芯片주 '검은 화요일': 기술적 조정인가, 아니면 강세장의 전환점인가?

- 핵심 견해: 2025년 6월 23일 글로벌 칩주 폭락은 한국의 '소문'에 의해 단독으로 촉발된 것이 아니라, AI 부문 거래의 극심한 과밀 현상과 레버리지 취약성 하에서 필연적으로 발생한 청산 과정이다; 골드만삭스 등 기관들은 AI 서사는 변하지 않았으며 이번 조정은 기술적 조정에 가깝다고 보지만, 금리 인상, 환매 중단 등의 압력이 이미 축적되어 중기 리스크에 대한 경계가 필요하다.

- 핵심 요소:

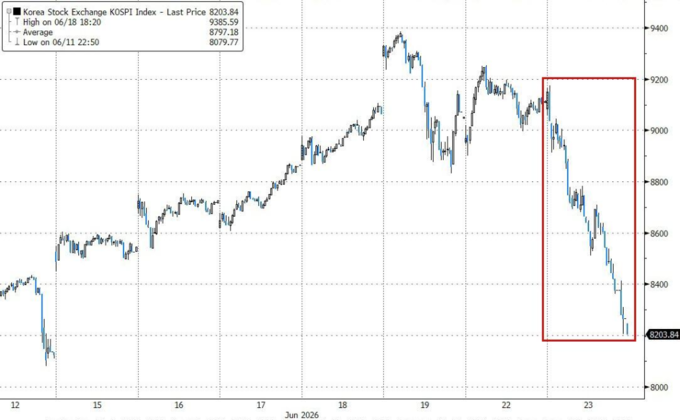

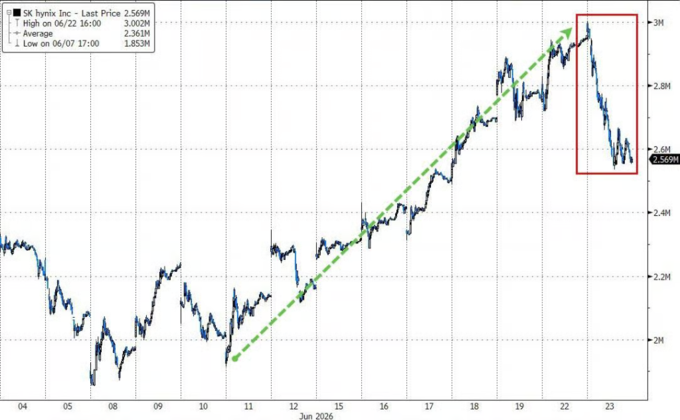

- 한국 KOSPI 지수는 하루 만에 10% 폭락했으며, SK하이닉스(HBM4 증설 둔화 루머)와 삼성전자는 10% 이상 하락해 서킷브레이커가 발동되었다; 미국 필라델피아 반도체 지수(SOX)는 7.9% 하락했고, 30개 구성 종목이 모두 하락했으며, 마이크론 테크놀로지는 13% 하락했다(연초 대비 300% 이상 상승).

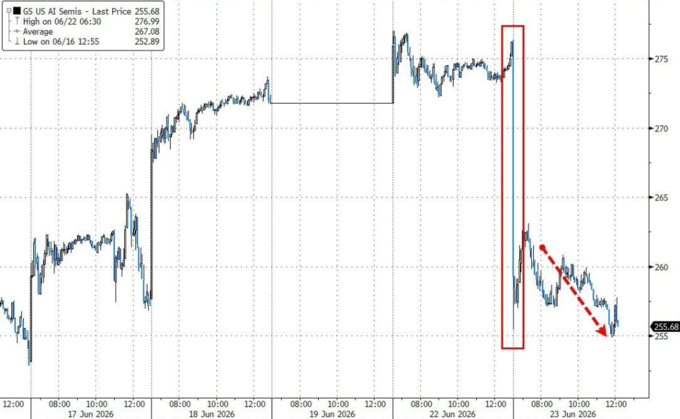

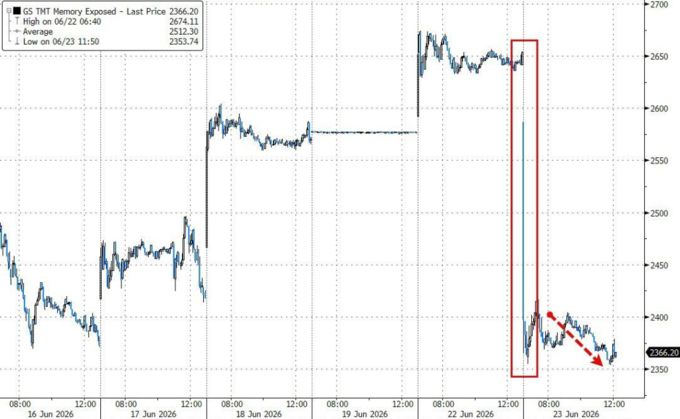

- 골드만삭스는 당일 매도세가 '질서정연'했으며 거래량은 평균 수준이었고, 투자자 대화는 AI 서사의 전환이 아닌 시장 상황에 집중되었으며, 대규모 자산 재배분은 나타나지 않았다고 지적했다; 하락폭은 '과밀 매수' 부문에 집중되었다(예: 골드만삭스 메모리 주식 바스켓 10% 하락, AI 반도체 바스켓 620bp 하락).

- 구조적 리스크는 다음과 같다: 나스닥 지수는 3월 말 이후 30% 이상 상승했으며, 6월 필라델피아 반도체 지수는 거래일의 절반에서 등락률이 ±5%를 넘었다; 65%의 기업이 환매 조용기간에 있어 '하방 지지' 세력이 부재하다; 연준的金利 인상 기대감이 고조되고 있어(7월 인상 확률 50% 상승), 고평가된 기술주를 억누르고 있다.

Original Title: [Korea Ignites 'Black Tuesday,' Global Chip Stock Bull Market Hit with a 'Blow,' Is It Just a 'Technical Adjustment'?]

Original Source: Wall Street Sights

The crash in chip stocks was not an accident triggered by a Korean 'rumor,' but an inevitable liquidation within an extremely crowded AI sector burdened by leverage. Analysts at Goldman Sachs and others believe the AI narrative has not shifted, and the sell-off was concentrated in crowded long positions, resembling more of a 'technical correction.' However, with rising expectations of interest rate hikes and 65% of companies in a buyback blackout period, multiple pressures are mounting, and the line between a correction and medium-term risk is not clearly defined.

On Tuesday, June 23rd, global chip stocks were caught off guard by South Korea. One Wall Street strategist dubbed the sell-off a 'chip-wreck.'

The first to collapse was South Korea's stock market, this year's 'hottest in the world.' The KOSPI index plunged 10% in a single day, triggering circuit breakers multiple times, with SK Hynix and Samsung Electronics each falling over 10%.

Several rumors ignited the storm: South Korean media reported that Nvidia's Rubin was expected to see production cuts, and SK Hynix was slowing the expansion of HBM4 production, shifting towards cheaper standard DRAM. Secondly, Yonhap News reported that lawmakers from multiple parties in South Korea were discussing a tax on unrealized gains from assets like stocks and real estate – meaning taxes would be due even on paper profits not yet sold.

This 'chip earthquake' quickly spread to the US stock market.

Overnight, the Philadelphia Semiconductor Index (SOX) fell 7.9% in a single day, with all 30 component stocks declining. Micron Technology dropped 13% – before Tuesday, it was up over 300% for the year and was the strongest component in the SOX. Micron, Nvidia, and AMD collectively accounted for about 50% of the S&P 500's decline. The Nasdaq closed down 3.3%, the Dow fell just 0.1%, and the S&P 500 dropped 1.4%.

Jonathan Krinsky, Chief Market Technical Analyst at BTIG LLC, stated: "Regardless of a short-term rebound, we still see medium-term downside risk in the tech/AI sector." He believes the semiconductor sector has another 10% to 15% downside, describing Tuesday's trading action as a "chip-wreck."

However, Peter Callahan, TMT sector specialist at Goldman Sachs Global Banking & Markets, wrote in a quick note on June 24th: "Today's conversations with investors have largely centered around 'what are you seeing out there' rather than signs of a broader narrative shift." This statement is crucial. It puts a boundary on the sell-off: the market action was ugly, but at least on that day, there was no evidence of capital deserting the AI trade altogether.

So the issue isn't simply "a Korean rumor crashes the global AI bull market." It looks more like a sector that was already fully priced, crowded with trades, and carrying significant leverage, hitting a trigger point and undergoing collective risk reduction. In the short term, it indeed has the hallmarks of a 'technical adjustment'; in the medium term, the vulnerabilities of the AI trade have not disappeared.

This Was a Contagion, Not an Accident

The crash in South Korea seemed sudden, but the logic behind it is not complicated.

The news of SK Hynix slowing HBM4 expansion smashed SK Hynix's stock. Given its weight in the Korean stock market – similar to Apple's weight in the Nasdaq – its sheer size meant trouble for the entire index. More crucially, a large number of Korean retail investors use leveraged ETFs to participate in AI/semiconductor trades. When the market falls, these products are forced to sell to maintain their leverage ratios, creating mechanical selling pressure.

The news itself was the trigger, but the leveraged structure was the dynamite. Meanwhile, some market observers ask: "Could Korean retail investors using leverage be the terminators of the US tech bull market?"

While somewhat exaggerated, this question points to a genuine vulnerability: AI/semiconductor trading is highly concentrated, with global investors holding remarkably similar positions. A sell-off at any node can propagate along this chain.

According to Goldman Sachs' post-market data, both longs and shorts were selling that day. Long-Only (LO) funds had a selling skew of -18%, and Hedge Funds (HF) were also selling consistently throughout the day, with shorts accounting for 60% of sales volume (vs. a recent average of ~50%). The notional exposure sold by both types of institutions exceeded $1 billion.

The worst-hit stocks in the US were those 'crowded long' positions and the 'most profitable' stocks of the year: Goldman Sachs' Memory Chip Basket (GSTMTMEM) fell 10%, the AI Semiconductor Basket (GSCBSMHX) dropped 620 basis points, the AI Stock Basket (GSTMTAIP) fell 440 bps, and the 12-month Momentum Basket (GSXHUHMOM) declined 420 bps.

Technical Adjustment? Goldman Sachs: Narrative Hasn't Shifted Yet

With such a significant drop, what does the market really think? If you only look at the decline, Tuesday seemed like a repricing of the AI trade. But based on volume and capital flows, the conclusion is less absolute.

Goldman Sachs TMT desk specialist Peter Callahan wrote in his post-market note that the feeling of the day could be described as 'orderly.' Despite the sizable decline, overall Nasdaq volume was roughly in line with the 20-day average, and cash and volatility desks functioned normally.

More importantly, he described the conversations with investors: "Today's conversations with investors have largely centered around the theme of 'how things look on your end,' with no signs of a broader narrative shift or incremental inquiries about 'new names' or 'laggards.'"

In other words, nobody was rotating. Nobody was searching for new investment directions. Everyone was just checking in with each other.

Another Goldman Sachs market strategist, Chris Hussey, provided specific data support: Of the 12 tech stocks that fell over 8% today, all but one remain up by double digits year-to-date, with most having more than doubled. His assessment:

"Today's sell-off feels more like 'skimming the froth' off an exuberant stock rally than a fundamental reassessment of the AI infrastructure trade. Investors aren't broadly selling the index; they are re-evaluating how much to pay for stocks that have doubled in six months."

Jack Janasiewicz, portfolio manager at Natixis Advisors, shares a similar view:

"This looks more like a technical sell-off than anything else. Market breadth was decent post-open, despite many big red numbers – a signal of a narrow sell-off." He also cautioned, "When you have such massive crowding in beta and momentum, it's a setup prone to an ugly deleveraging event."

The Other Side of 'Technical Adjustment': Structural Concerns That Can't Be Ignored

The term 'technical adjustment' can be comforting, but it can explain everything and may also mask real risks. Indeed, the market action on Tuesday had technical characteristics: decline concentrated in winning stocks, no full-blown capitulation in volume, and investor conversations showed no immediate narrative change. However, there isn't a clear wall between a technical adjustment and structural risk – the former, if violent enough, can easily morph into the latter.

Several background numbers are worth considering together.

First, the rally was too rapid. The Nasdaq has risen over 30% since the end of March. Just in June, the Philadelphia Semiconductor Index experienced intraday swings exceeding ±5% on 8 out of 16 trading days – meaning half of the trading days in June saw violent fluctuations in chip stocks. Even after Tuesday's drop, the SOX is still up about 5% for the month, outperforming the Nasdaq and S&P 500 by roughly 8 percentage points. A correction at this level has both the justification of a technical pullback and the fragility of being at high altitudes.

Second, positioning is too crowded, and a key 'support' is temporarily absent. Julian Emmanuel, Chief Equity and Quantitative Strategist at Evercore ISI, told Bloomberg TV: "People are looking for reasons to hedge, while simultaneously wanting to stay invested." This perfectly describes the market's conflicted mindset. Meanwhile, 65% of publicly listed companies are currently in a buyback blackout period. In past sell-offs, corporate buybacks provided a crucial support, but this tool is currently off the table.

Third, the macroeconomic backdrop is changing. Expectations for Fed rate hikes are rapidly rising – Bank of America predicts three more rate hikes this year, and the market's pricing probability for a July hike has jumped from near zero to around 50%. The valuation logic for high-growth tech stocks is built on low-rate discounting. If rates rise, the present value of future earnings naturally contracts, hitting hardest those stocks whose high valuations depend on future expectations.

Michael O'Rourke, Chief Market Strategist at JonesTrading Institutional Services, wrote: "Hyperscalers are the new software stocks. This sector is dragging down the 'Magnificent Seven,' yet can't seem to find its own footing."

Torsten Slok, Chief Economist at Apollo, outlined three core questions facing the market: What if AI companies start cutting their compute budgets due to insufficient ROI? What is the impact on equity and credit markets if the Fed raises rates in September and December? These questions have no easy answers, but the market is shifting from 'willing to ignore these risks' to 'beginning to take them seriously.'

The reason a 'technical adjustment' deserves serious attention is not the magnitude of the decline itself, but because it occurs when valuations, positioning, interest rates, and sentiment are all at extreme levels.

Historically, Korean Crashes Are Brief – The Next Stress Test is Micron

Historical data shows that sharp declines in the Korean stock market are often violent but brief. This is the 'silver lining' that bullish investors are quick to point out.

However, this time's context differs from past events confined to Korea: it touches the very core of the global AI trade – Is demand for memory chips truly as strong as expected? Has the frenzy in data center construction already borrowed from the future?

These questions will be partially answered after Micron's earnings report on Wednesday. As the strongest component in the SOX this year, up over 300% before Tuesday, Micron's report represents a genuine stress test.

BTIG's Krinsky perhaps put it most directly: "Regardless of a short-term rebound, the medium-term downside risk for semiconductors remains."