Huobi Growth Academy | Crypto Market Macro Research Report: Federal Reserve Power Transition, Bond Yields Surging, Liquidity Turning Point May Be Approaching

- Core Insight: In May 2026, the dual macro pressures of the Fed's change in leadership and surging global bond yields, combined with the triple selling pressure of ETF outflows, active spot/derivatives selling, and surging hedging demand from options, caused Bitcoin to plummet from $82,000 to $76,800. The market has entered a turning point where macro pressure coexists with the ongoing process of institutionalization.

- Key Factors:

- New Fed Chairman Warsh advocates for accelerated balance sheet reduction, redefining the inflation target, and weakening forward guidance. The short-term anti-inflation mandate exerts liquidity pressure on the crypto market, and the surprise PPI data in his first month in office intensified tightening expectations.

- Synchronized global bond sell-off: The 30-year US Treasury yield broke through 5.12% (a high since 2007), market probabilities for rate cuts plummeted while expectations for rate hikes rose, and the "higher for longer" rate narrative weighed on risk assets.

- Triple selling pressure resonance: ETF recorded consecutive net outflows exceeding $1.5 billion; simultaneous active selling in both spot and perpetual futures markets; options 25-Delta skew rose to 14.4%, indicating a sharp increase in hedging demand.

- Rising stagflation risk: US April CPI rose to 3.8%, PPI surged 6% year-on-year. The market's estimated probability of stagflation jumped from 11% to 40% within a month, putting the Fed in a policy dilemma.

- Institutionalization process not interrupted: Galaxy Digital is advancing its AI computing transition; some long-term holders are accumulating at lower prices, with net Bitcoin inflow to exchanges reaching $1.68 billion/week moving to cold wallets.

- Market trajectory scenarios: Range-bound consolidation ($75,000-$77,000, 55% probability), bullish rebound (dovish signals + geopolitical easing, 25% probability), bearish deep correction (US Treasury yield exceeds 5.2%, 20% probability).

1. Warsh Takes Over: Fed Power Transition and Policy Logic Restructuring

On May 15, 2026, Jerome Powell officially stepped down as Chair of the Federal Reserve, handing over the reins to Kevin Warsh, a Hoover Institution fellow at Stanford University and former Fed governor. Warsh's nomination was confirmed with a Senate vote of 54 in favor and 45 against, a relatively close tally that foreshadowed the persistent pressure his policy stance would face from all sides. On his first day in office, Wall Street put on a superficially "dignified exit" with the Nasdaq Composite rising over 1%, but deeper undercurrents of change were already brewing in market pricing.

Warsh's policy agenda revolves around three main directions. First, accelerating the reduction of the Fed's balance sheet. Currently standing at approximately $6.7 trillion, Warsh has been critical of the balance sheet's size and advocates for a more aggressive reduction. An accelerated pace of quantitative tightening would effectively drain liquidity directly from the financial system, pushing up long-term interest rates and tightening the overall monetary environment, exerting systemic pressure on risk assets, including cryptocurrencies. Second, redefining the inflation target. Warsh has questioned the authority of the 2% numerical target, leaning towards a vaguer formulation like "price stability." This could mean a higher actual tolerance for inflation, but also increases policy arbitrariness and makes market prediction more difficult. Third, scaling back forward guidance and the dot plot. Warsh advocates for reducing or eliminating predictive tools like "forward guidance" and the "dot plot," aiming to increase the Fed's policy flexibility. However, this would also widen the information gap between the market and the central bank, potentially amplifying short-term volatility.

For the crypto market, Warsh's stance has a nuanced duality. Before being nominated as Fed Chair in January 2026, Warsh publicly stated that Bitcoin is a "significant asset" and a "good cop for policy," showing an overall openness to cryptocurrencies. However, this moderate stance creates a structural conflict with his immediate urgent task: facing a PPI year-over-year surge of 6% in his first month, Warsh must prioritize proving his anti-inflation credibility over promoting crypto-friendly policies. Therefore, in the short term, Warsh's anti-inflation mission puts liquidity pressure on the crypto market. Long-term, his attitude towards digital assets could foster a more favorable regulatory environment for institutional entry into the crypto market. Weighing these factors, the market's short-term focus remains on when the tightening of liquidity will materialize, rather than distant regulatory dividends.

2. Bond Market Anomaly: The Alarm of a Global Liquidity Inflection Point

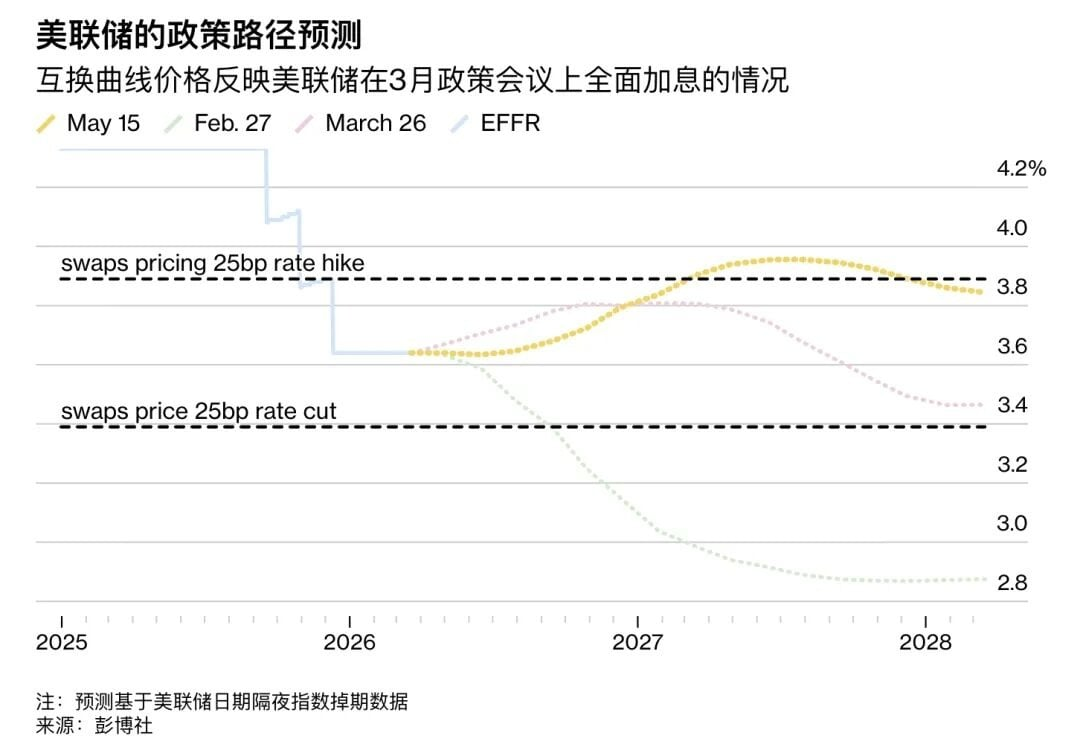

If the change in Fed leadership was merely a disruption to expectations, the concurrent turmoil in the bond market represents a more direct and tangible shock to risk assets. In May 2026, global bond markets experienced a rare sell-off, with sovereign bond yields in multiple countries surging to multi-year or even multi-decade highs. In mid-May, the yield on the US 30-year Treasury bond broke through the psychologically significant 5% mark, hitting 5.12%, its highest level since 2007; the 10-year Treasury yield correspondingly rose to 4.63%, a notably high level in recent years. Japan's 10-year government bond yield hit a 30-year high of 2.797%, the UK 30-year gilt yield rose to 5.86%, France's 30-year bond yield reached 4.675%, and even Germany's 30-year yield, long near negative territory, climbed to 3.704%.

The immediate trigger for this global bond sell-off was the surprising US April PPI data. The PPI rose 1.4% month-over-month, far exceeding the market expectation of 0.3% and marking the largest single-month increase since 2022. The year-over-year PPI reached 6%, nearly wiping out three years of the Fed's anti-inflation efforts. As a leading indicator for CPI, the surge in PPI made the market realize that inflation is not falling back to the 2% target as expected, prompting an immediate global repricing. More crucially, the anticipated path of interest rate cuts was completely shattered. Before the sell-off, the market broadly expected two rate cuts in 2026, with the first in June almost certain. After the sell-off, the probability of a rate cut plummeted to 15%, and expectations of a slight rate hike began to emerge, with the probability of a 25 basis point hike by July 2027 rising to 60%. The "Higher for Longer" narrative made a comeback.

The surge in bond yields transmitted to the crypto market through multiple channels. First, rising opportunity cost: higher risk-free rates make non-yielding assets like Bitcoin less attractive compared to cash and short-term Treasuries. Second, declining risk appetite: expectations of tighter liquidity lead to systematic selling of high-beta assets. Third, dollar strengthening: rising real interest rates typically coincide with a stronger US dollar, creating additional headwinds for dollar-denominated risk assets. Fourth, the leverage accelerator effect: a large buildup of leveraged long positions earlier in May 2026 led to margin calls triggering forced liquidations, creating a cascading deleveraging waterfall. Data shows that on the day Bitcoin hit its low of $78,704 alone, over $304 million in leveraged long positions were liquidated across the market, with Bitcoin longs accounting for about $94 million. This chain of transmission collectively formed the macro foundation for the recent Bitcoin crash.

3. Bitcoin's Plunge: The $76K Key Support Defense and the Triple Selling Pressure Resonance

In mid-May 2026, Bitcoin experienced a sharp sell-off since the start of 2026 under the resonance of multiple macro pressures. It fell from around $82,000 to $76,800 at one point, a decline of roughly 6%, washing out over $304 million in leveraged long positions across the market. Notably, the peculiarity of this decline lies in the simultaneous emergence of triple selling pressure signals, preventing market participants from simply attributing it to a technical correction.

The first wave of selling pressure came from the persistent outflow of institutional funds from ETFs. Starting May 7, 2026, US spot Bitcoin ETFs recorded consecutive net outflows, with a single-day outflow of $648 million, the highest since January 29. Total cumulative net outflows since May 7 have exceeded $1.5 billion. This scale of institutional capital exodus indicates a fundamental shift in institutional investors' macro pricing logic for Bitcoin. They no longer view Bitcoin as a beneficiary of loose monetary policy but are beginning to price it within the framework of traditional risk assets for hedging purposes. ETF outflows are both a result and a cause of the decline: falling prices trigger programmed stop-losses, which in turn exacerbate selling pressure, creating a negative feedback loop.

The second wave stemmed from synchronized active selling in both the spot and perpetual swap markets. Data from Glassnode shows that the Cumulative Volume Delta (CVD) in the spot market plummeted from +$16.9 million to -$126.2 million, and the CVD in the perpetual swap market registered a significant negative value of -$368.5 million. Both turning negative simultaneously means sellers are actively and unilaterally selling in both spot and futures markets, rather than being passively liquidated. Historically, this pattern of dual-market active selling usually corresponds to more persistent selling cycles, as passive liquidation is a one-off event, whereas active selling represents the seller's sustained bearish outlook.

The third source of pressure came from the sharply rising hedging demand in the options market. The 25-delta skew for options quickly rose from 10.9% to 14.4%, reflecting a significant increase in market participants' demand for downside protection. A higher skew indicates greater relative demand for put options, a typical institutional reaction when exposed to systemic risks. Vikram Subburaj, CEO of India-based exchange Giottus, pointed out that Bitcoin's first support level is around $76,000, with a secondary support zone between $74,000 and $75,000. A break below this area could trigger a deeper correction. On-chain data suggests the $76,000 to $75,000 range corresponds to price levels before the 2024 ETF-driven rally and is also a dense trading zone for a large amount of leveraged positions. A loss of this level could cause technical stop-loss selling, potentially triggering an even larger chain reaction.

4. Stagflation Fears Reignite: The Dual Dilemma of Sticky Inflation and Slowing Growth

The US April CPI rose to 3.8% year-over-year, its highest level since June 2023. The PPI surged 6% year-over-year, with a month-over-month increase of 1.4%, the biggest since 2022. The probability of stagflation (defined as facing a stagflationary shock by year-end) jumped from 11% to 40% within a month, indicating that the market's pricing of "stagflation" is rapidly intensifying. The frightening aspect of these figures lies not just in the numbers themselves, but in their crippling effect on the Fed's policy space: traditionally, an economic slowdown calls for rate cuts, but high inflation prevents the Fed from doing so; fighting inflation requires rate hikes, but signs of a slowing economy limit the room for hikes. The Fed is trapped in a "no-win dilemma," and the persistence of this dilemma is itself the biggest source of market uncertainty.

The transmission mechanism of rising stagflation risk to the crypto market is particularly complex. From a nominal rate perspective, high inflation pushes nominal rates higher, raising the benchmark for risk-free returns and increasing the opportunity cost of holding zero-yield assets like Bitcoin. From a real rate perspective, if nominal rates rise less than inflation, real rates could still fall, potentially providing some theoretical support for Bitcoin. However, the peculiarity of this cycle is the Fed's noticeably lagging policy response. While the market is already repricing rate hikes, the Fed is in a transition period under its new Chair. This "policy vacuum" prevents the market from relying on the "Fed put" (the implicit promise of the central bank to intervene during market crashes), amplifying the magnitude of downside volatility.

Simultaneously, global risk assets are experiencing a synchronized sell-off. South Korea's KOSPI index fell 6.12% in a single day, briefly triggering a circuit breaker. Japan's Nikkei 225 fell 6.22%, the Nasdaq dropped 1.54%, and China's Shanghai Composite fell 2.5% over two days. This pattern of cross-market synchronized decline indicates that the current adjustment is not an isolated event in the crypto market, but a systemic reflection of global liquidity tightening across all risk assets. The bond market "sounded an alarm" for both the AI bull market and the crypto market. When the "safety cushion" of risk-free rates disappears, all high-valuation assets dependent on future discounted cash flows face repricing pressure.

5. Market Structure Observations: Institutionalization Progress and Internal Differentiation

Despite the sharp short-term price decline, the institutionalization process of the crypto market has not been interrupted by this adjustment. Galaxy Digital successfully completed the initial delivery for the first Bitcoin computing power-related investment product targeting institutional clients. The first Phase 1 data hall was delivered to CoreWeave (CRWV) on time and on budget, marking the transition of Bitcoin mining infrastructure towards AI/HPC computing power leasing entering a substantive commercialization stage. The continuation of this structural trend suggests that over a longer time horizon, institutional capital is still systematically increasing its allocation to core crypto assets, rather than abandoning its layout due to short-term volatility.

Meanwhile, the division within the crypto mining camp is also widening. Keel Infrastructure (formerly Bitfarms) reported a Q1 2026 net loss of $145.4 million and a 23% year-over-year revenue decline to $37 million. However, its stock price rose over 8% on the day of the earnings release. The market's focus was not on the loss itself, but on whether its 2.2 GW of AI/HPC data center development pipeline can be converted into formal leases between 2027 and 2028. This narrative of "swapping Bitcoin mining tail assets for long-term AI infrastructure leases" is becoming the most market-recognized logic in the mining transformation camp.

On-chain data also reveals a differentiation pattern of "accumulation amidst panic." Despite significant ETF outflows, the net inflow of Bitcoin into exchanges is accelerating, with approximately $1.68 billion per week flowing into cold wallets. This indicates that some long-term holders are accumulating coins at lower prices. The supply held by long-term holders is stabilizing, and the selling of high-cost coins acquired in the $100,000 to $126,000 range is largely complete. This suggests that potential selling pressure has been significantly released. Historically, when the derivatives market is at an extremely bearish positioning (e.g., the 30-day funding rate at the 6th percentile, the lowest since early 2023), it often precedes a sharp reversal rather than a continued decline. When almost all participants have already shorted, the source of additional selling pressure is limited, but any positive catalyst could trigger massive short covering, providing fuel for a "V-shaped reversal."

6. Conclusion: Three Scenario Projections and Investment Framework

Looking ahead to the crypto market direction for late May and June 2026, the probabilities and trigger conditions for three scenarios warrant close attention. The most likely scenario is "range-bound consolidation": Bitcoin finds technical support in the $75,000 to $77,000 range, and the market waits for new catalysts while digesting macro headwinds. If bond yields can stabilize and the $76,000 support holds, the market could enter a 2-4 week consolidation phase, awaiting the next directional signal. In this scenario, the overall crypto market shows a pattern of "can't fall much, can't rise much," and alpha opportunities will come more from individual coin selection than systematic long bets.

The bullish scenario requires a confluence of two or more positive catalysts: first, a clear easing signal from the Fed or Warsh (e.g., a dovish stance at the June FOMC meeting); second, a substantial de-escalation in Middle East geopolitical tensions (the Hormuz Strait issue back at the negotiating table); third, confirmation that April inflation data is trending down. If all three conditions are met, reignited rate cut expectations could drive Bitcoin to quickly reclaim the $80,000 mark and potentially challenge the $85,000 to $87,000 range. The probability of a bullish scenario is currently estimated at around 25%, with the main obstacle being that Warsh is unlikely to quickly pivot towards easing early in his term.

The bearish scenario is the direction requiring the most vigilance: if the 30-year US Treasury yield continues to climb and effectively breaks through the 5.2% to 5.3% range, a rapid rise in risk-free rates could open the downside to $74,000-$75,000. A more extreme tail risk involves opening the channel to $54,000-$38,000 (corresponding to Stifel's trendline analysis target), which would mean a complete retracement of the 2025 bull market gains and a significantly prolonged bear market. The bearish scenario currently has a probability of about 20%, but the risk-reward is asymmetric. Once the $74,000 support is lost, programmed stop-losses could trigger a stampede, pushing prices below a fundamentally justified range.

In conclusion, the current market is in a structural inflection point characterized by the coexistence of "macro stress tests" and "deepening institutionalization." The alarm from the bond market has not been silenced, and the $76,000 to $75,000 support zone faces a severe test. However, against the backdrop of extreme bearish sentiment, continued accumulation by long-term holders, and the ongoing narrative of mining transformation, bottom signals are also gradually accumulating. Investors should maintain position flexibility at this stage, avoid aggressive chasing or heavy bottom-fishing, and patiently wait for the macro inflection point to appear. When the "Fed put" becomes effective again and bond yields turn downward, the next rally in the crypto market will have a more solid macro foundation.