The Epicenter of the Global Chip Stock Rout: "Various Horror Stories" Behind the South Korean Market Crash

- Core Thesis: The crash in South Korea's stock market triggered panic across the global semiconductor sector, but its root cause is not a sudden fundamental deterioration. Instead, it is a confluence of technically overextended positions, minor shifts in industry expectations, and a series of panic-inducing policy rumors, leading to mechanical selling driven by algorithmic trading, leveraged liquidations, and institutional rebalancing.

- Key Factors:

- South Korea's KOSPI index plunged 10% in a single day, triggering a circuit breaker. Samsung Electronics and SK Hynix slumped over 12%, accounting for more than 70% of the index's decline. Panic spread to US markets, dragging Micron Technology down 13%.

- Reports that SK Hynix is considering slowing the expansion of HBM4 production, alongside downward revisions in production forecasts for Nvidia's next-generation chips, have shaken expectations for AI hardware demand and the profit structure of the memory chip industry.

- Policy rumors surfaced about South Korea discussing a tax on unrealized stock gains, coupled with the country's failure to be included in the MSCI Developed Markets list. This prompted anticipatory selling by investors, amplifying policy uncertainty.

- Leveraged ETFs generated a "negative gamma" effect, where market declines beget heavier selling pressure. The total size of South Korea's leveraged ETFs is approximately $300 billion, prompting regulators to warn of the side effects and consider tightening measures.

- Retail investors' margin loan balance reached a record 38.5 trillion Korean won, triggering forced liquidations in the afternoon. The National Pension Service, having exceeded its position limits, was a net seller of $1.5 billion in June, transforming a traditional market stabilizer into a major source of selling pressure.

- Escalating global macro pressure: expectations for a Federal Reserve rate cut are cooling, and market focus is shifting to Micron Technology's earnings report as a test of the true AI industry cycle's sentiment and valuation support.

Original Author: Ye Zhen

Source: Wall Street CN

A severe sell-off in the South Korean stock market is evolving into a storm sweeping across the global semiconductor sector. This crash is not solely driven by deteriorating fundamentals, but is the result of a confluence of technical overextension, adjusted industry expectations, and panic triggered by a series of policy rumors.

On Tuesday, the Korea Composite Stock Price Index (KOSPI), a bellwether for the global memory chip industry, plunged 10% in a single day, triggering a circuit breaker. Index heavyweights Samsung Electronics and SK Hynix both tumbled over 12%, with the two giants collectively accounting for more than 70% of the index's decline. Panic quickly spread to global markets, directly impacting the US semiconductor supply chain. Micron Technology closed down 13%, and Western Digital plummeted 8.5%.

The immediate trigger for this selling frenzy was a confluence of dense negative news.

Reports from South Korean media suggesting SK Hynix might slow down the expansion of advanced AI memory chip production severely shook market expectations for AI hardware demand. Simultaneously, domestic policy discussions in South Korea regarding taxing unrealized stock gains, along with regulatory warnings about overheated leveraged ETFs, completely shattered the market's fragile confidence.

Analysts point out that this extreme volatility was more driven by mechanical selling from algorithmic trading, forced liquidations of retail leveraged funds, and institutional rebalancing, rather than an instantaneous deterioration of fundamentals. Amidst multiple pressures, global investors are closely watching the upcoming Micron Technology earnings report to assess the true health and valuation support of the AI supply chain.

Horror Story One: HBM Expansion Slowdown and NVIDIA Order Cut Concerns

The direct cause of fundamental concerns was a marginal shift in the supply chain strategy for high-end memory chips.

As previously mentioned by Wall Street CN, SK Hynix is considering slowing down the production ramp-up for its sixth-generation High Bandwidth Memory (HBM4), postponing some production line conversions, and reallocating resources towards general-purpose DRAM.

The logic behind this strategic adjustment lies in the reversal of product profit margins.

Currently, the profit margin for general-purpose DRAM is 15% higher than that of HBM, and Daishin Securities expects the operating profit margin for general-purpose DRAM to peak at 90% within the year. Furthermore, media reports, citing sources, indicate that production forecasts for NVIDIA's next-generation "Rubin" chip are being lowered, fueling speculation that tight HBM supply and soaring AI demand expectations might be waning.

This concern is also reflected at the macro industry chain level.

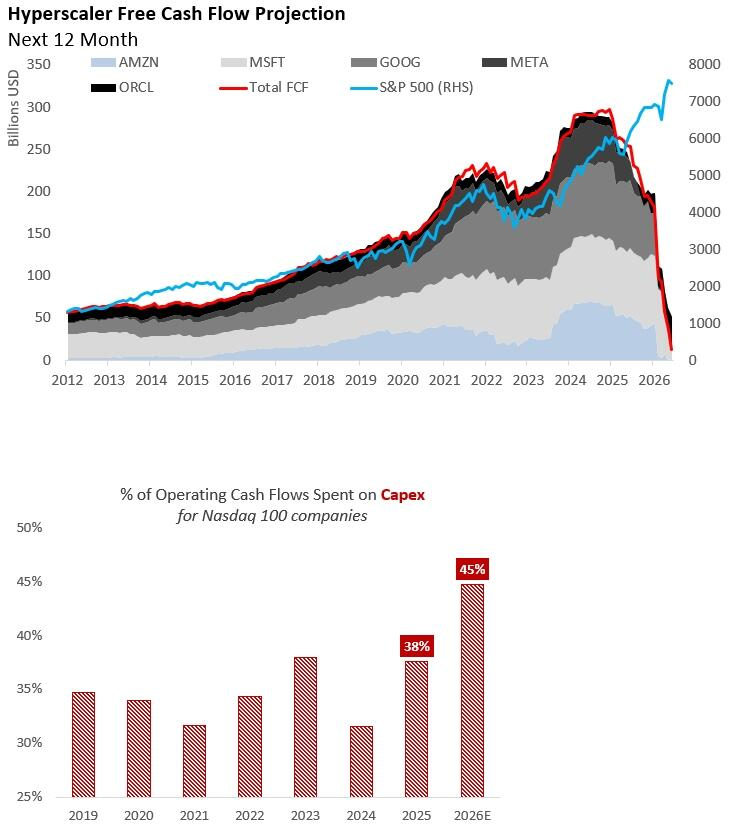

As hyperscale data center operators face surging capital expenditures and expectations of negative free cash flow, the market is beginning to question whether these tech giants, acting as the "source of funds," might scale back hardware procurement budgets, thereby constraining revenue across the entire memory, chip, networking, and server supply chain.

Horror Story Two: Policy and Tax 'Black Swan', Panic over Unrealized Gains Tax

Amidst diverging industry fundamentals, a discussion document on tax reform sparked significant恐慌 in South Korea.

According to Yonhap News Agency, multi-party lawmakers in South Korea jointly held a tax reform forum, advocating for a shift towards "comprehensive income taxation," i.e., exploring the inclusion of "unrealized gains" (paper appreciation) from assets like stocks and real estate into the tax system.

Although the proposal includes gradual paths like tax deferrals, it acted as a major negative catalyst for the already high-valuation South Korean stock market. Experts warned that while taxing only upon realization creates a "lock-in effect," the mere expectation of taxing unrealized gains directly prompted investors to sell preemptively before the policy materializes.

Furthermore, South Korea's failure to be included in the MSCI Developed Markets (DM) watch list, along with the South Korean President's recent comments expressing concerns about the stock market volatility's "wealth effect," further exacerbated policy uncertainty.

Horror Story Three: Leveraged ETFs and the 'Negative Gamma' Feedback Loop

From a quantitative and technical perspective, this crash was a classic structural collapse.

According to ZeroHedge, Nomura quant strategist Charlie McElligott noted that massive capital inflows into single-stock and memory-themed leveraged ETFs created a huge "real and synthetic" Negative Gamma effect.

This market structure led to pro-cyclical and mechanical capital flows—the more the market fell, the heavier the selling pressure. Charlie McElligott pointed out that during the sell-off, 0-DTE options traders aggressively shorted rallies, completely dismantling any attempted buying pressure. Coupled with options dealers adjusting their positions built up during the prior rally, this further exacerbated the systemic downward spiral.

This effect means that as the market declines, market makers and ETF managers must mechanically sell more stocks to maintain risk exposure balance. Chris Cha, Head of Korea High-Touch Trading at Goldman Sachs, disclosed in a report that the size of onshore leveraged ETFs in South Korea has reached $9.1 billion, while offshore leveraged ETFs tracking SK Hynix and Samsung have reached a massive $21 billion.

The shift in attitude from South Korean financial regulators worsened the technical picture. The head of the Financial Supervisory Service (FSS) publicly expressed regret over failing to prevent the listing of single-stock leveraged ETFs linked to Samsung and SK Hynix, warning that their side effects were intensifying. Discussions about tightening margin loan requirements and limiting ETF issuance directly undermined the technical buying that had underpinned the recent rally.

Horror Story Four: Liquidity Drain, Retail Liquidations, and Pension Fund Shift

The crash revealed the extreme singularity of the buying structure in the South Korean stock market.

Alexander Redman, Chief Equity Strategist at CLSA Singapore, pointed out that the rally in the South Korean market was almost entirely retail-driven, with a concerning level of inherent froth. This month, retail margin balances in South Korea hit a record high of 38.5 trillion won (approximately $25 billion). Seoul fund manager Kim Namho stated that the massive margin debt triggered forced liquidations in the afternoon, accelerating the market's freefall.

Meanwhile, the traditional stabilizer became a primary seller.

A Goldman Sachs report indicated that due to the previous stock market surge, the domestic equity allocation of the National Pension Service (NPS) exceeded its 28.8% upper limit. To rebalance its assets, NPS recorded its largest net selling ($1.5 billion) in June since April 2021.

When the pension fund shifted from passive support to mechanical supply, combined with foreign capital exiting, the marginal liquidity in the market dried up instantly.

External Macro Pressure: Cooling Rate Cut Hopes and Earnings Test

While South Korea's domestic fundamentals and technicals are both pointing downwards, variables in the global macro environment have also exacerbated market fragility.

Unexpectedly revived expectations of a Fed rate hike are systematically suppressing high-valuation tech stocks. Aditya Bhave, an analyst at Bank of America, predicts the Fed will resume rate hikes in September, October, and December of this year, totaling 75 basis points, to combat sticky services inflation and wage growth.

Following the extreme market turbulence, investors' attention is focused on Micron Technology's upcoming earnings report. Goldman Sachs notes that market expectations heading into Micron's earnings had been driven to very high levels, providing motivation for profit-taking. Dilin Wu, a strategist at Pepperstone Group, stated that Micron's report card will be the real test of the sustainability of the AI hardware investment boom.

As CLSA strategist Alexander Redman noted, the magnitude of this volatility is closely tied to the market's inherent retail-driven nature and degree of froth. Although the medium-term upcycle for memory chips and the AI demand thesis are not yet disproven, under the shock of forced deleveraging and multiple rumors, global chip stocks are undergoing a painful period of expectation reset and valuation digestion.