都是誰在使用Trade.xyz進行交易?

- 核心觀點:對Trade.xyz的鏈上分析發現,該平台確實存在大規模女巫錢包(佔總數44%),但它們僅貢獻了0.77%的交易量;真正支撐超過500億美元月交易量的核心力量是少數專業做市商(如Jump、Selini、Wintermute)、出身Bybit的套利機器人,以及一個與Polymarket高度重疊的散戶群體。

- 關鍵要素:

- 女巫層與交易量脫鉤:35,453個女巫錢包可追溯到同一Polymarket帳號「Themino」,採用接力式小額雙向交易策略,但累計交易量僅約4億美元,佔總量的0.77%。

- 高度集中的做市商力量:363個做市商錢包(佔0.46%)推動了63%的總交易量(3,275億美元),其中前5名佔據了做市量的一半,包括Powell、Jump Crypto、Selini和Wintermute。

- 專業套利機器人(SAT)主導激進交易:522個HFT機器人貢獻了6.7%的交易量,前4名佔據了該類別89%的份額,且大部分資金來源可追溯到Bybit交易所。

- 散戶群體與Polymarket高度重疊:在交易量最高的400個散戶錢包中,22%的交易量(163億美元)來自可識別的Polymarket用戶,表明預測市場用戶是核心交易驅動者。

- 演算法交易增加真實流動性:Tread.fi等演算法產品透過掛maker單刷分,為傳統做市商缺席的時段(如夜間、週末)提供了盤口頂部深度,結構上區別於女巫洗單。

Original Title: "Who is actually trading on Trade.xyz?"

Original Author: @web3_pastel, Arrakis Finance

Compiled by: Jaleel, BlockBeats

Editor's Note:

On the Hyperliquid landscape, one of the most unavoidable names for 2026 is Trade.xyz. It was the first product to truly take off after the launch of the HIP-3 "permissionless perpetual market deployment framework," moving assets like US stocks, crude oil, and silver – traditionally confined to traditional financial hours – onto a 24/7 on-chain order book.

In just a few months, it evolved from a niche experiment with only the XYZ100 index into an on-chain trading venue hosting multiple markets including oil, Tesla, and silver, with a monthly trading volume exceeding $50 billion.

However, its controversies have also sparked considerable discussion online: among those impressive wallet numbers, how many are real people, and how many are Sybils mass-created in anticipation of a yet-to-be-issued token?

Arrakis' research presents a rather interesting result: the Sybil layer does exist, with over thirty thousand wallets traceable to a single Polymarket account, "Themino"; however, it inflates user count, not dollar volume. The trading volume is truly driven by a few professional market-making desks, several taker bots with origins at Bybit, and a long tail of retail investors heavily overlapping with the Polymarket user base.

The following is the full text:

Summary

When we wrote our first piece, "Who's Trading on HIP-3?", our attribution method was statistical. We classified wallets based on their trading behavior over the previous three months: addresses primarily placing limit orders were categorized as market makers, high-frequency takers as arbitrageurs, and orders with low fill rates and builder tags as retail. This approach did reveal some interesting market structure characteristics, but the classification was probabilistic, and approximately 70% of wallets remained unclassified.

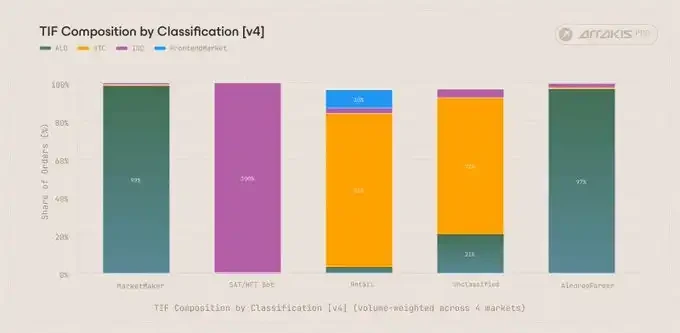

This article replaces statistical inference with mechanical classification. Every order on @HyperliquidX comes with a set of deterministic tags signed and published by the exchange itself: time-in-force (ALO, GTC, IOC, FrontendMarket), builder code, fill status, and holding time. We used this order metadata to classify each wallet into one of four categories: Retail, Market Maker, Arbitrage Bot, and Airdrop Farming Account.

The second step was identifying the wallets behind these categories, extracting identity and trading behavior data from the APIs of @arkham and HyperTracker. The top 450 wallets accounted for 78% of the total trading volume. Within this group, we identified several @Polymarket-associated accounts, @jump_, @SeliniCapital, @wintermute_t, Abraxas Capital, and others.

Through this two-step classification method, we observed several patterns. These are detailed below.

Trade.xyz Wallet Analysis

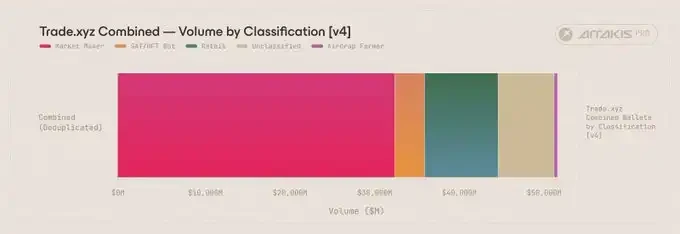

Our observation window spanned 21 days, from March 10, 2026, to March 31, 2026. During this period, @tradexyz's four markets (xyz:CL crude oil, xyz:SILVER silver, xyz:TSLA Tesla, xyz:XYZ100) recorded 79,622 unique participating wallets, with a total trading volume of $51.95 billion.

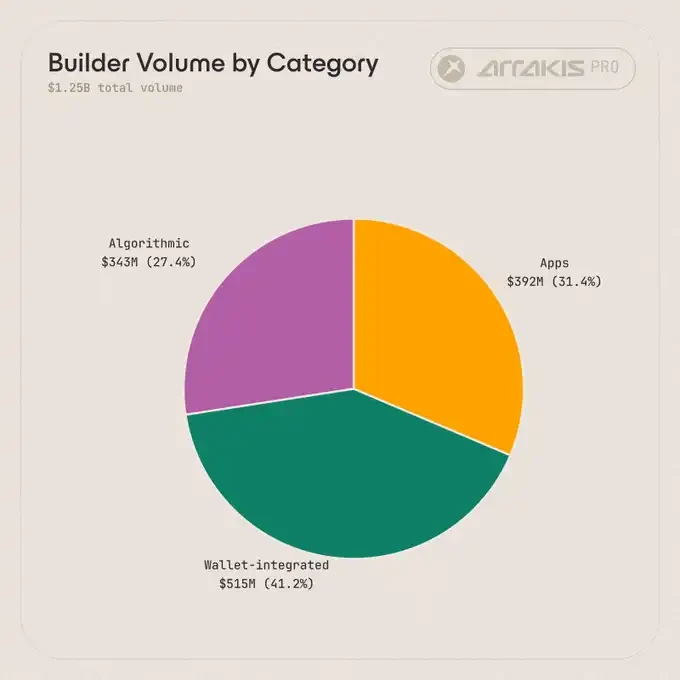

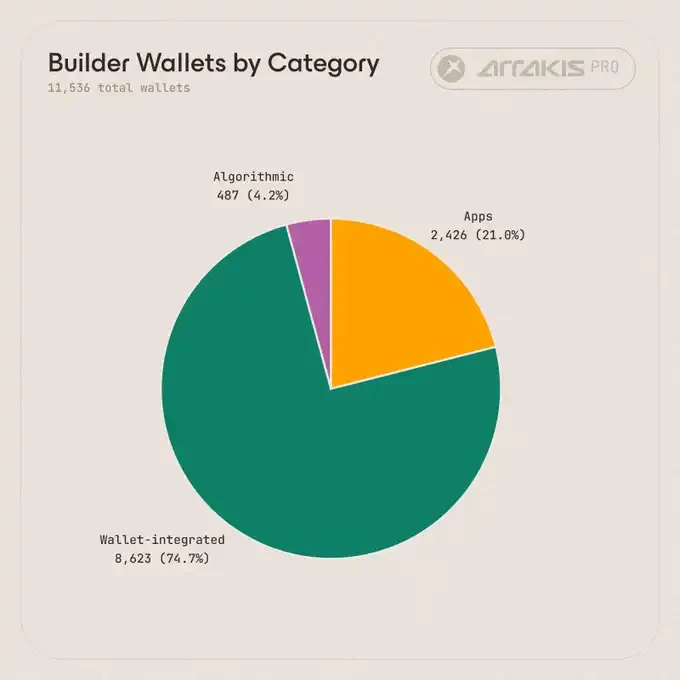

79,622 participating wallets broken down by volume. Market makers, though less than 0.5% of wallets, accounted for 63% of every dollar traded.

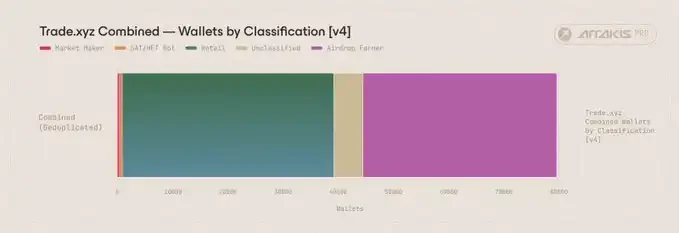

Classification by wallet count (not volume). The Airdrop Farming Account category alone had 35,091 wallets, nearly half of the identified wallets.

The Airdrop Farming Account category is one of the largest by wallet count but smallest by volume share. 35,091 wallets represent 44.07% of total wallets but generated only $400 million in volume during the entire window, a mere 0.77% of the total $51.95 billion volume on the exchange. Nearly half of the active wallets on Trade.xyz contributed less than 1% of the total volume.

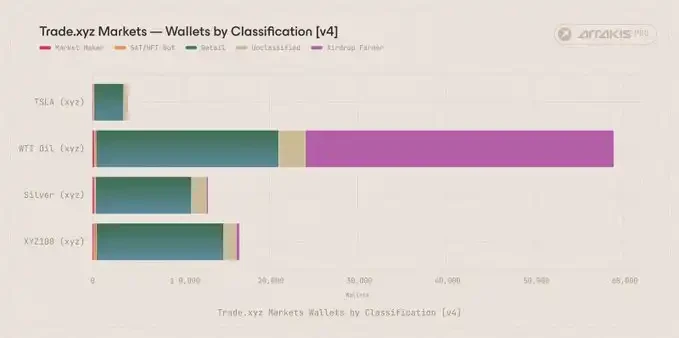

Breaking it down by market reveals another distinct pattern.

Wallet distribution by market. xyz:CL attracted 99.3% of airdrop farming accounts, likely due to its optimal execution costs.

Of the 35,091 airdrop farming wallets, 34,859 (99.3%) traded xyz:CL during the window, with the remaining 232 scattered across xyz:SILVER, xyz:TSLA, and xyz:XYZ100. This pattern aligns with airdrop farming behavior: each wallet repeatedly executes small, two-sided trades to generate volume without bearing price risk. This strategy relies on tight execution costs and is extremely sensitive to slippage. xyz:CL, having the best depth among the four Trade.xyz markets, naturally became the preferred venue for this activity.

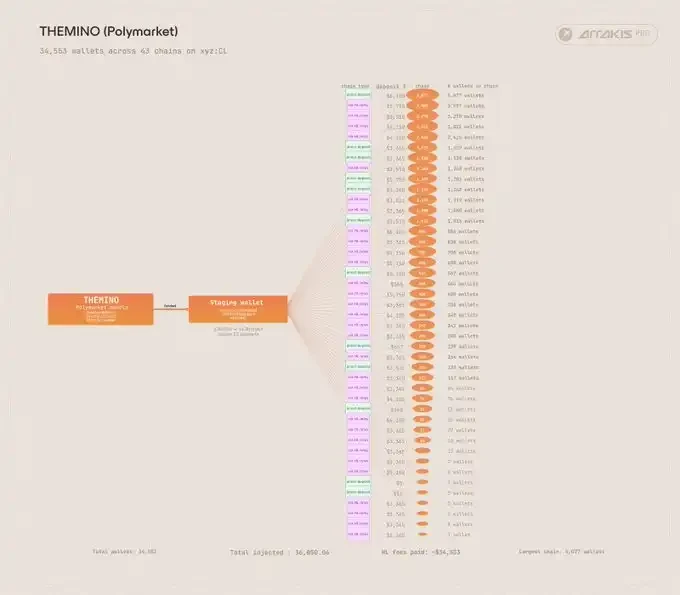

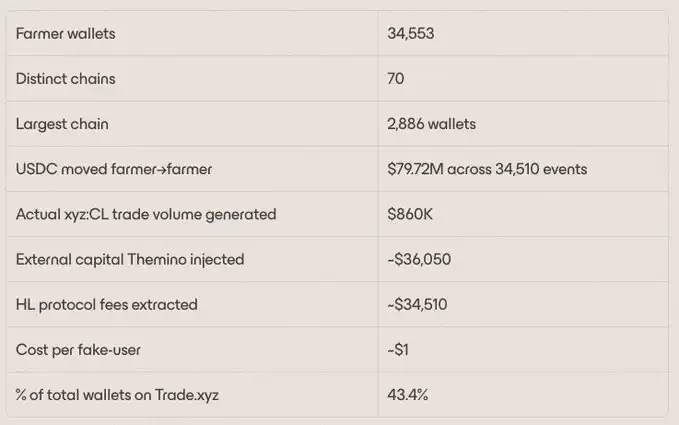

Another notable observation is who is behind these addresses. On-chain tracing, detailed below, shows that 34,553 airdrop farming wallets are linked to the same Polymarket operator. This single entity accounted for 43.4% of all participating wallets on Trade.xyz during this window.

On the other end of the spectrum are market makers. 363 wallets, representing 0.46% of active addresses, drove $32.75 billion in volume during the window – 63% of every dollar on Trade.xyz. The other three categories fall in between. 522 SAT/HFT bots contributed $3.5 billion (6.7%). 38,307 wallets classified as retail contributed $8.7 billion (16.7%). 5,339 unclassified wallets contributed $6.61 billion (12.7%).

The 12.7% volume in the unclassified category cannot be qualitatively assigned to a specific strategy based solely on metadata. A reasonable assumption is that a significant portion comes from retail users placing limit orders via the Hyperliquid frontend, or placing market and limit orders via the Trade.xyz frontend. Neither channel attaches explicit builder codes or specialized TIF tags to the orders, making these fills invisible to a metadata-driven classification method.

Time-in-force distribution weighted by order count per category. Unsurprisingly, 98.5% of market maker orders are ALO, while arbitrage bots use 100% IOC. The unclassified category has 71.5% GTC, a hallmark of manually placed limit orders from frontend users.

The TIF composition supports this hypothesis: 71.5% of orders in the unclassified category carry a GTC (Good Till Cancel) TIF tag, typically used when frontend users place resting limit orders.

"Themino," Uncovering Over 30,000 Wallets

In recent weeks, there's been much debate: is Trade.xyz's impressive user count genuine human participation, or is it inflated by airdrop farming accounts ahead of the anticipated TGE? We don't intend to comment on the broader landscape of farming behavior on the exchange. However, analyzing the trade-level data for the four Trade.xyz markets in March reveals a pattern worth presenting.

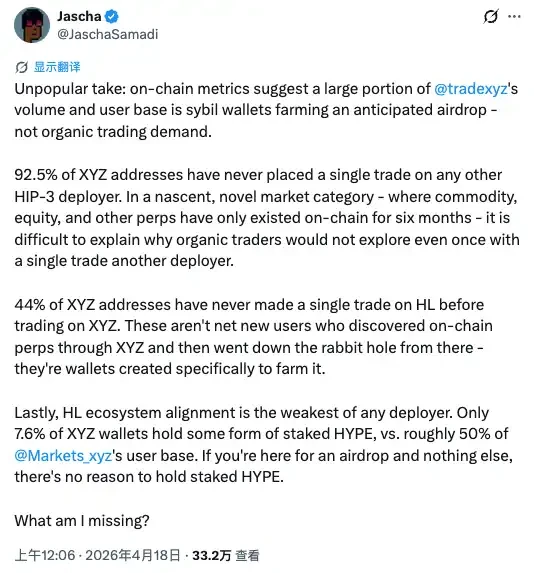

Analyst Jascha noted that 92.5% of XYZ addresses have never traded on any other HIP-3 deployer.

Of the 34,602 wallets classified as airdrop farming accounts, 34,553 (99.9%) can be traced back to a single Polymarket identity named "Themino."

"Themino," a Polymarket identity on Arbitrum, spawned 70 independent linear chains covering 34,553 wallets.

How did it work? Hyperliquid's L1 provides a primitive called `internalTransfer` for moving USDC between wallets, incurring a flat $1 fee regardless of the amount. The operator of Themino used this primitive to pass a seed deposit sequentially through tens of thousands of fresh wallets. Each wallet would execute the same five-step sequence in approximately 26 seconds:

1. Receive $X from the previous farming wallet via `internalTransfer`, losing $1 to the HL transfer fee.

2. Transfer $14 to the xyz sub-account.

3. Execute two IOC orders on xyz:CL – one buy and one sell – generating two fills and some volume.

4. Transfer approximately $13.99 back to the main account (the $0.01 difference accounting for execution slippage and trading fees).

5. Transfer $X minus $1 to the next farming wallet via `internalTransfer`.

The next wallet would then repeat the sequence.

With 34,510 internal transfers in total, Themino lost $34,510 in protocol fees alone. This approach is consistent with his trading history on Polymarket.

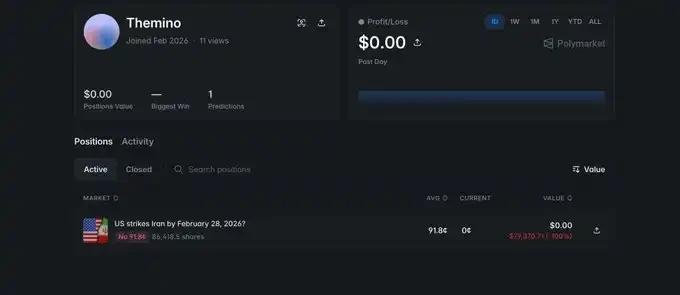

Themino also bet "No" on Polymarket for "Will the US strike Iran before February 28, 2026?", losing approximately $80,000. The strike occurred on February 28.

What are the Builder Types?

Hyperliquid attaches an identifier to orders routed through third-party frontends, allowing these applications to collect custom frontend fees. This identifier is the "builder code" and is the most direct way to determine which interface a wallet used, if any. Among wallets that traded on the four markets, these builders can be broadly categorized into three types.

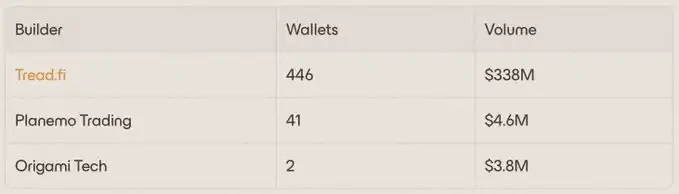

Algorithmic Builders. These are products designed for retail users to maximize trading volume on DEXs, farming potential airdrop points. Before late 2025, farming points on a perpetual DEX meant either wash trading or algorithmically executing non-directional taker-to-taker trades – costly for participants and net-negative for the exchange. Retail market-making bots like @tread_fi, @PlanemoTrading, and @origamitech_ replaced wash trading with genuine market making. Every order placed by these products is post-only, meaning the wallet adds liquidity to the order book rather than consuming it.

As stated by @davidyjeong, CEO of @tread_fi: "Before retail market-making solutions appeared, farming points on perpetual DEXs meant wash trading, inflating volume at the cost of execution fees, slippage, and the risk of account bans. We solved this with a novel farming approach: bots place maker orders on both sides. Users farm points at lower cost, often profiting from captured spreads, and a byproduct is genuine top-of-book liquidity for the market – exactly what HIP-3 equity perpetuals desperately need during nights and weekends when traditional market makers are absent. It's a better way to farm, and it's why HIP-3 markets have excellent execution experiences today."

The contribution of these market-making bots is most evident during periods when traditional market makers are offline. CME WTI futures close on Friday afternoon and reopen on Sunday evening; equity perpetuals face a similar "night and weekend" gap. During these times, retail market-making bots sustain the top-of-book order depth on markets like xyz:CL and xyz:TSLA.

It should be noted: in this analysis, we classify wallets routed through these algorithmic products as Airdrop Farming Accounts. However, their trading behavior and market impact are structurally entirely different from Sybil activity.

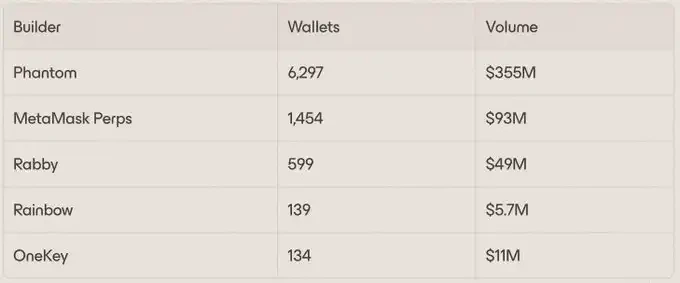

Wallet-Embedded Builders are perpetual contract interfaces embedded within consumer wallets. Since early 2026, this integration type has become one of the largest sources of retail order flow on HIP-3. This group includes @phantom, @MetaMask, @Rabby_io, @rainbowdotme, and @OneKeyHQ. Their median trading volume per wallet ranges between $1,000 and $3,000, consistent with retail users prioritizing ease of use over marginal builder fees.

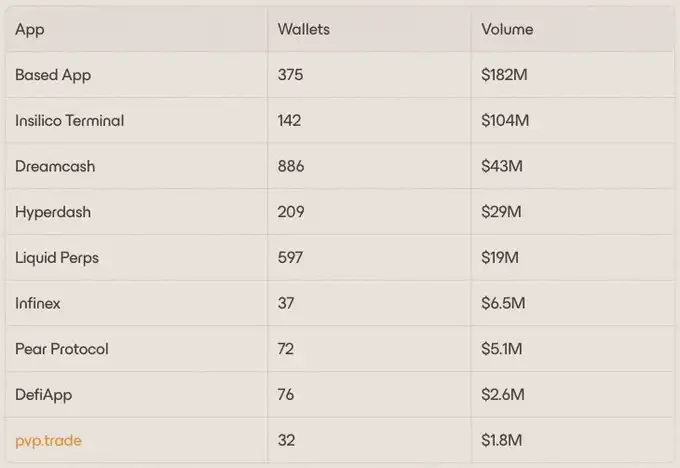

Application Builders are standalone perpetual frontends and integrated products: tools designed for traders, offering specialized workflows for users who find wallet plugins insufficient and need superior order placement, charting, position management, and execution tools. This category has fewer wallets than the Wallet-Embedded type but higher volume per wallet, aligning with advanced users who value functional depth over plug-and-play simplicity. These products include the @InsilicoTrading terminal, @liquidtrading, @hypurrdash, @BasedOneX, @Dreamcash, @infinex, @pear_protocol, @defiapp, and @pvp_dot_trade.

@0xVKTR, Head of Growth at @InsilicoTrading (the team behind the Insilico terminal), describes it: "At Insilico, we see HIP-3 markets as the next step in making real-world exposure native to crypto rails. Traders want more than just another frontend. They want fast execution, clean market access, and the ability to seamlessly move between crypto and macro assets without leaving their existing workflow. Trade.xyz is one of the clearest examples of this demand. The order flow routed through Insilico proves that when a venue has depth, a product is useful, and the experience is built for serious participants, there is a real base of advanced users for on-chain perpetuals."

Who is the Largest Market Maker on Trade.xyz?

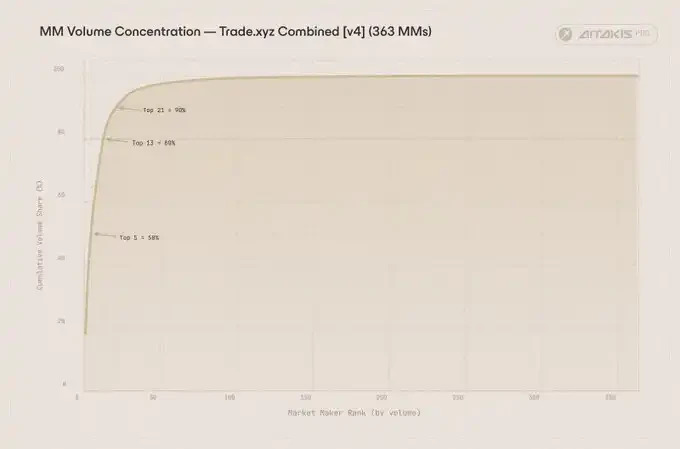

The market-making landscape across Trade.xyz markets is highly concentrated. The top 5 market makers account for 50% of market-making volume, the top 13 for 80%, and the top 21 for 90%. A handful of market-making desks support the vast majority of the exchange's market-making book.

Cumulative share of market-making volume by wallet rank. Top 5 desks account for 50%, top 13 for 80%, and top 21 for 90%.

The second-largest market maker is the most interesting wallet in the entire sample. 0xc926ddba…98d3, with a volume of $4.39 billion and a fill rate of 0.52%, presents a textbook maker profile. Arkham marks this address as "Powell" on Polymarket. One of the largest market makers on Trade.xyz is a Polymarket user running a market-making book across multiple markets on HIP-3.

Other notable market-making desks:

![]()

![]()

![]()

![]()

![]()

![]()