AI 인프라 3대 라인, 누가 먼저 오르고, 누가 가장 강하며, 누가 아직 추격할 수 있을까?

- 핵심 관점: AI 산업의 폭발은 명확한 전달 체인을 보여준다: 우선 칩(기초 연산 수요)에 호재가 되고, 다음으로 에너지 병목 현상(데이터센터의 높은 전력 소비)이 드러나며, 마지막으로 장기적으로 저장 수요( AI 시스템의 지속적인 데이터 처리)가 상승한다. 이 논리는 지난 1년간 미국 주식 및 A주 관련 자산 상승률에서 유의미하게 입증되었다.

- 핵심 요소:

- 칩 계층: AI 수요는 가장 먼저 GPU(엔비디아), HBM 및 첨단 공정 주문으로 전환된다. 엔비디아의 2026 회계연도 매출은 전년 대비 65% 증가했으며, 장비 쪽(ASML, 램 리서치)은 연초 이후 27%-30% 상승했다.

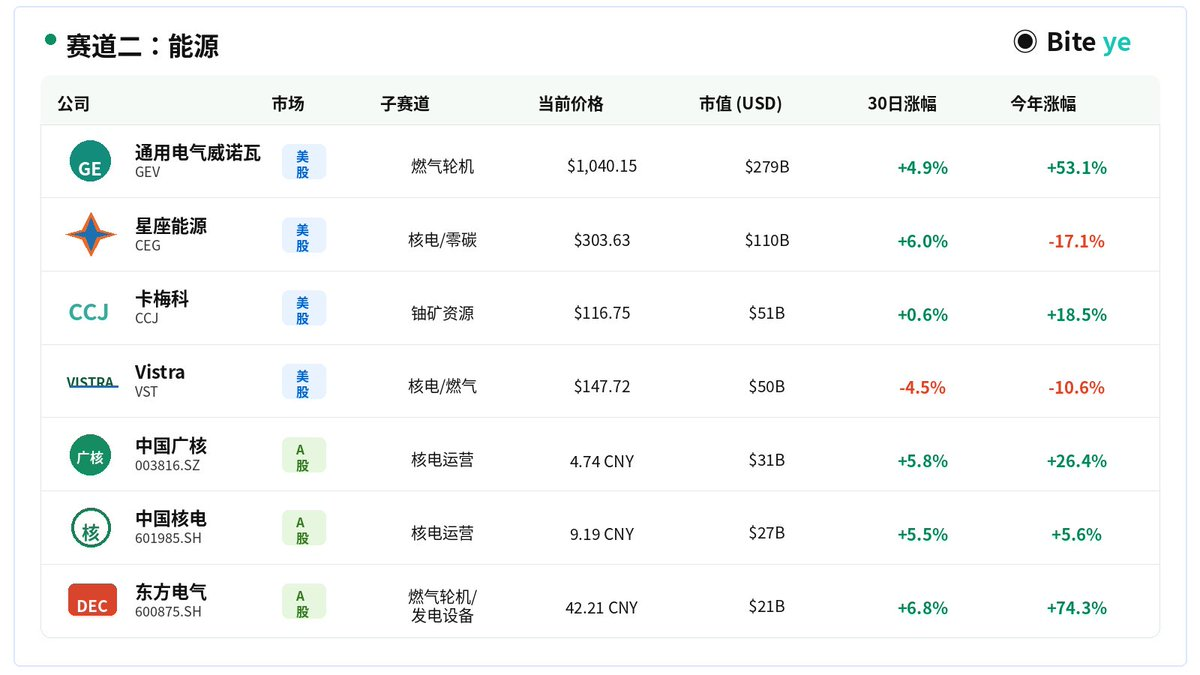

- 에너지 계층: AI 데이터센터의 랙당 전력은 50-100킬로와트(기존 5-15킬로와트)로 증가했다. IEA는 2030년 데이터센터 전력 소비가 945 TWh에 달해 두 배로 증가할 것으로 예측하며, 가스터빈(GE Vernova, 연간 167% 상승), 원자력 발전 운영사 등 자산 재평가를 촉진했다.

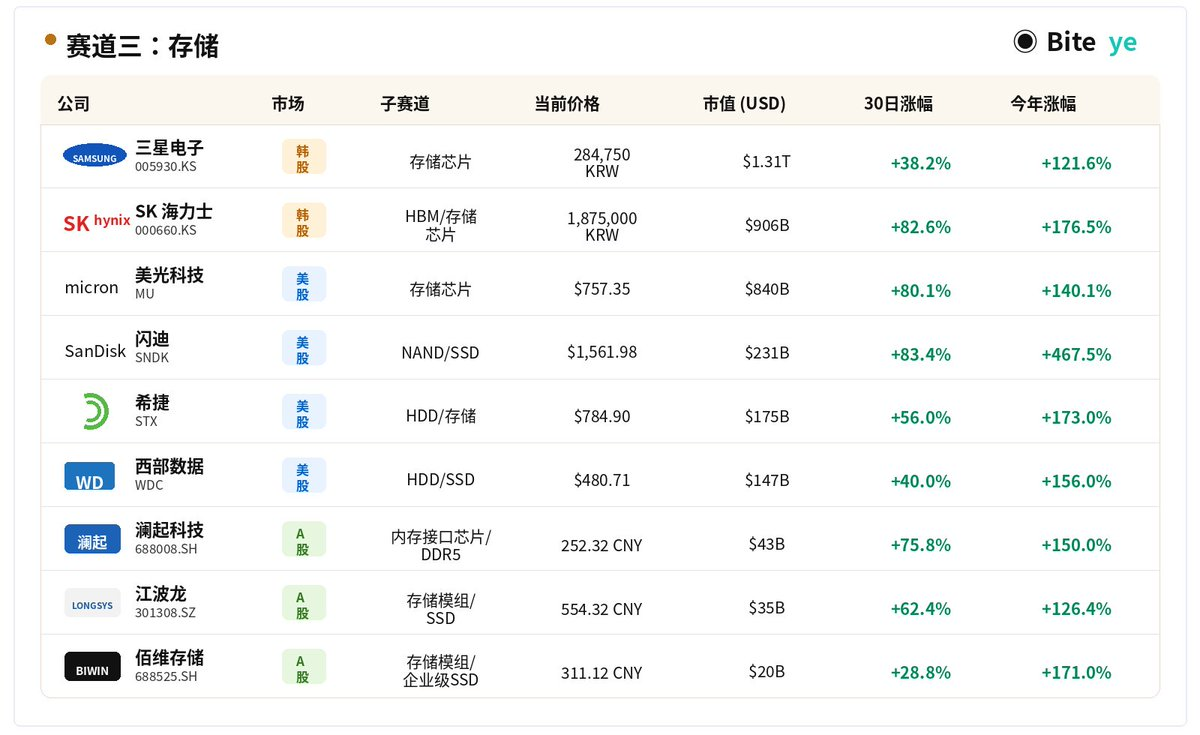

- 저장 계층: AI는 잦은 데이터 읽기/쓰기, 실시간 호출 및 캐시 압박을 초래한다. 저장 칩 원사(SK하이닉스 1분기 매출 198% 증가, 이익 406% 증가) 및 HDD 제조사(샌디스크, 연중 350% 상승)의 성과가 두드러진다.

- 저스틴 션(孙宇晨)이 지난해 11월 트윗에서 언급한 칩, 에너지, 저장 세 가지 라인. 당시 마이크론, 샌디스크 등 미국 주식 저장 컨셉주를 매수했다면 지금까지 180%-552% 상승했다.

- 국내 자산 측면에서, 海光信息(하이광신시)는 2024년 매출 91.62억 위안으로 전년 대비 52.4% 증가했다. 국산 연산 칩 및 저장 설계 기업(兆易创新(GigaDevice), 普冉股份(Puya Semiconductor) 등)도 동시에 혜택을 받았다.

Original Author: Changan I Biteye Content Team

Last November, Justin Sun posted a tweet:

If you take this statement as an industry judgment, not just a catchy phrase, looking back reveals:

These three lines represent almost the most realistic profit path in the AI market trend.

If, after that tweet, you bought into US-listed memory and storage concept stocks, what would the outcome be today?

• Micron: +214%

• Seagate: +180%

• Western Digital: +190%

• Sandisk: +552%

This article will break down the analysis along these three lines:

Why does AI first benefit chips, then create an energy bottleneck, and finally drive long-term growth in storage demand? Which assets have already emerged in this structural trend?

1. Chips: The First Thing AI Realizes is Not Narratives, But Orders

The first thing AI ignites is not the application layer, but the underlying computing power.

Whether it's training large models, daily inference, Agent calls, or multimodal processing, the first step is to run the computations, and these ultimately rely on GPUs, HBM, high-speed interconnects, and advanced manufacturing processes.

In other words, the growth in AI demand doesn't trickle down to the very end first; instead, it directly translates into a more immediate reality:

More chips needed. Stronger chips needed. Higher bandwidth chips needed.

This is why AI demand is first reflected in the chip sector.

Industry data already makes this very clear. Based on the fiscal year 2026 outlook, NVIDIA's revenue grew 65% year-over-year, indicating that demand for high-end computing chips continues to be released.

🌟Assets in this Direction

Core Computing Layer: NVIDIA (NVDA), AMD, Broadcom (AVGO), TSMC (TSM)

Domestic Computing Layer: Haiguang Information Technology (688041.SH), Cambricon Technologies (688256.SH), etc. Haiguang is a representative domestic x86 server CPU company, with 2024 revenue of 9.162 billion RMB, up 52.4% year-over-year.

Semiconductor Equipment Layer: ASML, Applied Materials (AMAT), Lam Research (LRCX). The ADR price of lithography giant ASML hit an all-time high at the start of 2026, surging over 8% on January 2nd alone, and has risen 27% since the beginning of 2026. Lam Research has risen 30% year-to-date, and Applied Materials has risen 28% year-to-date. All three semiconductor equipment giants significantly outperformed the S&P 500 index.

🌟Performance Over the Past Year

The chip track was the first to start and saw the largest gains in this wave of the AI bull market. NVIDIA, as the leader, has accumulated gains of over 1000% since early 2023. Equipment stocks continued to hit new highs in early 2026, remaining in a strong upward cycle. Citigroup released a research report predicting that the global semiconductor equipment sector will enter a "Phase 2 Bull Upward Cycle," with the clear main themes for chip stocks in 2026 being ASML, Lam Research, and Applied Materials.

2. Energy: As AI Scales, the Bottleneck Shifts from Chips to Electricity

No matter how many chips you have, they can't run without power.

Buying chips is just the beginning. The long-term operation of large models, data centers, and inference services requires a continuous power supply, plus additional power for cooling and heat dissipation loads. Traditional data center racks typically have a power density of 5 to 15 kW, while AI data centers have significantly raised this to 50 to 100 kW, creating an entirely different magnitude of power consumption and heat dissipation pressure. An IEA analysis this year noted that data center electricity consumption will roughly double from current levels to about 945 TWh by 2030, with AI being the primary driver. The US Department of Energy has also explicitly stated that the growth in data center electricity demand is placing significant pressure on regional power grids.

🌟Assets in this Direction

Gas Turbines: GE Vernova (GEV): Gas turbine orders are booming. Full-year 2025 orders reached $59 billion, with a backlog growing to $150 billion. Management raised its 2026 revenue guidance to $44-$45 billion.

Independent Power Producers: Constellation Energy (CEG): The largest zero-carbon power operator in the US, with nuclear assets directly signing long-term power purchase agreements with tech giants. Vistra (VST): Holds both nuclear and gas assets, with 2026 EBITDA guidance midpoint ~30% higher than 2025.

Uranium Resources: Cameco (CCJ): The world's largest publicly traded uranium mining company, a beneficiary of the nuclear energy resurgence at the upstream level.

🌟Performance Over the Past Year

GE Vernova's stock price has risen 167% over the past year. Its 52-week low was $408, and it reached a high of $1181, nearly tripling in that range. Constellation Energy hit an all-time high in 2025 but subsequently corrected about 28% from its peak due to regulatory policy uncertainty, currently trading at relatively lower levels. Vistra has remained strong overall, with long-term power supply contracts for data centers continuously being signed. The energy sector as a whole has been repriced from a traditional defensive position to a core beneficiary direction of AI infrastructure.

3. Storage: The Most Overlooked Direction, But Will Benefit Long-Term

The core logic favoring storage is simple: AI is not a one-time call; it is essentially a system that continuously ingests, accumulates, and calls data.

Training requires reading vast amounts of data, saving checkpoints during the process. Inference requires loading models and caches. RAG and Agents constantly access knowledge bases, logs, and memory.

Consequently, AI leads not just to "more data," but to:

• More frequent data reads and writes

• More real-time data access

• More complex data management

• Greater pressure on data migration and caching

Furthermore, the more expensive GPUs become, the less they can afford to be idle. This means the industry will place increasing importance on delivering data to computing power faster and more reliably.

In other words, the more AI develops, the less storage is just a "warehouse for data." It becomes the foundational data layer ensuring the entire AI system can run continuously.

🌟Assets in this Direction

Memory Chip Manufacturers: SK Hynix (000660.KS), Samsung Electronics (005930.KS), Micron Technology (MU)

NAND / SSD / HDD Manufacturers: Sandisk (SNDK), Seagate (STX), Western Digital (WDC)

Domestic Memory Design: GigaDevice, Puya Semiconductor, Dongxin Co., Ingenic Semiconductor, Montage Technology, as well as memory module manufacturers such as Deming Li, Shannon Xinchuang, and Longsys.

🌟Performance Over the Past Year

Since the beginning of 2026, the storage sector has been one of the strongest segments in the AI industry chain. In the US stock market, driven by AI infrastructure investment and demand for high-capacity storage, Seagate, Sandisk, and Western Digital have all surged significantly this year. Reuters reported in late April that Seagate and Western Digital had more than doubled year-to-date, while Sandisk's year-to-date gain was around 350%. Memory chip manufacturers also strengthened in tandem. Micron has risen sharply this year, while SK Hynix continues to benefit from the tight supply of HBM and capacity grabs by major clients. Its Q1 revenue grew 198% year-over-year, and operating profit surged 406% year-over-year, further strengthening its profitability.

Final Thoughts: Chips Rise First, Then Energy Catches Up, Storage Benefits Last

The first wave of AI realization is chips. The second bottleneck is energy. The third long-term beneficiary is storage.

A correct logic doesn't necessarily mean a comfortable entry point. Structural opportunities exist, but it's not about blindly chasing highs.

What truly matters isn't the hype itself, but which layer of the industry chain you are positioned on.

Disclaimer: The above is merely an industry chain review and does not constitute investment advice. Some targets, in particular, have experienced very significant gains since 2026; correct logic does not equal a comfortable buying opportunity.