Selling U.S. Treasuries, Buying Japanese Government Bonds: Wall Street Preps for 'Japanese Capital Repatriation'

- Core Thesis: As Japanese government bond (JGB) yields surge, global investors are betting that Japanese institutions will massively unwind roughly $1 trillion in U.S. Treasury holdings, with capital flowing back into the domestic JGB market, potentially delivering a major shock to global financial markets.

- Key Factors:

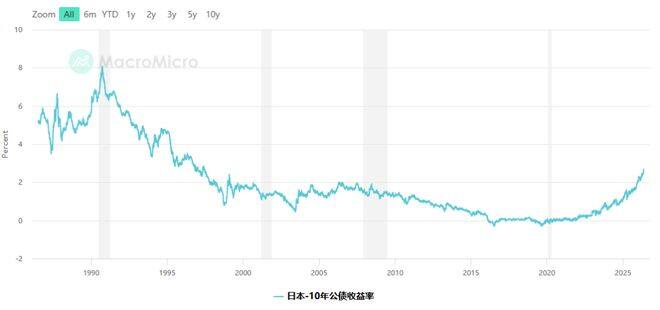

- Japan's 10-year government bond yield has climbed to 2.73%, a 28-year high; the 30-year yield has broken through 4% for the first time, signaling profound shifts in the interest rate environment.

- Japanese investors hold approximately $1 trillion in U.S. Treasuries, making them the largest foreign holders globally, implying enormous potential for capital repatriation.

- The Bank of Japan (BoJ) has raised its policy rate to 0.75% with the possibility of further hikes, and is gradually exiting quantitative easing, significantly enhancing the appeal of domestic bonds.

- Data reveals early signs: In March, Japan's sovereign bond funds saw net inflows of roughly $700 million, a monthly record, although over the past 12 months Japan still net purchased about $50 billion in foreign bonds.

- Analysts warn that Japanese fiscal expansion could depress JGB prices. Furthermore, as yield expectations continue to rise, investor willingness to buy is currently weak, meaning a large-scale repatriation has not yet materialized.

Original Author: Long Yue

Original Source: Wall Street Sights

The Japanese government bond market is experiencing dramatic shifts not seen in decades, prompting global asset managers to reassess a long-overlooked risk: could Japanese investors, who hold approximately $1 trillion in U.S. Treasuries, repatriate their capital?

According to the latest report from the Financial Times, several investment firms have begun preparing for a large-scale repatriation of Japanese funds, betting that Japanese investors will gradually sell U.S. Treasuries and pivot to buying Japanese Government Bonds (JGBs), whose yields continue to climb.

JGB Yields Surge to Multi-Decade Highs

On Friday, the benchmark 10-year JGB yield rose to 2.73% during trading, its highest level since May 1997.

The 30-year JGB yield breached the 4% mark for the first time—a level never reached since this bond was first issued in 1999. Yields on 5-year and 20-year JGBs also hit record highs earlier this week.

Japanese Finance Minister Satsuki Katayama told reporters on Friday that yields in major global bond markets are all rising, adding, "These dynamics interact with each other, creating a compounding effect."

Analysts expect JGB yields to continue climbing. The Bank of Japan raised its policy rate to 0.75% last December, the highest in three decades, and the market widely anticipates a further 25-basis-point hike to 1% in June this year.

The Logic Behind Trillions of Dollars 'Returning to Japan'

Understanding this bet requires first understanding why Japanese investors hold such massive assets overseas.

For decades, Japan maintained ultra-low interest rates, making domestic bonds nearly yieldless. In pursuit of returns, institutional investors—including Japanese insurance companies, pension funds, and banks—sought opportunities abroad on a large scale, buying U.S. Treasuries, European bonds, and global assets across the board.

Currently, Japanese investors hold approximately $1 trillion in U.S. Treasuries, making them the largest foreign holders of U.S. debt, far surpassing all other nations.

Now, with JGB yields rising sharply, this logic is reversing. Mark Dowding, Chief Investment Officer at British asset management firm BlueBay, directly highlighted this shift. BlueBay launched its first-ever Japan-focused bond fund this March.

Dowding stated, "New money will not be allocated overseas anymore. It will not flow into U.S. corporate bonds, nor U.S. Treasuries. It will come back to Japan for domestic allocation."

Funds Have Begun to 'Trickle' Back

Market data shows signs of capital repatriation are already emerging, albeit on a small scale.

According to data from fund tracking firm EPFR, investors poured a net inflow of approximately $700 million into Japanese sovereign bond funds in March this year, the largest single-month inflow on record for this category. Net inflows in April slowed to $86 million, returning to recent normal levels.

Matt Smith, a fund manager at Ruffer, offered a more direct assessment. He said, "Pressure is building—long-end domestic yields keep rising, and institutional signals clearly say, 'Bring your money back to Japan.' We believe the yen will strengthen, first slowly, then suddenly."

Smith also noted that Ruffer currently holds a long yen position as a core hedge. "Once market turmoil hits—especially centered around the U.S. credit market—as Japanese investors repatriate capital, the yen will strengthen."

Repatriation Not Yet in Full Swing, JGBs Also Face Concerns

However, analysts caution that Japanese institutional investors are still net buyers of foreign bonds.

Abbas Keshvani, Asia Macro Strategist at RBC Capital Markets, pointed out that despite JGB yields "ostensibly offering better compensation to investors," Japanese investors have still net purchased approximately $50 billion in foreign bonds over the past 12 months.

The reason lies in the uncertainty surrounding the JGB market itself. Japanese Prime Minister Shigeru Ishiba won the election in February this year, pledging expanded government spending and subsidies to counter inflationary pressures. Analysts increasingly warn that the government will be forced to compile a supplementary budget later this year, which would further depress JGB prices and push yields higher.

Keshvani stated, "Supply and demand dynamics both point to yields continuing to rise. As an investor, if you know yields will go up further, it's hard to find the motivation to buy now."

Previously, the Bank of Japan was the most important buyer in the market, heavily purchasing JGBs through quantitative easing and yield curve control policies. As the BOJ gradually exits, the market has reverted to traditional supply-demand logic, causing significantly increased price volatility in JGBs.

What This Means for the U.S. Treasury Market

The potential scale of Japanese capital repatriation means the U.S. Treasury market must take this risk seriously.

Japan is the largest foreign holder of U.S. Treasuries, with a position of approximately $1 trillion. If Japanese institutional investors begin systematically reducing their holdings, the impact on the supply-demand balance of U.S. Treasuries would be substantial.

Currently, bets on Wall Street are more of a forward-looking positioning rather than a reaction to events that have already occurred. However, as JGB yields continue to climb—analysts see a 10-year JGB yield reaching 3% later this year as a realistic target—the logic behind this bet will become increasingly clear.