从ETH期货数据窥探市场对Merge的预期

原文作者:Kaiko 分析师 Conor Ryder

译者:Odaily 星球日报 Azuma

期货市场是机构、对冲者和投机者们的战场。

在 2021 年的牛市中,随着新资金以过高的杠杆涌入市场,期货市场成为了那轮牛市冲击新高的主要催化剂之一,时间快进至 2022 年 9 月,我们又看到了这些新资金比以往任何时候都更“凶猛”地回到期货市场,特别是 ETH 市场 —— 在万众瞩目的 Merge 之前,ETH 的未平仓合约量已打破了历史高点。

在这篇文章中,我将分析 Merge 前期货市场的头寸性质,并窥探这对 ETH 的短期和长期价格分别意味着什么,我还将从数据层面出发,以探析现在究竟是现货市场还是期货市场主导着 ETH 的价格变化。

全场焦点 —— ETH

随着以太坊历史上最重要的时刻之一的来临,ETH 投资者的焦虑和兴奋是可以理解的。

对于即将到来的 Merge,怀疑论者将其比作“在飞行途中更换飞机的引擎”,支持者们则欢呼这一升级将为以太坊的大规模采用带来质的改进。这种观念上的分歧为 ETH 期货市场的交易量增长铺平了道路,因为争论的双方都希望在 Merge 之前相应地调整自己的头寸。

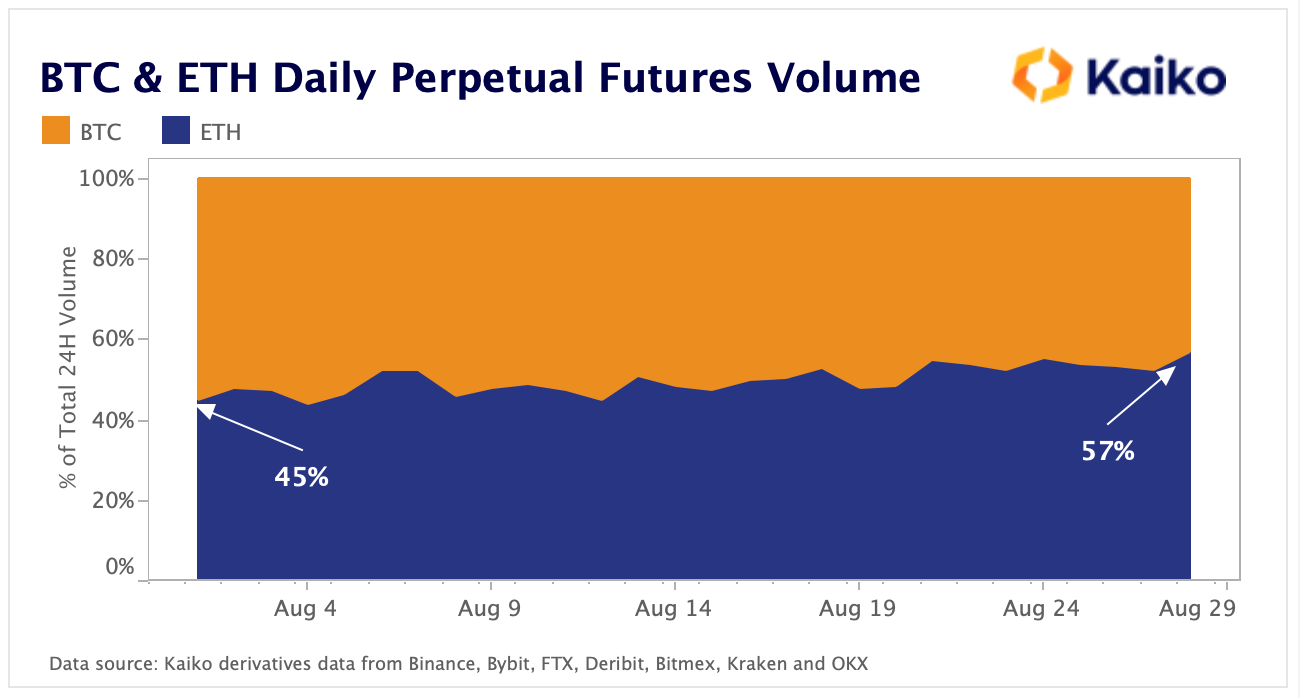

我们已经从 BTC 和 ETH 的期货交易量对比中看到了这一趋势,随着 Merge 的到来,ETH 在八月初控制了 45% 的期货市场交易量,月底这一数据已增长至 57%。

资金涌入ing

前文中我曾提到,随着 Merge 的临近,新资金进入期货市场的势头比以往任何时候都要“凶猛”。

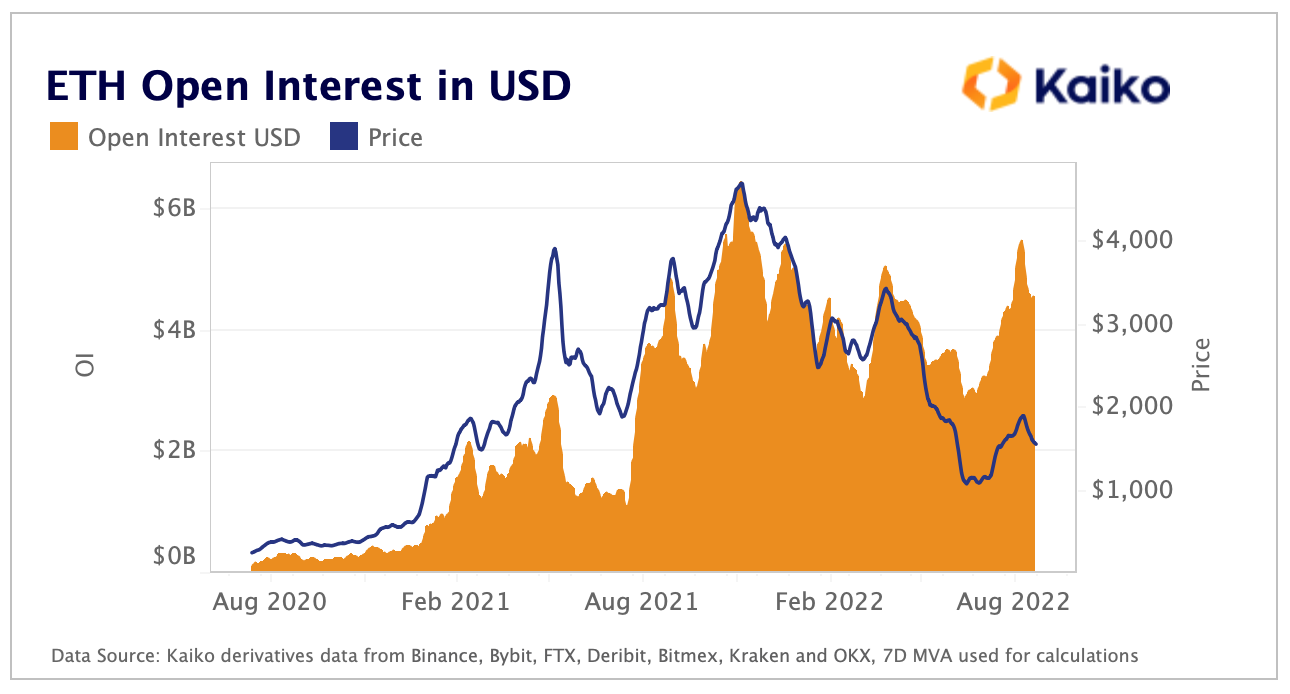

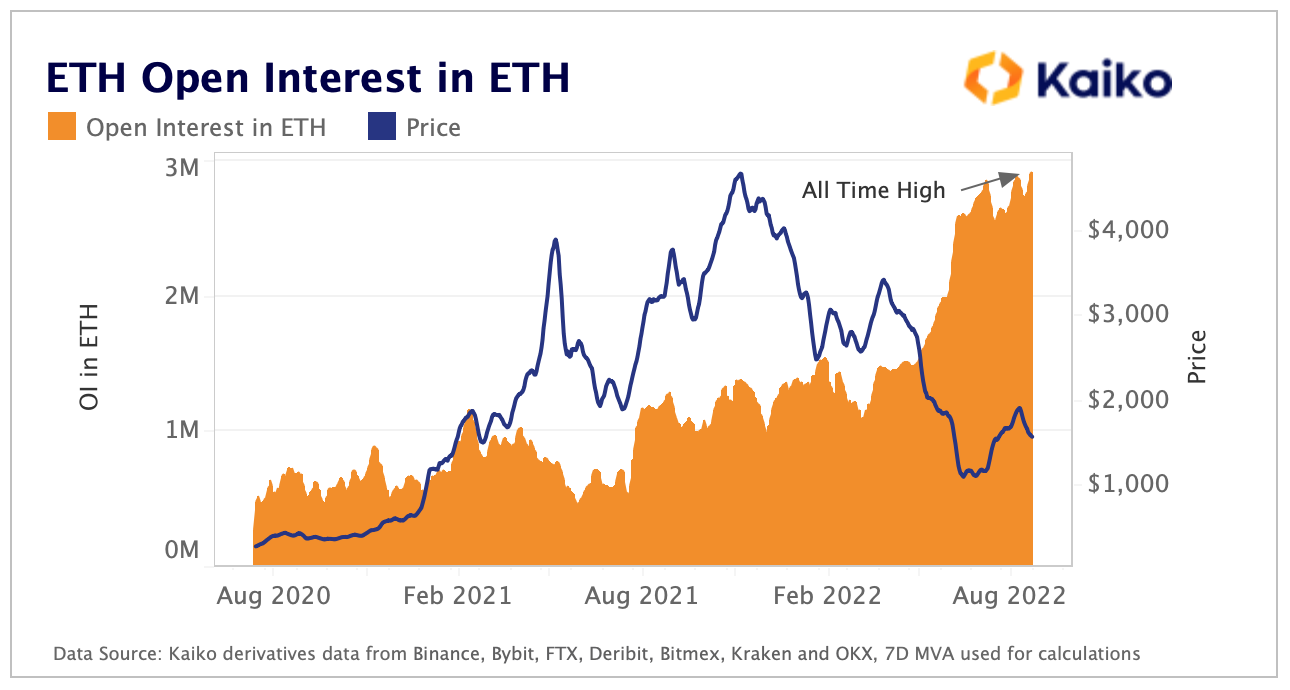

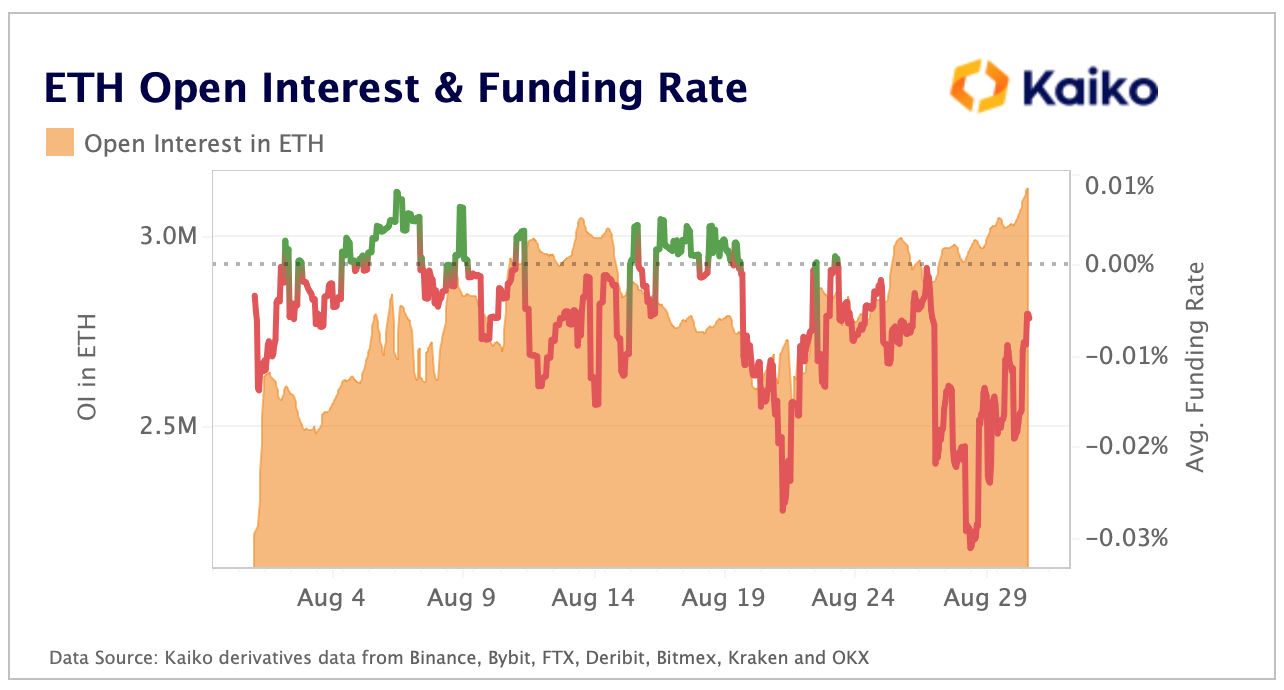

未平仓量是衡量当前有多少期货头寸尚未平仓的数据,代表着当前投资于该期货的资金数额。这里我想强调的是,关注未平仓量需要以标的资产本身为单位进行观察,即需要关注以 ETH 计价的未平仓头寸。因为当你关注以美元计价的数据时,实际上你已经考虑到了价格影响。

如下图所示,以美元计价的未平仓量会密切跟踪价格,这通常很难显示期货市场上的资本流动情况。

反之,如果我们选择以 ETH 计价,数据显示此时未平仓的期货头寸数量已达到了惊人的历史新高,这将对 ETH 未来几周的价格走势造成巨大影响。

资金费率

资金费率的存在可以帮助期货价格更接近它们所追踪的标的资产。如果多头期货的需求增加,资金费率将为正值,这时持有做多头寸的投资者需要向持有做空头寸的投资者支付一定费用,以激励头寸之间的平衡。

通常情况下,由于市场情绪往往都是不平衡的,所以资金费率往往也会持续偏向某一方,无论是正值还是负值,自 2021 年的牛市以来,由于悲观情绪的持续,资金费率一直都在中性以下徘徊。

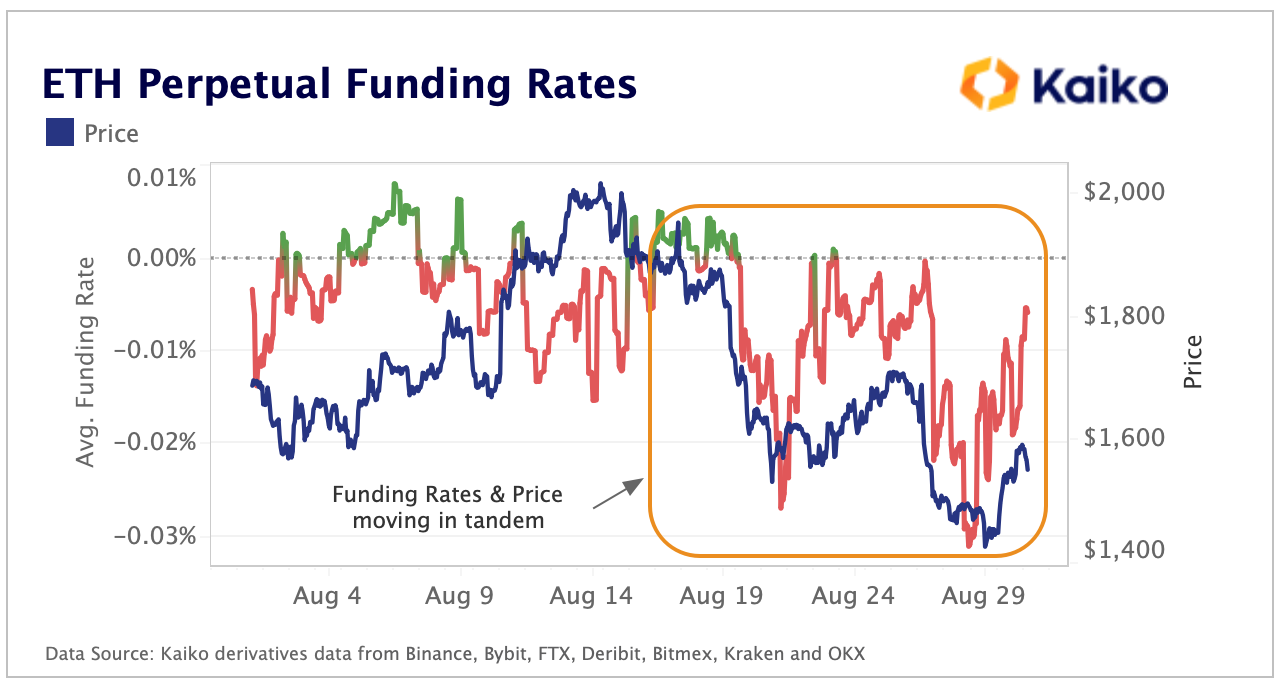

有趣的是,随着 Merge 的临近,我们看到 ETH 期货市场的资金费率已大幅下降,以负值结束了 8 月。这种负增长,与未平仓量的增长相吻合,使得我们得出了结论 —— 涌入 ETH 期货市场的大部分新资金都有做空倾向。

关于投资者选择开空的理由有很多:

第一个原因是单纯地看空 ETH,押注于 Merge 的失败或延迟。基于此前 Merge 日期已被推迟了数次的事实,这一押注并不难理解,但随着时间的推移,Merge 成功的可能性已变得越来越大,特别是在所有测试网都已顺利过渡之后。我很难相信,在这种级别的升级事件发生之前,会有投资者选择直接做空 ETH。

第二个原因(在我看来更有可能)是投资者在 Merge 之前对冲其长期持有的 ETH 多头头寸,这可以帮助投资者在事件发生前规避一些风险。另一个潜在的策略是利用期货市场套利,通过买入 ETH 现货并做空 ETH 期货,投资者即可规避价格波动上的风险,还可有机会获得潜在的分叉链代币空投。

如果 Merge 成功,且 PoW 链没能“起飞”,我们应该会看到大量的 ETH 空头头寸被平仓。这对相应资产的价格应该是利好消息,尤其是当一项资产的交易量主要集中在期货市场时(我们稍后会聊到这些)。如果将这些待平仓的空头头寸与每日数千万美元的矿工抛压结合起来,由于两股巨大的抛售力量有望同时被解除,你可能会对 ETH 的前景相当乐观。

如下面所示,负值资金费率的加剧发生在 ETH 自 2000 美元下跌的同一时间,且其变化也与价格的波动同步。如果这些空头在 Merge 后被平仓,ETH 的资金费率可能会走向正值,这肯定会有助于价格情绪。

现货 or 期货,谁在主导 ETH 的价格?

前文中,我们看到了负值资金费率和未平仓头村的增加,与此同时 ETH 从本月的高点下跌了 30% 以上。这就引出了一个问题,期货市场对加密货币的价格究竟有多大影响?这是一个价格发现的问题,实际上可以归结为现在哪个市场在主导价格发现,现货还是期货?

解答该问题的一种方法在于观察交易量——成交量通常与价格波动相关,如果在某一时期内期货市场的成交量增幅大于现货市场,我们可能会判断该时期内期货市场正在引领价格发现。

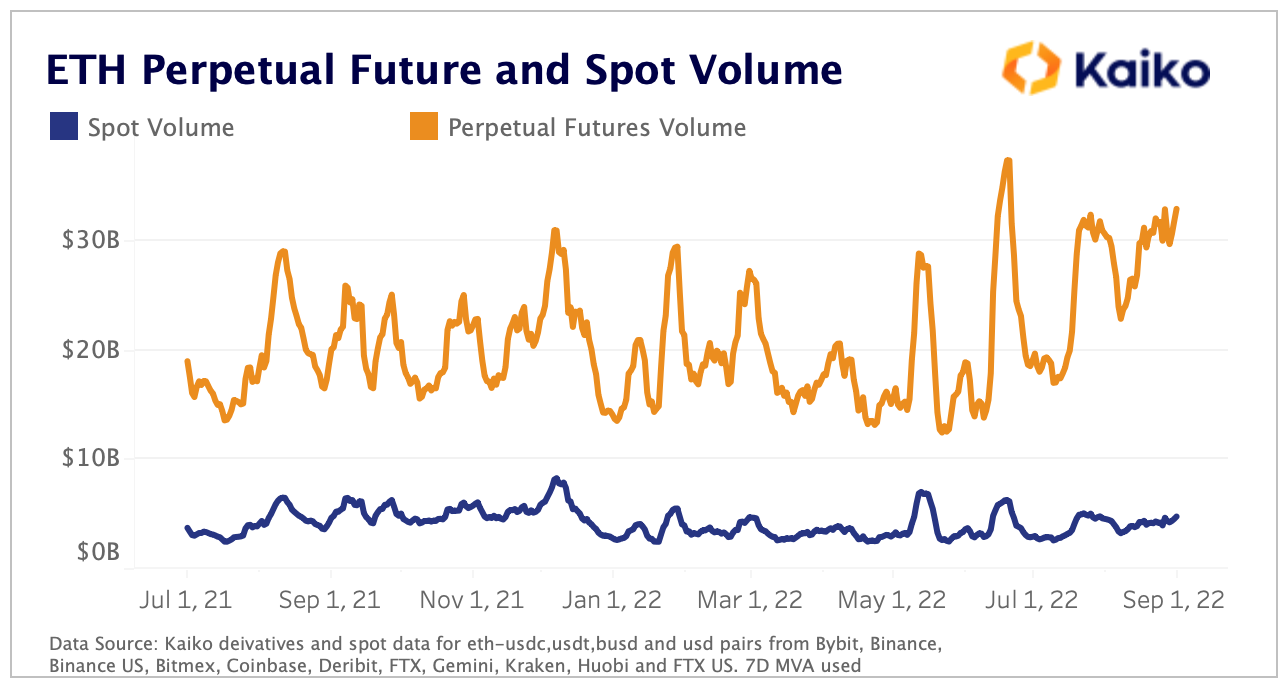

自去年以来,ETH 期货市场的日交易量已从 190 亿美元大幅增长到超过 330 亿美元,与此同时现货的日交易量也从 37 亿美元升至 48 亿美元。

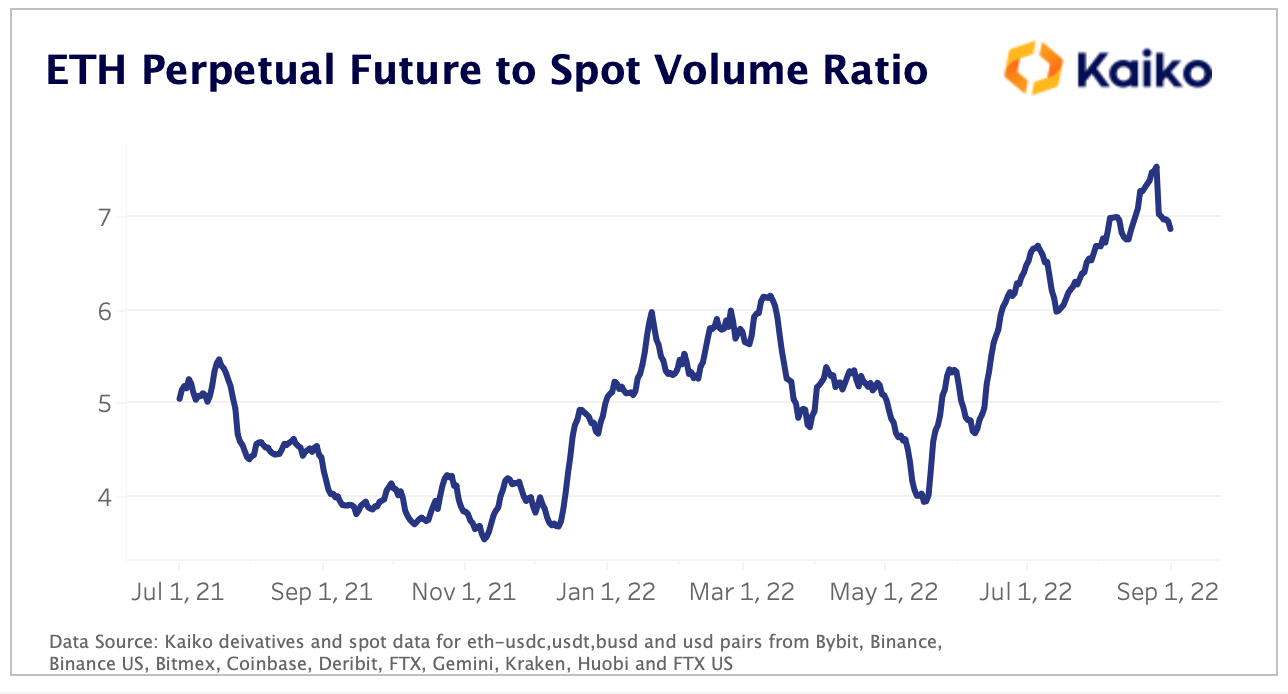

将这些交易量分解成一个比率来评估彼此之间的变化情况,我们可以看到 ETH 期货交易量的主导地位正在上升,因为期货与现货交易量的比率已从 5 倍增加到了大约 7 倍。

相对于现货市场,期货的交易量越来越大,它们开始对围绕 ETH 的情绪产生巨大影响。去年 11 月,当市场处于历史高点时,期货的交易量仅为现货市场的 4 倍,现在这一数据则为 7 倍,未平仓量也处于历史高位,似乎投资者和机构们正在转向通过期货来押注 ETH —— 正如我们在过去一个月看到的,倾向上会偏向于空头。

期权

我们在 ETH 的期货市场上看到的趋势,也反映在了期权市场上。

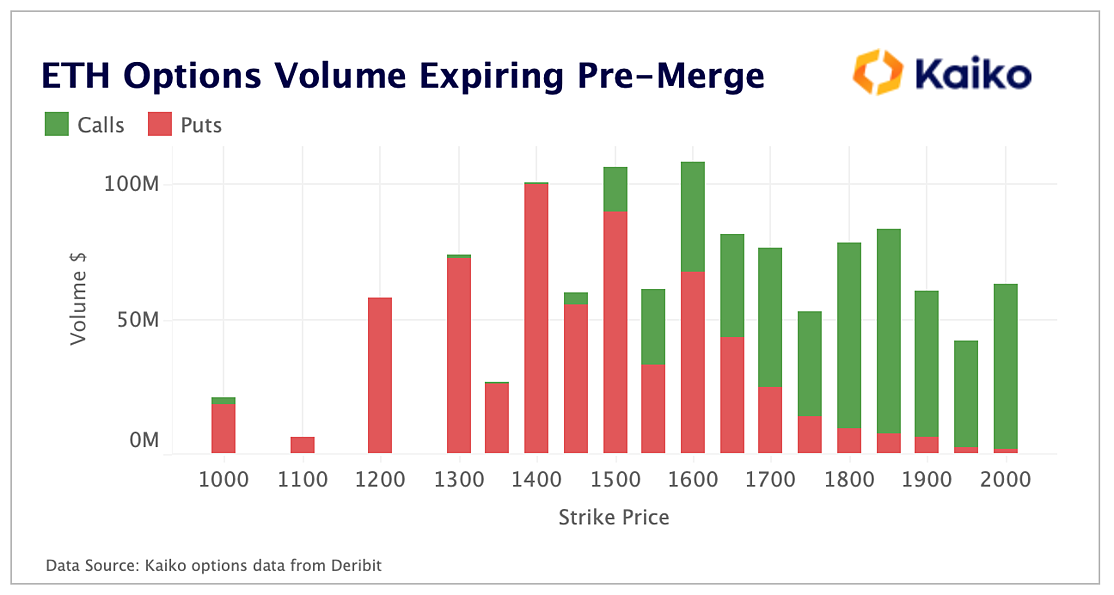

看跌期权的买家希望(将其收益)锁定在一个可止损的价格水平。当查看 Merge 前到期的 ETH 期权交易量时,我们可以很明显地看到在 1000 美元 - 2000 美元的价格区间内,交易量最高的三个点位分别是 1600、1500 和 1400,其中后两个点位几乎完全由看跌期权构成。

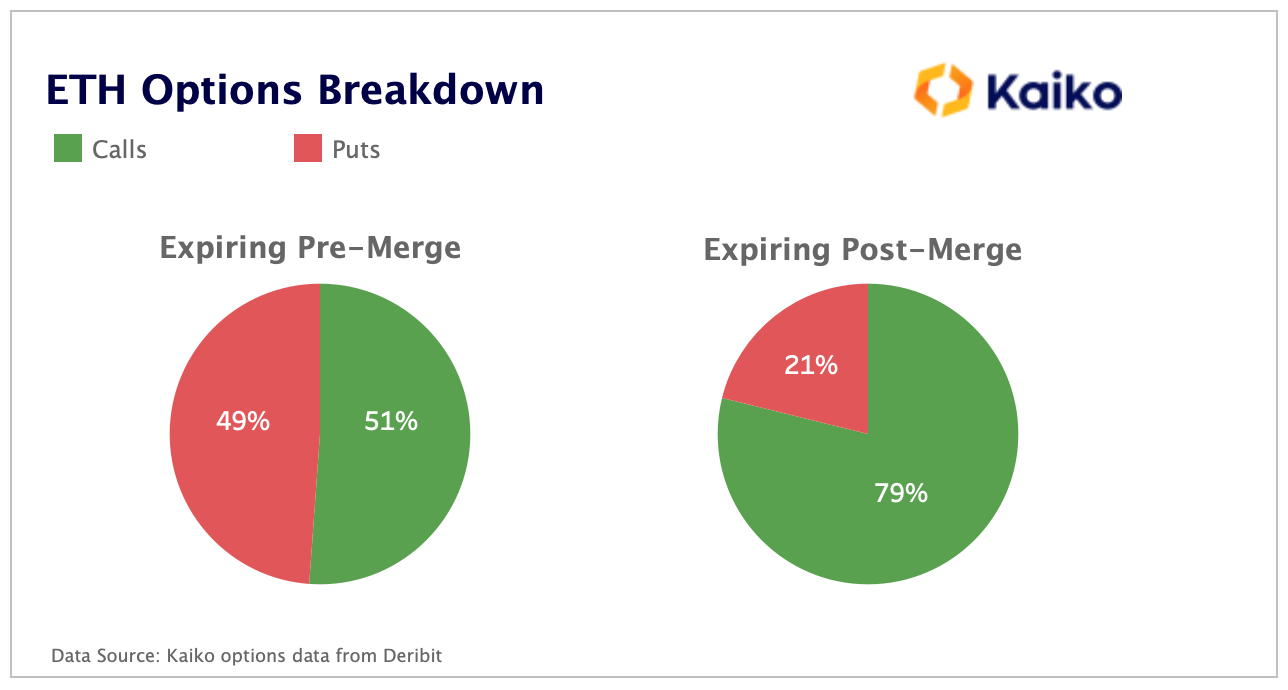

当人们联想到加密市场上的期权交易时,往往会想到投机性的多头头寸,但 Merge 前的期权市场可能是一个非常典型的风险对冲案例。对于 Merge 前到期的期权,看跌/看涨的交易量比例几乎达到了“五五开”的局面,这在加密货币的期权市场中是极为罕见的。然而,在合并之后,由于投机行为继续占领主导地位,押注看涨期权的比例再次恢复到73%。

ETH 的期权市场或许是观察 Merge 前两周投资者情绪最好的地方。简单地说,这就是在为 Merge 时的非预期事件做准备,并对冲相关风险。而如果观察 Merge 后的情况,我们会发现投资者似乎不太愿意做空,因为随着上述抛售压力的消除,短期内正面价格走势的可能性相当高。

结论

与现货市场相比,期货市场的主导地位正日益上升,衍生品目前正在对加密资产的价格走势产生巨大影响。

ETH 是最典型的例子,它将在几周内迎来一场重大且存在不确定性的大升级,期货市场正是为这样的高波动性事件量身定制的。正如期权市场所证明的那样,投资者似乎看好以太坊的长期未来,但在短期内仍然会潜在的非预期时间。

无论如何,这次 Merge 是最近加密货币领域唯一的一个非宏观因素驱动的事件,如果它能够在降低加密货币与股市相关性方面带来了突破,这将是一件非常有趣的事情。