SEC는 '주식 토큰' 혁신 면제를 연기했습니다. 누가 그렇게 맹렬히 반대하고 있을까요?

- 핵심 의견: 미국 증권거래위원회(SEC)는 원래 '미국 주식 토큰화'를 위해 '혁신 면제'를 도입할 계획이었으나, 월스트리트의 전통 세력과 SEC 내부에서 유동성 파편화, 규제 준수 위험 및 법적 허점을 이유로 강력히 반대하여 해당 계획이 연기되었고, 이로 인해 암호화폐 시장이 단기간에 크게 하락했습니다.

- 핵심 요소:

- SEC가 '혁신 면제' 계획을 연기했습니다. 이 계획은 원래 더 완화된 조건에서 미국 주식의 체인 상 토큰 거래 서비스를 제공하는 것을 허용하려는 것이었으며, 토큰화 증권을 지원하는 중요한 신호로 간주되었습니다.

- 이러한 악재 소식의 영향으로 BTC는 76,000 USDT 아래로, ETH는 2,100 USDT 아래로 각각 하락했습니다. 관련 개념 토큰인 ONDO는 상승분을 반납하며 24시간 동안 6.4% 하락한 0.382 USDT를 기록했습니다.

- 반대 진영은 주로 Citadel Securities, SIFMA 등 월스트리트의 전통 세력으로 구성되어 있으며, 시장 유동성 파편화, AML/KYC 규정 준수 부재, 그리고 법적·기술적 측면에서 토큰 권리 집행의 허점을 우려하고 있습니다.

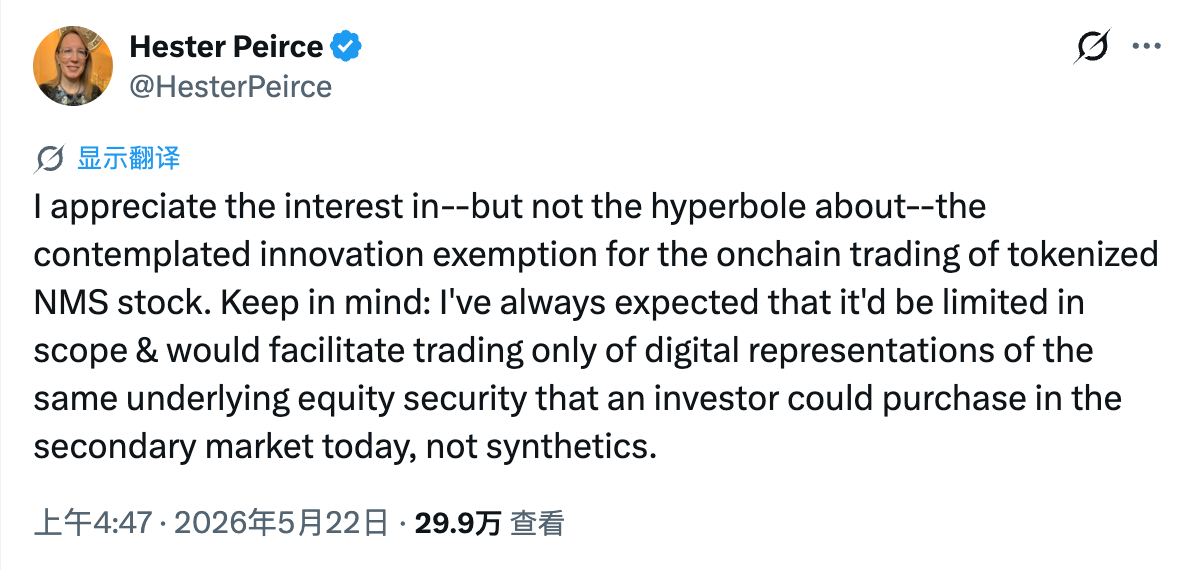

- SEC 위원이자 '암호화폐 엄마'로 불리는 Hester Peirce 역시 면제 범위를 축소하는 쪽에 기울고 있으며, 제3자가 합성 자산을 발행하는 방식 대신 발행자 자체가 주도하는 토큰화만을 허용하는 것을 지지합니다.

- 규제가 일시 중단되었음에도 불구하고, Ondo, Hyperliquid와 같은 암호화폐 네이티브 세력과 DTCC, 나스닥, ICE와 같은 월스트리트 기관들은 각자 토큰화된 자산과 블록체인 프레임워크 구축을 더욱 가속화하고 있습니다.

Original | Odaily Planet Daily (@OdailyChina)

Author | Azuma (@azuma_eth)

In the early morning of May 23rd, Beijing time, Bloomberg reported citing sources that the U.S. Securities and Exchange Commission (SEC) has postponed the planned “innovation exemption” initiative. Originally intended to greenlight products related to “tokenized U.S. stocks,” the SEC decided to halt progress due to numerous concerns raised by market participants.

Affected by this negative news, the cryptocurrency market experienced a sharp short-term decline, with BTC falling below 76,000 USDT and ETH dropping under 2,100 USDT. Tokens related to the “tokenized U.S. stocks” concept were hit even harder; ONDO completely reversed the short-term gains it had made yesterday following the indirect stimulus from the “SEC's penalties on brokerages like Tiger Brokers, Futu, and Changlei,” and as of writing, it is trading at approximately 0.382 USDT, down 6.4% in 24 hours.

Innovation Exemption, Brakes Slammed at the Last Minute

Since the inauguration of current Chairman Paul Atkins, the SEC has shifted away from the previous hardline stance of “enforcement as regulation,” leaning towards providing a compliant testing ground for the crypto industry.

Earlier this week, market rumors emerged that the SEC would unveil an exemption proposal as early as this week, aiming to allow trading platforms to offer on-chain token trading services for already listed securities (such as US stocks like NVDA, AAPL, and TSLA) under more relaxed regulatory conditions. Driven by SEC Chairman Paul Atkins and Commissioner Hester Peirce, this exemption aims to create a legal testing space for tokenized securities. The market interpreted this as a significant signal of US regulators moving further towards supporting tokenized securities.

However, this innovation exemption, initially expected to be publicly revealed as early as this week, was abruptly halted at the last minute. Sources revealed that the SEC has now withdrawn the draft and has re-initiated intensive consultations with stock exchanges and other market participants.

From “full green light” to “emergency brake,” what kind of resistance has the SEC faced? In this epic battle over “putting US stocks on-chain,” who is fiercely opposing it?

Opposition, Again from Wall Street

Similar to the CLARITY Act, which also faces resistance (see Why is there such deep division over the delayed CLARITY review?), at the forefront of the opposition against this exemption proposal are Wall Street's traditional powers, represented by Citadel Securities and the Securities Industry and Financial Markets Association (SIFMA).

As early as months ago, when this policy was still in its early stages, these traditional financial giants had already submitted sharply worded opposition letters to the SEC. In summary, the core arguments from Wall Street are mainly focused on the following three points.

First, concerns about potential market liquidity fragmentation. Institutions like Citadel Securities warn that allowing various third parties to bypass issuers and issue “synthetic US stocks” indiscriminately would lead to the fragmentation of US stock assets scattered across countless DeFi platforms lacking interconnectivity, depth, and price transparency. This would not bring efficiency but would instead leave investors uncertain about the actual value corresponding to the tokenized stocks they hold at any given moment.

Second, fears that tokenized stocks might threaten traditional compliance defenses. On anonymous or pseudo-anonymous public blockchain networks, how can it be ensured that transactions of these third-party tokens do not become a hotbed for money laundering? Wall Street giants argue that the current technological capabilities of decentralized platforms are simply insufficient to rigorously enforce core investor protection mechanisms like AML and KYC.

Third, existing technological and legal gaps. Citing opinions from legal experts, institutions point out that allowing an unaffiliated third-party crypto platform, without authorization from companies like Apple or Microsoft, to implement features like “granting token holders voting rights and dividend distribution” on-chain still presents uncertainties under the current legal frameworks and technological pathways.

Internal Reservations Within the SEC

It is noteworthy that this wave of opposition comes not only from Wall Street's “vested interests” but also includes cautious reservations within the SEC itself.

Hester Peirce, the SEC commissioner affectionately known as “Crypto Mom” within the community and a long-time ally, publicly stated yesterday on X that she had shifted her position, indicating that the scope of this exemption should be strictly limited.

Peirce stated that what the SEC should allow are attempts by “the issuers themselves or their affiliates” to digitize or tokenize their own stocks on-chain; not to let a bunch of synthetic assets issued by third parties, free from regulatory control, flood the market. In other words, the “tokenized US stocks” that Peirce envisions should be led, authorized, or endorsed by the specific listed company itself (the issuer), and must guarantee investors rights equivalent to those of ordinary shareholders (such as dividends, voting rights, etc.), rather than the derivative synthetic tokens currently more common in the market, which track the price performance of the underlying stocks and are issued by third parties.

Even Peirce, who has consistently been an aggressive supporter of crypto innovation, chose to side with “restricting the scope of the exemption,” highlighting the significant legal and compliance hurdles the proposal faces.

What Future Awaits the Intersection of Crypto and Stocks?

This week's “halt in progress” undoubtedly deals a heavy blow to the RWA (Real World Assets) track, which was on the cusp of a breakout. The sharp short-term decline in tokens like ONDO reflects the market's overly optimistic expectations for the “full on-chain compliance of US stocks.” However, it is undeniable that regardless of the regulatory stance's vacillation, the trend of combining US stock assets with blockchain technology has become an irreversible torrent. Beneath the shadow of this regulatory struggle, both crypto-native forces and traditional Wall Street institutions are racing fiercely on their respective tracks.

- On one hand, crypto-native forces are pushing through from the bottom up. Projects like Ondo, xStocks, and MSX are actively bringing US stock assets onto the chain, while platforms like Hyperliquid, Trade.xyz, and major CEXs are indirectly providing global crypto users with windows to invest in US stocks through perpetual contracts. This grassroots demand for innovation is constantly forcing regulators to provide clear answers.

- On the other hand, Wall Street itself is accelerating its layout in related businesses. The Depository Trust & Clearing Corporation (DTCC) plans to officially launch limited production trading of tokenized assets this July and expand promotion in October. Nasdaq is also developing a blockchain-based stock issuance framework. Intercontinental Exchange (ICE) has chosen to collaborate with leading crypto exchange OKX to jointly advance the development of tokenized stocks and crypto-related products.

In essence, this delay of the exemption is a fierce clash between an innovative attempt by a nascent force and the defensive mechanisms of the traditional establishment. Based on current developments, the SEC has not made a final decision on the revised draft, meaning the “innovation exemption” is not completely dead. However, it is foreseeable that given the fierce backlash from Wall Street giants and the correction of opinions within the SEC, even if this exemption is eventually reintroduced, its aggressiveness and scope of application may be somewhat “discounted.”

The dream of fully liberalizing the trading of “crypto-stocks” may still require a long journey through regulatory tug-of-war, but the door to asset tokenization has been forced open and is destined never to close again.