八年行业复盘:加密最终走了另一条更有价值的路

- 核心观点:加密行业经过八年发展,未能实现去中心化颠覆传统金融的最初愿景,但通过稳定币和代币化浪潮,逐步与主流金融融合,构建起全新互联网金融基础设施,其实际价值远超预期。

- 关键要素:

- 经历ICO泡沫、DeFi之夏、NFT热潮和2022年系统性崩盘(如Terra、FTX暴雷),行业在投机周期中不断重建,重心转向金融基础设施。

- 稳定币(如USDC、USDT)成为核心用例,当前供应量超3000亿美元,2025年结算规模预计达100万亿美元,通过锚定美债契合美国国家战略利益。

- Memecoin无序繁荣后,特朗普当选推动监管友好化,《GENIUS法案》通过明确稳定币规则,华尔街开始布局资产代币化,如贝莱德CEO表态支持。

- 人工智能与加密技术融合,AI智能体将利用稳定币和钱包进行自主交易,推动无人商业实体诞生,加速行业主流化与后端基础设施替换。

Original Author: Connor Dempsey

Original Translation: Chopper, Foresight News

On Monday, I will start a new job. Before embarking on my fifth career chapter, I wanted to write this article to reflect on my eight-year journey through the crypto industry.

When I entered the crypto industry in 2017, I believed this technology would change everything.

Government-issued fiat currencies would be replaced by decentralized tokens; blockchains would eliminate all rent-seeking intermediaries in the transaction chain; power would shift from large corporations back to ordinary users.

Looking back now, almost none of those initial visions have materialized, but the industry has carved out an entirely different path.

I have worked at four crypto companies over eight years, witnessing the industry's scale grow from less than $1 billion to over $4 trillion, enduring multiple speculative bubbles, and experiencing one systemic collapse. I've gradually realized that what the industry is actually building is far more valuable than I initially imagined.

Before starting my next job, I want to document what I have seen and heard, along with my predictions for the industry's future direction.

The Illusory Gold Rush: The 2017–2018 ICO Mania

In early 2017, I stumbled upon an introduction to Bitcoin in a book and was completely hooked. Soon after, I devoured every Bitcoin book I could find and got the idea to move to Singapore to write a blog and delve deeper into this new technology.

At the time, I didn't realize we were in the tail end of the ICO (Initial Coin Offering) super-speculative bubble. ICOs allowed anyone to raise funds globally by selling cryptocurrency to investors, crowdfunding capital for creative projects.

And Ethereum was the star of this show.

In November 2017, I published a beginner-friendly guide to Ethereum that went viral on Reddit. It happened to coincide with the peak of the bubble; just a month later, the market bubble burst completely.

Reading that article now feels more like a time capsule: it captured the widespread optimism of the era and also predicted a future that ultimately never came true.

My main argument was that blockchain networks like Ethereum could be used to build new consumer-facing applications.

Traditional internet platforms (Facebook, Uber, etc.) primarily funnel value to large corporations and a few investors; the value generated by blockchain applications could be shared between early participants and ICO investors.

The article also imagined building a decentralized Uber. In this system, early users and drivers would receive tokens for each completed ride, gaining ownership of the network and ensuring fairer value distribution for early builders.

The vision looked good on paper, but this decentralized revolution ultimately failed completely.

It was a crypto speculation party replicating the 2001 dot-com bubble.

Ethereum became the most powerful fundraising platform in history, with over 3,000 ICO projects raising a combined $22 billion globally.

But, just like the dot-com bubble, the underlying technology wasn't mature enough to support the sky-high valuations the market was giving.

More critically, ICOs completely distorted the incentive structure between entrepreneurs and investors. Projects could raise tens of millions of dollars overnight based on just an idea; investors were left holding tokens, hoping the project would materialize and appreciate. Meanwhile, founding teams held large amounts of native tokens they could cash out immediately upon listing, destroying any motivation to diligently build a product.

During the bull market, founders and early investors made a killing; during the bear market, ordinary retail investors were left holding the bag. Despite some builders with good intentions, ICOs ultimately became a breeding ground for greed, hype, and fraud.

Throughout centuries of financial history, every speculative bubble has followed this pattern.

Rebuilding from the Rubble: The Circle Years of 2018–2019

As the market soured, leveraging the small reputation I had built on Reddit, I joined Circle in early 2018 for an entry-level marketing role.

Circle had been around for four years then, with several consumer-facing products (investing, payments, exchange) that weren't profitable. However, its over-the-counter trading desk was quietly generating steady revenue, propping up the entire company.

Over the next two years, the industry wallowed in the post-ICO bust. Most ICO projects were abandoned or defunct, countless tokens went to zero, and industry sentiment hit rock bottom.

But it was precisely during this dark period that the seeds for the industry's next revival were planted.

The industry's focus shifted away from consumer applications and towards rebuilding the traditional financial system on the internet.

Stablecoins pegged to the US dollar, initially created to facilitate traders moving in and out of crypto positions, maintained their $1 peg by holding a 1:1 reserve of dollars and Treasuries.

Tether’s USDT rose rapidly during the ICO craze, with its dollar reserves largely held in bank accounts outside the US. Stablecoins were initially used for trading but quickly found another user base: people without access to the traditional banking system who wanted to hold US dollar assets.

This included citizens trying to bypass capital controls, wealthy Chinese individuals diversifying assets offshore, and people in countries like Argentina and Turkey suffering from high inflation.

In 2018, Circle partnered with Coinbase to launch the regulated USDC dollar stablecoin. Its early use case was still primarily trading, but people began imagining this internet-native currency allowing anyone with an internet connection to access US dollar assets 24/7, without barriers.

Meanwhile, the surviving quality projects from the ICO era were mostly focused on finance. Ethereum was not just for fundraising but could rebuild the underlying infrastructure of financial markets: Uniswap in trading, Aave and Compound in lending – together forming the decentralized finance (DeFi) ecosystem.

Stablecoins and DeFi became deeply intertwined, and a once-in-a-century global pandemic would propel them to their peak.

Back to the Wild West of the Internet: The Messari Era 2019–2021

In late 2019, I joined the 13-person data research startup Messari as its first full-time marketing hire.

The company had just 4 analysts focused on cutting-edge DeFi research; the total market cap of DeFi at the time was only $665 million.

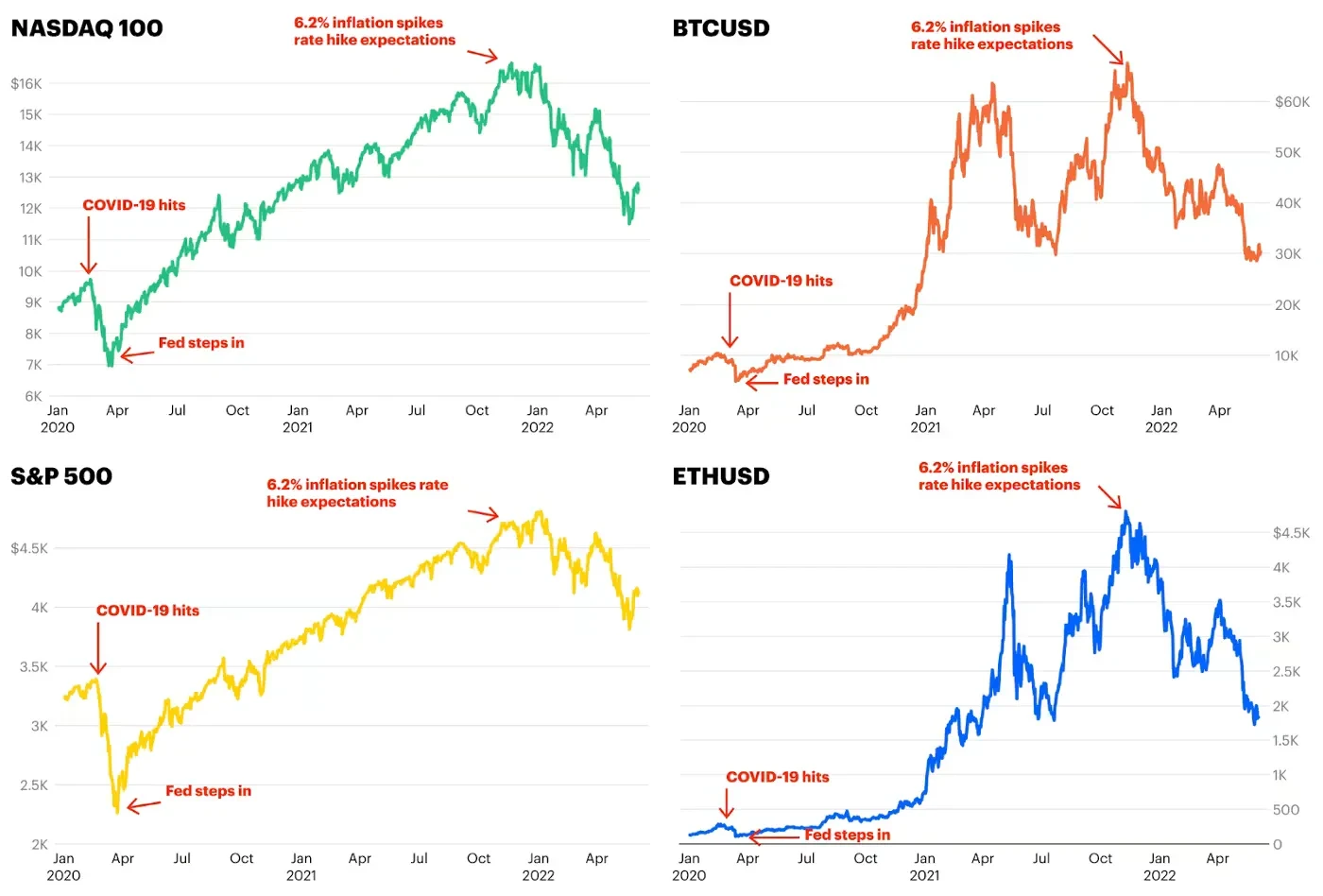

In early 2020, the COVID-19 pandemic hit, the global economy ground to a halt, and all asset classes crashed.

To prevent economic collapse, central banks worldwide began massive money printing, with a staggering $9 trillion injected in 2020 alone.

This flood of capital needed a place to go. Combined with nationwide lockdowns, a huge amount of hot money flowed into Bitcoin, Ethereum, DeFi, and various speculative assets.

Bitcoin soared from under $4,000 to nearly $70,000, surpassing a trillion dollars in market cap with institutional backing and outperforming macro assets like gold.

The loose monetary environment also gave birth to the famous "DeFi Summer," where the market cap of DeFi protocols exploded 250-fold to $180 billion.

While DeFi was expected to reconstruct traditional finance, DeFi Summer felt more like a massive online game dominated by profit-seeking traders, with tens of billions of real dollars at play.

The core mechanic of the game was yield farming. Anonymous developers launched new protocols one after another, with project names oddly clustered around food themes: YAM Finance, Spaghetti Money, SushiSwap. Traders could deposit mainstream tokens like ETH, USDC, USDT to claim newly issued tokens like YAM, SPAGHETTI, SUSHI.

The scene was absurd and crazy: newly launched food-themed tokens could reach a market cap of over a billion dollars in days. Early players cashed out at the top, and the tokens then crashed precipitously.

This was the true Wild West of the internet.

Like the ICO mania before it, DeFi Summer created a new class of crypto millionaires but eventually succumbed to the bursting of its own bubble. This wave also launched a new crypto billionaire, Sam Bankman-Fried, who would later become the central figure in the industry's next major catastrophe.

At the Peak of the Bubble: The Coinbase Period 2021

Shortly after Coinbase went public with a $100 billion market cap in April 2021, I was invited to join the company's Corporate Development and Venture Capital team.

My work involved M&A, evaluating early-stage crypto venture investments, writing industry trend analyses, and contributing to Coinbase's short-lived podcast. It remains one of the best teams I have ever been a part of.

It was also during this period that another speculative bubble quietly formed: the NFT craze, centered around digital artworks.

If DeFi was the arena for professional traders, NFTs broke through to the mainstream. It offered artists a new way to monetize online and laid the groundwork for establishing digital property rights on the internet.

But, just like ICOs and DeFi Summer, NFT speculation quickly spiraled out of control. Digital collectibles like cartoon apes, punks, and penguins sold for single-unit prices of $1 million; artist Beeple's collage fetched an absurd $69 million at Christie's.

Crypto concepts completely took over the mainstream: Larry David mocked crypto skeptics in a Super Bowl ad; Sam Bankman-Fried's exchange FTX paid $135 million for the naming rights to the Miami Heat's arena. Everyone seemed to be getting rich from tokens, NFTs, or concept stocks.

The madness of 2017 was back, but amplified fourfold by unprecedented monetary stimulus.

The Reckoning: The Great Industry Collapse of 2022

But soon, the party ended, and the industry began to crumble.

The same easy money – rate cuts, quantitative easing, fiscal stimulus – that had inflated all asset prices eventually led to consumer inflation. By late 2021, Bitcoin, Ethereum, the NASDAQ, and the S&P 500 all peaked simultaneously; with inflation out of control, central banks were forced to tighten the very policies that had driven stocks and crypto to all-time highs.

As the interest rate hiking cycle began and fiscal stimulus was withdrawn, investors started re-evaluating their high-valuation assets: Was that cartoon ape really worth $1 million? Why did a sushi-themed token have a $3 billion market cap? Could Dogecoin truly support a $90 billion valuation?

As pessimism spread, a chain of defaults within the industry began.

If the ICO bust was akin to the 2001 dot-com crash, the 2022 crash felt more like the 2008 global financial crisis: a few toxic assets combined with high leverage nearly brought down the entire industry.

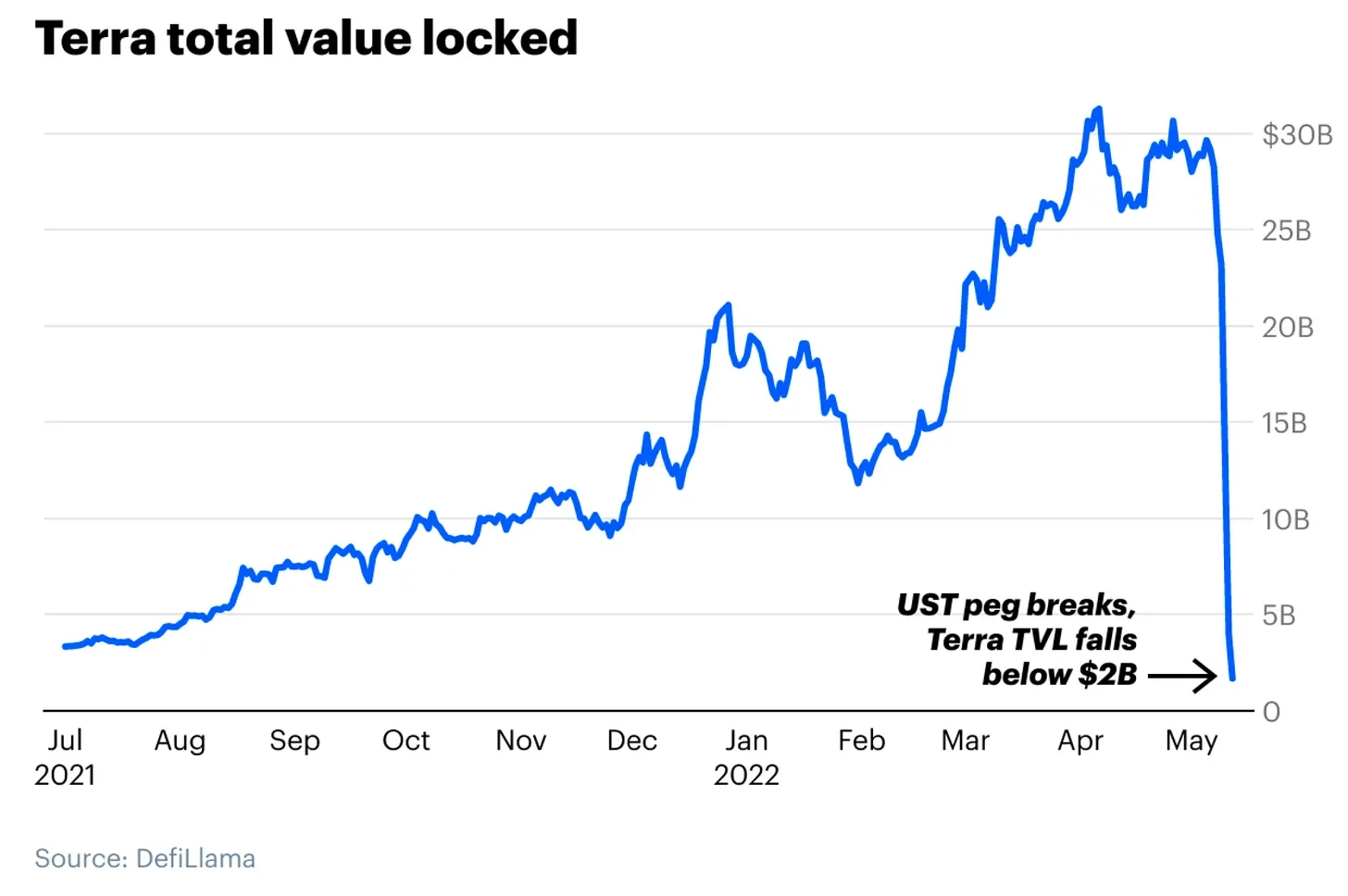

The first domino to fall was Terra's algorithmic stablecoin, UST.

Unlike USDC or USDT, which were backed 1:1 by cash and Treasuries, UST relied on a complex algorithmic mechanism to maintain its $1 peg. This mechanism worked during stable market conditions but completely failed when a selling panic hit.

Within days, $32 billion in market value evaporated, and countless holders saw their assets become worthless.

Next came the collapse of Three Arrows Capital, a $10 billion hedge fund that was heavily long on Terra and leveraged to the hilt. Three Arrows Capital had borrowed heavily from crypto lending platforms like Celsius and Voyager, which had in turn used user crypto deposits to chase seemingly safe 8% annual yields. When Three Arrows Capital imploded, these lending platforms froze withdrawals and filed for bankruptcy, leaving ordinary user deposits worthless.

During my time at Coinbase, we watched FTX and Sam Bankman-Fried step in to rescue several distressed crypto lenders like BlockFi. He was hailed as "JP Morgan of crypto," the industry's white knight.

But the truth eventually surfaced: SBF and FTX were the biggest risks of all.

Remember FTX's massive naming rights deal? That expense, and indeed SBF's entire business empire, was propped up by its own exchange token, FTT, which was issued out of thin air. SBF borrowed heavily using FTT as collateral. When FTT's price collapsed, the loans were margin called, and FTX declared bankruptcy.

Worse still, FTX had been improperly using customer funds to make investments and plug financial holes. This once $32 billion giant imploded within a week, with $8 billion in customer deposits vanishing.

SBF violated the golden rule of exchange operation: never touch user assets.

This was crypto's "Lehman Moment."

Gambling and Casinos: The Memecoin Mania 2023–2025

After the FTX collapse, SBF was sent to prison. Within 12 months, the crypto market cap shrank from $3 trillion to less than $1 trillion.

Then, the Biden administration began a full-scale crackdown on the US crypto industry.

SEC Chair Gary Gensler sued most compliant US-based crypto companies for securities violations. Coinbase, Kraken, Uniswap, Robinhood – all received enforcement notices. The very companies that had spent years navigating regulations became the SEC's primary targets.

Simultaneously, Senator Elizabeth Warren pressured traditional banks to cut ties with crypto clients, isolating the industry from the banking system and driving many teams overseas.

This regulatory approach had several unintended consequences.

First, any crypto project with a real business model (like various DeFi protocols) was deemed a potential unregistered security, facing constant litigation risk. The legally safest option became the Memecoin – a token with no utility, no clear vision, just narrative.

Platforms like Pump.fun launched millions of Memecoins. Celebrities like Iggy Azalea, Caitlyn Jenner, and the Hawk Tuah girl launched their own, each eventually descending into farce.

The crypto industry once again became a massive casino, bigger than ever before. Over 6 million Memecoins were launched, and the sector's market cap hit a peak of $150 billion in late 2024, even surpassing the scale of the NFT bubble.

Towards Institutionalization: The Crossmint Era 2025–2026

Putting aside this industry circus, the crypto community's bet on Donald Trump's election paid off.

As Trump's victory seemed likely, Bitcoin hit new all-time highs. The market's logic was clear: a shift from hostile to friendly regulation from the world's largest economy. Gary Gensler resigned. The new SEC dropped lawsuits against US crypto companies. Traditional banks reopened relationships with crypto businesses.

Most importantly, the GENIUS Act was passed in July 2025, the first comprehensive federal crypto legislation in the US, establishing clear regulatory rules for stablecoins.

Washington sent a strong signal to Wall Street: crypto, especially stablecoins, was about to become a major business sector. Stablecoin companies like Bridge and BVNK were acquired by Stripe and Mastercard for over $1 billion valuations. Rain raised nearly $2 billion in Series C funding. My old company, Circle, the issuer of USDC, went public, reaching a peak valuation of $60 billion in June 2025.

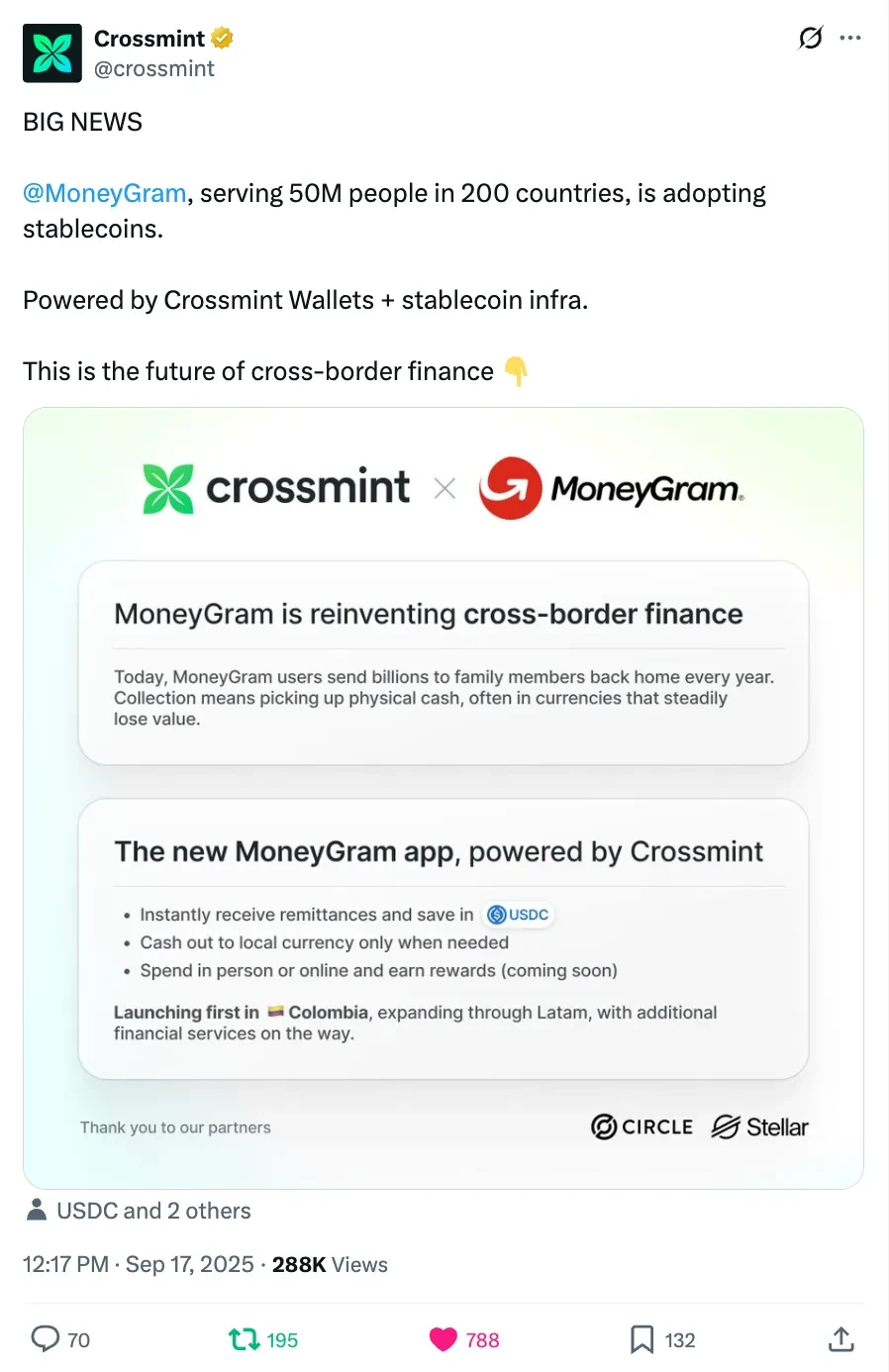

At the time, I was Head of Marketing at Crossmint. The company partnered with MoneyGram, helping this century-old cross-border remittance giant leverage stablecoins for global money movement.

As the value of dollar tokenization became clear, Wall Street began seriously considering the on-chain tokenization of other assets. Even Larry Fink, CEO of BlackRock, who once called Bitcoin an "index of money laundering," changed his tune, stating that tokenization is the next generation of financial markets, and that all asset classes – stocks, bonds, real estate – will eventually come onto the blockchain.

An Unforeseen Revolution: The State of the Industry Today

Eight years after my Reddit beginner's guide, we still don't have a decentralized Uber.

Blockchains haven't eliminated all intermediaries, and decentralized tokens haven't replaced