SpaceXの富を追う「ブラインドボックス株主」:入れ子構造の果てに、裸で泳ぐのは誰か?

- 核心的な見解:SpaceXなどの有名企業による24年にわたる長期非公開期間は、巨大な私募セカンダリーマーケットを生み出した。その中で、多数のSPV(特別目的会社)が入れ子状に重なり、買い手は最終的な資産の真偽を確認できない可能性があり、「ブラインドボックス」的な取引を構成している。一方、企業側は株主数と規制リスクを管理するため、セカンダリー譲渡を段階的に厳格化している。

- 重要な要素:

- SpaceXの2026年のIPO評価額は1.75兆ドルに達し、その私募セカンダリーマーケットは2300億ドル規模に膨れ上がり、少なくとも170のSPVがその株式を巡って形成され、一部の入れ子構造は5層に及ぶ。

- SPVの各層で費用(例:6%の設立手数料+管理費)が発生し、実際の投資額は目減りする。さらに、最下層の買い手は自分の持ち分が実際の株式に対応しているかどうかを確認する権利を持たず、上位の仲介者に依存するしかない。

- 企業の非公開期間の長期化(1980年の平均6年から2024年には13年半に)により株式の転売が繰り返され、さらにSpaceX自身が優先購入権と買戻しを通じて取引を厳格に管理しているため、外部市場でのプレミアムが押し上げられている。

- 株主数が2000人を超えると財務諸表の公開義務が生じるという米国の規制線を回避し、ストックオプションの価格設定や経営情報のセキュリティを保護するため、Anthropic、Figure AIなどの企業は、無許可のセカンダリー取引を無効とすることを公に宣言している。

- SpaceXの上場書類には、初めて照合可能な株主名簿が添付される予定であり、その際に長年にわたる入れ子取引の合法性が試されることになり、一部のSPVの底辺に潜む「空箱」リスクが露呈する可能性がある。

A few days ago, the Wall Street Journal published a report about a hedge fund almost no one had heard of, named Darsana Capital.

Founded in 2014, this fund was modest in size. In 2019, it made a decision: to bet on a rocket company that had not yet gone public. That year, SpaceX's valuation was around $30 billion.

Seven years later, SpaceX is set to go public with a valuation of $1.75 trillion. Darsana's roughly $600 million invested over that period is now worth about $15 billion. This bet ranks among the most profitable single trades in hedge fund history on Wall Street. This single SpaceX position accounts for nearly 60% of Darsana's total assets.

SpaceX, the biggest IPO ever, also fires the starting gun for this year's wave of tech company listings. Stories like Darsana's are appearing frequently in the news. Google's $900 million investment in 2015 is now worth hundreds of billions. Founders Fund's $20 million lifeline in 2008 has ballooned to $19.5 billion.

But flip to other reports, and the picture changes completely.

At the end of March, both Bloomberg and Reuters reported on a peculiar situation: a group of investors bought SpaceX shares but couldn't confirm if they actually owned them. One of them, an entrepreneur named Tejpaul Bhatia, believed he held SpaceX stock but couldn't verify the authenticity of the shares supposedly belonging to him.

On one side, you have wealth creation myths precise to the billions; on the other, people who can't even confirm whether they bought anything. How can the same company and the same IPO create such a stark divide?

The Private Secondary Market Driven by "AI Anxiety"

Over the past two or three years, AI has pushed valuations in the primary market to absurd heights.

Companies like OpenAI, Anthropic, xAI, and SpaceX regularly command valuations in the hundreds of billions or even trillions of dollars, and they are still rising rapidly. Faced with these numbers, average investors have only one thought: I want a piece of that too.

There has never been a greater number of people wanting to get in. The trouble is, these companies are not public. For ordinary people, finding a way to buy in before the IPO is almost impossible.

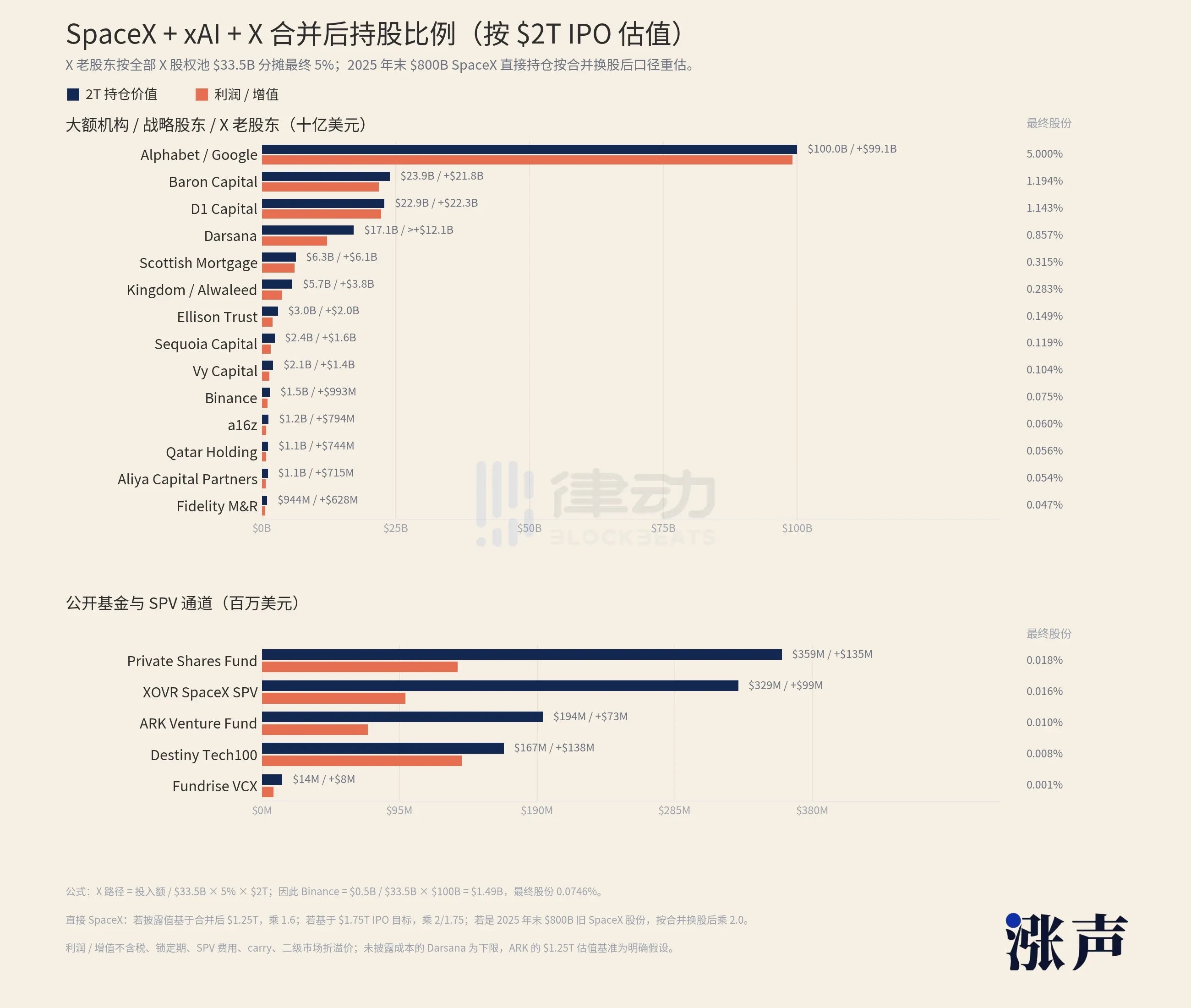

Just look at SpaceX's shareholder list. Large institutions and strategic shareholders hold tens or hundreds of billions of dollars' worth. Alphabet, Google's parent company, holds over a hundred billion by itself. Through all currently available public channels, a few ETFs and funds that hold SpaceX have a combined exposure of about $1 billion.

Based on a $2 trillion valuation, how much money could SpaceX's investment institutions make?

Moreover, most avenues keep ordinary investors out. Most channels in the private market are only open to accredited investors. In the US, this means an annual income exceeding $200,000 or assets exceeding $1 million excluding one's primary residence. Those who don't meet this threshold may not even be able to squeeze through that $1 billion crack.

For other things, such a disparity would be enough to make people back off. But FOMO works in the opposite way. The more scarce something is, the more you see others profiting, the more you want to force your way in.

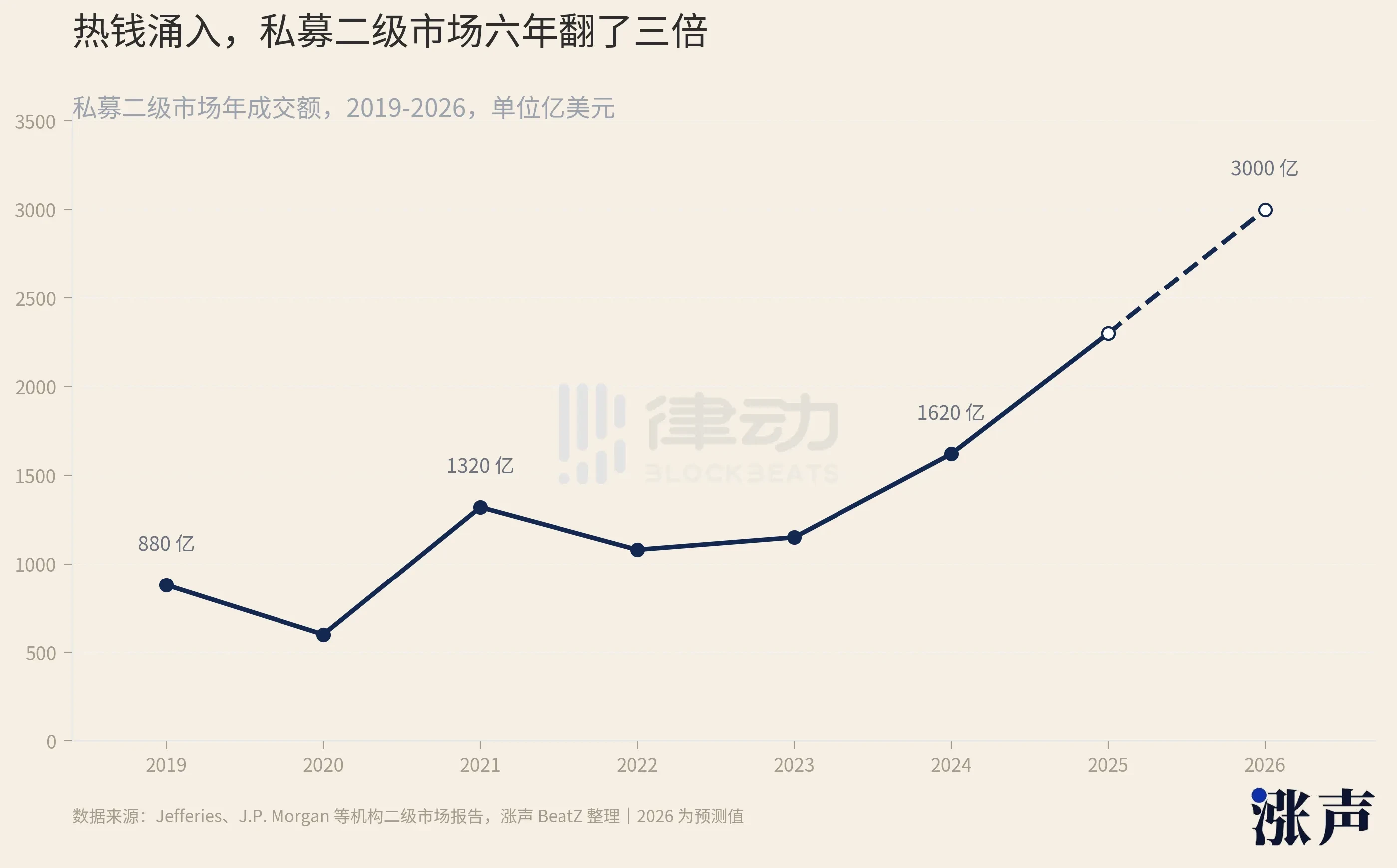

The money didn't retreat. It flowed into a place called the private secondary market.

This market specializes in buying and selling shares of unlisted companies. Early investors and employees who want to cash out, those who missed the early boat and want to get in, and the platforms, funds, and various vehicles that facilitate these transactions make up this market.

In recent years, its growth has been staggering. From 2019 to now, its size has tripled. Total transaction volume was approximately $162 billion in 2024, rose to around $230 billion in 2025, and is projected to reach $250 billion in 2026. The number of companies willing to open their shares for secondary transfers jumped from 12 to 31 within a single year.

As money poured in, sellers of SpaceX shares emerged.

How many emerged? According to a tally by the New York Times, there are at least 170 Special Purpose Vehicles (SPVs) that have purchased SpaceX shares. An SPV is a shell. Whoever can get their hands on a bit of SpaceX stock puts it into the shell, and then sells shares of the shell to subsequent investors. 170 shells, all surrounding the same company.

These shells come from all sorts of backgrounds.

In October 2025, an institution called Witz Ventures listed an SPV on the fundraising platform Republic, named The Cashmere Fund. This shell packaged three of the hottest targets—xAI, SpaceX, and Perplexity—to sell to retail investors. About 150 listeners of a financial podcast called Rich Habits, through a collective group purchase, also jumped the queue into SpaceX. Rapper 2 Chainz and SkyBridge founder Anthony Scaramucci have both publicly claimed to hold SpaceX.

Retired NBA player Tristan Thompson stated on a show that he invested in SpaceX when its valuation was $300 billion.

The problem is that this swarm of middlemen is a mixed bag.

One institution, Vika Ventures, collected $5.9 million from investors, promising to buy SpaceX shares. It was later discovered that the founder used the money to purchase luxury watches and a private jet. In 2023, another financial broker was sentenced to eight years for defrauding over 50 investors of nearly $6 million, also by selling pre-IPO shares of SpaceX and other companies.

Then there's Linqto, a once-popular platform specializing in star targets like SpaceX. It went bankrupt in 2025, and the SEC is investigating whether it properly verified users' accredited investor status, affecting over 13,000 investors.

Even if you don't encounter a scam, things aren't necessarily clear.

DataPower Capital is an institution dealing in SpaceX shares. Its founder, David Yakobovitch, told the New York Times that he only accepts trades one layer removed from SpaceX. "A few layers below that," he said, "things start to get murky."

Stacking Up to the Fifth Layer

Let's go back to those 150 podcast listeners from Rich Habits. They didn't buy SpaceX.

They bought into Witz Ventures, and Witz Ventures bought shares of DataPower Capital. DataPower is the one that actually got the stock directly from a shareholder on SpaceX's official register. This means an ordinary person placing an order after hearing a podcast is separated from the actual SpaceX stock by at least two or three layers of shells.

With each additional layer, two things happen simultaneously.

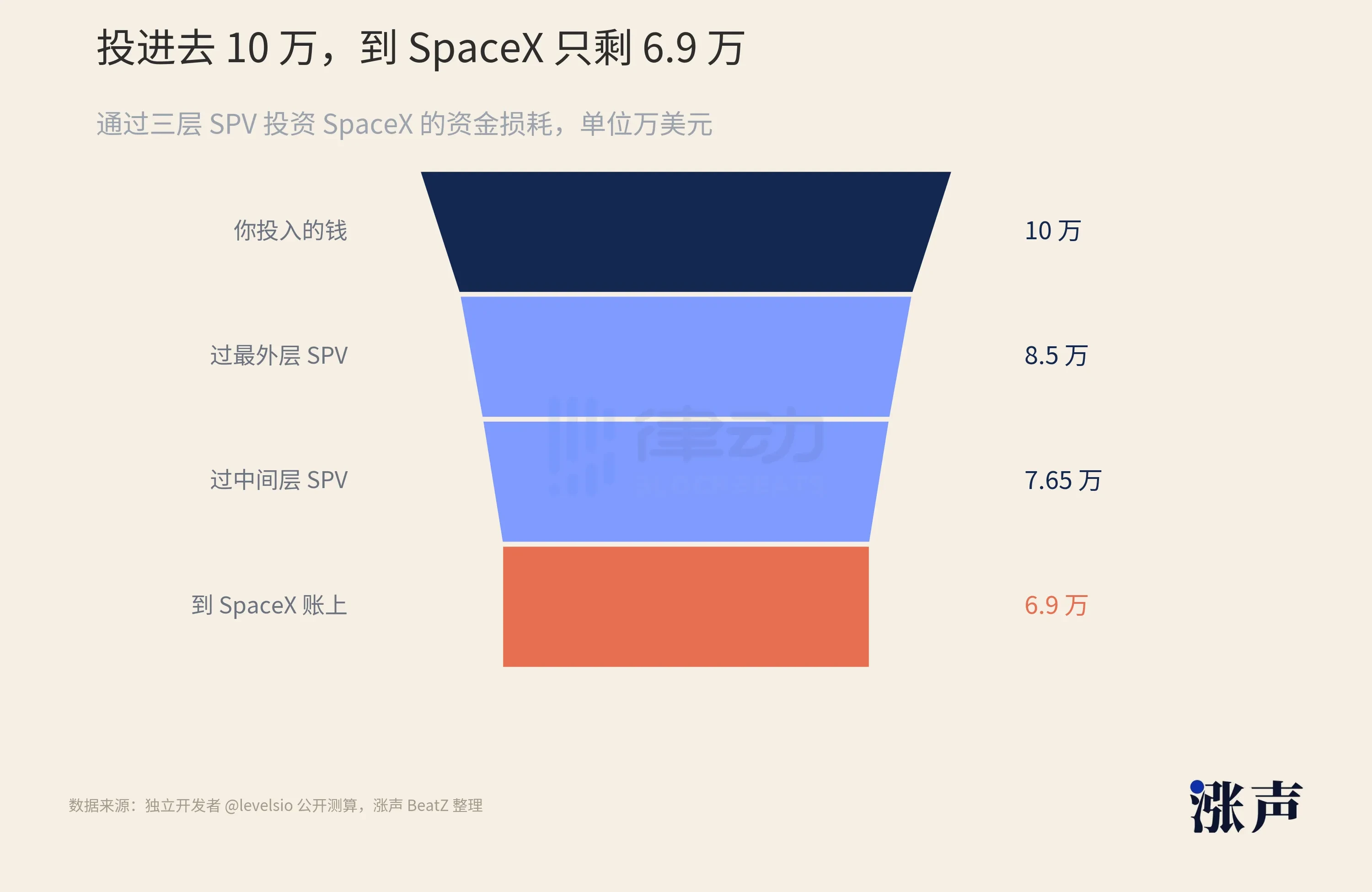

First, the money shrinks. Independent developer levelsio calculated online: suppose you invest $100,000 in SpaceX through three layers of SPV. The outermost layer charges a 6% setup fee, and the inner two layers each take management fees and profit shares. The money that actually reaches the bottom layer of SpaceX is only about $69,000. Before you even start to earn, 30% is already gone.

Second, the truth gets further away. A critical characteristic of this SPV structure is that investors in each layer can only see the layer directly above them. You buy the outermost shell, and its manager tells you it holds shares in a lower-layer shell. Is that lower layer real? Is there actually SpaceX stock underpinning it all at the bottom? You can't see, and you have no right to check.

Among those 170 shells, the deepest stacking reaches up to five layers. This is why people like Bhatia can't confirm their holdings. It's not because they aren't careful; the structure is designed precisely to prevent those outside the shell from seeing what's inside.

Why could the SpaceX nesting doll be stacked so deep?

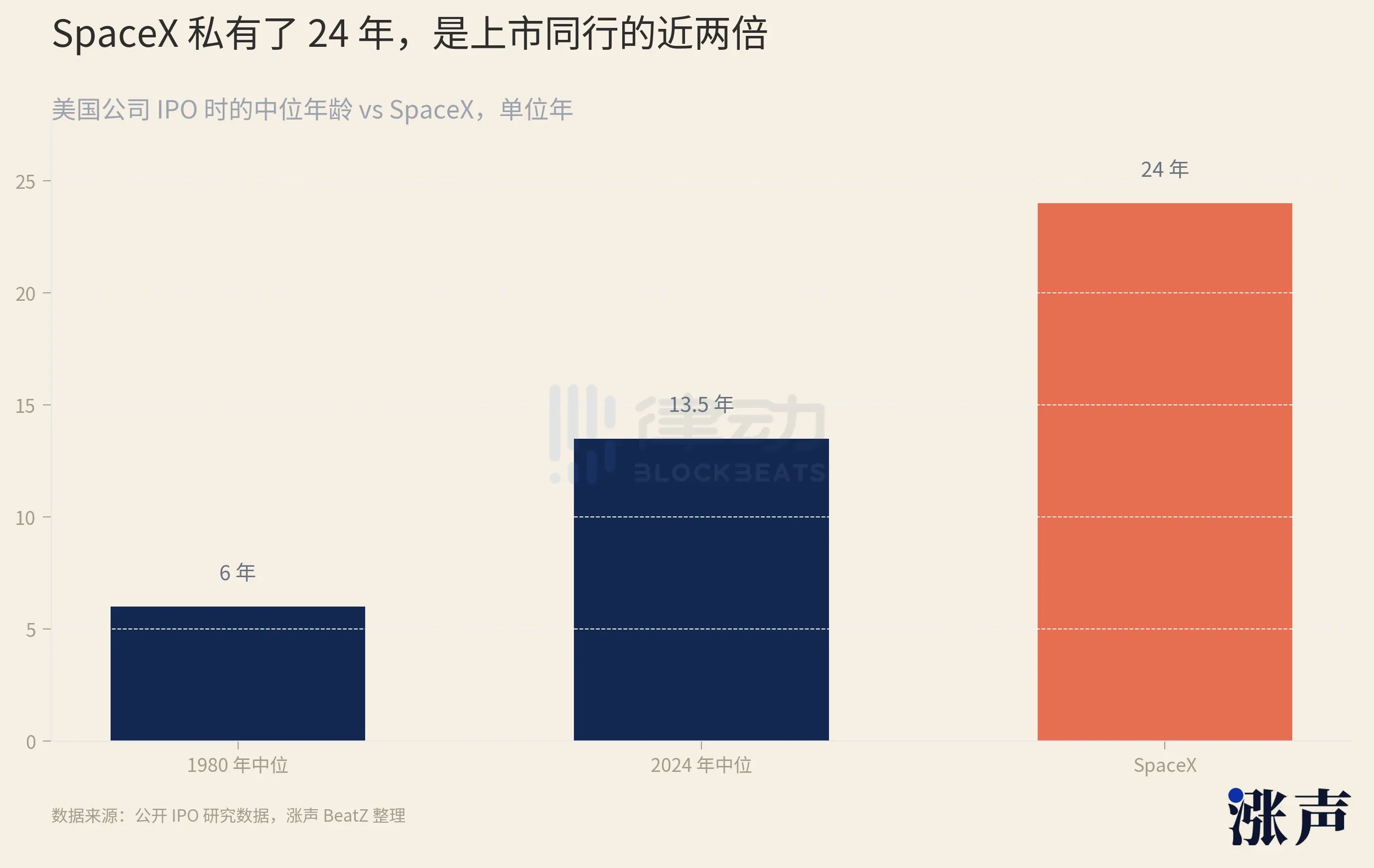

This comes down to how long it has been in the private market. Founded in 2002 and going public in 2026, SpaceX remained private for a full 24 years.

What does 24 years mean? The tech companies that went public in 1999 were, on average, only 4 years old. The class of 2014 averaged 11 years. More recently, the median age for a US company going public has stretched to 14 years. SpaceX's 24 years is an extreme on an already lengthening curve.

The longer a company stays in the private market, the more years its shares are traded, transferred, and wrapped in shells. SpaceX's shares have circulated in the over-the-counter market for over twenty years, inevitably accumulating layer upon layer of shells.

This lengthening private period isn't unique to SpaceX.

The median age of a US company at its IPO has risen from 6 years in 1980 to 13.5 years in 2024. The reason is simple: there's just too much money sloshing around in the private market.

As of 2023, global venture capital firms held over $650 billion in dry powder (uninvested capital). Companies don't lack financing, so they are in no rush to go public and face the quarterly earnings pressure and regulatory scrutiny of the public markets. Consequently, the number of billion-dollar unicorns keeps piling up. Globally, there are now over 1,500, worth a combined $6 trillion, and most haven't raised a round at a public valuation in over three years.

The longer a company stays private, the longer employees' and early investors' shares are locked up. For those wanting to cash out, the secondary market is the only exit. Demand builds up, and SPVs designed to meet this demand spring up in droves.

During the venture capital peak in 2021, the number of newly established SPVs in the US jumped 235% year-over-year. By Q3 2024, there were over 2,400 identifiable and operational SPVs alone. When a tool is used on such a massive and repeated scale for over twenty years, stacking shells up to the fifth layer is almost an inevitable outcome.

And SpaceX happens to be one of the tightest controllers of its stock in the entire private market. Externally, for nearly every share transfer, SpaceX exercises its right of first refusal (ROFR), intercepting the trade. It conducts a share buyback every six months, purchasing shares employees want to sell into its own controlled pool.

The tighter the door is welded shut, the higher the ticket prices outside it go.

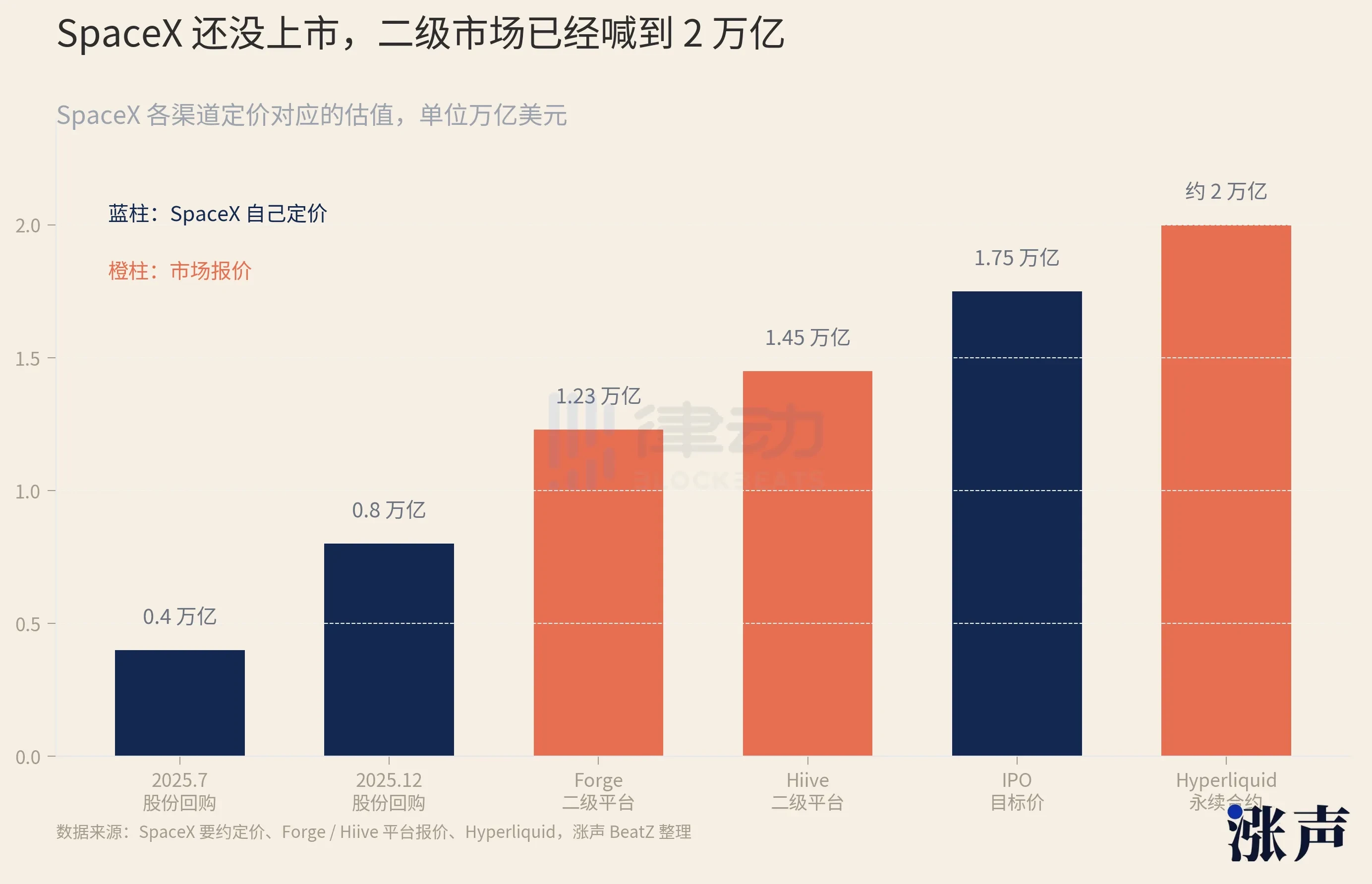

SpaceX's own pricing is known: a $400 billion valuation for its share buyback in July 2025; doubling to $800 billion six months later in December. But secondary market quotes had already run far ahead. Forge platform quotes implied ~$1.23 trillion, Hiive showed ~$1.45 trillion, and perpetual contracts on the crypto exchange Hyperliquid even implied over $2 trillion, higher than the listing valuation SpaceX itself aims for.

Another source of this tangled mess is mergers. In March 2025, Musk merged X, formerly Twitter, into his AI company xAI. In February 2026, SpaceX then completely acquired xAI. Those who bought Twitter and xAI back then, along with their entire system of shells, all got tied into SpaceX's shareholder register through two rounds of stock swaps.

Opening Blind Boxes

When nesting dolls reach this level, even the companies themselves get restless.

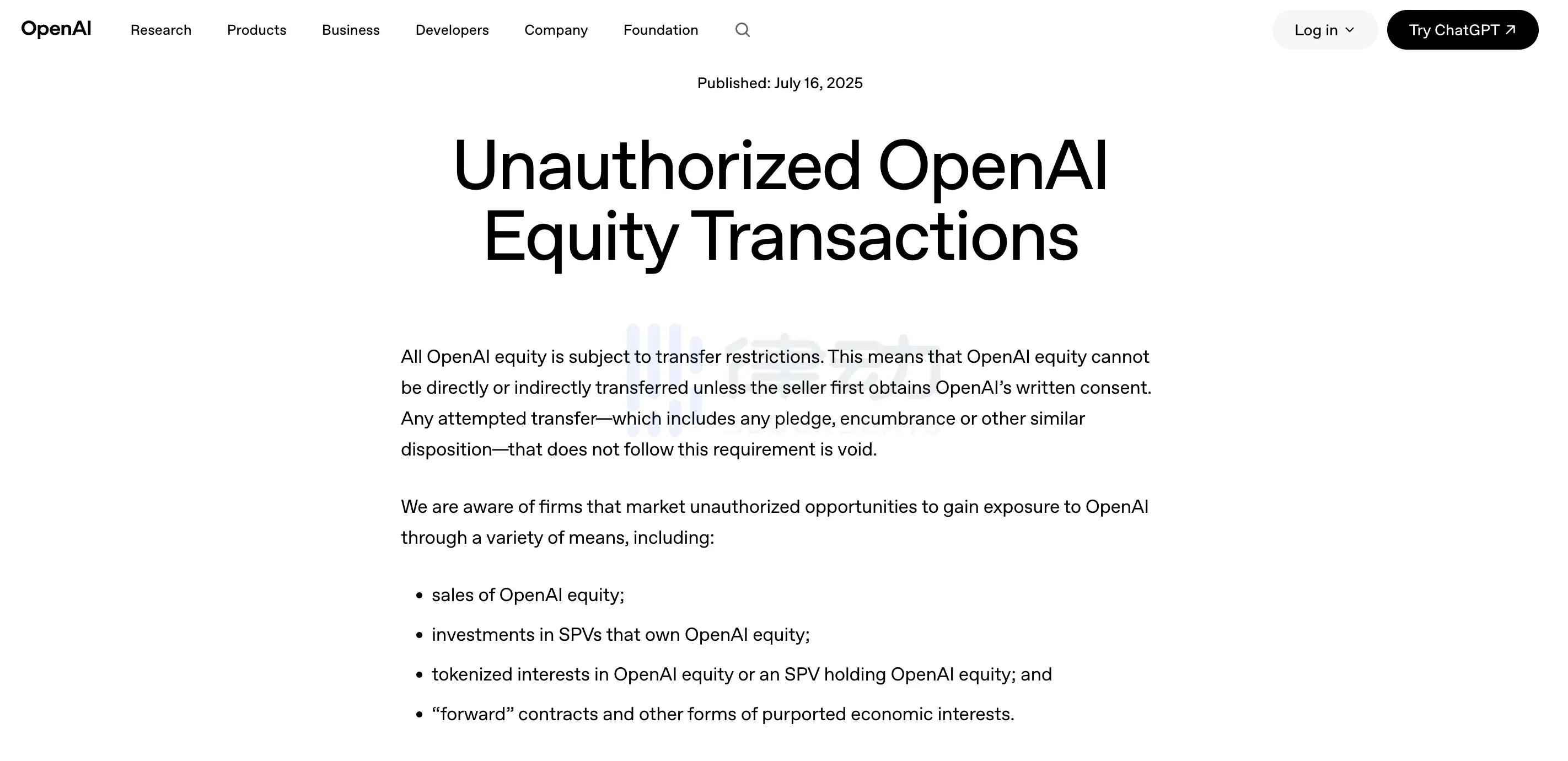

In May 2026, Anthropic and OpenAI issued public statements, clearly telling the market that any share transfers not approved by their boards are void and will not be recorded on their books. They named eight platforms, including Forge and Hiive, as unauthorized. The news caused related linked tokens on chain-based pre-IPO secondary markets to plummet, losing 30-40% of their value within a single day.

These announcements targeting secondary market transactions aren't just a whim of one or two companies.

Previously, robotics company Figure AI, upon news of a $39.5 billion valuation, also stepped in to block secondary trading of its shares. Almost all the hottest targets in the private market—Anthropic, SpaceX, Anduril, Stripe, Databricks—are doing the same thing: turning their tolerance for secondary trading down to zero.

Why did they all turn hostile simultaneously?

This leads to a "red line" for going public that usually goes unnoticed. Under US rules, if a company has more than 2,000 shareholders, even if it's not public, it must disclose its finances periodically like a public company. Nesting doll SPVs make it impossible for a company to count its total shareholders. One SPV counts as one on the register, but it might represent hundreds of people behind it. If a company inadvertently crosses the 2,000-shareholder line, it is forced to open its books.

Another reason involves pricing employee stock options. If a company's shares are freely traded on the secondary market and driven up to high prices, the company cannot ignore that number when setting the exercise price for new employee options. The crazier the secondary market, the less valuable employees' options become.

More critically, it's about information. Shareholders legally have the right to obtain company operating information. For AI companies, model architecture, training data, and compute allocation are their most closely guarded secrets. When a company can't even count its own shareholders, it can't be sure who this information is flowing to.

Cleaning up the countless shareholders, protecting option pricing, and closing information leaks—each of these issues individually is not new. But when the secondary market balloons to $230 billion and nesting dolls reach five layers, companies realize they can't control it through private handling alone. So they step into the spotlight, writing "Your shares are invalid" as a public announcement for the first time. SpaceX didn't follow with a similar statement, but its ROFR mechanism achieves the same thing.

This "invalid" declaration from the companies leaves those multi-layered shells hanging in the air. You bought an SPV and paid the money. Whether the underlying SpaceX stock was ever approved or is valid—nobody can give you an answer until the company's records are publicly reconciled.

Thus, buying a SpaceX SPV increasingly feels like opening a blind box.

When the box opens is fixed. On June 12th, when SpaceX rings the bell on the Nasdaq, its IPO filing will reveal a public, verifiable shareholder list for the first time. Every shell wrapped around its stock over the past twenty-something years will have to be reconciled at that moment. If they match, the box contains real stock; if not, it's a worthless piece of paper. On this day, Bhatia will find out which type he drew.

But after SpaceX comes OpenAI, then Anthropic, and a long list of names queuing up. Just scrolling through your social feed, you can easily see "proxy investment" posts for these hottest AI companies.

In recent years, AI has created a flood of hot money with nowhere to go. The truly worthwhile investment targets are few, and they are all tightly locked up. With too much money and too narrow a door, countless shells grow in the middle.

As long as this imbalance persists, the private secondary market will remain as it is now: a blind box that everyone wants to play, but where no one can really say what they've drawn.