Micron Earnings Preview: Amidst the Turmoil in Korean and US Tech Stocks, How Can We Secure the Storage Bull Market?

- Core Thesis: Micron Technology's upcoming earnings report is not just a test of quarterly performance, but a stress test for the entire AI storage bull market thesis. The core contradiction lies in market expectations being pushed to extreme highs. Micron must prove that the supply-demand gap is far from over and it can continuously raise guidance; otherwise, it risks triggering significant stock price volatility that could ripple through the entire industry chain.

- Key Factors:

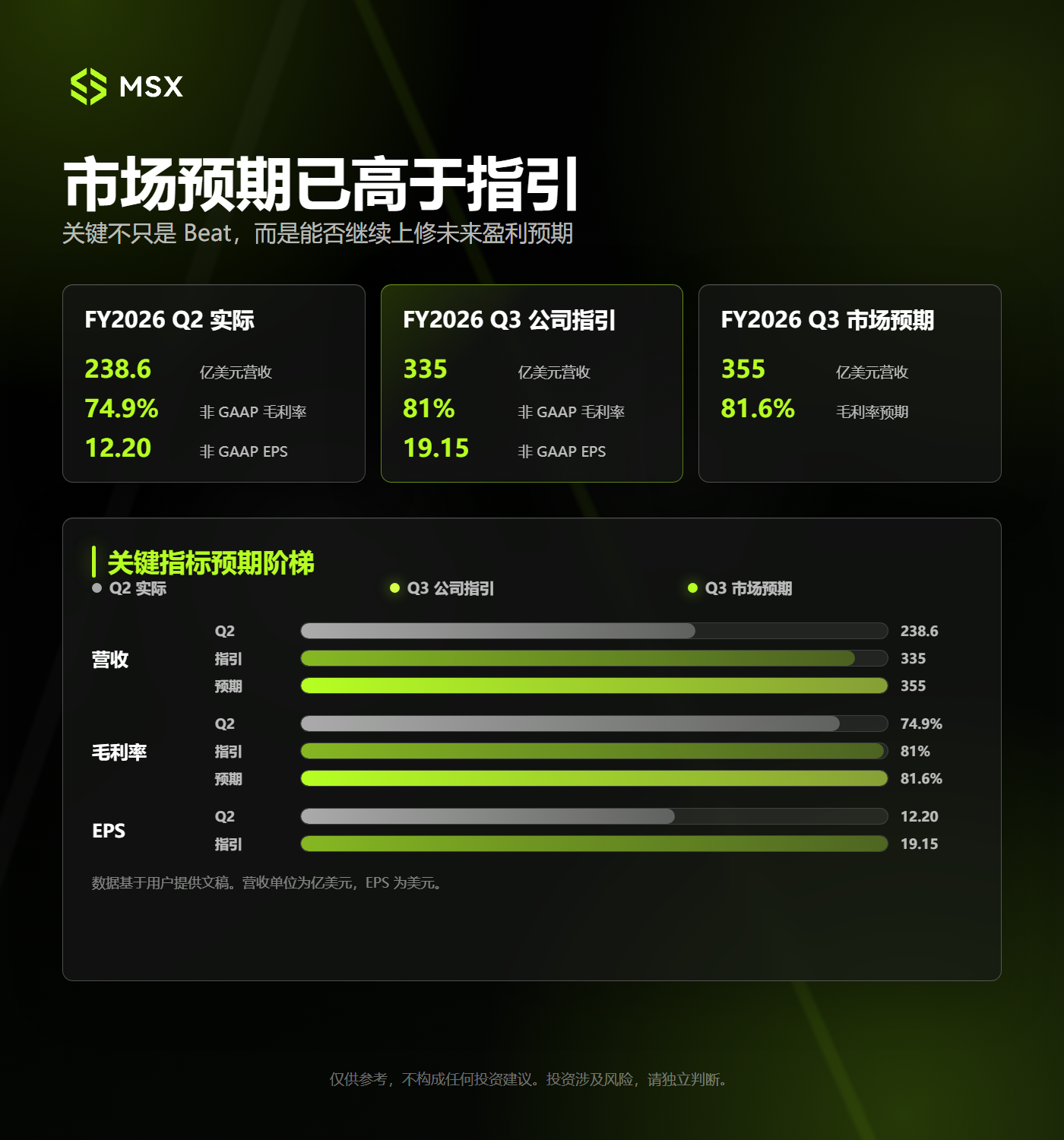

- Significant Gap Between Market Expectations and Company Guidance: Market expectations for Micron's Q3 revenue have already reached $35.5 billion, exceeding the company's prior guidance of $33.5 billion. This requires the company to not only beat guidance but also surpass already highly bullish consensus estimates.

- Sustainability of HBM Supply and Demand Becomes Focal Point: Micron must clearly articulate HBM4 yield progress, order locking status for 2027, and the depth of collaboration with clients like Nvidia during its earnings call, to prove that the high prosperity reflects structural growth rather than a short-term product cycle.

- Whether Ultra-High Gross Margins (approximately 81% guided for Q3) Are Sustainable: The market will focus on management's description of future gross margin trends. A conservative outlook could undermine the high-valuation thesis, potentially triggering a "Sell the News" event.

- When Will Supply Fill the Demand Gap? The market is watching the ramp-up pace of new capacity. If supply enters the market faster than AI demand grows, the storage industry could revert to price competition. Micron needs to demonstrate that demand growth still outpaces supply.

- Options-Implied Volatility Reaches 13%: The market is already pricing in a double-digit stock price swing post-earnings, reflecting high divergence and overcrowded trading risks among current capital focused on the storage theme.

On June 23, from the Korean stock market to US stocks, global tech assets experienced a sharp sentiment cooldown.

Starting in the Asian session, the KOSPI index fell nearly 10% in a single day, with both Samsung Electronics and SK Hynix dropping over 12%, triggering a temporary market-wide trading halt. The sell-off sentiment quickly spread to US stocks in the evening, with AI and memory assets—the strongest performers over the past year—becoming the epicenter of the global tech stock correction.

Paradoxically, this market turmoil coincided with Micron Technology's upcoming Q3 FY2026 earnings report, due after the market close on June 24—a rather delicate timing.

On one hand, global AI memory stocks are retreating collectively, prompting the market to reassess high valuations and crowded trades. On the other hand, Micron is about to deliver a highly anticipated report card. The combination of these factors means this earnings report's significance transcends a single company's quarterly results, acting more like a concentrated stress test for the entire memory narrative.

After all, the core drivers propelling global memory stocks—soaring HBM demand, DRAM and NAND price increases, persistent supply constraints, and rapidly climbing gross margins—all require renewed confidence. This leads to a more direct question: With stock prices and market expectations already elevated, can Micron still deliver answers that exceed imagination?

In other words, a "results in line with expectations" may no longer suffice. What the market truly awaits is whether Micron can revise its guidance upward again, proving the supply-demand gap in AI memory is far from closing.

1. Why is This Micron Earnings Report So Crucial?

Looking at last quarter's data, Micron's fundamentals can hardly be described with a simple "beat expectations."

In Q2 of FY2026, Micron reported revenue of $23.86 billion, nearly tripling year-over-year. Non-GAAP gross margin rose to 74.9%, and non-GAAP EPS reached $12.20, both setting company records.

More importantly, Micron's guidance for Q3 was aggressive: projected revenue of $33.5 billion, non-GAAP gross margin of approximately 81%, and non-GAAP EPS of $19.15.

But the capital market's appetite has risen even faster than the company's guidance. Currently, the consensus market expectation for Micron's Q3 revenue has reached approximately $35.5 billion, exceeding the upper end of the company's previous guidance range. Gross margin expectations hover around 81.6%, indicating the market has already priced in another earnings beat.

This creates the major paradox of this report: Micron's results must not only beat the company's guidance but also surpass an already very optimistic market expectation.

Therefore, this report is not just about whether revenue and EPS "beat." It's crucial to observe if the market is willing to continue upward revisions of earnings estimates for coming quarters. Simply put, if the report is just "moderately good," it might not be enough. But if it's strong enough to prompt further guidance upgrades, yesterday's decline could turn out to be a pre-earnings shakeout.

After all, for a high-expectation stock that has already rallied significantly, the most dangerous situation is often not poor performance, but decent performance that isn't good enough to justify even higher valuations.

This is precisely the pricing environment Micron currently faces.

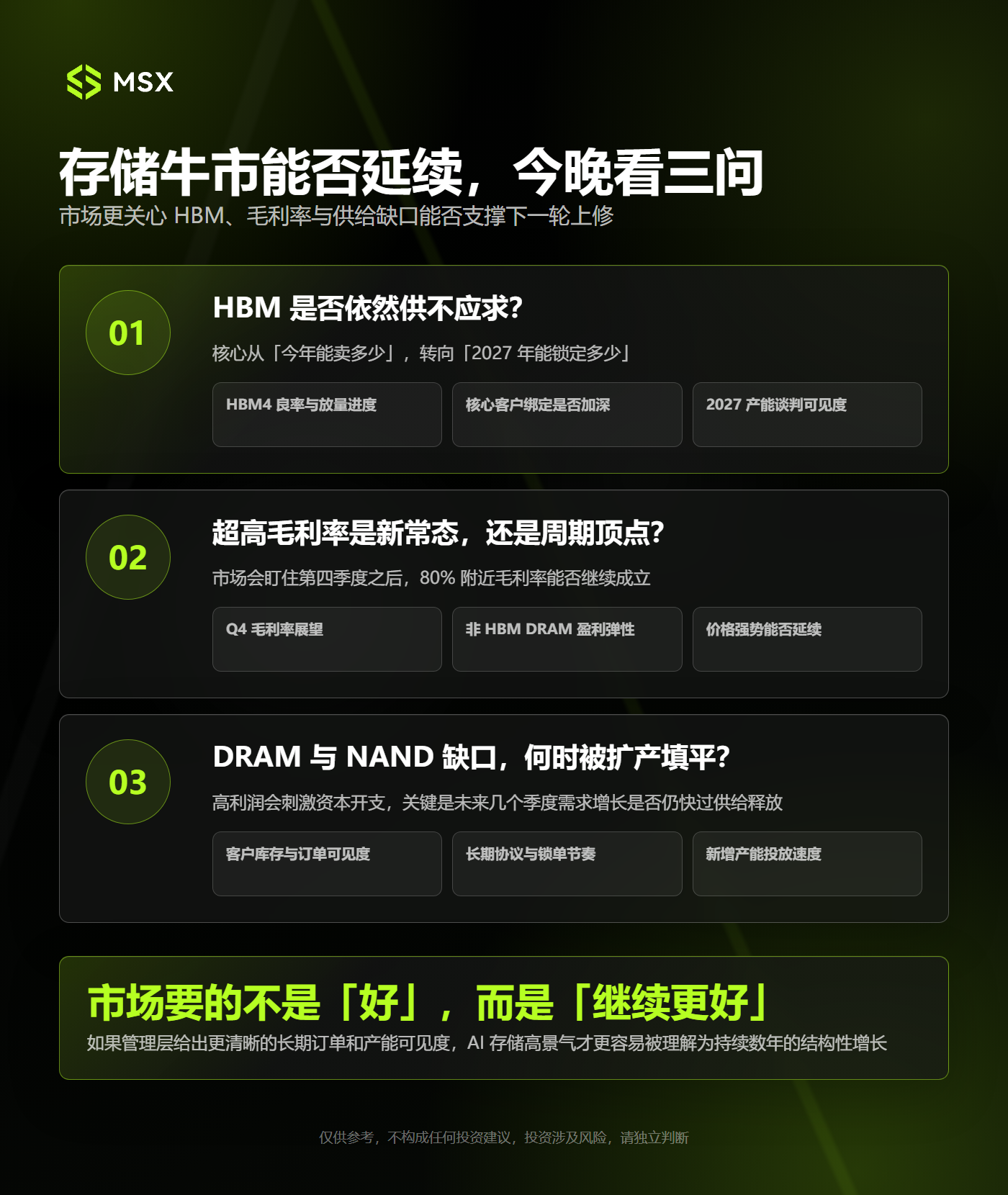

2. Can the Memory Bull Run Continue? Tonight, We Watch Three Issues

1. Is HBM Still in Short Supply?

Micron's core growth narrative remains HBM.

As is widely known, AI servers need more than just GPUs. With the computing power,功耗, and data throughput of individual AI accelerators continuously increasing, HBM has evolved from a standard supporting component into a critical factor determining the performance of the entire AI system.

Micron has already begun ramping up HBM4 production and shipments, supplying NVIDIA's new Vera Rubin platform. HBM capacity for 2026 is largely accounted for. Therefore, the market's focus will shift from "how much can be sold this year" to "how much can be locked in for 2027."

During the earnings call, investors will likely seek answers to several questions: Are HBM4 yields and volume ramp progressing as expected? Is the alignment with core customers deepening? How advanced are the capacity negotiations for 2027? Can subsequent products like HBM4E further close the gap with SK Hynix?

If Micron can provide clearer visibility on long-term orders and capacity, the market will be more inclined to view the current HBM boom as sustained structural growth lasting several years, rather than a product cycle nearing its peak.

Conversely, if management's language regarding 2027 demand and orders is vague, the market may begin to suspect that the period of tightest HBM supply and strongest pricing power has already been priced in by the stock.

2. Is the Ultra-High Gross Margin a New Normal or a Cyclical Peak?

For Micron, profit elasticity stems not just from shipment volume but also from pricing and gross margins.

Recall that last quarter, Micron's non-GAAP gross margin reached 74.9%, with Q3 guidance around 81%. This means for every $100 in revenue, Micron expects to retain over $80 in gross profit.

Such high gross margins are uncommon in past memory cycles. This is driven by a combination of factors: a higher mix of high-value products like HBM, broad-based DRAM and NAND price increases, supply constraints, and a product mix increasingly skewed toward data centers.

Notably, HBM isn't the sole driver of Micron's margin expansion. Management previously indicated that profitability for some non-HBM DRAM products is also very strong, sometimes exceeding HBM. This suggests the current memory upcycle is no longer confined to a niche high-end segment but is spreading across the broader DRAM market.

Therefore, the most important aspect of this report isn't just whether the gross margin hits 81%, but how management describes the trend for Q4 and beyond.

If Micron provides another outlook exceeding 80%, it signals robust supply-demand gaps and continued price increases, potentially leading to another upward revision of the earnings power. However, if the gross margin merely meets guidance or management's tone on future margins becomes cautious, the stock could face a "Sell the News" reaction.

3. When Will the DRAM and NAND Gaps Be Filled by Capacity Expansion?

Every memory bull market eventually returns to the same question: When will supply catch up with demand?

The current cycle has persistently exceeded expectations for two reasons. First, AI data centers are fueling rapid demand for HBM, server DRAM, and enterprise SSDs. Second, memory production capacity cannot be brought online simultaneously in the short term.

HBM production, in particular, consumes more wafer and advanced packaging resources. As manufacturers shift capacity toward HBM, it inevitably constrains the supply of traditional DRAM to some extent, driving up prices across the entire product line.

Micron previously stated that in the medium term, it can only meet about one-half to two-thirds of customer demand, while some new fabs will not contribute meaningful output until much later. This implies, in the near term, new capacity is unlikely to quickly fill the supply-demand gap.

However, the market will also focus on the other side. Attracted by high profits, Micron, Samsung, and SK Hynix are all increasing capital expenditures. If new capacity ramps faster than AI demand growth, the memory industry could revert to its traditional cycle of price competition and inventory correction.

Thus, in this call, management's commentary on customer inventories, order visibility, long-term agreements, and the pace of new capacity deployment will likely be more important than single-quarter shipment numbers. The focus will be on whether Micron can demonstrate that demand growth continues to outpace supply release, at least for the next few quarters.

3. 13% Implied Volatility in Options: What is the Market Betting On?

Beyond fundamentals, the options market has already provided another perspective.

Based on options pricing around the close on June 22, the combined price of near-the-money Call and Put contracts expiring June 26 was approximately $159. Relative to Micron's stock price of roughly $1,211 at the time, the options market implied an earnings-related move of about 13%.

This means that buying options now requires Micron's stock to move over 13% post-earnings to cover the premium cost. For stock holders, this signals that a double-digit gap move after the report should not be surprising.

In other words, the options market is pricing in not a small move, but a very significant reaction to the earnings.

More importantly, the high implied volatility itself reflects the current market divergence: some funds believe AI memory is still in the early stages of supply shortage, while others worry that the stock price has already discounted too much future growth.

From a post-earnings scenario perspective, the MSX Research Institute identifies three likely possibilities:

Scenario 1: Earnings Beat, Guidance Revised Upward

This is the most ideal outcome.

If Micron beats current market expectations on revenue, EPS, and gross margin, provides strong Q4 guidance, and reiterates smooth HBM4 ramping, improved 2027 order visibility, and robust DRAM/NAND pricing, the logic of the memory bull market would be further confirmed.

In this case, a Micron rally could re-energize the entire memory supply chain, including SanDisk, Western Digital, Samsung, SK Hynix, and certain semiconductor equipment and AI server related names.

However, even with strong results, be wary of profit-taking at elevated levels. As mentioned, the options market has already priced in significant volatility. A surge after-hours does not guarantee a sustained upward move the following trading day.

Scenario 2: Good Results, But No Better Guidance

This is perhaps the riskiest scenario for this report.

Micron could easily deliver a record-breaking report. But if the figures merely confirm previous guidance, or if the Q4 gross margin and revenue outlook are not revised upward, the market may still choose to sell.

This isn't because Micron's fundamentals suddenly deteriorated, but because the market has already priced in a "beat." Ultimately, for stocks at high levels with high crowding, meeting expectations can sometimes equate to falling short of expectations.

The recent turmoil in the Korean market amplifies this risk. On June 22, South Korean regulators publicly reflected on the swift approval of leveraged single-stock ETFs for Samsung and SK Hynix. A day later, the KOSPI index crashed nearly 10%, with both memory giants falling over 12%.

This correction may not signify a reversal in long-term AI memory demand. However, it serves as a stark reminder that when high valuations, leveraged capital, and crowded trades converge on one theme, any information falling short of expectations can be rapidly amplified.

Therefore, the decline in Korean memory stocks feels like a stress test ahead of Micron's earnings: If Micron is strong enough, it can restore market confidence. If Micron is merely "normally good," the Korean market correction could be interpreted as a signal that the memory trade is beginning to cool.

Scenario 3: Gross Margin or Forward Guidance Falls Short

If Micron reports significantly below expectations in areas like HBM4 progress, gross margins, product pricing, or Q4 guidance, the stock could face significant downward pressure.

The reason is that Micron's current stock price embodies at least three layers of expectations:

- Layer 1: Long-term memory demand driven by AI computing expansion.

- Layer 2: A price upcycle fueled by tight DRAM and NAND supply-demand dynamics.

- Layer 3: Micron's continued improvement in market share and profitability within the high-end HBM segment.

If any of these layers weakens, the market could simultaneously lower future earnings forecasts and valuation multiples. The impact would not be limited to Micron but could spread across the entire memory and AI hardware supply chain.

Conclusion

Based on currently available information, Micron's long-term narrative remains intact.

AI servers continue consuming more HBM and DRAM, data center SSD demand is growing steadily, and the traditional NAND market is recovering. New production capacity is unlikely to be rapidly deployed in the short term, and supply constraints still afford memory manufacturers strong pricing power.

However, strong fundamentals do not mean the stock is without risk.

When revenue, profit margins, and stock prices have repeatedly set records, the market's yardstick for Micron inevitably shifts: Previously, it just needed to prove the industry was recovering. Now, it must demonstrate that this boom can not only continue but also be stronger than investors have already anticipated.

Therefore, the true suspense of this earnings report is not whether Micron can deliver another good set of results, but whether it can elevate the market's imagination of the future.

In a nutshell, Micron no longer needs to prove that the memory bull market is still ongoing. It needs to prove that the end of this bull market is still further away than where the market is currently pricing it.