Buy Aave at a 70% Discount? The Misread Rumors Hide Kraken’s Listing Ambitions

- Core Thesis: The rumored Kraken investment in Aave reveals the exchange's strategic shift towards becoming a full-stack financial infrastructure provider, while also highlighting structural questions about value attribution between the AAVE token and company equity. However, Aave's founder denied reports of a discounted transaction.

- Key Elements:

- Kraken reportedly plans to acquire 250,000 AAVE tokens and a 15% stake in Aave Group for approximately $71 million (including 35,000 ETH), valuing the deal at just $385 million – a roughly 70% discount to AAVE's token market capitalization.

- Aave founder Stani clarified that the transaction involves token holdings from Labs, not the protocol layer, and that all protocol revenue flows to the token, denying that AAVE was sold at a 70% discount.

- The value attribution remains unclear: if the protocol's entire value is captured by the token, the specific rights Kraken gains by purchasing equity rather than tokens have not been explicitly explained, bypassing core questions for retail investors.

- Kraken's strategic pivot is evident: building its own Layer 2 (Ink), engaging in a flurry of acquisitions (Bitnomial, Reap, Backed Finance), and securing a Federal Reserve master account, all aimed at constructing full-stack financial infrastructure.

- IPO timeline delayed: Paused in March after Bitcoin dropped to $65,000 and BitGo's share price fell 44% post-listing, but plans to complete by the end of 2026. This investment aims to enrich the narrative for its IPO prospectus.

In the early hours of this morning, a report ignited the DeFi community.

Citing three sources familiar with the matter, CoinDesk reported that cryptocurrency exchange Kraken is in talks to acquire a stake in Aave. The proposed deal structure involves Kraken contributing 35,000 ETH in exchange for 250,000 AAVE tokens plus a 15% equity stake in Aave Group, valuing the entire transaction at approximately $71 million, corresponding to a $385 million valuation. The report also mentioned this is the first of a series of transactions under Payward Asset Management, with plans to syndicate it externally and take a more active role in DeFi and other investment opportunities.

The most eye-catching aspect of this deal is the valuation reached. At $385 million, it's nearly 70% lower than AAVE token's market cap of roughly $1.24 billion. Aave has always emphasized that the protocol's value is entirely captured by the token. So what exactly is Kraken buying with its cash for a 15% equity stake? If all value is supposed to flow to the AAVE token, why does Kraken need a board seat?

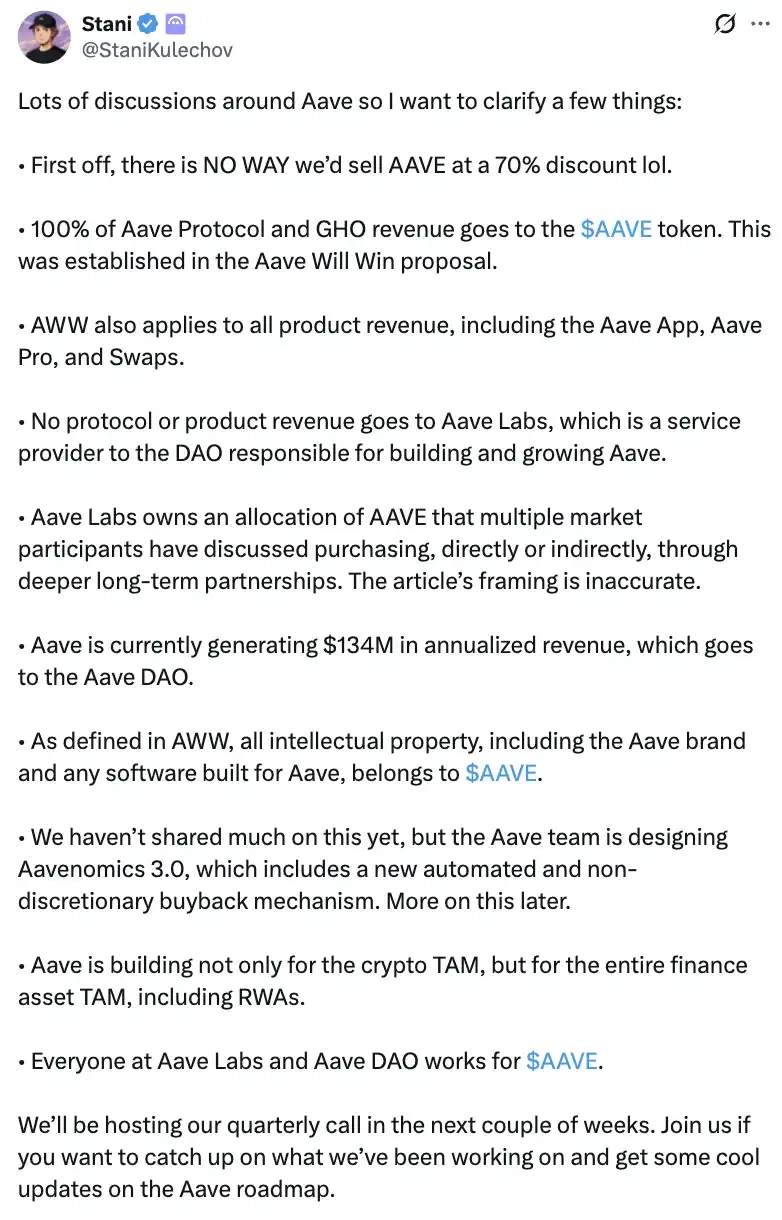

A few hours later, Aave founder Stani Kulechov stepped in to clarify.

He refuted the report's framework point by point. Aave Labs would never sell AAVE at a 70% discount; what was being discussed was a portion of the AAVE held by Labs itself, negotiated by "multiple market participants through deeper long-term partnerships," unrelated to the protocol level. He emphasized that all revenue from the Aave protocol and the GHO stablecoin flows to the AAVE token, a rule established by the "Aave Will Win" proposal, which also includes revenues from products like Aave App, Aave Pro, and Swaps; Aave Labs is merely a service provider to the DAO and receives no share of protocol revenue.

Stani also revealed that the team is designing Aavenomics 3.0, which will introduce an automated, non-discretionary buyback mechanism.

According to his account, what was being sold wasn't discounted AAVE; CoinDesk's comparison of the equity deal's total value to a single token's market cap was fundamentally flawed.

If Stani's version is accurate, CoinDesk's report was indeed misleading.

However, Stani didn't answer the retail investor's original question. If the protocol's value indeed resides entirely in the token, what exactly is Kraken buying with its 15% stake in Aave Group? He sidestepped this point. The question of value attribution between equity and tokens remains unresolved.

The deal's details remain pending, and Kraken has not officially commented on the report.

But their motivation is clear. CoinDesk noted that Kraken's parent company, Payward, characterized this transaction as "the opening move in a series of asset management operations." A company preparing for an IPO is making its stake in a DeFi leader a signature move.

Over the past year and a half, Kraken has taken new actions almost every quarter, advancing on three fronts simultaneously.

First, building infrastructure.

Kraken incubated its own L2, "Ink," attempting to replicate the path taken by Binance and Coinbase by funneling CEX users on-chain for lending and trading. The most active protocol on Ink is the Perp DEX "Nado," offering unified margin accounts for spot, margin, and perpetuals, attracting real users with its points program and airdrop expectations.

Second, strategic acquisitions.

Kraken's acquisitions over the past year and a half have been intense: $550 million for derivatives exchange Bitnomial, acquiring its full set of CFTC licenses for brokerage, clearing, and exchange; $600 million for stablecoin payment company Reap, adding card issuance and cross-border settlement capabilities; purchasing Backed Finance, behind the tokenized stock protocol xStock s, late last year; and acquiring token management platform Magna this February.

Third, regulatory identity.

In March of this year, Kraken became the first digital asset bank in the US to receive a master account from the Federal Reserve, allowing it to settle dollars directly on the Fedwire system without needing an intermediary bank. That same month, Nasdaq announced a partnership with Kraken to build a framework for tokenizing stocks, preserving issuer control and shareholder voting and dividend rights. A crypto exchange is donning the identity of traditional finance.

Kraken is transforming from a crypto exchange into a full-stack financial infrastructure company.

The IPO is a primary driver behind all these strategic moves. Last November, Payward raised $800 million at a $20 billion valuation, a 30% increase in valuation within two months. The investor list included Citadel Securities, Jane Street, and Apollo Global Management.

Viewed through this lens, Kraken's desire to invest in Aave becomes understandable—it's extending its narrative of "being able to handle any financial business" directly into DeFi. Acquiring a stake in a leading protocol is much faster than building a lending protocol from scratch and fits well into the growth narrative for its prospectus.

However, Kraken's IPO path hasn't been smooth.

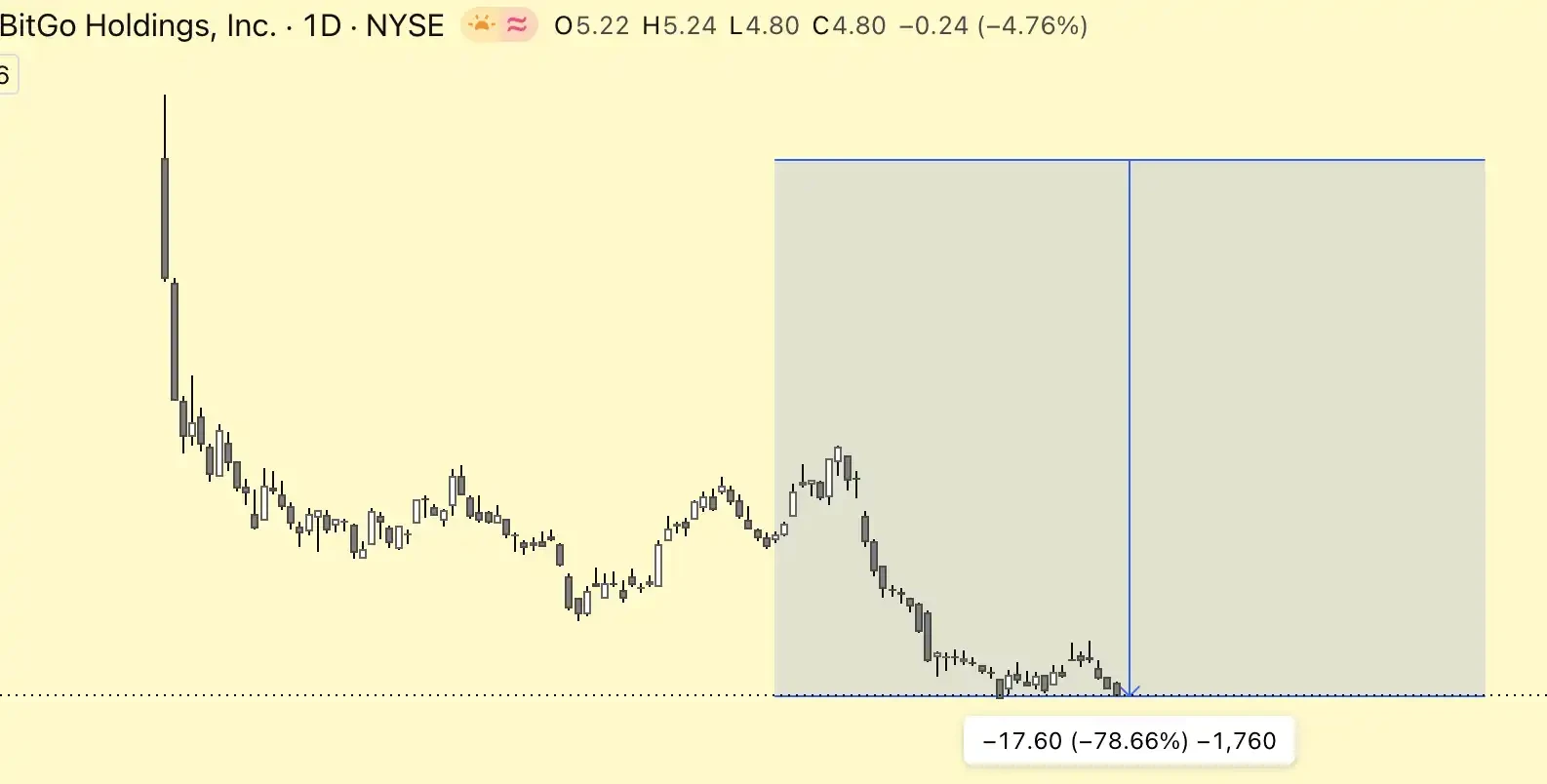

On March 18th of this year, Kraken's IPO was put on hold. The core reason was the bleak market conditions, with Bitcoin falling from $126,000 last October to around $65,000, wiping out over a trillion dollars in market value. BitGo, which went public earlier, was the only digital asset company listed in 2026, and its stock price dropped 44% after listing—a stark cautionary tale for everyone.

Market tastes are also changing—2025 saw at least 11 crypto IPOs raising a total of $14.6 billion, but 2026 started much colder, with advisors saying investors are now scrutinizing financial infrastructure targets much more carefully, re-evaluating factors like regulatory maturity, recurring revenue, and resilience. Just one month before the IPO was paused, Kraken replaced its CFO of only 16 months, handing the responsibilities to a newly promoted Deputy CFO. Changing a financial leader at the eleventh hour is a red flag for a company undergoing due diligence.

However, a pause doesn't mean a withdrawal.

This May, reports emerged that Payward was raising a new round of funding at a $20 billion valuation, and Co-CEO Arjun Sethi has repeatedly stated in recent months that the company's goal is to complete its IPO by the end of 2026. It's foreseeable that Kraken may act even more frequently in the coming months, adding weight to the valuation in its prospectus.

The rumored investment in Aave is just the latest step. Whether this deal closes and what exactly the 15% equity stake buys will likely remain unclear until the S-1 filing is made public, providing a written answer.