六巨头诸神之战:13F 美股持仓全景,顶级机构开始互为对手盘?

- 核心观点:2026年Q1美股顶级机构13F持仓文件显示,华尔街对AI领域的投资共识已破裂,从共同买入转向内部激烈分歧。机构不再笼统投资“AI”,而是基于不同假设对平台层、应用层、硬件层进行分层定价,形成清晰的对手盘格局。

- 关键要素:

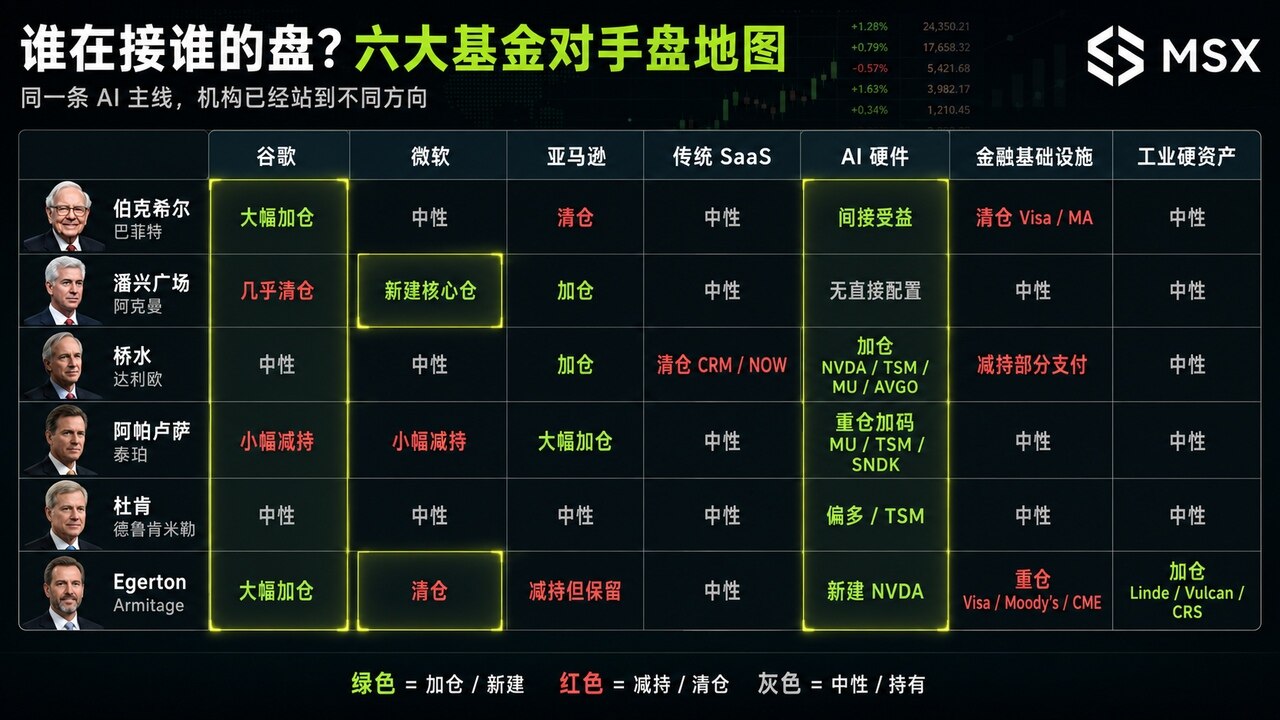

- 谷歌(Alphabet)成为最大分歧样本:伯克希尔大幅加仓,押注现金流与低估值修复;阿克曼的潘兴广场近乎清仓,担忧生成式AI颠覆搜索商业模式。

- AI交易从“泛化”进入“分层”:机构持仓分化为三条主线——平台层(微软、谷歌)、应用层(Salesforce被抛售)、硬件与基础设施层(NVIDIA、台积电被集中买入)。

- 传统SaaS(如Salesforce)遭桥水基金大幅清仓,而AI硬件(NVIDIA、台积电)获增持,反映机构从“软件中间商”撤向“AI硬通货”的结构性转变。

- 微软也出现明显分歧:阿克曼新建仓位,看好Azure与企业AI;Egerton Capital清仓微软,认为其AI溢价已被透支。

- 伯克希尔清仓亚马逊、Visa,同时加仓谷歌,体现了在高位市场下精简组合、严守估值纪律的趋势,而非长期持有同一资产。

The Q1 2026 portfolio adjustments of six major fund managers have been revealed.

As is widely known, mid-May each year marks one of the most noteworthy time windows for global stock markets. At this point, major institutions must submit their 13F filings to the U.S. Securities and Exchange Commission (SEC), disclosing their holdings at the end of the previous quarter. Although 13F filings inherently have a lag, typically submitted within 45 days after the quarter ends, they are not suitable for "real-time copycat trading." However, they are excellent for observing how institutional funds reassessed the market's main narrative in the previous quarter.

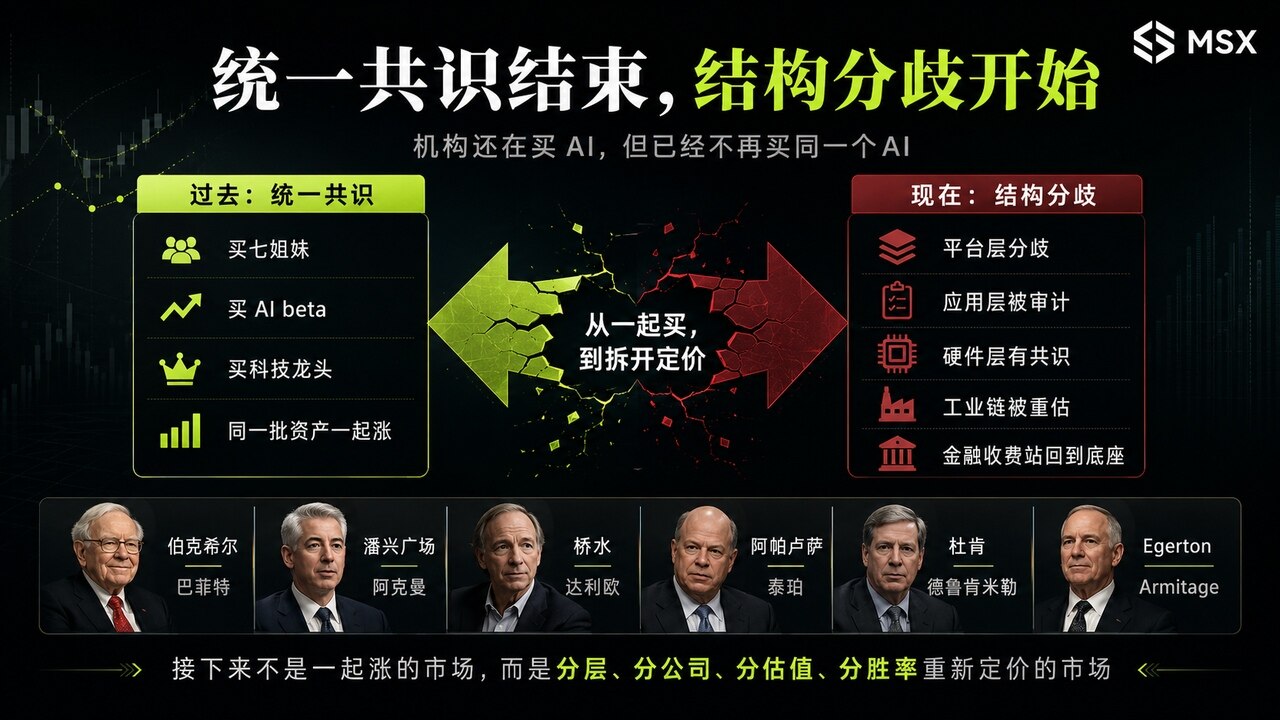

The most important change in the Q1 2026 13F filings is not about which stock was bought by whom, nor is it about which major investor liquidated what. Instead, it is that the consensus among top Wall Street funds has begun to fracture.

For the past few years, the U.S. stock market had a very clear, shared narrative: buy the Magnificent Seven, buy AI, buy leading platforms, buy high-quality tech. While capital flows had different timings, the general direction was the same. But this time is different – for instance, with Google, some are frantically adding to their positions while others are almost completely selling off; with Amazon, some have sold out entirely while others continue to hold heavy positions; with Microsoft, some are establishing new core positions while others are directly liquidating them. Traditional SaaS has been heavily liquidated by Bridgewater, yet AI hardware and computing infrastructure are being aggressively bought by another set of funds.

This indicates a clear divergence in their judgments on "which layer will ultimately capture the profits from AI," "which company's moat will be reevaluated by AI," and "which valuations have already discounted the future."

Therefore, this batch of 13F filings is not simply a list of holdings. It is more akin to a map of Wall Street's counterparty risks.

1. The Core Change: Consensus Shifts from "What to Buy" to "Who is Dumping on Whom"

The most notable trend in this 13F season is that institutions have begun acting as counterparties to each other within AI-related assets.

In the past, institutional trading in U.S. stocks was more like a wide river, with everyone heading in a similar direction, differing only in position size and timing. Now, it's more like a fork in the road. Everyone knows AI is the main theme, but no one is willing to pay the same valuation for the same story anymore:

- Some buy Google because it's cheap, has strong cash flow, and YouTube and Search still have moats; others sell Google because AI-powered search could directly undermine its core business model.

- Some buy Microsoft because Azure and the enterprise AI gateway offer more certainty; others liquidate Microsoft because the market has already priced in an excessive AI premium.

- Some buy Amazon because AWS remains the core platform for AI cloud capital expenditure; others sell Amazon because their portfolio no longer needs to bear the risk of such high-valuation platforms.

- Some are fleeing Salesforce and ServiceNow because the intermediary value of traditional SaaS is being compressed by AI; others are buying NVIDIA, TSMC, Micron, and SanDisk because, regardless of which AI application wins, the underlying hardware must be purchased first.

So, the core of this 13F season is not simply "buy AI."

Rather, AI as a unified concept is disintegrating. Institutions are beginning to break it down into the platform layer, application layer, hardware layer, industrial capex layer, and financial tollbooth layer, and are repricing them accordingly.

Let's dissect each major player in detail.

1. Berkshire Hathaway: Redrawing the Lines in the Post-Buffett Era

Objectively speaking, Q1 2026 represents the first complete observation window for Berkshire Hathaway as it enters the post-Buffett era.

The most fascinating aspect of this 13F filing is that it did two seemingly contradictory things simultaneously: significantly streamlining its portfolio while also significantly increasing its stake in Google (Alphabet).

According to public reports, Berkshire substantially increased its Alphabet holdings in Q1, while also establishing new positions in Delta Air Lines and Macy's, and liquidating holdings in Amazon, Visa, Mastercard, UnitedHealth, and others:

- Liquidating Amazon, Visa, and Mastercard indicates it no longer wishes to hold all seemingly high-quality business models from the past.

- Increasing its position in Google signifies it is not moving away from tech. Instead, it is seeking assets within tech that align more closely with Berkshire's traditional investment philosophy: strong cash flow, reasonable valuation, significant market controversy, but with underlying business models not yet fully disproven.

This is precisely why Google has become the biggest point of divergence in this 13F season. Berkshire isn't buying an "AI story"; it's buying a cash flow giant that is being re-evaluated by the market. It is betting on the side that "Google's moat still holds value."

2. Pershing Square: Ackman Takes the Opposite Side of Buffett

If Berkshire was one of the largest buyers of Google this quarter, then Bill Ackman is the quintessential counterparty.

The most striking move by Pershing Square in Q1 was nearly liquidating its entire Alphabet position and establishing a new position in Microsoft. In his public explanations, Ackman emphasized that Microsoft's valuation became more attractive after its stock price correction, and the long-term growth potential of Azure, Microsoft 365, and enterprise AI remains strong. In other words, he rotated his tech exposure from Google to Microsoft.

This presents a stark contrast to Berkshire. In essence, Berkshire sees resilience in Google's search, YouTube, cloud, and advertising cash flows, while Ackman sees the risk of generative AI disrupting the search gateway.

One believes Google is undervalued; the other believes Google's moat is being repriced. To put it bluntly, Ackman hasn't given up on AI; he simply believes Google is not the highest-conviction bet in this AI trade.

3. Bridgewater Associates: Dalio Sells Software, Buys Hardware

Bridgewater's 13F filings are always complex, as its decisions are driven by macro allocation rather than single-company calls.

However, Bridgewater's direction this time is very clear: selling traditional software, buying AI hardware.

Public tracking of Bridgewater's 13F shows it exited Salesforce in Q1 and notably shifted towards AI hardware and infrastructure players like NVIDIA, TSMC, and Amazon. Market reports also indicate TSMC was one of Bridgewater's major new positions this quarter, while Salesforce was a key exit. This trajectory is highly significant.

It indicates Bridgewater is not simply bullish on tech; it is executing a rotation within the tech sector's industrial chain. Over the past decade, traditional SaaS boasted one of the most comfortable business models: subscription revenue, customer stickiness, high margins, and excellent cash flow. However, with the advent of AI, the valuation logic for traditional SaaS is being reevaluated.

If large language models can automatically generate code, automate workflows, and replace some enterprise software functions, the value of the traditional SaaS intermediary layer will be compressed. So, Bridgewater isn't retreating from tech stocks; rather, it's shifting from "software middlemen" to "AI hard currency."

Assets like NVIDIA, TSMC, Micron, Broadcom, Oracle, and Amazon represent computing power, wafer fabrication, memory, networking, cloud, and infrastructure. Their commonality is that regardless of which AI application ultimately wins, the underlying capital expenditure will likely flow through these stages first.

In a nutshell, Bridgewater isn't buying the AI concept; it's buying the money that AI must spend.

4. Appaloosa Management: Tepper Bets on 'Essential Hardware for Everyone'

David Tepper's Appaloosa Management also provided a very strong directional signal in Q1.

Public reports show Appaloosa significantly increased its positions in Amazon and Uber in Q1, exited airline stocks, added SanDisk, and continued to raise its exposure to semiconductor and AI hardware chain assets like Micron and TSMC.

Tepper's logic is similar to Bridgewater's and quite straightforward: The ultimate winner of AI doesn't matter; first, buy everything that all winners must procure:

- Micron represents HBM and memory;

- TSMC represents advanced process technology and foundry capacity;

- SanDisk represents the storage chain;

- Amazon represents the AWS cloud infrastructure;

These are not pure AI application stories, but rather the hardware, cloud, and infrastructure in the AI arms race. Of course, upon closer inspection, while this overlaps with Bridgewater's approach, Tepper is more concentrated and more aggressive.

Put another way, Bridgewater's is a macro-driven "increase hardware, decrease software" allocation. Tepper seems to be directly betting that the AI computing cycle is not over, and the chain best positioned to secure orders and cash flow is the hardware and infrastructure one.

In a nutshell, Tepper is buying the pick-and-shovel sellers, specifically those closest to the computing bottleneck.

5. Duquesne Family Office: Druckenmiller's Signal is 'Don't Chase the Hottest Areas'

Stanley Druckenmiller's Duquesne Family Office differs from the previous firms.

It is not the most typical large buyer of AI hardware this quarter. However, its significance lies in representing another institutional mindset: don't linger too long in the most crowded trades.

Druckenmiller has previously reduced or exited positions in popular AI concepts like NVIDIA and Palantir while consistently focusing on more upstream parts of the supply chain like TSMC. Public reports also show that macro-driven funds like Duquesne are characterized by rapid adjustments rather than clinging to a single narrative for the long term.

This is highly consistent with the main theme of this 13F season: When the market speculates on the AI application layer into a consensus, truly sensitive macro capital has already begun moving towards more upstream, fundamental, and cheaper links.

In a nutshell, he doesn't stand where the crowd is thickest, but instead goes early to areas where the market hasn't fully priced things in yet.

6. Egerton Capital: Liquidates Microsoft, Adds Google, NVIDIA, and Industrial Hard Assets

Egerton Capital didn't just buy AI; it also bought financial infrastructure and industrial hard assets. More importantly, it liquidated its Microsoft position, positioning itself as the opposite of Ackman.

Public 13F tracking shows Egerton Capital's Q1 13F portfolio was approximately $9 billion. Its top five holdings included Visa, Alphabet, Moody's, Linde, and Carpenter Technology. It also established or increased positions in NVIDIA, Linde, Devon Energy, and Canadian Natural Resources.

This set of holdings is very interesting. It's not simply buying the Magnificent Seven. Instead, it breaks the portfolio into several lines:

- Line 1: Financial infrastructure – Visa, Moody's, CME, Interactive Brokers, Mastercard;

- Line 2: AI platforms and computing – Alphabet, NVIDIA;

- Line 3: Industrial hard assets and capital expenditure – Linde, Vulcan Materials, Carpenter Technology, Amphenol;

- Line 4: Energy and resources – Devon Energy, Canadian Natural Resources;

This shows Egerton isn't buying a single AI story. It is buying the intersection of the AI cycle, industrial capex, and financial tollbooths.

Most critically, its liquidation of Microsoft creates a clear counterparty position with Ackman.

Ackman believes Microsoft has a higher probability of success in the enterprise AI gateway and Azure, so he built a new position. Egerton chose to eliminate Microsoft, allocating its tech exposure more towards Google and NVIDIA.

Same AI theme, same quality growth, yet different institutions arrived at completely opposite conclusions.

2. Horizontal Comparison: Who is Actually Acting as Counterparty to Whom?

1. Google: The Ultimate Example of Divergence in This 13F Season

It can be said that Google is the asset most worthy of a standalone discussion in this 13F season: Berkshire significantly increased its stake, Egerton also increased its Alphabet holdings, but Ackman nearly liquidated his.

This illustrates that Google has transitioned from a consensus tech leader to a divergent asset. The bullish side argues that Google's search, YouTube, cloud, and advertising cash flows remain strong; its valuation is relatively less expensive; and the market has overly amplified the AI impact. The bearish side argues that generative AI could change the search gateway; the advertising business model faces reevaluation; Google Cloud and Gemini need to prove their commercial efficiency; and capital expenditures could pressure profit margins.

So, Google is not a case of "institutions are all buying" or "institutions are all selling." It acts more like a moat stress test.

Those buying Google are buying cash flow and a low-valuation recovery story. Those selling Google are selling the risk that AI search will disrupt its old gateway.

2. Microsoft: Seen as an Enterprise AI Gateway by Some, Overpriced by Others

Microsoft is also a stock with significant divergence this quarter.

Ackman built a position in Microsoft because he sees long-term certainty in Azure, Microsoft 365, and enterprise AI. However, Egerton's liquidation of Microsoft indicates that another type of institution is unwilling to continue paying an excessively high AI platform premium for Microsoft.

This divergence is crucial. Microsoft is not being abandoned by the market, but it is no longer an uncontested consensus asset.

Its problem poses a classic question for high-flying tech stocks: Has the "good company" premium been fully baked into the stock price in advance? The business can continue to perform well, but the stock price may have already discounted several years of future growth.

3. Amazon: Buffett Sells, Ackman and Tepper Buy

Amazon is not a consensus holding either.

Berkshire liquidated its Amazon position, but Ackman and Tepper still value it. Bridgewater also kept it as an important holding. Even Egerton, despite reducing its stake, retained a position.

The divergence here is whether Amazon represents a high-valuation platform risk or a core piece of infrastructure in the AI cloud capex cycle.

Bullish observers point to AWS, the e-commerce base, advertising business, and AI cloud demand. Bearish observers see portfolio simplification, valuation discipline, and the need for rebalancing platform assets.

So, Amazon isn't about a "moat controversy" like Google. It's more of a "portfolio position controversy." Institutions seem to be questioning whether, at the current price and within their portfolio structure, they still need such a large exposure to Amazon.

4. Traditional SaaS: From Safe Haven Asset to Audited Asset

Bridgewater's liquidation of Salesforce and ServiceNow is one of the most structurally significant actions in this 13F season.

It's not simply selling two stocks. It represents the market beginning to re-examine the business model of traditional SaaS. Historically, SaaS was a high-quality asset, profiting from subscriptions, stickiness, data, and workflow processes. However, after the generalization of large AI models, the value of the middle layer in enterprise software is being challenged.

If many processes can be automated by AI, code generated by AI, and software functions directly invoked by large models, then the high valuations of traditional SaaS need a new explanation.

This is precisely why, in this 13F season, traditional software and AI hardware have formed a very clear counterparty relationship. One side sells software middlemen; the other buys computing, memory, foundry capacity, cloud, and hardware infrastructure.

5. Financial Infrastructure: Buffett Sells, Egerton Buys

Visa and Mastercard also exhibit interesting divergence.

Berkshire liquidated its Visa and Mastercard holdings, yet Visa is Egerton's top holding, alongside other financial infrastructure assets like Moody's, CME, and Interactive Brokers. This indicates that financial tollbooths haven't lost their value.

It's simply that different institutions hold divergent views on their role in a portfolio. Berkshire might be cleaning its portfolio and trimming older positions. Egerton views assets like Visa and Moody's as long-term cash flow anchors.

So, this is not simply a "payment stocks are doomed" scenario. Rather, financial infrastructure is no longer a no-brainer consensus, but it remains a high-quality core holding in the eyes of some institutions.

3. How Should We Understand This 13F Season?

Many might say: This 13F season still looks like everyone is buying AI. How can you say consensus is gone?

The key point is that while the directional consensus on AI remains, the beta consensus on AI is gone.

As everyone knows, in the past, buying AI, the Magnificent Seven, tech leaders, or semiconductor ETFs would likely track the main