让市场本身上链:Canton Network正悄然成为机构金融的新底层

- 核心观点:全球支付巨头Visa以最高权重加入Canton Network成为超级验证人,标志着传统金融对隐私保护型区块链基础设施的认可从实验阶段进入生产准备期;Canton Network通过数据可见性控制等差异化设计,正成为受监管金融机构开展链上业务的核心基础设施。

- 关键要素:

- Visa首次提交区块链治理提案,3天内获批并以最高10级权重加入Canton Network,体现传统金融对该网络的深度信任与合规审核的完成。

- Canton Network核心差异化在于将数据可见性控制内置于L1协议层,仅交易参与方可见细节,解决银行对隐私缺失的顾虑,使受监管机构能安全开展业务。

- 链上月处理量超9万亿美元,真实运作传统金融业务(如代币化回购、国债结算),而非虚假刷量;摩根大通JPM Coin、DTCC国债代币化为旗舰用例。

- 代币CC为零预挖、零团队分配、零VC份额的“网络效用资产”,价值锚定于链上真实金融活动量,减少机构对筹码不公平的顾虑。

- Canton Network验证人名单包括高盛、摩根大通等“老钱”机构,由华尔街出身团队Digital Asset打造,目标是在合规框架内复刻传统金融成功。

- Visa加入旨在实现原子化结算:买方付款与资产交付同步完成,消除时间差与对手方风险;Canton在资本市场侧已有布局,支付侧获机构锚点。

Original: Odaily Planet Daily (@OdailyChina)

Author: jk

1. A Proposal Approved in Three Days

On March 20, 2026, Visa, the globally renowned payment service provider whose logo appears on most bank cards, submitted a governance proposal to the Canton Network. According to a report from The Block, just three days later, the proposal was approved, and Visa officially became a Super Validator on Canton with the highest weight level 10 (Super Validator Weight 10). This marks the first time Visa has submitted a blockchain governance proposal.

Within the crypto sphere, this might appear as yet another incursion by traditional finance. However, if you are sufficiently familiar with the legal and compliance processes inside traditional institutions like Visa, you would realize that a three-day approval is highly unusual. The premise for Visa's compliance team submitting this document undoubtedly carried the caution and seriousness of the traditional financial world. Securing the highest weight level indicates that negotiations and due diligence were fully completed beforehand. The proposal seen by the public is likely the result of months of collaboration between traditional finance and the crypto world.

Rubail Birwadker, Head of Global Growth Products and Strategic Partnerships at Visa, stated: "Many banks see the lack of privacy as the biggest barrier to migrating meaningful business onto the chain. By becoming a Super Validator on the Canton Network, we bring Visa-level trust, governance, and operational standards to this privacy-preserving blockchain infrastructure, allowing regulated financial institutions to move payment operations onto the chain without disrupting their existing operations."

As we can see, Visa's entry is an endorsement of an already mature institutional network, not a starting point.

Since 2017, each market cycle has seen a batch of traditional financial institutions loudly announce their "exploration of blockchain," but very few end up with real-world business applications. This time, Visa has chosen to enter the blockchain's governance layer, holding voting rights and participating in infrastructure decisions. Eric Saraniecki, Network Strategy Lead at Digital Asset, co-founder of the Canton Network, said in a statement: "Visa's participation confirms that this technology has moved from the experimental stage to a production-ready stage."

Driven by curiosity about this collaboration, Odaily Planet Daily interviewed the Canton Network team. What exactly facilitated this partnership? And what made Canton, a long-quiet project, the chosen one?

2. Not More Assets On-Chain, But the Market Itself On-Chain

To understand why Canton can attract Visa, we need to first look at the core differences between Canton and other chains.

Ethereum and Solana solve the problem of: How to get more people involved, how to bring more assets on-chain. Canton solves the problem of: How financial institutions can conduct business normally on-chain. While the focus seems different, at the specific design level, their trade-offs are almost entirely opposite.

Ethereum's global transparency is an advantage for retail investors but an obstacle for institutions. Take a specific example: In a bank's foreign exchange trading desk, if every buy/sell order for USD or EUR is visible in real-time, counterparties can immediately adjust their quotes based on this information, significantly increasing the bank's trading costs. If a market maker's positions and hedging operations are all public, competitors can simply trade in the opposite direction, squeezing out profit margins. Repurchase agreements between institutions involve the fund positions and collateral sizes of both parties. Leakage of such data poses risks to the entire institution's liquidity management. These restrictions have little to do with regulation directly; they are dictated by basic business logic.

Even without a link between addresses and real-world institutions, transparent on-chain transactions alter the logic of the entire secondary market. No traditional financial institution wants its trades to be front-run. Therefore, designs like Ethereum and Hyperliquid are not optimal for large institutions.

Canton's approach incorporates data visibility control into its design.

This approach embeds the selective disclosure of data itself into the protocol layer as a native L1 design, rather than relying on patching at the application layer. Specifically, only the direct participants of a transaction can see its details; the network validates the transaction without exposing any sensitive data. Two banks can conduct cross-border settlements on the same shared infrastructure, with the transaction being completely invisible to all unrelated parties. Competitors can interact on the same network without their respective positions and strategies being exposed.

We also inquired about the relevant technical details. Canton's response was: "Canton separates the coordination layer (shared across the network) and data visibility (limited to participants), achieved through isolated execution environments and selective synchronization. This allows institutions to trade securely and competitors to interact without exposing their positions or strategies. This is the mechanism that enables the market itself, not just assets, to operate natively on-chain."

The Canton Network told us that the summary of this design logic is: Data visibility control is foundational, not an add-on feature.

So, why does the list of Canton validators look like a gathering of old money: Goldman Sachs, JPMorgan Chase, BNP Paribas, Citibank, Bank of America, DTCC, Nasdaq, Broadridge, Tradeweb… These institutions join because this infrastructure allows them to replicate the successes of traditional finance, and thus liquidity gradually flows in.

Canton's Super Validator list

3. Born on Wall Street, Slow and Steady Wins the Race

Canton's creator is Digital Asset Holdings, founded in 2014 by Blythe Masters. Blythe Masters, a former star executive at JPMorgan Chase and a key pioneer in the CDS field, has deep connections and industry credibility on Wall Street. From day one, this company was not building blockchain products for retail investors; its target clients were strictly regulated financial institutions with real balance sheets that need to operate within legal frameworks.

Regarding its background, we asked a pointed question: We saw the launch of Canton in 2023. Why did it take until this year for a full-scale launch?

Canton's answer: Slow and steady wins the race.

Its Wall Street origins dictate the pace of the entire project. Canton admitted in the interview that this chain took longer than other L1s to reach its current state because it has been dealing from the start with regulated financial systems, building institutional trust, and figuring out how to genuinely integrate into markets with real business activity.

This rhythm is completely opposite to the mainstream narrative of Web3. Most public chains pursue rapid launch, rapid ecosystem expansion, and rapid hype generation, launching a TGE and then "the team isn't really sure what's next." Canton's path has been one of step-by-step negotiation: first securing DTCC, then Goldman Sachs, then JPMorgan Chase, then Visa, using their endorsements to attract actual business.

2026 is a turning point, not because of project marketing itself, nor because this crypto bear market is shaking things out, but because, beyond the narrative, the infrastructure has, for the first time, truly met institutional requirements: there is real balance sheet activity running on it. This is why now is the best time to focus on the Canton Network.

"So, how much business has been brought in?" we continued asking.

4. Canton's On-Chain Activity

Canton's current data is an outlier in the entire blockchain industry, and the nature of these figures is very different from most public chains. Currently, the Canton Network processes over $9 trillion monthly, with tens of millions of daily transactions, and the number of ecosystem participants has grown by orders of magnitude over the past three years. These figures correspond to traditional financial operations: tokenized repos, treasury settlements, and cross-institutional collateral movement. These are not farmed volumes but real operations on institutional balance sheets.

We also asked which products are currently mainstream on the chain. Currently, there are several flagship products:

JPMorgan's JPM Coin: In January 2026, JPMorgan's Kinexys division announced the native deployment of JPM Coin onto the Canton Network. JPM Coin differs from USDT and USDC; it is a deposit token representing a direct claim on JPMorgan Chase deposits, operating within the existing bank regulatory framework. For example, two institutions settling a cross-border transaction using JPM Coin on Canton is essentially the same as what they do in the traditional system, but the settlement speed is much faster, and operations are no longer limited to business days. Kinexys currently processes an average daily transaction volume between $2 billion and $3 billion, with a cumulative total exceeding $1.5 trillion since 2019, and this flow of funds will soon be operating on Canton.

DTCC's Tokenization of US Treasuries: In December 2025, the US securities depository DTCC announced a partnership with Digital Asset to tokenize a portion of its custodial US Treasuries on Canton, aiming for a first version in a controlled production environment in the first half of 2026, with expansion based on market demand thereafter. DTCC also co-chairs the Canton Foundation alongside Euroclear, directly participating in network governance.

DTCC processes securities transactions valued at over $2 quadrillion annually, forming the core of the clearing and settlement system for the entire US capital market. To use an intuitive analogy: DTCC's status in traditional finance is like the central bank; no one deposits money there, but everyone's stock and bond transactions must go through its backend infrastructure. Traditional repo markets only operate on business days; after Friday afternoon, you have to wait until Monday. But on Canton, repo transactions can run 24/7, using on-chain US Treasuries as collateral, enabling real-time fund intermediation across institutions, time zones, and weekends.

So, what will Visa do on Canton?

A core goal described by Canton in the interview is atomic settlement: the buyer's payment and the seller's delivery of assets are completed in a single operation, without requiring two steps or relying on an intermediary to bridge them. For example, currently, when an institution buys a batch of bonds, the transfer of assets and the settlement of cash are often two separate processes, creating time lags, counterparty risks, and costs for manual reconciliation. Canton aims for these two things to happen simultaneously, locked in one step with no time gap. To achieve this, capital market infrastructure and payment infrastructure must both be on-chain. Canton already has a solid presence on the capital market side, and Visa's participation provides a true institutional anchor on the payment side.

Beyond this, it also includes things blockchain excels at, such as real-time cross-border capital flows and embedding programmability into financial transactions.

Canton believes that 2026 is the cycle where infrastructure has truly met institutional requirements for the first time, which is why an institution like Visa is choosing to engage with blockchain infrastructure now.

Other Use Cases Already Running

Tokenized repos are currently the most mature scenario. Repurchase agreements (Repos) are the most common short-term financing tool between financial institutions. Simply put, Institution A sells bonds to Institution B for cash, agreeing to buy them back in a few days. Traditionally, this process can only be carried out during business hours on working days, and there are delays in fund settlement. Tokenized repos on Canton are already available 24/7 with instant settlement. Several top-tier institutions have already conducted real cross-institution repo transactions covering weekends on Canton.

Collateral mobility is another scenario with real demand. Large financial institutions often need to move collateral from one account or institution to another, e.g., moving bonds held at Institution A to Institution B to meet margin requirements for a derivatives trade. Traditionally, this process takes days, during which the assets are locked and unavailable for other uses. Canton's settlement model allows this process to be completed near-instantly.

Digital bond issuance is another area where Canton holds an advantage. Canton mentioned in the interview that it currently accounts for over half of the global digital bond issuance market. The reason is that Canton offers complete Delivery versus Payment (DvP), bond lifecycle management, and multi-party coordination, allowing bonds to have a complete lifecycle on-chain from issuance to settlement, rather than just tokenizing the asset and relying on off-chain processes to finish.

Stablecoin settlement is an area accelerating with Visa's involvement, aiming to enable stablecoin payments between institutions on the same compliant infrastructure with data visibility control, rather than routing through public chains.

Simply put, RWA wasn't explicitly mentioned, but every point spoke to the needs of RWA.

Canton also gave a general outline of the upcoming roadmap in the interview: In the medium term, corporate bonds, private credit, and trade finance will follow; in the longer term, equities are also on this path. The logic is consistent from existing use cases to this roadmap: asset classes with higher liquidity and more mature regulatory frameworks will move first.

5. What Does the Token CC Represent?

For broader market participants, understanding what the CC token is remains an unavoidable question.

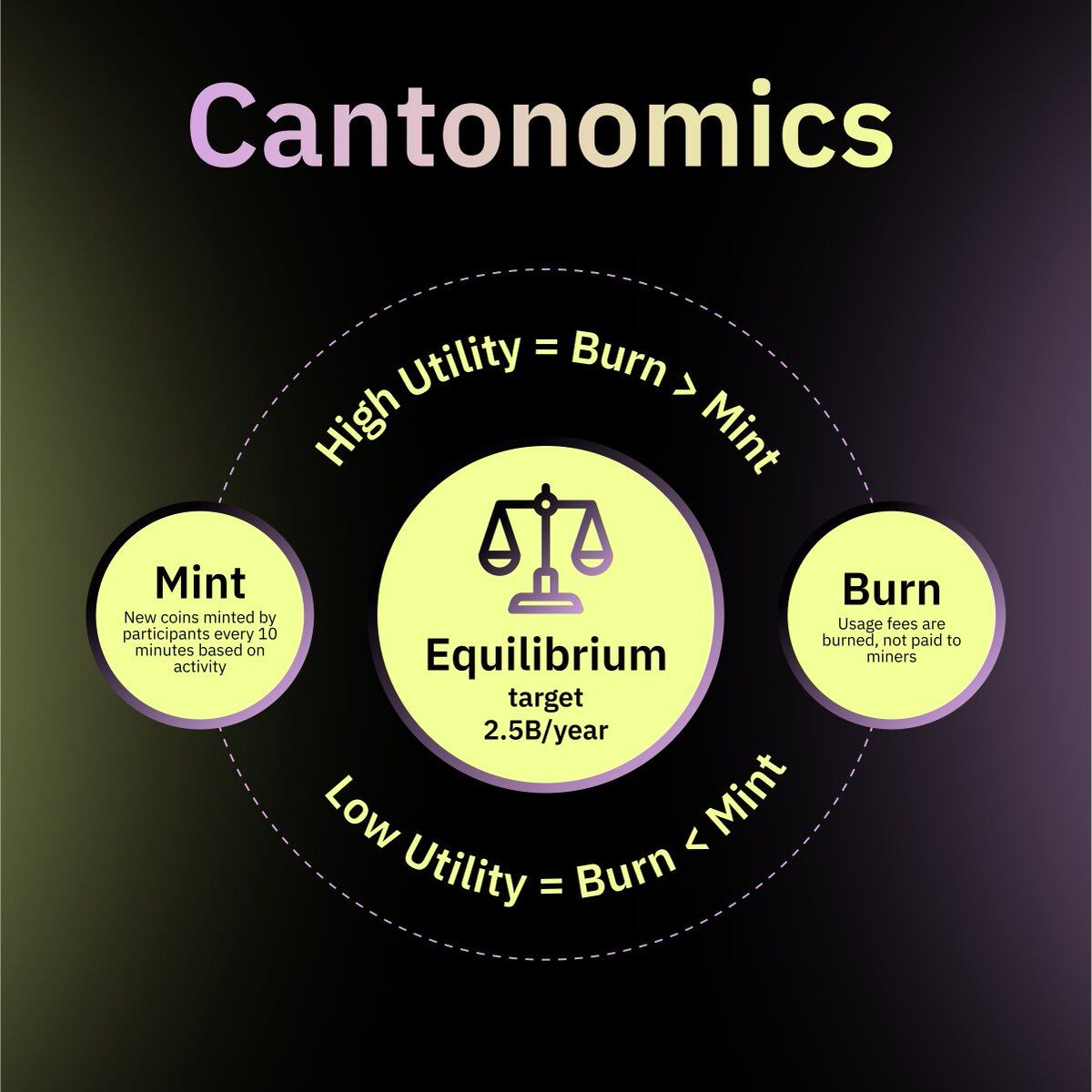

Canton's characterization in the interview was quite direct: CC is a "network utility asset," its value pegged to the volume of real financial activity occurring on the network.

This means demand comes from actual usage; the more transaction volume institutions have on Canton, the more CC the network consumes. The long-term drivers for the token include institutional transaction flow, stablecoin settlement scale, total on-chain asset value, and the depth of interoperability between Canton and other networks.

CC has a token distribution feature quite rare in the Web3 space: zero pre-mine, zero team allocation, zero VC shares, with all tokens entering the market through fair mechanisms. For institutional participants, this setting reduces concerns about someone holding ultra-low-cost tokens ready to dump on the secondary market; the rules are transparent and equal for all participants.

For ordinary market participants, Canton exists more as backend infrastructure. The average person is more likely to interact with it through exchanges, wallets, or financial platforms rather than directly interfacing with the protocol. The improvements it brings—like faster settlement speeds, tighter bid-ask spreads, and better financial product terms resulting from reduced operational costs—will gradually trickle down to end users through product layers, rather than in a directly perceptible way.

6. The Next Steps

Canton's 3-to-5-year goals outlined in the interview are not measured by on-chain TVL or token price. Looking at the specific goals listed by Canton: Stablecoins becoming the standard means of inter-institutional settlement, much like SWIFT wire transfers are the standard today; major financial institutions operating loans, deposits, bond issuances, and product packaging directly on-chain; cross-border capital flows moving near-instantly instead of the days-long settlement cycles in the traditional system; multiple asset classes being natively issued and settled on Canton, rather than being issued off-chain first and then manually synced to the chain.

Canton uses the term "invisible" to describe its ideal state: By that time, Canton would just be one of the underlying protocols silently driving global finance, much like TCP/IP is to the internet today or SWIFT is to cross-border payments. Users would be unaware of its existence, but nothing would work without it.

Of course, the road is still long. Regulation is highly fragmented across jurisdictions; what is compliant in Europe is completely different in Asia. Integrating with existing legacy systems is extremely difficult; banks cannot migrate core systems used for decades overnight. Interoperability between different blockchain networks remains an unresolved technical issue. Coordinating institutions on the same infrastructure involves complex power dynamics. The Canton team did not shy away from these issues in the interview, telling us: The technological bottleneck is no longer the biggest problem; the real challenge is how to achieve global rollout.

As we can see, changes in financial infrastructure never happen overnight. SWIFT was established in 1973 and took nearly two decades to become the true standard for cross-border settlements. People use it today without thinking about its origins. The current position of Canton is likely the stage where "nobody has realized what it will become yet." But for something that truly aims to be infrastructure, being forgotten might just be what success looks like.