The "biggest negative" for chip stocks has finally arrived? Could Meta be the "first big tech to cut capital expenditure"?

- Core Thesis: Meta's plan to sell excess computing power has shattered the market's belief in "absolute scarcity of compute," marking a shift in the AI investment cycle from a hardware arms race to financial discipline and compute utilization, triggering a sell-off in chip stocks and a rotation of capital towards software and tech giants cutting expenditures.

- Key Elements:

- Meta is forming a new business unit, "Meta Compute," to sell excess compute capacity to external customers via API services or direct leasing, putting it in direct competition with suppliers like CoreWeave.

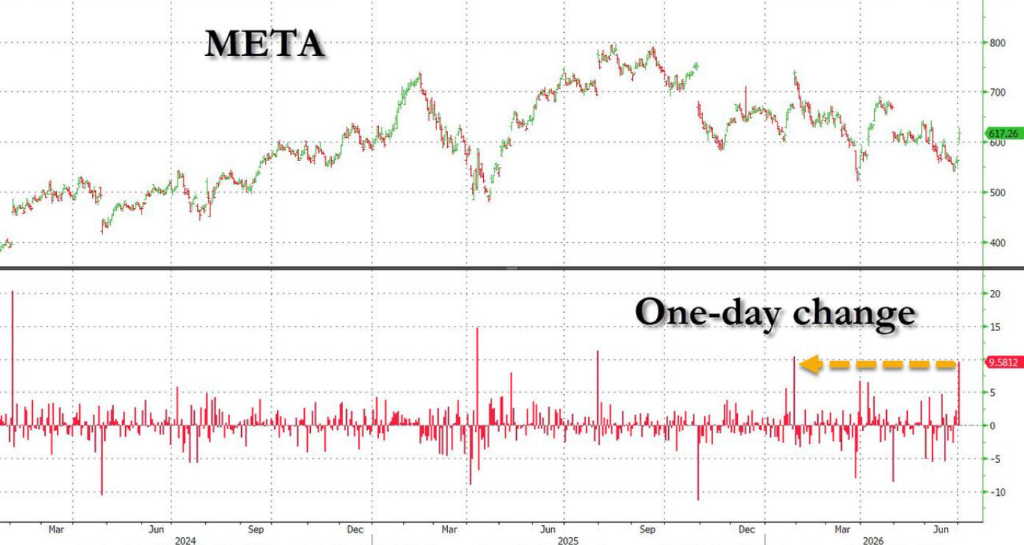

- Reacting to the news, Meta's stock surged 10% in a single day, while chip stocks like Nvidia and Micron, along with emerging cloud service providers, faced a猛烈 sell-off, causing significant volatility in the Nasdaq index.

- Goldman Sachs warns that with the "compute scarcity" narrative upended, the hardware sector will come under pressure first. The AI market is like a "stretched rubber band," and the accumulation of negative signals to a tipping point will trigger a valuation restructuring.

- Momentum trading strategies collapsed, with Goldman Sachs' high-beta momentum basket plunging 9% in a single day, and the long/short high-beta momentum index recording its worst single-day performance since 2020.

- Market focus has shifted to free cash flow stability and financial discipline. UBS notes that this move alleviates concerns over continuously rising capital expenditure, with funds rotating into the software sector.

- The mention of "excess capacity" has sparked concerns about real AI demand. The upcoming earnings season and capital expenditure guidance will be key to whether the valuation revaluation can persist.

- Despite record trading volume, market liquidity is extremely poor. The top-tier liquidity for S&P 500 E-mini futures has plummeted 33% quarter-over-quarter, making large trades prone to triggering sharp volatility.

Original author: Ye Zhen

Original source: Wall Street CN

Meta's plan to sell excess computing power has shattered the market's core belief in the "absolute scarcity of computing power." This strategic pivot has triggered a massive capital outflow from chip stocks, while also marking an inflection point in the market's tolerance for unchecked capital expenditures by tech giants.

The news sparked extreme polarization in the secondary market. Meta, which proactively signaled spending cuts, saw its stock price surge 10% in a single day, its best performance this year. Conversely, traditional AI hardware beneficiaries—semiconductor giants, memory chip manufacturers, and emerging cloud service providers (Neocloud)—suffered heavy losses, dragging the Nasdaq index into significant volatility.

Wall Street institutions generally interpret this as a major narrative shift in the AI investment cycle. The market's focus is rapidly shifting from pure hardware infrastructure buildout toward corporate free cash flow stability and compute utilization rates. Investors are now rewarding tech giants that demonstrate financial discipline with real capital.

This reshaping of the underlying logic not only rewrites the power dynamics between hyperscale cloud providers (Hyperscalers) and chip suppliers but also directly leads to the collapse of crowded momentum trading strategies, injecting new uncertainty into the upcoming earnings season and market liquidity.

Meta Pivots to Sell "Excess Compute," CapEx Inflection Point Looms for Big Tech

According to Bloomberg, Meta is establishing a new business unit to sell its excess computing capacity to external customers for revenue. Sources say potential plans include allowing external access to various AI models hosted on Meta's existing AI infrastructure, similar to AWS's Bedrock service. Meta would be responsible for operating the data centers and chips powering models like Muse and Spark, charging developers for access.

Furthermore, Meta is also considering directly selling "raw" computing power. Ironically, Meta had just signed multi-billion dollar contracts with emerging cloud service providers like CoreWeave and Nebius, and this move now means it will compete directly with its own suppliers.

This internal initiative, named "Meta Compute," aims to build and manage the company's AI infrastructure. The team is co-led by Meta's infrastructure chief Santosh Janardhan, AI executive Daniel Gross from the superintelligence lab, and Meta President Dina Powell McCormick.

In fact, this shift was foreshadowed. Meta CEO Mark Zuckerberg hinted to investors during May's shareholder call that selling excess compute or API services was "definitely on the table." Another company that previously sold excess compute, Space, is now also facing intensified competition in selling its computing capacity.

"Compute Scarcity" Logic Challenged, Chips and Momentum Stocks Hit Hard

Meta's move directly challenges the core premise underpinning the recent surge in chip stocks. Rich Privorotsky, head of Goldman Sachs' 1-Delta trading desk, warned that the market's core premise has been compute scarcity. If supply increases and leasing prices fall, the scarcity narrative is directly overturned, and the hardware sector will feel the pain first.

Goldman Sachs warned that the AI market is like a stretched rubber band, and the market's persistent disregard for negative signals will eventually reach a tipping point. If any major tech giant takes the lead in cutting AI spending, the valuation logic for the entire AI sector will face a complete overhaul. Meanwhile, the rise of low-cost AI models is challenging the existing "high spending for growth" logic.

Reacting to the Meta news, the chip and memory sectors bore the brunt, with star stocks like Nvidia, Micron, and SanDisk experiencing heavy selling. Emerging cloud service providers, seen as the most obvious losers, saw one of their largest single-day percentage declines this year.

The hardware sector crash triggered a wholesale collapse of momentum strategies. Goldman Sachs' high-beta momentum basket (currently composed mainly of chip and memory stocks) plummeted 9% in a single day after reaching historic gains. BTIG analyst Jonathan Krinsky noted that the long-short high-beta momentum index fell 10%, its worst single-day performance since 2020.

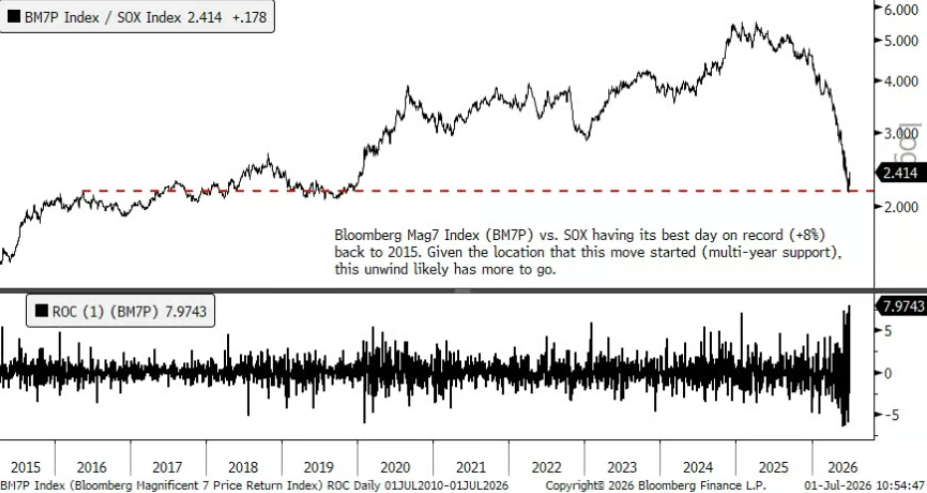

Additionally, the spread between the Bloomberg Mag7 Index and the Philadelphia Semiconductor Index (SOX) hit its largest single-day extreme (+8%) since 2015, indicating a frantic capital exodus from the semiconductor sector.

Market Logic Reshaped, Investors Reward "Spending Cuts"

In stark contrast to the hardware stocks' poor performance, the market assigned a high premium to signals of capital expenditure reduction. As Goldman Sachs previously predicted, the first hyperscaler to signal the ability to slow spending would be rewarded with stock price gains.

Meta's 10% surge confirms this thesis, suggesting investors find incremental revenue streams and financial discipline more attractive than an endless arms race at current valuation multiples.

UBS trader Christina Dwyer stated that the reports shifted the market narrative towards stricter financial discipline, alleviating concerns over continuously rising capital expenditure. CapEx expectations are no longer unilaterally upward-sloping, shifting focus to free cash flow stability.

Amid the capital rotation, the software sector posted its second-largest single-day excess return relative to semiconductors in a year.

Intensified Competition and Liquidity Concerns, Upcoming Earnings as Key Guide

Meta's entry complicates the supply-demand outlook for hyperscalers. While the emergence of a new competitor disrupts the existing landscape, the alleviation of supply chain bottlenecks could also relieve cost pressures.

UBS noted that the mention of "excess capacity" has sparked market concerns about true underlying AI demand. Looking ahead to the upcoming Q2 and Q3 earnings seasons, company guidance and full-year CapEx plans will be crucial in determining whether the current valuation recalibration is sustainable.

It is worth noting that amidst the massive capital rotation, the market faces significant liquidity risks. Goldman Sachs' trading desk warned that despite U.S. stocks reaching their highest average daily volume since 2026, market liquidity remains extremely poor. In June, S&P E-mini futures' top-of-book liquidity plunged 33% month-over-month, from $12 million to just $8 million.