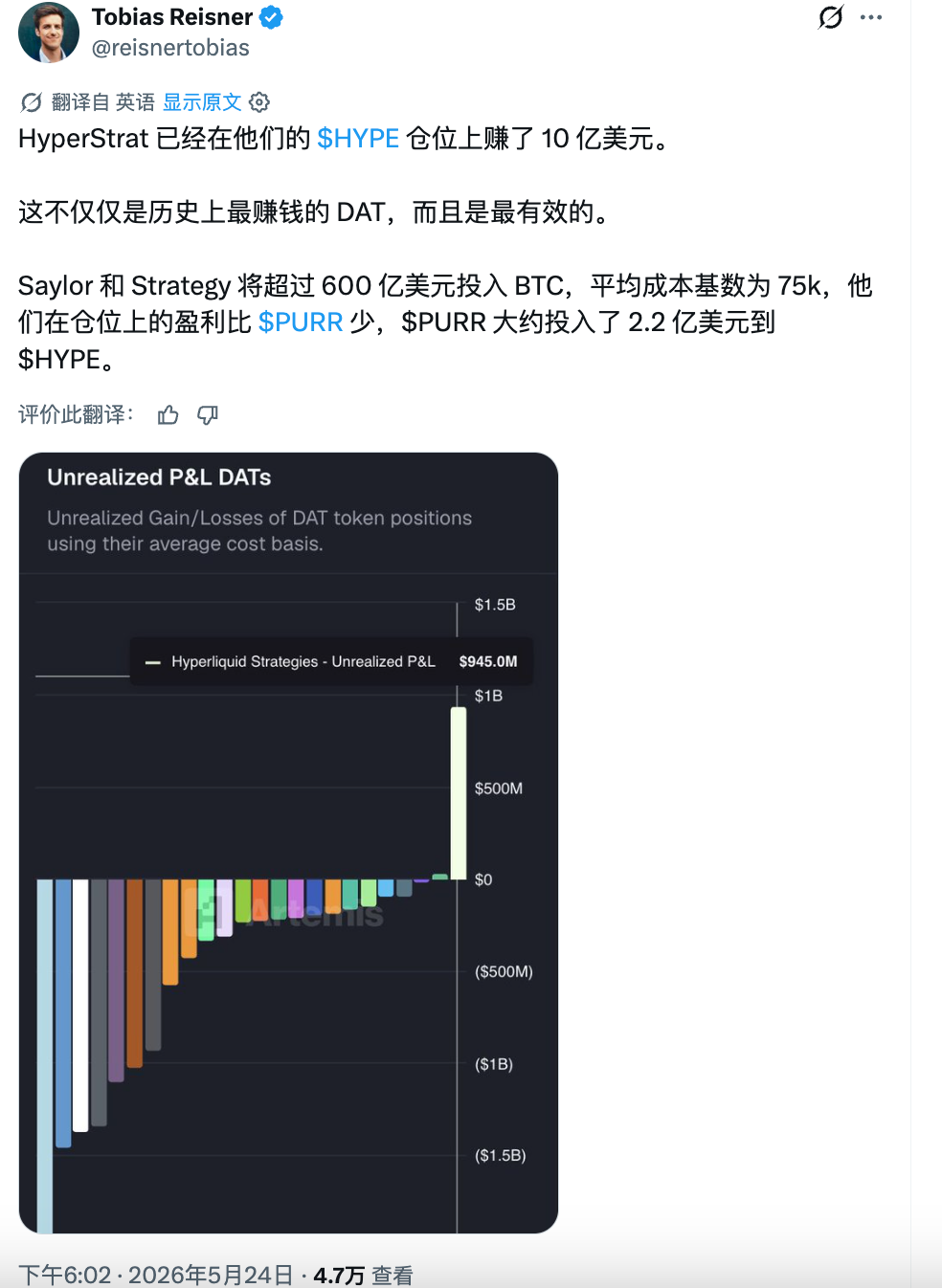

The company used approximately $220 million to purchase HYPE, with unrealized profits now approaching $1 billion, surpassing even the efficiency of Michael Saylor's Strategy (formerly MicroStrategy) in Bitcoin gains.

This discussion is now gradually spreading to Chinese-speaking circles. HYPE recently hit a new all-time high above $62, with year-to-date gains exceeding 150%, making it one of the best-performing major crypto assets this year.

As the only publicly traded proxy for HYPE in the US stock market, PURR has also surged over 100% year-to-date, naturally becoming a FOMO target in US equity research.

But before jumping on the bandwagon, several questions need to be clarified:

1. What exactly is this company?

2. How is it different from buying HYPE directly?

3. Does the claim of "capital efficiency surpassing MicroStrategy" hold up under scrutiny?

$PURR: Pure DAT

First, the conclusion: PURR is not a company with actual business operations; it is essentially a pure $HYPE stock wrapper product.

Its business model is simple: Buy HYPE, stake HYPE, hold HYPE. As of April 2026, public information shows the company holds approximately 20 million HYPE, along with about $113 million in cash and zero debt.

This means that the entire value of the stock depends on one thing: the price of HYPE.

Since there is no business to analyze, evaluating such a company comes down to two dimensions: the underlying asset itself and who is running the shell.

The latter determines capital operation capabilities, such as when to issue shares to buy coins, when to conduct buybacks to support the price, and how to manage the premium/discount relationship between the stock price and net asset value. It also determines whether institutional capital is willing to enter through this vehicle.

Historically, PURR was formerly Sonnet BioTherapeutics, a small-cap biotech company listed on Nasdaq. In July 2025, it announced a merger with Rorschach I, completing the transaction in December of the same year. The overall valuation was $888 million, and it was renamed Hyperliquid Strategies with the ticker PURR.

Notably, the deal was initiated by Paradigm and Atlas Merchant Capital.

Paradigm is one of the top venture capital firms in the crypto industry, with investments in projects like Uniswap, Blur, and Friend.tech. It has deep ties to the Hyperliquid ecosystem and directly participated in forming the SPAC.

Atlas Merchant Capital is a financial services investment firm based in New York and London. Its two founders secured key positions at PURR: Chairman Bob Diamond, former CEO of Barclays, and CEO David Schamis, former partner at J.C. Flowers.

The board also includes former Boston Fed President Eric Rosengren and former NYSE COO Larry Leibowitz. Other participants include Galaxy, D1, and Pantera—all top-tier institutions in crypto and macro finance.

Most DAT companies have management teams from the crypto-native world, but PURR is almost entirely staffed by traditional finance veterans.

$HYPE's Strength Lifts $PURR

PURR caught the attention of Chinese-speaking circles primarily due to HYPE's own strong performance.

HYPE surged from around $25 at the start of the year to a new all-time high above $62 in May, marking year-to-date gains of over 150%. Against a backdrop of BTC trading sideways and ETH and SOL showing lackluster performance this year, HYPE stands out as the most impressive major crypto asset.

Our previous article has already analyzed Hyperliquid's fundamental flywheel: approximately 70% market share in perp DEXs, weekly fee revenue exceeding $10 million, and 97% of protocol fees used to buy back and burn HYPE. This flywheel continues to accelerate.

(Reference: Market Observation: From HYPE to ZEC, Grasping 4 Narrative Lines Behind Recent Altcoin Hype)

As HYPE rises, PURR naturally follows suit.

As the only HYPE proxy listed on US stock exchanges, PURR has gained over 100% year-to-date, rising from the $3 range to a recent high of $8.79.

For investors who only have US stock accounts and no direct exposure to the crypto market, PURR is almost the only way to gain HYPE exposure. However, what turned PURR from a "niche asset" into a "social media topic" were several institutional signals that materialized in May.

Goldman Sachs disclosed in its Q1 13F filing that it had purchased approximately 650,000 shares of PURR. While the amount is modest (around $3.3 million), the Goldman Sachs name itself serves as an endorsement. Around the same time, HYPE spot ETFs from 21Shares and Bitwise were listed on Nasdaq and NYSE respectively, and Cantor Fitzgerald raised its PURR price target from $6 to $8.

These events, coinciding with HYPE's new highs, propelled PURR into the spotlight for more people.

Then came the tweet mentioned at the start of the article: PURR used $220 million to buy HYPE, with unrealized gains now approaching $1 billion. In the short term, its capital efficiency certainly surpasses that of MicroStrategy.

A massive price surge naturally attracts significant attention. However, if you are considering trading this stock, caution is warranted.

The Most Capital-Efficient DAT? Really?

Strategy (formerly MicroStrategy) invested over $60 billion to buy BTC, with an average cost of around $75,000. PURR only used about $220 million to buy HYPE, yet its unrealized gains approach or even exceed those of Strategy. Does this mean PURR's "capital efficiency" is far superior to MicroStrategy's?

The comparison works on a numerical level, but it is misleading logically.

PURR's early HYPE holdings had an average cost of about $7, and the current price of $62 represents an increase of nearly 9 times. Strategy's average BTC cost is around $75,000, and BTC is currently hovering around that level, showing almost no gain.

Therefore, PURR's higher unrealized gains are not due to any smarter actions by the company; rather, the magnitude of the underlying asset's price appreciation is entirely on a different scale. Anyone who bought HYPE directly with the same amount of money at the same time would have achieved the same return, without bearing the risk of equity dilution.

In other words, this is the triumph of "picking the right coin." If PURR had been formed six months later, entering when HYPE was at $40, this "capital efficiency" narrative would completely fall apart.

For US stock investors paying attention to PURR today, the more practical question is: Are you paying a premium or a discount relative to the value of HYPE held by the company?

This leads to the core valuation metric for DAT companies—mNAV (Modified Net Asset Value per share).

We pulled data from PURR's official dashboard and SEC filings to perform a simple mNAV calculation.

The company currently holds 20.8 million HYPE (worth approximately $1.296 billion at current prices). Adding $114 million in cash and deducting deferred tax liabilities and other liabilities, the net asset value is approximately $1.34 billion.

Based solely on the 134.6 million shares outstanding, the NAV per share is approximately $9.98. At the current stock price of $7.67, this represents a discount of about 23%. If the approximately 29.8 million outstanding warrants are included, the fully diluted share count rises to about 155 million, reducing the NAV per share to approximately $8.66, a discount of about 11%. However, the company has just registered 35.16 million new shares for issuance. If all of these are exercised, the total share count would expand to about 190 million, lowering the NAV per share to $7.07. In this scenario, the stock price actually trades at a slight premium of 1.08 times NAV.

Therefore, whether PURR is "cheap" or "expensive" depends on how much future dilution you anticipate.

Share issuance itself is not necessarily a bad thing. If management issues shares at a high premium and uses the proceeds to buy more HYPE, the amount of HYPE per share could actually increase. However, if sentiment cools and the stock price falls below NAV while the company continues to issue shares, that would dilute existing shareholders.

This company has only been around for six months and has not yet experienced a full market downturn. There is no track record to reference regarding how management would operate under extreme conditions.

Another point to note: the above calculation uses a deferred tax liability of $60.5 million as of the Q3 earnings cut-off date (March 31). However, HYPE has risen significantly since the end of March, which means the tax liability associated with unrealized gains has likely increased further. The actual NAV may be slightly lower than our estimate.

What's the Difference Between Buying PURR and Buying HYPE Directly?

This is the most practical question. Since all of PURR's value comes from HYPE, why not skip the middle layer and buy HYPE directly?

The answer is simple: some investors simply cannot buy it directly. US retirement accounts (IRAs, 401(k)s), traditional brokerage accounts, and certain institutionally managed funds with strict compliance requirements cannot directly hold crypto assets.

Furthermore, the Hyperliquid platform's interface explicitly restricts access for US residents.

Therefore, PURR provides a Nasdaq-listed stock wrapper that allows these funds to gain HYPE exposure through standard stock trading. The shell structure built by Paradigm essentially sells this compliance channel.

For investors in this category, PURR is indeed currently the only viable option. While HYPE spot ETFs from 21Shares and Bitwise were launched in mid-May, these products have been available for an extremely short time, and their liquidity and tracking error remain to be seen.

But if you are capable of buying HYPE directly, then PURR's stock wrapper becomes a pure friction cost with negative effects; it cannot be considered a source of HYPE Beta returns.

This cost manifests at several levels:

First, dilution risk. By holding HYPE directly, your share cannot be diluted by others. However, by holding PURR stock, the company can issue new shares at any time to buy more HYPE.

Second, incomplete yield transmission. Holding HYPE directly allows you to stake it yourself for staking rewards, and future airdrops and ecosystem incentives go directly to you. By holding PURR, staking rewards first go into the company's accounts. After deducting operating expenses and taxes, they are only indirectly reflected in the net asset value per share.

Third, trading hours and pricing friction. HYPE trades 24/7, while PURR only trades during US market hours. If HYPE experiences significant volatility over the weekend or after hours, PURR holders can only react when the market opens.

Fourth, counterparty risk. SEC filings reveal that all of PURR's HYPE holdings are stored with a single custodian. By holding PURR, the safety of your assets depends on the custodian's performance and the company's operational continuity.

My assessment is that PURR is more of a "channel product" than an "investment product." Its value lies in opening a channel from traditional financial accounts to HYPE, and nothing more. If you don't need this channel, every additional risk introduced by the middle layer is unnecessary.

Therefore, for crypto and US stock investors in the Chinese-speaking world, the conclusion is straightforward:

The question you need to answer is whether you are bullish on HYPE, not whether you are bullish on the PURR shell.