Gate Institutional Weekly Report: BTC Short Squeeze Momentum Slows, Aave Funding Rates Return to Rational Levels

- Key Insights: Last week, the market shifted from hedging against geopolitical conflicts to trading a soft economic landing and expectations of interest rate cuts. BTC broke through $82,000 driven by sustained ETF capital inflows. On-chain TradFi transactions were dominated by macro assets like gold, but capital has begun to flow back into leading DEXs and compliant stablecoins, indicating a recovery in risk appetite but with structural caution.

- Key Elements:

- BTC ETFs saw a net inflow of $631.6 million for the week, with IBIT leading at a net inflow of $596.3 million; ETH ETFs recorded a net inflow of $70.3 million, turning positive from negative driven by ETHA.

- In the perpetual contract transaction structure of TradFi, precious metals still account for over 60%, but the number of CEX stock-type assets has increased by 25.9% since the end of April, signaling that capital is beginning to pay attention to US stock indices alongside the macro trading narrative.

- On-chain funds are flowing back to leading DEXs like Uniswap and PancakeSwap; stablecoin trading is favoring compliant and cross-chain settlement assets. Circle received MiCA authorization in France and integrated USDC into Injective.

- Aave is still absorbing the impact of the rsETH incident, with lending scales contracting. However, the new public chain MegaETH has absorbed some of the new loan demand, and Aave is shifting its growth focus towards Euro stablecoins and new chain markets.

- The BTC derivatives market shows a short-squeeze structure characterized by "negative funding rates + high-level consolidation." Open Interest (OI) declined after a spike and has not risen with the price, indicating that upward momentum stems mainly from short covering rather than new leveraged buying.

- BTC options trading volume concentrated during the breakout phase and then cooled down. Implied volatility declined and stabilized after the spike, placing the market in a high-level consolidation observation phase, with short-term directional pricing not yet fully established.

- In May, Gate's institutional spot trading volume increased by 14.54% month-over-month, and futures trading volume increased by 18.10% month-over-month. CrossEx has seen consecutive weekly highs in trading volume and asset balance for three weeks, with demand for cross-exchange arbitrage continuing to grow.

Summary

• Last week, the market shifted from "war risk-off" to "soft landing + rate cut expectations" trading. The Middle East ceasefire proposal released positive signals, and strong earnings reports from AI and tech companies drove the Nasdaq up 4.70% for the week. BTC broke through $82,000, fueled by continuous ETF inflows.

• BTC ETFs saw net inflows of $632 million for the week, with IBIT continuing to dominate institutional capital; ETH ETFs turned positive from negative, with ETHA becoming the main source of incremental inflows, indicating a significant improvement in institutional allocation sentiment.

• TradFi on-chain trading is dominated by macro assets like gold and crude oil, while stock and ETF-related transactions continue to recover market share; the number of TradFi assets on CEXs continues to expand, with stock-related categories seeing the most growth.

• On-chain capital flows are returning to leading DEXs and mature liquidity venues, with Uniswap and PancakeSwap as core platforms; stablecoin markets favor USD-backed assets with stronger compliance, settlement, and cross-chain capabilities.

• Aave is still digesting the impact of the rsETH incident, with the lending market remaining weak; new venues like MegaETH and Plasma are starting to absorb incremental capital, with Solana LSTs being the first to benefit from the recovery in risk appetite.

• The derivatives market continues its structure of "negative funding rates + high-range consolidation"; the BTC short squeeze was partially triggered. Options volume and implied volatility expanded during the breakout phase but subsequently cooled down.

• In May, Gate Institutional's spot volume increased 14.54% month-over-month, while futures volume grew 18.10% month-over-month. CrossEx's trading volume and asset under custody hit new highs for three consecutive weeks. Preparations for the Gate Institutional Circle Amsterdam event are underway.

1. Market Focus Interpretation

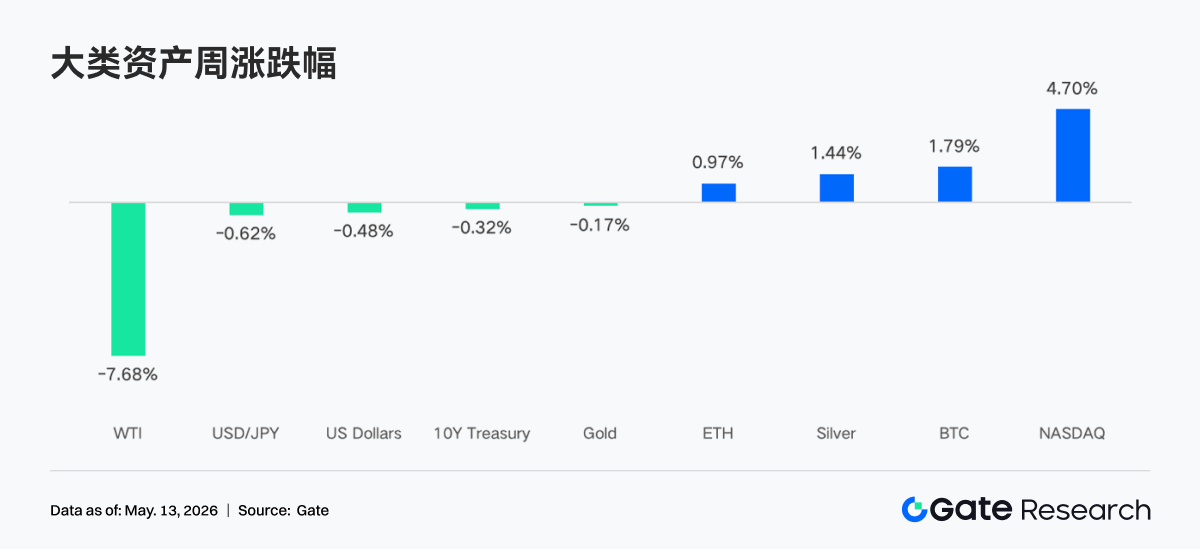

The US proposed a ceasefire plan with substantial progress, covering 14 articles including a suspension of Iran's nuclear enrichment activities, a phased lifting of sanctions, and the removal of restrictions related to the Strait of Hormuz. Sources say this is the closest the two sides have come to an agreement since the conflict began. The market reacted positively to this news, combined with strong Q1 earnings across various sectors, especially technology and AI companies, propelling the Nasdaq index up 4.70% for the week, reaching a new recent high. Meanwhile, although geopolitical conflicts provided support for gold and silver, the sharp drop in crude oil prices (WTI fell 7.68% for the week) due to eased supply disruption concerns, coupled with cooling inflation expectations, limited gold's gains. In the cryptocurrency space, Bitcoin steadily broke through the $82,000 mark, driven by continued spot ETF inflows and improved market liquidity. In the forex market, the US dollar index weakened due to the Fed's dovish stance, supporting a slight rebound in the Japanese Yen.

Despite the impact of the oil crisis, the latest labor market data continues to show improvement. Non-farm payrolls increased for two consecutive months in March and April, hitting new highs in nearly a year, bringing the average monthly private sector job growth this year to nearly 90,000. Meanwhile, the unemployment rate has fallen from its 2025 peak, with the latest April data showing a rate of 4.3%, flat year-over-year. Overall, the market has shifted from the early-week "war panic" to an optimistic pricing of "economic soft landing" and "room for Fed rate cuts."

2. Liquidity Analysis

2.1 BTC ETF Scale Continues to Expand

Last week, BTC ETFs exhibited a "strong start, weak finish" pattern, recording net inflows for the first three trading days, followed by net outflows in the last two. Total net inflows for BTC ETFs were $631.6 million for the week, a significant increase from the previous week, with overall market sentiment being positive. Total net inflows for ETH ETFs were $70.3 million for the week, a clear improvement from the previous week, turning negative to positive.

• Overall AUM Situation: As of May 8th, total net assets under management for BTC ETFs were approximately $106.77 billion, with historical cumulative net inflows exceeding $59.4 billion. Total net assets for ETH ETFs were approximately $13.6 billion, with historical cumulative net inflows of about $12.1 billion, representing approximately 4.94% of Ethereum's total market cap. BTC ETF scale continues to expand. IBIT's AUM alone has reached approximately $66.9 billion, accounting for about 66% of the entire BTC ETF market, surpassing the size of most traditional commodity ETFs.

• Institutional Moves: Capital flows diverged significantly this week. IBIT dominated with net inflows of $596.3 million for the week, solidifying its leading position in institutional allocation. ARKB ranked second with $53.1 million, indicating sustained institutional interest in higher-beta strategy products. In contrast, FBTC saw net inflows of only $52.2 million for the week, with significant outflows on Thursday and Friday totaling $226.6 million, reflecting a more cautious stance by institutions towards Fidelity's product. GBTC continued its structural outflow, totaling $62.3 million for the week. For ETH ETFs, ETHA led with $100.1 million in net inflows, while FETH was dragged down by a single-day outflow of $62.3 million on Thursday, resulting in a net outflow of $32.2 million for the week, showing a clear divergence in trend between the two major ETH products.

2.2 TradFi Liquidity

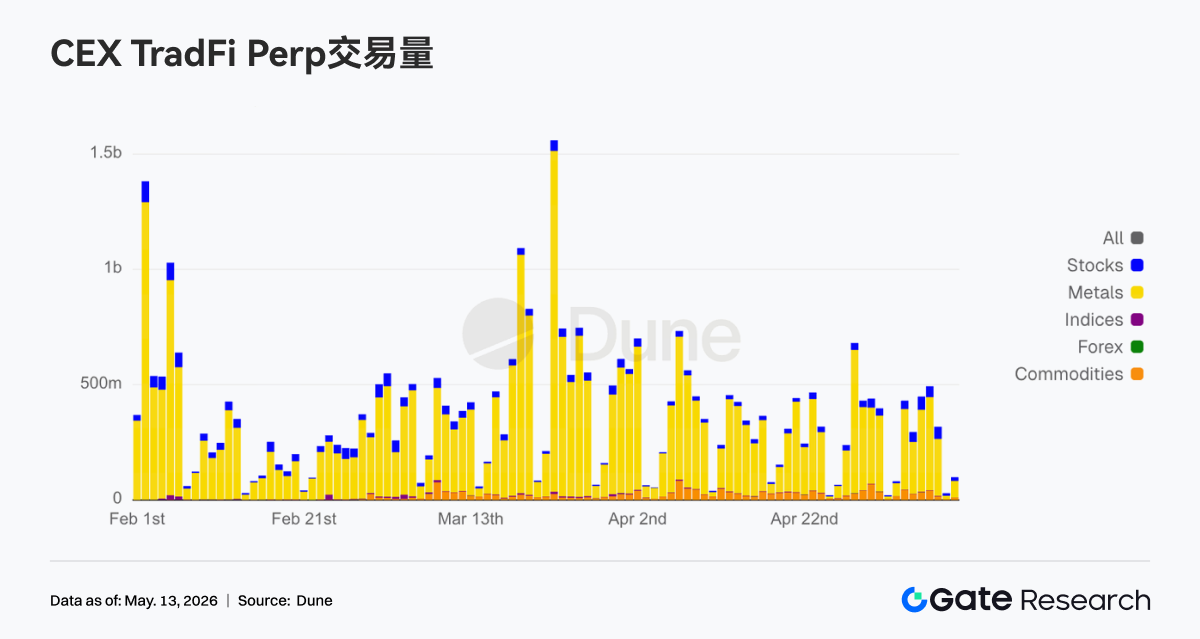

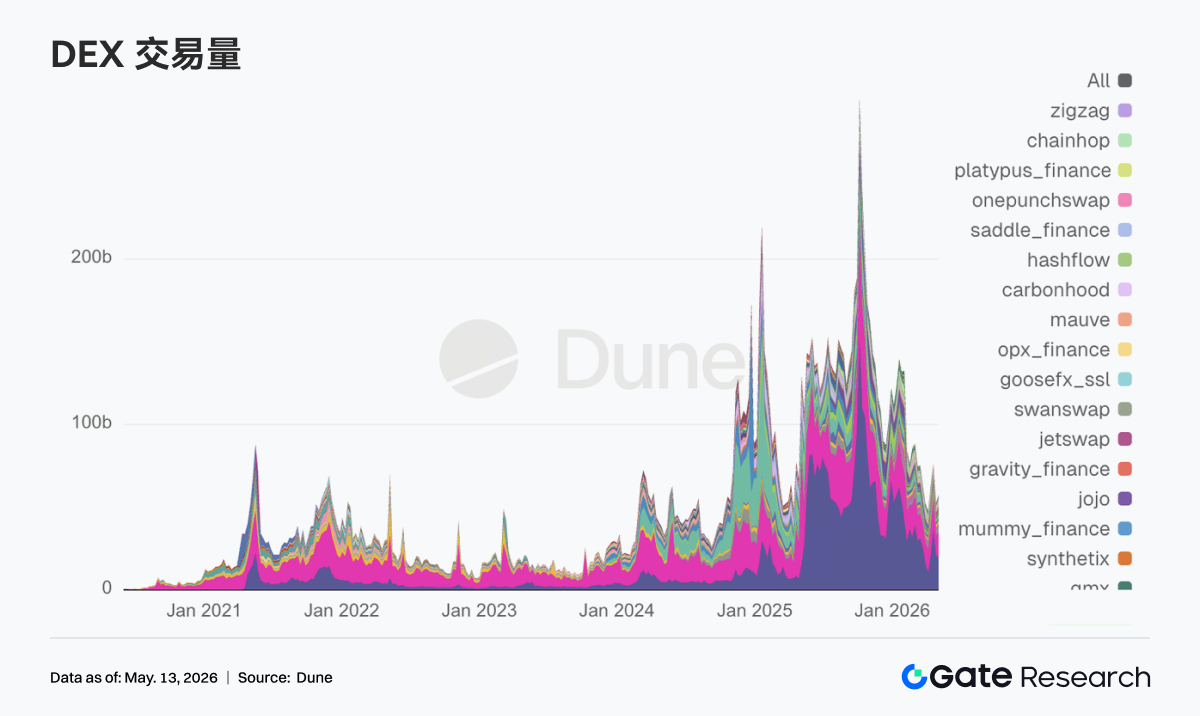

• TradFi Perp DEX: Over the past week, the trading structure of TradFi Perp DEXs remained absolutely dominated by commodities, maintaining a share of around 60% or more, indicating that macro assets like gold and crude oil continue to drive on-chain TradFi trading demand. Amid ongoing geopolitical risks and risk-off sentiment, capital is clearly favoring commodity assets with higher volatility and more direct narratives. Meanwhile, the market share of Indices/ETFs and Stocks sectors continued to recover steadily, reflecting some capital starting to re-engage with US stock index and ETF trading opportunities; FX, Bonds and other traditional macro assets continued to maintain a low share. Overall, the current trading preference of TradFi DEXs remains highly concentrated on the "macro trading" theme, and on-chain capital risk appetite has not yet significantly shifted towards low-volatility assets.

• TradFi Perp CEX: Over the past week, CEX TradFi perpetual contract trading volume remained high and volatile, with metals like gold continuing to hold absolute dominance. The precious metals sector still contributes the vast majority of transaction volume, reflecting the market's sustained strong participation in safe-haven and macro trading assets. Meanwhile, stock sector trading volume remained stable, indicating continued capital attention to US stock index and tech stock volatility opportunities. Commodities saw a periodic surge in volume driven by oil price fluctuations. Overall, the current CEX TradFi trading structure remains centered on gold-driven activity, with macro events and safe-haven demand continuing to dominate market risk appetite.

• Number of CEX TradFi Assets: Over the past week, the number of CEX TradFi asset categories expanded further. The total number of TradFi assets (excluding perpetual contracts) on three major CEXs increased from 956 to 1,107, a growth of 15.80% compared to the end of April. Among these, stocks saw the most significant growth, increasing from 594 to 748, a 25.90% increase from the end of April; Gate's stock TradFi assets increased by 104 compared to the end of April, a growth rate of 38.95%.

• TradFi Order Book Depth: We selected XAUT, which has the highest TradFi trading volume, and analyzed its order book depth (Delta). Over the past week, XAUT's depth structure exhibited a clear characteristic of "price increase, sell-side wall thickening." From May 4th to 5th, the order book Delta recorded positive values exceeding $1 million for several consecutive periods, indicating a significant increase in buy-side initiative, although the price still retreated to around $4,500 during the period, reflecting strong support at lower levels. Starting from May 6th, as the gold price rapidly surged above $4,700, the order book Delta turned persistently negative, with multiple instances of liquidity outflows exceeding $1.5 million per hour, indicating a significant increase in sell orders at higher levels, with some capital starting to actively take profits or hedge. Despite this, the overall price of XAUT remained high and volatile, suggesting that the market's demand for safe-haven gold allocation remains solid. The depth structure has now gradually shifted from the early stage of "active buying driving the rise" to a "battle between high-level selling pressure and capital absorption." In the short term, attention should be paid to whether the liquidity support around $4,650 can be maintained.

3. On-chain Data Insights

3.1 Capital Flows Back to Leading DEXs, Trading Focus Shifts Back to Deepest Liquidity Platforms

The first week of May on DEXs had a strong "return-to-home-court" characteristic. PancakeSwap topped the rankings, but incremental capital gave higher weight to trading venues with deeper liquidity like Uniswap and Aerodrome. The Solana side hasn't cooled off; Meteora and Raydium still show activity, and trading isn't just propped up by a single Meme narrative like previous weeks. With Bitcoin reclaiming key psychological levels, the overall risk appetite in the market was rekindled, and DEX volumes switched back to a more active state. It's worth noting that Grayscale removed Aerodrome and added Ethena in its quarterly DeFi fund rebalancing this week, while retaining Uniswap as its top weight. This indicates that institutional capital still prioritizes mature liquidity protocols before selecting new narrative directions.

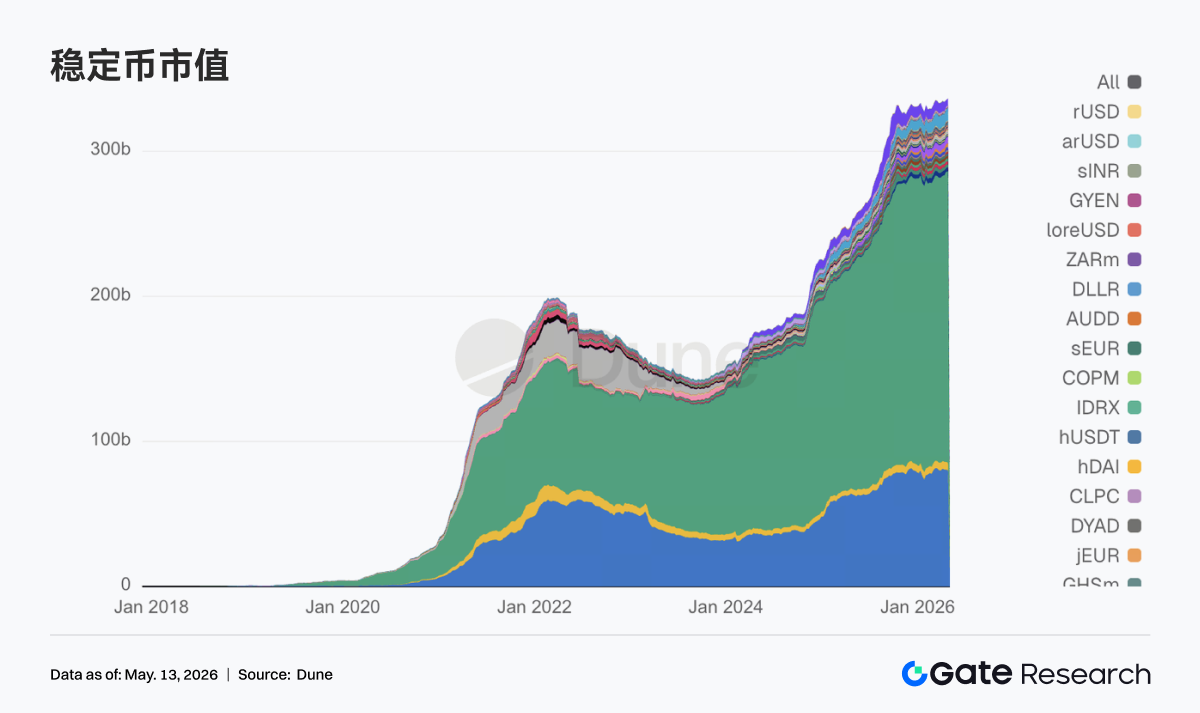

3.2 Market Attention Returns to Settlable, Compliant, Cross-Chain Stablecoin Assets

Besides the two top stablecoins USDT and USDC, payment-focused, compliant stablecoins capable of directly entering DeFi collateral and liquidation processes occupied more prominent positions this week, while the popularity of yield-oriented and more experimental varieties cooled down. This change aligns with the policy landscape. Reuters reported that the Senate reached a key compromise on stablecoin reward and yield terms, prompting the market to quickly reassess which stablecoins best fit the next regulatory framework. Notably, Circle was heavily involved in bridging reality, regulation, and ecosystem development this week. It obtained a MiCA license in France on May 4th, submitted comments on GENIUS rules the next day, and connected USDC and CCTP to Injective on May 7th, advancing along the main line of compliant distribution and cross-chain settlement.

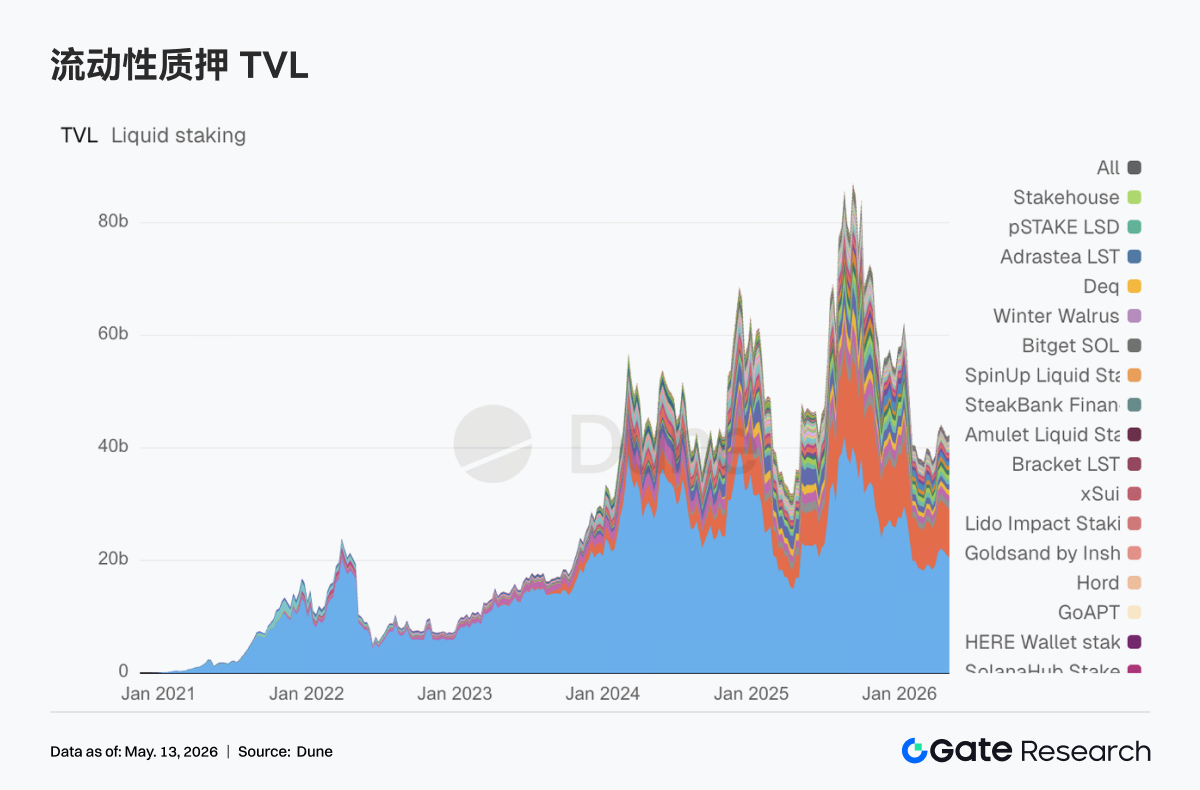

3.3 ETH LST Leaders Remain Stable, Solana Side First to Absorb Risk-On Shift

Leading protocols on the ETH side haven't yet shown a decisive strong recovery. Lido itself appears somewhat restrained, while Rocket Pool and StakeWise are relatively stable. In contrast, LSTs on the Solana side have been quicker to absorb the market's risk-on shift. Assets like Sanctum and Jupiter Staked SOL see more active absorption, with capital willing to reprice high-elasticity staking assets. Meanwhile, Lido obtained Web3SOC certification this week, continuing to advance along the main lines of institutional due diligence, governance transparency, and security frameworks, further strengthening its slow-variable advantage in institutional capital.

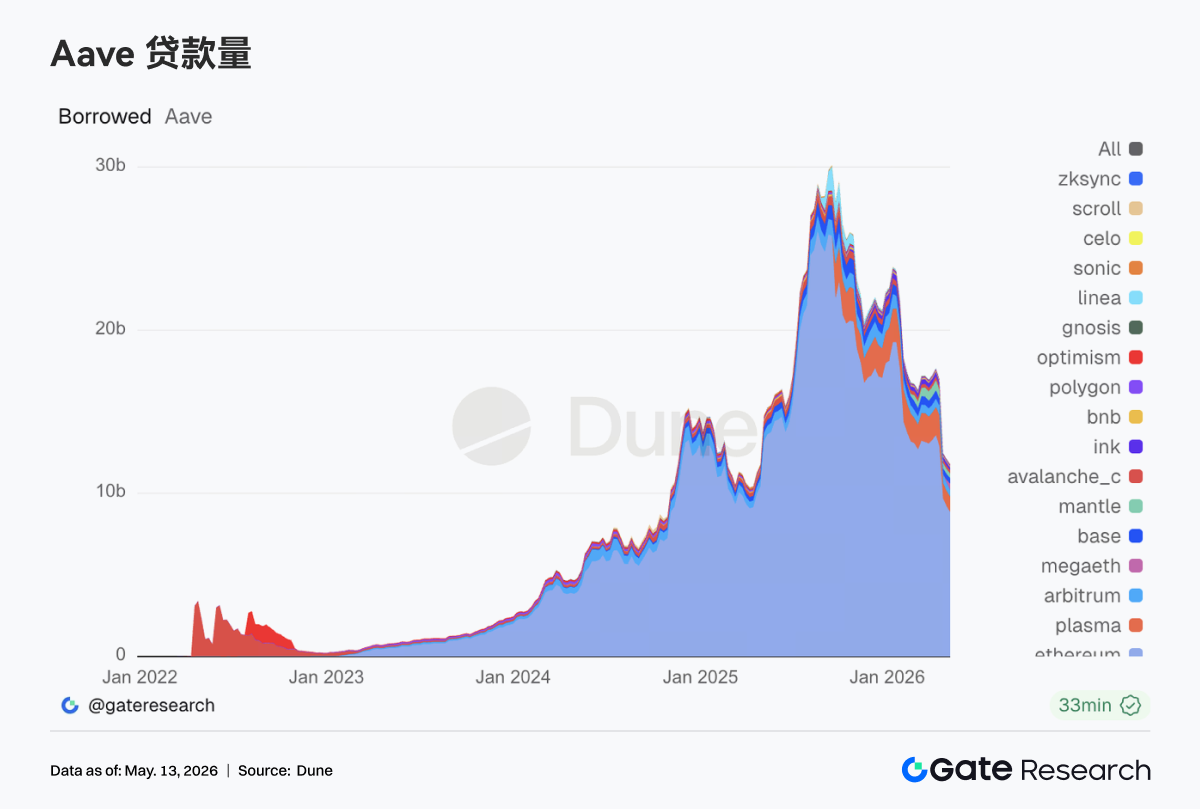

3.4 Aave Still Digesting rsETH Aftermath, MegaETH Absorbs New Lending Demand

Aave's lending data this week still bore strong signs of post-incident repair. The lending pool on the Ethereum main market contracted further, and older major markets like Arbitrum, Base, and Ink also remained weak. The multi-chain recovery seen a few weeks ago did not return. Conversely, Plasma continued to strengthen, and the lending pool on the new L1 MegaETH rose particularly noticeably, with capital moving from traditional main markets towards newer venues with more incentive space. Aave Labs stated directly in its early-May monthly update that the rsETH incident had disrupted the early growth rhythm of Aave V4. Subsequently, on May 5th, the Aave Labs risk team pushed forward increases in the supply caps for EURC on Ethereum and USDm on MegaETH. Aave is redirecting its new growth focus towards stablecoins with clearer regulatory attributes and lending markets on new chains that can more easily form closed loops.

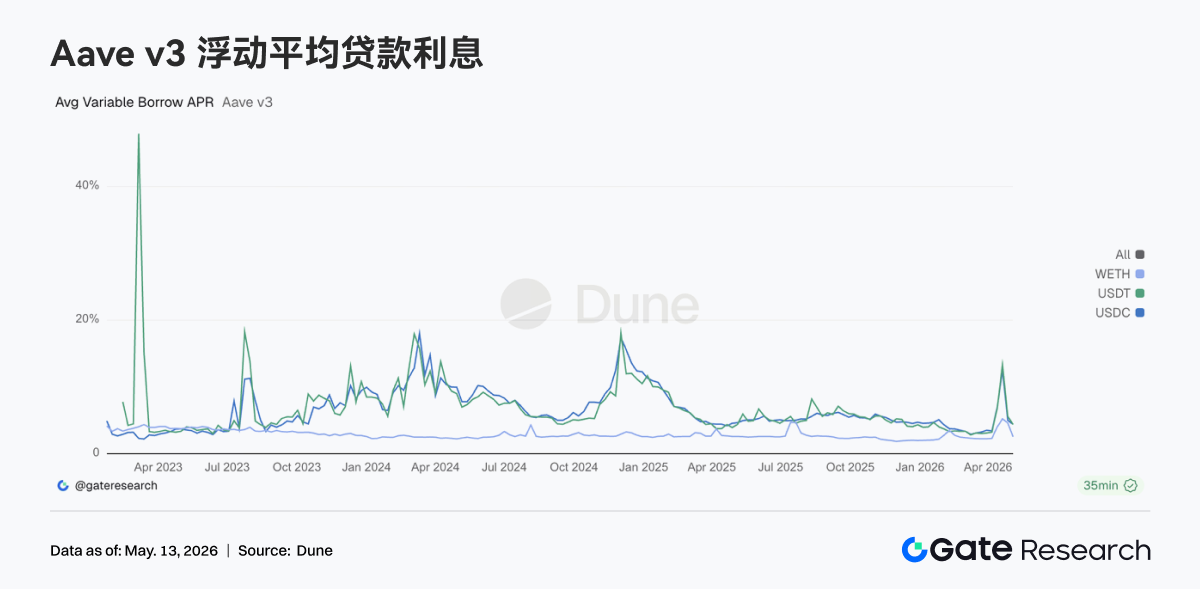

3.5 Aave Core Assets Retreat from Stress Levels, WETH Leverage Fades Most Significantly

Compared to the event-driven interest rate spikes of the previous two weeks, Aave's lending rates have noticeably cooled this week. Average borrowing costs for USDC and USDT have returned to normal ranges, while those for WETH dropped even faster. Looking at this alongside lending volumes, market demand has shifted from "scrambling for liquidity" back to "selectively borrowing liquidity." This explains why EURC and USDm were prioritized for supply cap increases – the demand for stablecoin loans persists, but it is now more focused on structured arbitrage, regional currency needs, and incentive-based trading on new chains.

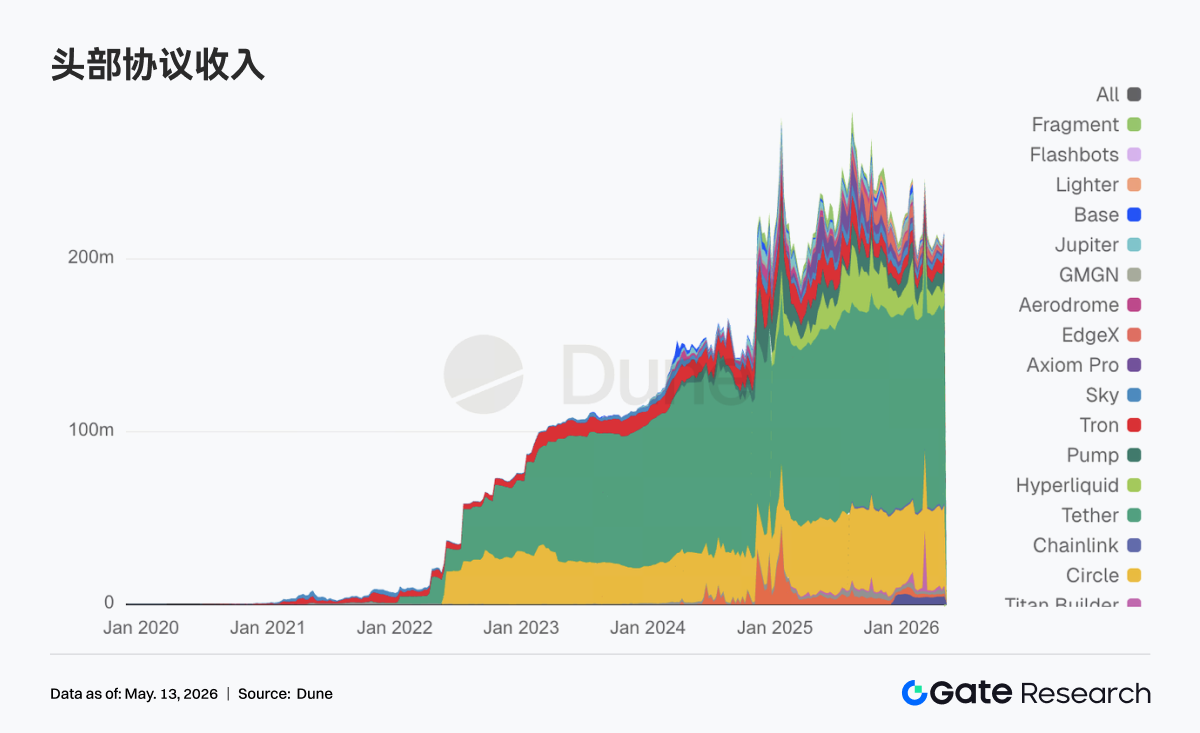

3.6 Protocol Revenue Returns to Structure of Stablecoin Base, with Derivatives and Lending Providing Elasticity

Tether and Circle's stablecoin issuance sides continue to contribute the most stable cash flow. This week, the elasticity mainly returned to on-chain derivatives and lending infrastructure. Hyperliquid saw high activity, and Aave's revenue elasticity was also significantly stronger than the previous week, with transaction and liquidation demand not dying down due to the late-April risk event. Hyperliquid started moving into Bitcoin outcome markets on May 5th. Combined with Hyperliquid Strategies disclosing an expansion of its HYPE reserve and advancing validator partnerships, the market is pricing this as a signal of evolution from a perpetuals exchange towards a complete financial stack. On the other side, Aave's revenue increase occurred simultaneously with a contraction in lending pools, reflecting the risk premium and capital repricing following the impact event.

4. Derivatives Tracking

4.1 BTC Funding Rate Deeply Negative with OI Rising, Short Squeeze Structure Continues to Strengthen

From May 4th to May 10th, the BTC price continued its upward trend and consolidated at high levels, moving from around 79K to above 82K. Although it dipped back to around 80K around May 7th, it subsequently recovered. Regarding funding rates, they remained in negative territory for most of the week, particularly around May 5th and 6th where they were deeply negative. This indicates that bearish sentiment hasn't completely faded during the price uptrend, creating a divergence where "price strengthens but funding rates remain negative."

Different from the previous phase, OI surged to over 29B on May 5th but quickly pulled back, subsequently consolidating in the 26B to 27B range. The combination of negative funding rates and the OI surge-and-retreat suggests that the previous crowded short structure experienced some relief during the price uptrend, with some leveraged positions exiting passively or actively. After May 7th, the BTC price maintained a high-level recovery, but OI failed to return to previous highs, indicating limited willingness for new leverage-driven chasing. The market is gradually transitioning from a phase of "shorts adding positions + price not declining" accumulation for a squeeze, to a state of "churning at high levels post-squeeze."

Overall, the current derivatives structure remains bullish-leaning, but the short-squeeze momentum has been partially absorbed compared to the period around May 5th. If the price continues to break above 82K in the future, accompanied by a rebound in OI, it could re-establish a resonance between leverage chasing and short covering. However, if the price consolidates at high levels while OI continues to decline, it would suggest that the upward momentum stems more from the closure of previous short positions, requiring subsequent spot buying or fresh long-leverage to take over.