U.S. CPI Preview: Headline Inflation May Exceed 4%, Hitting a Three-Year High, While Core Inflation Could Miss Expectations Significantly

- Key Insight: Driven by surging energy prices, the U.S. headline CPI for May may break through 4%, reaching a three-year high. However, due to cooling components such as housing and auto insurance, the month-over-month increase in core inflation could be significantly lower than the market consensus, indicating a marked divergence between the two.

- Key Factors:

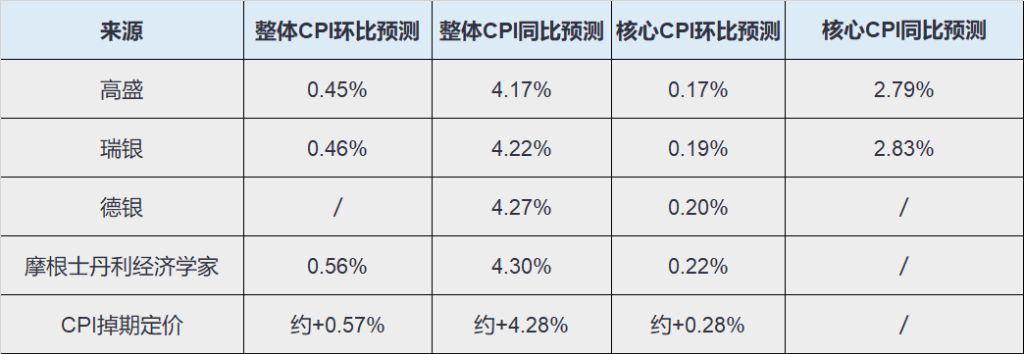

- Five major investment banks project the year-over-year headline CPI for May to be in the range of 4.17% to 4.3%, all higher than March’s 3.81%. Energy is the primary driver, with its year-over-year increase potentially approaching 24%.

- Month-over-month core CPI forecasts range from just 0.17% to 0.22%, significantly below the market expectation of 0.27% to 0.30%. This is mainly attributed to a slowdown in housing rents (with Owners' Equivalent Rent increasing only ~0.22% month-over-month) and an expected decline in auto insurance prices.

- Gasoline prices have already peaked and subsided since May 20. UBS anticipates this will lead to a sequential decline of approximately 0.13% in the June headline CPI, suggesting May may represent the cycle's peak for inflation.

- The cooling in core inflation is not broad-based. Airline ticket prices are projected to rise 1.3%-2% month-over-month due to higher fuel costs, while IT goods and certain service prices continue to face upward pressures.

- Inflation swap market pricing (4.27%-4.28%) implies a 0.48 standard deviation upside surprise for the U.S. dollar. Historical analysis suggests such deviations typically lead to the DXY index rising approximately 0.14% within one hour of the data release.

Original Author: Long Yue

Original Source: Wall Street Insight

At 20:30 Beijing time tonight, the U.S. Bureau of Labor Statistics will release the May CPI data. This is also the most closely watched inflation data before Fed Chair Walsh's next policy rate meeting next week.

According to information from the trading desk, four major Wall Street institutions—Goldman Sachs, UBS, Deutsche Bank, and Morgan Stanley—have released dense forward-looking reports on the eve of the data release. The four agencies' forecasts vary but are directionally similar: Headline inflation may be high, but core inflation may not be as hot. Energy prices push the headline CPI up, while rents, car insurance, and other factors drag core CPI down.

Headline CPI May Surge Past 4% to a Three-Year High, Core CPI Could Be Below Consensus

In terms of forecasts, the four institutions' predictions for May's year-over-year headline CPI are concentrated in the 4.17%-4.3% range, all higher than April's 3.81%. However, their month-over-month core CPI forecasts are generally lower than the market consensus.

The trends of headline inflation and core inflation show a clear divergence.

The "worrying" part is headline inflation. The year-over-year forecasts from Goldman Sachs, UBS, Deutsche Bank, and Morgan Stanley are all above 4%. Deutsche Bank's estimate of 4.27% and Morgan Stanley's estimate of 4.3% are 46-49 basis points higher than April and would be the highest since April 2023.

The "good" part is core inflation. Excluding food and energy, month-over-month core CPI might be only 0.17%-0.22%, significantly lower than the mainstream market expectation of 0.27%-0.30%.

Headline Inflation May Break 4%: Energy is the "Culprit"

Energy will be the core driver behind this potential inflation jump.

Following the outbreak of the Iran war, U.S. retail gasoline prices rose sharply, driving energy commodity prices up an estimated ~6%-7% month-over-month in May, with the entire energy category increasing by nearly 4% month-over-month. This effect directly pushed the year-over-year headline CPI from 3.81% in April to 4.17%-4.3% in May.

Deutsche Bank's calculations show that year-over-year energy inflation could be approaching 24%; in February, this figure was only 0.5%.

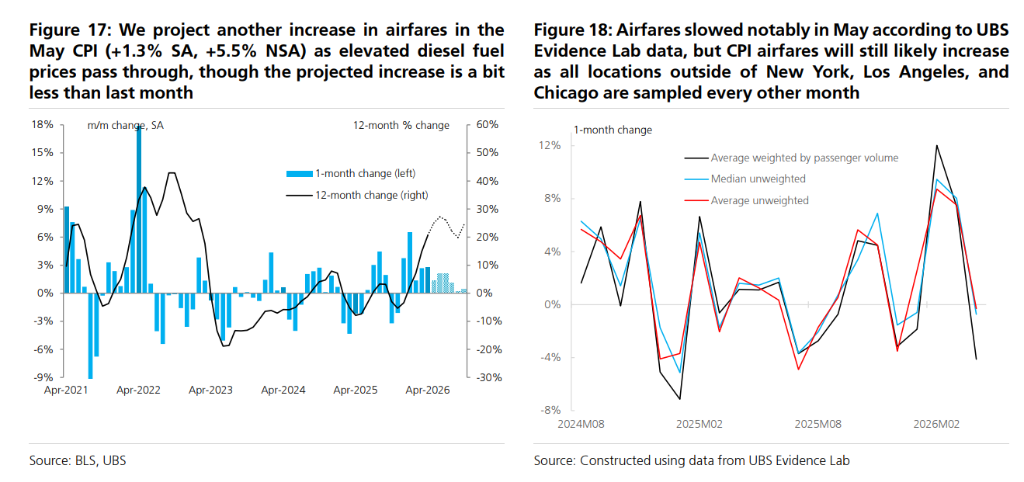

Airline ticket price increases are one of the most direct transmission chains. Rising fuel costs directly increase airline operating costs, with ticket prices expected to rise between 1.3% and 2% month-over-month in May.

The good news is that gasoline prices have fallen by about 40 cents per gallon since peaking on May 20th. UBS expects this will lead to a decrease in the June headline CPI by about 0.13% month-over-month, bringing the year-over-year figure back to around 3.81%. In other words, May is likely the peak of this round of headline inflation.

Why Core Inflation Might Be Lower Than Expected: The Key Lies in Housing Cooling Down Again

Core CPI excludes food and energy. Precisely because it removes these two hottest components, the May core data will appear much milder.

Housing carries a significant weight in the U.S. CPI, approximately 35%.

Goldman Sachs and UBS both forecast that Owners' Equivalent Rent (OER) and Rent of Primary Residence will increase by about 0.22%-0.23% month-over-month in May, continuing a slowing trend. In April, these two components rose by 0.53% and 0.55%, respectively. Deutsche Bank also cites "housing inflation trend remaining moderate" as one of the reasons for the soft core inflation reading.

Due to the large weight of OER, even a drop from around 0.5% to just over 0.2% will significantly drag down the core CPI reading.

Car insurance is another cooling factor.

Goldman Sachs expects motor vehicle insurance prices to fall 0.1% month-over-month in May. Its online data model suggests that premium changes signal downside pressure on the car insurance CPI component. Deutsche Bank also mentioned that car insurance is expected to be weak again.

Used cars also show no significant upward pressure. Goldman Sachs expects used car prices to be flat and new car prices to rise by 0.1%; UBS expects used car prices to fall by 0.26% and new car prices to fall by 0.10%.

This means that the factors that have frequently disturbed U.S. core inflation in recent years—housing, car insurance, and used cars—are not sending strong inflationary signals this time. In other words, the relatively low May core CPI is not simply due to one component "suddenly cooling down."

Not All Core Inflation Is Cooling: Airfare, IT Goods, and Some Services Still Under Pressure

Core CPI being below consensus does not mean all core components are cooling.

Airline tickets are an upward component.

Goldman Sachs expects airfare prices to rise 2% in May. UBS expects a 1.34% increase. This is because jet fuel prices remained high for much of May and may continue to pass through to ticket prices.

There is significant divergence in forecasts for hotel prices. Goldman Sachs expects hotels to rise 0.2%; UBS, based on Smith Travel Research (STR) data, lowered its lodging forecast, expecting out-of-home accommodation prices to fall 0.77%. However, UBS also notes that CPI tracks prices at the time of booking, while STR data is closer to prices at the time of stay. This time lag could pose upside risk, potentially reflecting World Cup-related demand in advance.

There is also stickiness in goods.

UBS expects core goods prices to rise 0.08% month-over-month, between March's 0.11% and April's 0.03%. Its assessment is that the impact of tariffs on 12-month core goods inflation may have passed its peak, but residual transmission will still cause monthly core goods prices to maintain slight positive growth for the remainder of the year.

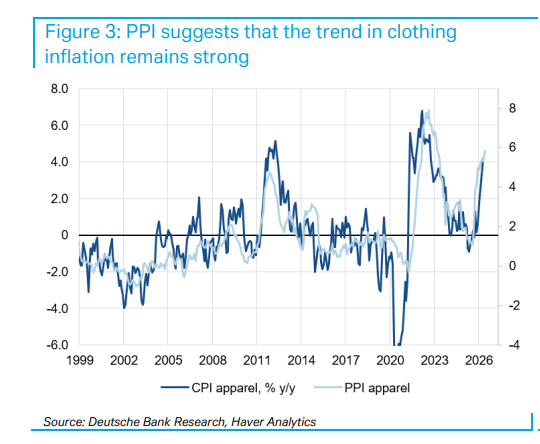

Deutsche Bank also noted that import prices suggest IT goods prices still have strong momentum, partly due to high global memory chip prices. At the same time, apparel PPI indicates a still-strong inflation trend in clothing, although import prices are weak, suggesting CPI momentum may slow compared to previous months.

The services components are more complex.

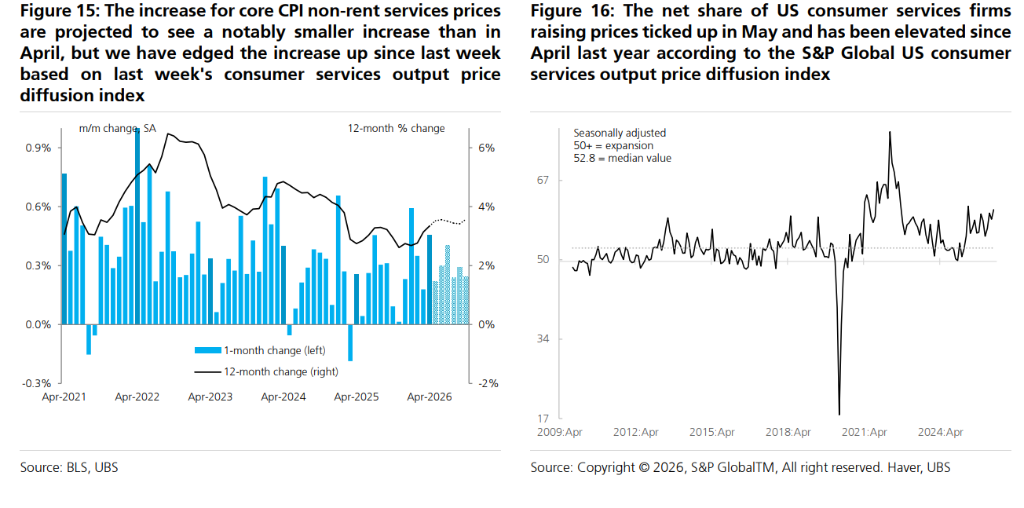

UBS revised its forecast for non-shelter core services prices up from 0.17% to 0.21%. This is because the S&P Global U.S. Consumer Services Output Price Diffusion Index shows that the proportion of consumer services companies raising prices in May increased, reaching the second-highest level since 2009, excluding pandemic anomalies.

What to Really Watch Tonight: More Than Just a Headline Inflation Above 4%

The headline number for May CPI might look high, but what's underneath is more critical.

If the headline CPI is high, mainly driven by gasoline and energy, the market may judge its sustainability based on the decline in gasoline prices in June.

If the core CPI is significantly below expectations, the market will look deeper to see where the disinflation is coming from: is it a trend of slowing housing, or a one-off seasonal drag?

If airfare, IT goods, and non-shelter services remain strong, the quality of the core cooling will be discounted.

So, this CPI report may simultaneously tell the market two stories:

On one hand, headline inflation breaks above 4% again, possibly hitting its highest level since April 2023.

On the other hand, core inflation might be only around 0.2%, significantly below the market consensus.

This is precisely what makes tonight's CPI data difficult to trade: the headline inflation looks hot, but core inflation may not be as hot; oil prices push the headline up, while housing and car insurance drag the core down.

Inflation Swap Pricing: Market Bets on a Dollar Upside Surprise

The interest rate swap market currently prices the May headline CPI at 4.27%-4.28%, slightly higher than the Bloomberg survey median of 4.2%.

Analysis framework from Morgan Stanley strategist Molly Nickolin shows that inflation swap pricing correctly predicted the direction of year-over-year inflation in 9 out of the last 12 releases before the CPI data. Current pricing implies an upside deviation of about 0.48 standard deviations relative to economist expectations.

Based on historical backtesting, a 0.48 standard deviation upside surprise typically corresponds to the DXY dollar index rising by approximately 0.14% within one hour of the release. Among all G10 currencies, the Swedish Krona (SEK) tends to perform the weakest on "dollar-bullish" CPI release days, showing the largest average decline.

Looking Ahead: Oil Prices Are the Biggest Variable for the Inflation Path

The trend of core CPI in the coming months depends on how long oil prices persist.

The current baseline forecast is for month-over-month core CPI to remain around 0.2%. However, if the Middle East situation continues and the decline in oil prices falls short of expectations, upside risks become more pronounced – high oil prices not only directly boost energy prices but also continue to permeate core inflation through intermediate channels like airfare and transportation.

Deutsche Bank's longer-term forecast is more pessimistic: even if oil prices begin to fall in June, year-over-year energy inflation is expected to remain above 10% until early 2027 before turning negative. Core services inflation (excluding rent/OER) is also expected to remain above 3% for an extended period.